Preliminary Results

Summary by AI BETAClose X

The Artisanal Spirits Company plc

("The Artisanal Spirits Company", "ASC" or "the Group")

Preliminary Results for the year ended 31 December 2025

FY25 results in line, start to the year in line with expectations

The Artisanal Spirits Company (AIM: ART), the creator of outstanding, limited-edition whiskies and experiences around the world, and owner of The Scotch Malt Whisky Society ("SMWS"), Single Cask Nation ("SCN"), J.G. Thomson and Artisan Casks, announces Preliminary Results for the year ended 31 December 2025 ("FY25").

Against a backdrop of subdued consumer demand due to global economic and political uncertainty, ASC continued to make strategic progress and delivered a mixed but resilient year-on-year performance across the Group, notwithstanding the previously announced disruption caused by the US government shut down and the strategic change to Route-To-Market (RTM) in the US in Q4, which directly impacted revenue and EBITDA.

As a result, the Group delivered an adjusted EBITDA loss of £1.9m. This reflects the impact of the US government shutdown and US RTM change which resulted in an inability to complete anticipated US shipments in Q4 2025 equating to around £1.8m of EBITDA and also a provision for US stock expected to be transferred to the SMWS America at the end of March from our current 3-tier partner of £0.8m. Excluding the Americas region, the Group saw a £0.4 million (c2%) decline in revenue.

From FY26, the US RTM will report in-market depletions as opposed to shipments to the US further aligning revenue and cash and improving efficiency and speed to market for new initiatives. Additionally, this change will generate cost savings of c$1m (£0.75m) over three years.

|

£'m |

12 months to 31 December 2025 Reported |

12 months to 31 December 2025 Adjusted1 |

12 months to 31 December 2024 |

USA Government Shutdown Impact2 |

USA Stock Transfer 3 |

|

Revenue |

19.9 |

19.9 |

23.6 |

(2.4) |

(1.1) |

|

EBITDA |

(2.4) |

(1.9) |

1.1 |

(1.8) |

(0.8) |

|

Loss before tax |

(7.0) |

(6.5) |

(3.1) |

(1.8) |

(0.8) |

1 Adjusted EBITDA defined as earnings before interest tax, depreciation, amortisation and non-recurring costs. The non-recurring cost in the year being the £0.5m operational expense in January 2025 with our previous partner to take more direct management of the US RTM

2 Anticipated impact of government shutdown - shipments bottled and planned prior to closure which could not ship due to the inability to receive required COLA approval to import

3 Impact of stock to be transferred at the end of the contract with our previous partner, at the end of March 2026, as we change our RTM partner in the US market

Financial Headlines

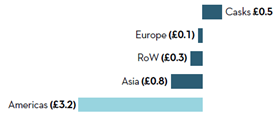

· Continued effective revenue diversification, with revenue growth in cask sales (+13%), Venues (+8%) and Single Cask Nation (+10%) mitigating a 25% decline in Asia, where continued market and economic headwinds remain. The Asian region for ASC is now around 50% of the size it was in 2022, significantly impacted by economic headwinds in China over the period; however, we remain well placed in the Asian market for when improvement in market sentiment returns.

· Cost management and efficiencies delivered a further £0.3m of recurring savings in the year (excluding the non-recurring US operational expense of (£0.5m)) - notably marketing cost per acquisition down around 1/3 year in year delivering growth in recruitment from a lower spend.

· An organisational redesign completed in Q4 2025 will realise circa £0.9m of gross savings in FY 2026.

· EBITDA loss of £2.4m (2024: £1.1m profit), being a loss of £1.9m at an adjusted level reflecting the £0.5m operational expense in January 2025 as part of the US RTM strategic change.

· Loss before tax of £7.0m (2024: (£3.1m)), primarily due to the US operational impacts.

· Cask stock holding with NBV of £28.3m (2024: £27.8m), which when independently appraised in July 2024 was valued at £102m and a 2026 bank valuation, on average, of 200% of NBV.

· Successfully completed the RCF refinancing with Santander (September 2025), representing an increased facility of £13.5m at a 20bps lower headline margin rate and no financial covenants, with a 4-year term.

|

£'m |

Note |

12 months to 31 December 2025 |

12 months to 31 December 2024 |

|

Revenue |

6 |

19.9 |

23.6 |

|

Gross profit |

|

11.3 |

15.0 |

|

Gross margin |

|

57% |

64% |

|

EBITDA |

7 |

(2.4) |

1.1 |

|

Adj. EBITDA |

7 |

(1.9) |

n/a |

|

Loss before tax |

7 |

(7.0) |

(3.1) |

|

Loss after tax |

|

(7.2) |

(3.3) |

|

Net Debt** |

|

(31.5) |

(25.5) |

|

Cask inventory |

15 |

28.3 |

27.8 |

|

Cask inventory valuation*** |

|

n/a |

102.0 |

* Adjusted EBITDA defined as earnings before interest tax, depreciation, amortisation and non-recurring costs

** Net debt defined as current and non-current financial liabilities less cash and cash equivalents per the Statement of Financial Position, less interest accrued on inventory financing.

*** Cask inventory valuation based on an independent valuation completed by sector experts in July 2024.

Operational Headlines

· Underlying membership was maintained in the year: UK increased 1%, offset by 1% decline in Asia; Growth in China and Japan of 2% and 5% respectively, was offset by decline in Taiwan of 20%.

|

Global Membership |

|

|

|

|

|

|

Dec 2025 |

Dec 2024 underlying* |

% Change |

Dec 2024 reported |

|

Europe |

24,700 |

24,400 |

1% |

27,400 |

|

Americas |

8,100 |

8,000 |

- |

8,000 |

|

Asia |

5,200 |

5,500 |

(1%) |

5,500 |

|

Other |

1,700 |

1,800 |

(1%) |

1,800 |

|

Total |

39,700 |

39,700 |

- |

42,700 |

* Underlying membership excludes the c3,000 members who joined in Nov 24 on a complimentary basis (where engagement has been exceptionally low)

· Product innovation continued at pace: Following the launch of the Creators' Collection in 2024 and rapid expansion of our Heresy range, we introduced our newly defined flavour profiles as part of our refreshed Signature range in Q4 2025, enhancing the messaging and storytelling of the range, and representing a unique and differentiated offering within the wider whisky industry. Member engagement is strong with regard to innovations with a number of bottlings selling out within hours or days.

· In July 2025 we unveiled our newest ASC brand 'Artisan Casks' - a new luxury private cask programme, enabling private individuals the chance to purchase an individual cask to appreciate and enjoy the artisanal nature of whisky, with early achievement of sales in 2026 building on H2-25 delivery.

· We announced new franchise agreements in India and Vietnam, both of which are in the top 15 Ultra-Premium Scotch Whisky markets for volume and value (IWSR 2024), as we look to build a presence in those geographies.

· Another year of growth in our UK Venues, up 8%, further evidence of our members valuing the in-person experience on offer in our SMWS UK members rooms.

Current Trading/Post Period Highlights

· The start to the year has been solid, FY26 guidance remaining unchanged, with trading in line with expectations. Cask sales growth alongside year-on-year revenue improvements in Asia and America are offsetting a slower start in Europe where consumer confidence remains subdued.

· The change to the US RTM, which will take effect from April 2026, allows us to take more direct involvement in boosting member engagement and brand awareness that will drive membership, revenue and EBITDA growth.

· The Group holds no direct exposure to the current conflict in the Middle East, given we do not sell directly to any of those key geographies. Any impact would be more indirect, relating to associated inflationary pressures and consumer confidence.

Andrew Dane, CEO of Artisanal Spirits Company, commented:

"Despite persistent macroeconomic and complex geopolitical challenges, as well as the previously announced US operational disruption at the end of the year, ASC continues to manage the factors within its control well. We made good strategic progress in 2025, demonstrating the strength of our brands, the depth of our expertise and our ability to pivot and evolve.

"The operational platform we have in place, combined with our cost base efficiency, more direct control over our US operations and increasingly diversified revenue streams, positions us well to benefit as market conditions improve. 2025 saw us further consolidate our presence in key Asian markets in India and Vietnam, and SMWS continued to progress, underpinned by a loyal, global membership base with around 70% member retention, demonstrating the enduring appeal of our unique single cask and small batch spirits.

"Looking ahead, we continue to focus on delivering exceptional and unique whisky, growing our membership and deepening member engagement. We will continue to expand in international markets where the appreciation for premium spirits and experiential brands is growing, as well as diversifying our revenue portfolio, through the likes of Single Cask Nation and the growth in trade cask sales to strengthen our future profit delivery.

"While mindful of near-term uncertainties, we remain confident in the strength of our brands, assets, strategy and medium-term opportunity."

30 March 2026

Sellside analyst presentation

Andrew Dane, Chief Executive Officer, and Billy McCarter, Chief Financial Officer, will host an in-person presentation for sellside equity analysts today at 09.00 hours GMT.

Analysts wishing to join should register their interest by contacting: artisanalspirts@teamlewis.com.

A recording of the presentation will also be made available via the Group's website later today.

Investor Meet Company presentation

Andrew Dane, Chief Executive Officer, and Billy McCarter, Chief Financial Officer, will host a virtual presentation on Thursday 2 April at 10.30 hours GMT.

Investors can sign up to Investor Meet Company for free and add to meet The Artisanal Spirits Company via: https://www.investormeetcompany.com/the-artisanal-spirits-company-plc/register-investor

Investors who already follow The Artisanal Spirits Company on the Investor Meet Company platform will automatically be invited.

For further enquiries:

|

The Artisanal Spirits Company plc Andrew Dane, Chief Executive Officer Billy McCarter, Chief Financial Officer |

https://artisanal-spirits.com/link/P3D5By

|

|

Panmure Liberum Limited (Nominated Adviser and Broker) Dru Danford Edward Thomas John More

|

Tel: +44 (0)20 3100 2222

|

|

Team Lewis (Financial PR) Justine Warren Hannah Scott

|

Tel: +44 (0)20 7802 2617 / 2634 |

About The Artisanal Spirits Company

ASC's purpose is to captivate a global community of whisky adventurers, by creating and selling outstanding, limited-edition whiskies and experiences around the world, with an ambition to create a high quality, highly profitable and cash generative, premium global business.

Based in Edinburgh, ASC owns The Scotch Malt Whisky Society (SMWS), Single Cask Nation (SCN), J.G.Thomson (JGT) and Artisan Casks. Owning over 18,000 casks primarily comprising Single Malt Scotch Whisky, ASC's stock includes outstanding whisky (and other spirits) from 100 different distilleries across 20 countries which is sold to members both as individual bottles and whole casks.

With an established global presence in some 30 countries, SMWS operates a direct-to-consumer model (90% of revenue) primarily through e-commerce, in addition to four member rooms in the UK. SMWS provides members with inspiring experiences, content and exclusive access to a vast and unique range of outstanding, expertly curated Scotch malt and other whiskies.

In January 2024, ASC acquired SCN which sources, curates and bottles single-cask whiskies and other spirits selling both online and via traditional retail channels to its following of over 10,000 whisky enthusiasts in the USA.SCN also retails to key international whisky markets around the world.

Launched in the UK in late 2021, JGT has a focus on outstanding small batch blended malt whiskies and other spirits, available both through direct-to-consumer online sales and through traditional retail channels. The award-winning brand has subsequently expanded into international markets.

In July 2025, ASC launched Artisan Casks, a luxury private cask programme allowing private individuals the chance to purchase an individual cask of a quality that allows for immediate bottling and joining a select network with a discerning appreciation for finest craftsmanship and luxury experiences.

With proven e-commerce reach and a growing family of brands, ASC is building a portfolio of limited-edition and small-batch whisky and other spirits brands for a global movement of discerning consumers - predominantly from outside the UK, with an expanding presence in the other key global whisky markets including USA, China, Europe, Japan, Australia and Taiwan.

ASC has a substantial asset backing and is delivering profitable growth and cash generation.

Chair's Statement

Introduction

2025 has been a mixed year for the Group, as we navigated a challenging economic and political backdrop and initiated a significant change to our US route-to-market.

Artisanal Spirits celebrated its 10th anniversary in March 2025 and as I reflect on the past 12 months, I am encouraged that, in the face of significant headwinds, the Group has continued to build on its Scotch Malt Whisky Society (SMWS) foundations, achieving strategic progress, engaging the 40,000 members of the SMWS and spearheading award-winning innovation, whilst remaining true to our core purpose of delivering exceptional whisky experiences.

We recognise the frustration due to the full year profit downgrade caused by the USA government shutdown which led to the cancellation of shipments to the USA prior to Christmas. This issue did allow us to accelerate fundamental changes to our USA route-to-market which incurred an additional, but smaller than anticipated, non cash financial impact while enabling material cost savings in future years. The Board would like to thank shareholders for their patience and continuing support.

ASC post IPO

Despite a persistently challenging market and economic backdrop, over the five years since our IPO, we have successfully grown and diversified the business with measured cost and investment management and a disciplined, strategic approach.

A significant milestone was achieved in 2024 with our first full year of positive EBITDA since listing, a testament to the team's focus on our strategic priorities and operational efficiencies.

We have further expanded our international footprint, most recently building on our presence in key Asian markets with the establishment of franchises in India and Vietnam. In the USA, we acquired Single Cask Nation in early 2024 and then at the end of 2025 we made a fundamental change to our route-to-market in the country giving more direct control of our operations.

Our strategic delivery has included a move into a clear and structured cask sales programme, as we realise value from the surplus stocks we hold, an opportunity which we later extended to private individuals with the launch of the luxury private cask programme, Artisan Casks.

The opening of our own supply chain facility in Masterton has been another transformative step, enabling us to become fully self-sufficient in bottling and dispatch, enhancing our operational resilience.

We have invested in our whisky stock to the point where we now own over 18,000 casks, primarily comprising Single Malt Scotch Whisky, but including outstanding whisky from 100 different distilleries across 20 countries. As a result, the cask spirit asset base has grown over 50% over the last five years, at a Net Book Value (NBV) level and, from an independent valuation performed in 2024, has an inherent market value of over 3x NBV[1].

Collectively, these steps since IPO have supported a circa 40 percent increase in SMWS membership numbers and an over 50 percent increase in Group revenues in 2024 (2025 revenues impacted by significant one-off US impacts) compared to 2020, demonstrating the strength and adaptability of our business model and positioning us for future profitable growth.

2025 performance and progress

In 2025 the Group delivered a resilient year-on-year performance, in spite of the significant impact of the cancelled shipments relating to the US government shutdown and accelerated USA route-to-market changes alongside ongoing macroeconomic uncertainty and associated weaker consumer demand for premium and luxury spirits globally. SMWS has continued to evolve, underpinned by a loyal, global membership base with around 70% member retention. This year, underlying membership was broadly maintained, with record underlying recruitment in the UK and China and increasing member engagement across Europe, a testament to the enduring appeal of our unique single cask and small batch spirits.

In the past year, we welcomed new franchise partnerships in India and Vietnam, building on our previous successes in Taiwan and South Korea. Whilst entry into the Indian market is expected to deliver marginal returns initially, we believe the future growth potential is a key long-term opportunity for the business as the Indian whisky market further develops and there is an expected reduction in tariffs in 2026 from 150% to 75%, dropping to 40% over 10 years.

In the USA, we are initiating important changes to our route-to-market in line with our strategy to take more direct management of our US operations over time, as we continue to take steps to reduce the potential impact of any tariffs. The US government shutdown in the latter part of 2025 caused a delay to anticipated shipments at the end of FY25 which were entirely out of the Company's control and which alongside the change to RTM and associated operational expense had a one-off impact on the reported results for FY25 of £3.5 million of revenue and £3.1 million of EBITDA. Importantly, this will have no impact on in-market operations.

To commemorate the 10th anniversary of The Artisanal Spirits Company in March 2025 we released 260 bottles of a limited-edition 10-year-old bourbon-cask single malt Scotch whisky, for Spirited shareholders to purchase exclusively. We supplemented this with the introduction of a new, enhanced Spirited shareholders benefits programme, offering additional benefits for existing members who hold at least 1,000 shares, as well as a new tier of benefits to those who hold at least 5,000 shares.

Product innovation remains at the heart of our offering. In 2025, SMWS continued to delight members with a diverse range of single cask and small batch releases. Following on from the launch of the Creators' Collection in 2024, towards the end of 2025 we released the new Signature range, enhancing the messaging and storytelling of the range, and representing a unique and differentiated offering within the wider whisky industry. This was underpinned by the simplification of the SMWS flavour profiles ensuring that members can easily navigate the portfolio. Our focus on quality and exclusivity has ensured strong demand for our bottlings and reinforced our reputation for creativity and excellence.

Sustainability continues to be a key pillar of our strategy. We have maintained our commitment to responsible sourcing, efficient operations, and reducing our environmental impact, in line with the Scotch Whisky Association's Sustainability Strategy.

Celebrating continued industry recognition

Once again, the quality of our spirits was recognised by many awards from the top competitions around the world. Among those, SMWS won five medals at The Spirits Business Scotch Whisky Masters, seven medals in the International Spirits Challenge and four awards from the International Wine and Spirits Competition.

Single Cask Nation retained the honour of Independent Bottler of the Year in 2025 at the World of Whiskies awards.

Solid performance against a challenging backdrop

The Group faced a challenging situation in 2025, with significant cost inflation in addition to difficult economic, political and market conditions. In particular, market conditions in Asia were a major driver of the gap to prior year.

While underlying membership remained broadly flat in the face of tough market conditions, we saw revenue growth in trade cask sales, venues, and Single Cask Nation.

Our exclusive SMWS Members' Rooms continued their consistently strong performance throughout 2025, with mid to high single digit revenue growth in each quarter of the year. Our disciplined approach to cost management and operational efficiency has enabled us to continue investing in our strategic priorities while supporting long-term value creation for shareholders. In the second half of 2025 we undertook a top to bottom cost review and almost £1 million of gross annualised cost savings were identified that will start to flow through in the Income Statement in 2026.

We successfully completed a new financing agreement with Santander in September. The new agreement contains improved terms, such as a longer term, greater headroom and lower margin than the previous facilities with another bank.

Strategic priorities

Looking ahead to 2026, our strategic priorities remain clear. Delivering exceptional and unique whisky, growing our membership and deepening member engagement are at the forefront of our agenda, and we continue to invest in member experiences, both in our venues and through digital channels, to foster a strong sense of community and loyalty. We continue to look towards international expansion where our focus is on markets in which appreciation for premium spirits and experiential brands is growing.

The UK, Europe, the USA and Asia remain the priority markets and the next step in our US strategy will take place from April when we transition the in-market stock to our direct partners and commence the new route-to-market which we are confident will deliver substantial recurring cost and efficiency benefits.

People

Our achievements in 2025 would not have been possible without the dedication, resilience and expertise of our people. I would like to extend my sincere thanks to the Board, executive leadership and all colleagues across the business. Their passion for our brands and commitment to our mission are evident in everything we do. We continue to uphold the highest standards of governance, ensuring that our decision-making is transparent, accountable, and aligned with the long-term interests of all stakeholders.

Outlook

The Group has consistently demonstrated its ability to adapt to a changing world, and 2025 has been no exception. I remain mindful of the external uncertainties that continue to shape our industry and the significant headwinds the Group is facing, predominantly due to factors out of its control. However, we are well placed to achieve future profitable growth, as the well-held belief that the cyclical rather than structural dynamics of the spirits market means the last few years' headwinds turn into positive tailwinds.

The Board and I are grateful to our members, partners and shareholders for their continued support and trust, and I remain confident that our strategic initiatives and dedicated team will drive our company forward, delivering value for our members and shareholders.

CEO Statement

Strategic progress and resilience a key part of FY25

2025 was a year that tested our resilience as a business, as an industry and as a global community of whisky lovers. Despite persistent macroeconomic challenges, a complex geopolitical environment, and the previously announced US operational disruption at the end of the year, The Artisanal Spirits Company continued to make strategic progress, demonstrating the strength of our brands, the depth of our expertise, and the commitment of our people.

Crucially, we have maintained a relentless focus on ensuring the business is future fit for the opportunities ahead. This included a rigorous, Group wide emphasis on cost discipline and operational efficiency, with active steps to streamline our cost base and embed stronger productivity across our operations. This work is already delivering benefits, and our focus on cost management will continue into 2026, allowing us to focus our resources on the areas that deliver long-term growth and value creation.

Performance & Strategic Context

Excluding the Americas region, the Group saw a £0.4 million (c2%) decline in revenue, with a similar sized reduction in EBITDA. Momentum in key markets improved in H2, and we saw some strong performances within the Group, including SMWS recruitment in UK and China, resilience in global membership and retention, expansion of Single Cask Nation and the launch of Artisan Casks.

Within the United States, while the momentum for in-market sales improved during the year, returning to growth from Q4-25 following a c30% decline in H1-25, the US government shutdown prevented us from completing an anticipated £2.4 million shipment in the period, which would have delivered around £1.8 million of EBITDA. Alongside the one-off £0.5 million cost of the change in RTM and a known stock return revenue reversal of £1.1 million (with a related £0.8 million EBITDA effect), these non-recurring factors created a significant temporary distortion in the reported FY25 results. Importantly, these steps mark the final chapter of transition, and establish the conditions for stronger, more profitable growth from FY26 onwards.

At the same time, continuing challenges in Asia remained a meaningful drag on performance. However, we believe these challenges are cyclical rather than structural, and we are now starting to see signs of stabilisation. Recent Scotch Whisky Association export data for 2025 highlighted that the value of global exports held relatively stable at £5.4 billion, supporting our confidence that underlying consumer demand remains robust. The long term drivers of premiumisation - rooted in "less but better" consumption and the deep emotional connection consumers have with single malt whisky, craftsmanship, provenance and experience - remain firmly intact.

In the meantime, we continue to have a strong focus on operational efficiency, delivering significant cost savings and the broader shift to a leaner, more agile operating model, and this cost discipline together with operational efficiency will continue to be core priorities throughout 2026.

Progress Across Our Brands

Scotch Malt Whisky Society (SMWS)

SMWS continues to be the jewel in our crown: a unique, global whisky community grounded in creativity, discovery and experiences. In 2025, we held membership steady at around 40,000, underpinned by record underlying recruitment in the UK and China and growing engagement across Europe.

We invested in the brand and proposition: evolving our flavour navigation, launching the Signature range, advancing the Creators' Collection, and redesigning the proposition with "Get Into The Good Stuff" to make our world more accessible without compromising the depth or integrity of our whisky or our storytelling. Member experience continues to be a powerful differentiator - demonstrated through the outstanding performance of our Members' Rooms, each delivering consistent mid-to-high single-digit growth.

Single Cask Nation (SCN)

SCN delivered another strong year, growing revenue by 10% despite a market backdrop in the USA that remained exceptionally difficult for all Scotch whisky importers following the introduction of tariffs. SCN's reputation is rising around the world, recognised again in 2025 with its second consecutive Independent Bottler of the Year award.

The combination of the new US route-to-market and SCN's growing appeal positions this brand extremely well for accelerated global expansion.

Cask Sales & Artisan Casks

Our structured trade cask programme delivered year-on-year growth of 13%, reinforcing its strategic role in both revenue diversification and balance sheet optimisation. The early momentum of Artisan Casks, our luxury private cask programme launched in July, was especially encouraging. We believe it represents a major multi-year opportunity.

Global Expansion

2025 marked the expansion of our franchise model into two major international whisky markets: India and Vietnam. These new partnerships represent long term strategic footholds in markets with exceptional potential. Whilst we anticipate an initial contribution in FY26 will be modest, we are confident that our disciplined, partnership-led approach will create both brand equity and commercial opportunity for years to come.

The US - Delivering a Major Strategic Transition

The USA remains the largest whisky market globally and a critical growth frontier for ASC and we have made significant strategic progress in recent times:

- We completed the acquisition of SCN in early 2024;

- We initiated the transition to direct control of SMWSA in early 2025;

- We made the final operational shift in late 2025, with the new route-to-market going live in April 2026.

Although the US shutdown created unavoidable disruption to FY25 shipments, the foundations now in place are exactly what the business needs: greater control, greater visibility, and improved cost efficiency, including around $1m (£750k) of savings over the next three years. Late 2025 showed depletions returning to growth, a significant milestone, and this has continued into early 2026.

Our People & Culture

The resilience, expertise and passion of our teams across the UK, USA, China, Europe, Japan, Australia and Taiwan and our global partners were central to everything we achieved in 2025. Our engagement scores remain strong and our culture continues to be one of ASC's greatest assets. Our people are the custodians of our brands and the creators of the experiences our members love.

Looking Forward - A Clear Vision & Strategy

As we look ahead, we are laser-focused on delivery of our 2026 targets and our strategic priorities remain clear:

- Recruit, engage and retain more SMWS members worldwide;

- Accelerate SCN's growth into new global markets and US states;

- Realise value from our cask stock through trade and private cask sales;

- Expand ASC's reach, through portfolio, markets and route-to-market.

Alongside that, we are sharpening the articulation of who we are, why we exist and the strategy that will deliver our long-term ambitions, through our remarkable brands,

significant cask holdings, bottling and supply chain capability and whisky expertise.

Outlook

The industry has experienced a number of years of significant headwinds; however, we believe these are cyclical, not structural, and the signs of stabilisation supported by global export values holding steady reinforce our confidence in the underlying fundamentals of premium whisky.

The operational platform we now have, combined with our cost base efficiency, enhanced US model, diversified revenue streams and continued global expansion, positions us well to benefit as conditions improve.

While mindful of near-term uncertainties, I remain confident in the strength of our brands, our assets, our people and our strategy. The Artisanal Spirits Company has never been better placed to unlock the full potential of its proposition and deliver long term value for members, customers and shareholders.

CFO Statement

Impact of US Government shut-down in late 2025 and RTM change drives FY25 loss

The FY25 reported EBITDA loss was £2.4 million (FY24; £1.1 million EBITDA profit) and a Loss Before Tax of £7.0 million (FY24; £3.1 million loss). At an adjusted EBITDA level, the loss reduced to £1.9 million due to the non-recurring £0.5 million operational expense made with our previous partner in January 2025, directly linked to our taking greater management of our US operations.

These two key events had a significant impact on the EBITDA loss in FY25. Firstly, in addition to the £0.5 million non-recurring operational expense, we recognised a reversal of revenue of £1.1 million (as a result of stock to be returned), with an associated £0.8 million on EBITDA, at the end of December 2025, for stock we expect to be returned to us at the end of March 2026, when our agreement with our current RTM partner expires. This change allows us the ability to progress with new partners in the market that not only gives ASC more direct control to drive growth in the market, but also realises around $1 million (£750k) of savings over a three-year period.

Secondly, due to the US government shutdown in Q4 2025, we were unable to complete an anticipated £2.4 million worth of shipments, which would have represented around £1.8 million of EBITDA. The shutdown particularly impacted our operations due to the unique model of the Society's limited-edition whiskies, with each new bottle in the shipment requiring a Certificate of Label Approval (COLA) which could not be obtained as the relevant US government body was closed.

Revenue diversification and cost efficiencies remained key in FY25

Revenue Diversification

Revenue in the year was £19.9 million, down £3.7 million on the prior year, with the majority of the reduction related to the £3.5 million impact of the two key US impacts (£3.5m impact of the £3.2m Americas region decline).

Outwith the US impacts, encouraging growth continues to be delivered within the recent strategic additions to the Group: Cask Sales and Single Cask Nation, up £0.5 million (13%) and £0.1 million (10%) respectively.

The marginal revenue decline of 2% (excluding the Americas) in year was predominantly driven by Asia - a region that witnessed a 25% decline in 2025, now around 50% of the size it was in 2022. However, we remain well placed in the Asian market for when improvement in market sentiment returns.

Cost base management and efficiencies

Building on cost savings achieved in 2024, we achieved further net cost savings in 2025 of £0.3 million (excluding the cost of the £0.5 million previous partner operational expense) maintaining a key focus on the right sizing of the business during continued challenging trading conditions.

Selling & Distribution Expenses

This area represented the greatest level of savings in year, totalling £0.8 million. The largest element was within Advertising and Promotion (A&P) (£0.6 million) ensuring the greatest return on investment possible, with a focus on membership recruitment and retention, resulting in a reduction of 25% to £1.7 million (FY24: £2.3 million).

Depreciation was slightly up on FY24 at £1.7 million (FY24: £1.6 million) through IFRS16 depreciation increase as FY25 was the first full year in the Edinburgh George Street HQ.

The net FX loss in year was £0.1 million relating to USD and £0.3 million in JPY (FY24: £0.1 million).

The FX impact is managed closely with hedging where required.

Future cost opportunities that exist within the Group, include a reduction in depreciation from FY27 onward of around £0.6 million, as the Masterton facility depreciation ends and for every +/-0.25% base rate interest movement, an indicative saving of +/-£80k would be achieved.

As a group, we also currently hold a £5.5 million unrecognised deferred tax asset.

Administrative Expenses

Excluding the non-recurring item of £0.5 million operational expense in the US operations, overheads reduced by £0.1 million.

Payroll saw an increase of 8% year on year with £0.6 million of cost from direct employment of the SMWSA team, previously recorded as the commission cost paid to the third-party partner in the USA. £0.1 million represented increased NI cost.

Outwith these costs, payroll was flat year on year at £7.1 million (FY24: £7.1 million), with efficiency savings to offset around £0.2 million impact of employee pay increases.

|

|

Selling & Distribution Expenses |

Administrative Expenses |

||

|

2025 £'000 |

2024 £'000 |

2025 £'000 |

2024 £'000 |

|

|

Commission |

491 |

1,071 |

- |

- |

|

Advertising & Promotion (A&P) |

1,737 |

2,297 |

- |

- |

|

Depreciation |

1,672 |

1,627 |

- |

- |

|

FX Loss |

419 |

118 |

- |

- |

|

Overheads |

- |

- |

3,859 |

3,485 |

|

Payroll |

- |

- |

7,735 |

7,143 |

|

Total |

4,317 |

5,114 |

11,595 |

10,628 |

* Represents payroll cost within Overheads (noting catering employee payroll costs sits within Cost of Goods Sold)

Regional Review

Europe

As the home of SMWS, the European region comprises UK online, UK Venues, Europe and our two franchise markets, Denmark and Switzerland.

Membership numbers closed the year in Europe around 25,000, with 17,500 UK members, the remainder based in Europe. The closing 2025 position was down 8% on prior year; however, discounting around 3,000 members who temporarily joined via a complimentary code at the end of 2024 (of which around 80% did not renew), membership increased by 3% year on year. FY25 was a strong year for new members in the UK - achieving almost 5,000 new members, alongside a steady retention rate of around 70%.

Trading performance was mixed in the region with a notable strong performance in Venues, achieving year-on-year growth of 8%, highlighting the importance of experience in the current trading climate, boosted by changes in our catering approach with the premium food offering elevating the whisky experience. However, UK online and EU online sales, down 3% and 10% respectively, mirroring the current challenges in the global whisky industry.

Cask sales remained a strategic area for the business, with continued trade sales, alongside the launch in 2025 of the new luxury, private cask programme, Artisan Casks. Cask sales overall achieved growth of 13%, achieving a total of £4.7 million of revenue (FY24: £4.2 million). The opportunity for further growth in 2026 exists as Artisan Casks delivers in its first full year.

Americas

The Americas region includes The Scotch Malt Whisky Society America (SMWSA) brand and the 2024 acquired Single Cask Nation (SCN) brand, as well as the franchises in Canada and Mexico. SMWSA membership was up marginally, 1%, to around 8,000 members, and saw an increase in retention from 63% to 65%, supported by the recent loyalty scheme launch.

SMWSA shipments trading was significantly impacted by the US government shutdown and the change in RTM. Without the government shutdown, we estimate that revenue would have been broadly flat YoY. At a depletions level, the US market remains challenging, recently highlighted by SWA export data showing a 15% volume drop in exports to the market in the period May to December 2025, following the introduction of 10% tariff on Scotch Whisky imports in the US in April 2025. SMWSA depletion volumes were down around 14% and revenue down around 20%, but encouragingly, momentum improved during the year (down 4% in H2, vs 34% in H1) and returned to growth from Q4-25.

SCN recorded another year of growth in 2025, following its strong first year within the Group, delivering revenue growth of 10% to £0.8 million (FY24: £0.7 million).

With the last stage of the US RTM strategy taking effect from April 2026, we remain confident that we can drive revenue and profit growth through a significant membership increase and an optimised RTM cost base, saving $1 million (£750k) over the next three years. We will continue to support the SWA in engagement to achieve removal of the 10% tariff on Scotch Whisky imports.

Asia

Our key Asian markets consist of China, Japan, Taiwan and our franchise partners in Korea, Malaysia and SE Asia. In 2025 we announced the introduction of two new franchises in Vietnam and India. Although we anticipate that initial returns will be marginal, the Indian tariff reduction from 150% to 75% in 2026, reducing to 40% over 10 years, should help stimulate the market. India, particularly, remains a long-term strategic opportunity for the Group.

Membership in the region finished the year around 5,000 members, down 4% on prior year, predominantly as a result of lower retention levels in Taiwan. China and Japan saw membership growth of 2% and 5% respectively.

The region witnessed another year of challenging market conditions, recording a revenue decline of 25%, similar to that witnessed in 2024, across all markets in the region.

Rest of World (RoW)

The other markets within SMWS consist of our wholly-owned subsidiary in Australia and franchise operations in New Zealand and South Africa.

Australia, representing around 84% of the RoW category, saw a 11% decline in revenue, RoW region in total achieving £0.9 million in year (FY24: £1.0 million). Membership in the region was also down 8%.

Share member schemes and EPS

No new share options were awarded in 2025. Our Earnings per Share (EPS) at the end of 2025 was (10.3p), (2024: (4.6p)).

Balance Sheet strength supported by our cask spirit holding

Our balance sheet contains net assets of £7.7 million (FY24: £15.1 million), the movement reflecting the loss in year, impacted by the US operational change and US government shutdown.

The strength of our balance sheet remains in significant cask spirit holding of £28.3 million, representing the net book value paid for the over 18,000 casks that we currently hold. This is further strengthened when we consider the inherent value of those casks, which are most tangibly supported by two key comparators completed by independent valuers: 1) appraisal value based on market recovery within 180 days, and 2) appraisal value based on normal trading approach over a longer term, circa five-year period.

Appraisal based on market recovery within 180 days applies an average valuation to NBV of around 200% the most recent valuation completed in early 2026.

An appraisal based on a longer term market recovery was completed on around 18,000 casks in July 2024 and attracted a valuation to NBV of over 300%.

As a result, from the NBV of around £28 million, we have inherent values of between £50 million to £100 million. This is important to understand when we consider our net debt levels and the current valuation of the business, the former considered manageable against the inherent valuation and the latter considered to not fully incorporate the inherent value, with market cap of around £24 million and an enterprise value of around £55 million.

Net debt in the year increased to £31.5 million (2024: £25.5 million), the increase a result of the adjusted EBITDA loss recognised in the year alongside interest cost of £2.2 million, £0.5 million of US operational expense and £0.8 million of spirit and wood spend. This lower level of spirit and wood spend (representing around 1/3 of the 2024 level, 1/5 of the 2023 level and the lowest level since our IPO in 2021) is a key objective as we reduce net investment here to support our aim of net cash generation - the intention for FY26 where profitability delivery will drive the achievement.

Our wider capital allocation approach, alongside our aim of measured and steady net debt reduction, is a balanced one that recognises the opportunities to drive growth through operational investment in driving membership growth and to remain open to opportunities with regards to spirit investment, where and when applicable.

Successful refinancing of banking facilities

In September 2025 we successfully signed a new financing agreement with Santander plc to replace, and on preferential terms, the revolving credit facility (RCF) which was due to expire on 19 June 2026.

The new financing agreement represents an increased facility of £13.5 million at 20bps lower headline margin rate and no financial covenants, covering a 4-year term. Following completion, The Royal Bank of Scotland RCF of £21.5 million was completely repaid, alongside the remaining term loan and Lombard cask wood funding, totalling £0.5 million.

The Company's remaining borrowings with Fero (formerly Ferovinum), outwith the new Santander facility, totalling £6.3 million at December 2025, will be repaid as each tranche reaches the 2-year tenor, with the final repayment due in August 2026.

Optimism for the future

FY25 has very much been a year of transition, particularly with regard to the strategic change in the US RTM. This change which becomes fully effective from April 2026 gives us the opportunity to move forward and achieve greater trading penetration in the US market, through increased awareness of the SMWS and growth in membership as we take greater control of our ability to reach and engage new members, alongside substantial cost efficiencies.

In the coming year, we believe the work we have completed in recent years around our diversifying revenue portfolio, notably the acquisition of Single Cask Nation and the growth in trade cask sales, which will be further supported in FY26 by the Artisan Casks luxury cask programme, will strengthen our future profit delivery, given that we remain at 0.4% of the Ultra-Premium Scotch Whisky market which in 2024 was valued at $7.6 billion.

Consolidated Statement of Comprehensive Income for the year ended 31 December 2025

|

|

Notes |

2025 £'000 |

2024 £'000 |

|

Revenue |

6 |

19,867 |

23,601 |

|

Cost of sales |

|

(8,596) |

(8,576) |

|

Gross profit |

|

11,271 |

15,025 |

|

Selling and distribution expenses |

|

(4,317) |

(5,114) |

|

Administrative expenses |

|

(11,595) |

(10,628) |

|

Finance costs |

|

(2,448) |

(2,461) |

|

Other income |

9 |

59 |

36 |

|

Loss on ordinary activities before taxation |

7 |

(7,030) |

(3,142) |

|

Taxation |

11 |

(218) |

(109) |

|

Loss for the year |

|

(7,248) |

(3,251) |

|

Other comprehensive income: Items that may be reclassified to profit or loss: Movements in translation reserve |

|

(61) |

(71) |

|

Tax relating to other comprehensive loss |

|

- |

- |

|

|

|

(61) |

(71) |

|

Total comprehensive loss for the year |

|

(7,309) |

(3,322) |

|

Loss for the year attributable to: - Owners of parent company |

|

(7,274) |

(3,300) |

|

- Non-controlling interest |

|

26 |

49 |

|

|

|

(7,248) |

(3,251) |

|

Total comprehensive loss for the year attributable to: - Owners of parent company |

|

(7,335) |

(3,371) |

|

- Non-controlling interest |

|

26 |

49 |

|

|

|

(7,309) |

(3,322) |

|

Basic EPS (pence) |

12 |

(10.3p) |

(4.6p) |

|

Diluted EPS (pence) |

12 |

(10.3p) |

(4.6p) |

Consolidated Statement of Financial Position as at 31 December 2025

|

|

Notes |

2025 £'000 |

2024 £'000 |

|

Non-current assets Investment property |

|

- |

285 |

|

Property, plant and equipment |

13 |

9,581 |

10,734 |

|

Intangible assets |

|

2,183 |

2,352 |

|

|

|

11,764 |

13,371 |

|

Current assets Inventories |

15 |

32,242 |

31,768 |

|

Trade and other receivables |

|

3,055 |

4,286 |

|

Cash and cash equivalents |

|

1,478 |

2,868 |

|

|

|

36,775 |

38,922 |

|

Total assets |

|

48,539 |

52,293 |

|

Current liabilities Trade and other payables |

|

2,763 |

3,459 |

|

Current tax liabilities |

|

762 |

705 |

|

Financial liabilities |

19 |

7,024 |

3,032 |

|

Lease liability |

21 |

586 |

513 |

|

|

|

11,135 |

7,709 |

|

Net current assets |

|

25,640 |

31,214 |

|

Non-current liabilities Financial liabilities |

|

26,772 |

25,938 |

|

Lease liability |

|

2,294 |

2,920 |

|

Deferred tax liabilities |

|

- |

- |

|

Provisions |

|

686 |

670 |

|

Total non-current liabilities |

|

29,752 |

29,528 |

|

Total liabilities |

|

40,887 |

37,237 |

|

Net assets |

|

7,652 |

15,056 |

|

Equity Called up share capital |

|

177 |

176 |

|

Share premium account |

|

15,308 |

15,255 |

|

Translation reserve |

|

(271) |

(211) |

|

Retained earnings |

|

(7,664) |

(424) |

|

Cash flow hedge reserve |

|

- |

- |

|

Equity attributable to owners of the parent |

|

7,550 |

14,796 |

|

Non-controlling interest |

|

102 |

260 |

|

Net assets |

|

7,652 |

15,056 |

Consolidated Statement of Changes In Equity as at 31 December 2025

|

£'000 |

Called up share capital |

Share premium account |

Retained earnings |

Cash flow hedge reserve |

Translation reserve |

Other reserves |

Total controlling interest |

Non- controlling interest |

Total equity |

|

Balance at 31 December 2023 |

176 |

15,255 |

2,789 |

- |

(140) |

- |

18,080 |

195 |

18,275 |

|

Issue of share capital |

- |

- |

- |

- |

- |

- |

- |

- |

- |

|

(Loss)/profit for the period |

- |

- |

(3,300) |

- |

- |

- |

(3,300) |

49 |

(3,251) |

|

Share-based compensation |

- |

- |

135 |

- |

- |

- |

135 |

- |

135 |

|

Transactions with non-controlling interest |

- |

- |

(48) |

- |

- |

- |

(48) |

16 |

(32) |

|

Other comprehensive loss |

- |

- |

- |

- |

(71) |

- |

(71) |

- |

(71) |

|

Balance at 31 December 2024 |

176 |

15,255 |

(424) |

- |

(211) |

- |

14,796 |

260 |

15,056 |

|

Issue of share capital |

1 |

53 |

- |

- |

- |

- |

54 |

- |

54 |

|

(Loss)/profit for the period |

- |

- |

(7,274) |

- |

- |

- |

(7,274) |

26 |

(7,248) |

|

Transaction with non-controlling interest |

- |

- |

- |

- |

- |

- |

- |

(184) |

(184) |

|

Share-based compensation |

- |

- |

33 |

- |

- |

- |

33 |

- |

33 |

|

Other comprehensive loss |

- |

- |

- |

- |

(60) |

- |

(60) |

- |

(60) |

|

Balance at 31 December 2025 |

177 |

15,308 |

(7,664) |

- |

(271) |

- |

7,550 |

102 |

7,652 |

Consolidated Statement of Cash Flows as at 31 December 2025

|

|

Notes |

2025 £'000 |

2024 £'000 |

|

Loss for the year after tax Adjustments for: Taxation charged |

|

(7,248)

218 |

(3,251)

109 |

|

Finance costs |

|

2,278 |

2,293 |

|

Interest income |

|

(2) |

(1) |

|

Movements in provisions |

|

16 |

16 |

|

Share-based payments |

|

33 |

135 |

|

Investment property fair value movement |

|

- |

(20) |

|

Investment property gain on disposal |

|

- |

(14) |

|

Lease interest |

|

154 |

151 |

|

Non-cash currency gains and losses |

|

349 |

- |

|

Depreciation of tangible assets |

|

1,397 |

1,308 |

|

Amortisation of intangible assets

Movements in working capital: Increase/(decrease) in inventory |

|

223 247 |

321 (560) |

|

Decrease/(increase) in trade and other receivables |

|

151 |

486 |

|

(Decrease)/increase in trade and other creditors |

|

27 |

1 |

|

Cash flow (absorbed by)/from operations |

|

(2,157) |

974 |

|

Income taxes paid |

|

(163) |

(104) |

|

Interest paid excluding lease interest |

|

(2,158) |

(1,676) |

|

Net cash outflow used in operating activities |

|

(4,478) |

(806) |

|

Cash flow from investing activities Purchase of intangible assets |

|

(61) |

- |

|

Purchase of property, plant and equipment |

|

(718) |

(948) |

|

Sale of investment property |

|

285 |

169 |

|

Sale of property, plant and equipment |

|

21 |

19 |

|

Cash paid to acquire trade and assets of J&J Spirits |

|

(201) |

(238) |

|

Interest income |

|

2 |

1 |

|

Net cash (used in)/generated from investing activities |

|

(672) |

997 |

|

Cash flows from financing activities Share issue |

|

53 |

- |

|

Transactions with non-controlling interest |

|

- |

(16) |

|

Dividend paid to non-controlling interest |

|

(184) |

(213) |

|

Asset backed lending received |

|

2,903 |

4,343 |

|

Repayment of asset backed lending |

|

(3,550) |

(116) |

|

Drawdown of Santander RCF |

|

27,829 |

- |

|

Repayment of Santander RCF |

|

(1,057) |

- |

|

Drawdown of Natwest RCF |

|

1,000 |

500 |

|

Repayment of Natwest RCF |

|

(21,500) |

- |

|

Repayment of loan |

|

(966) |

(487) |

|

Repayment of leases |

|

(707) |

(504) |

|

Net cash from financing activities |

|

3,821 |

3,507 |

|

Net increase/(decrease) in cash and cash equivalents |

|

(1,329) |

1,704 |

|

Foreign currency translation |

|

(61) |

(71) |

|

Cash and cash equivalents at beginning of year Non-controlling interest movement |

|

2,868 - |

1,235 - |

|

Cash and cash equivalents at end of year |

|

1,478 |

2,868 |

|

Relating to: Bank balances and short term deposits |

|

1,478 |

2,868 |

Notes to the Financial Statements

1) Basis of preparation

The condensed interim financial information presents the consolidated financial results of The Artisanal Spirits Company plc and its subsidiaries (together the "Group") for the twelve months ended 31 December 2025 and the comparative figures for the twelve months ended 31 December 2024.

The Group's consolidated financial statements have been prepared on a going concern basis under the historical cost convention; in accordance with UK adopted International Accounting Standards.

This statement does not include all the information required for the annual financial statements and should be read in conjunction with the Annual Report & Accounts.

The financial information set out above does not constitute the company's statutory accounts for 2025 or 2024. The statutory accounts for 2024 have been delivered to the Register of Companies, and those for 2025 will be delivered in due course. The independent auditor has reported on these accounts, their reports were (i) unqualified, (ii) did not draw attention to any matter by way of emphasis without qualifying their report and (iii) did not contain a statement under section 498 (2) or (3) of the Companies Act 2006.

This announcement was approved on behalf of the Board on 27 March 2026.

2) Accounting Policies

The accounting policies applied in preparing the condensed consolidated financial information are the same as those applied in the preparation of the Annual Report and Accounts for the year ended 31 December 2025, and those applied in the preparation of the Group's Historical Financial Information included within the Company's Admission Document.

3) Going concern

The Directors are, at the time of approving the financial statements, satisfied that the Group and Company have adequate resources to continue in operational existence for a period of at least 12 months. Thus, they continue to adopt the going concern basis of accounting in preparing the financial statements.

The Group meets its day-to-day working capital requirements from a revolving credit facility of £35.0m together with cash balances. The Group has further access to a £15.0m inventory financing facility which can be drawn upon if required, subject to the maximum borrowings cap under the revolving credit facility. The revolving credit facility was established in September 2025 and is not due for renewal until September 2029 whilst the inventory financing facility has an evergreen term. The revolving credit facility has no attached financial covenants and carries a maximum borrowing cap combined with the inventory financing facility of £35.0m.

In the context of the above, the Directors have prepared cash flow forecasts for the period to 30 April 2027 which indicate that, taking account of reasonably plausible downside scenarios, the Group will have sufficient funds to meet its liabilities as they fall due for that period.

The Directors have assessed the potential future impacts of geopolitical risk and have modelled scenarios as follows:

1. A base cash flow forecast. The 2026 figures in this forecast are based on the Group's 2026 budget, which is compiled using board approved forecasts and reflecting current performance, expected revenue growth and membership retention. The 2027 figures in the base cash flow forecast assume flat performance on 2026. This base case assumes a more prudent growth trajectory than in previous years, with organic market growth rate at single digit, supported by full year delivery of strategic initiatives secured. Cost inflation has been considered and additional costs have been included to account for increased wage inflation.

2. A severe, but plausible downside scenario. The Directors have also prepared a sensitised forecast which considers the impact of certain severe but plausible downside events, when compared to the base case. This severe but plausible downside scenario assumes a global economic downturn, exacerbated by a geopolitical shock event with a resultant shut down of Asian operations impacting revenue in the region of £5m per annum, together with an associated reduction in global sales based on recent experience from other economic downturns. Under this scenario, one-off costs to implement the required cost-base reductions are assumed in the impacted markets.

In this scenario, capital expenditure has been reduced, investment in spirit and wood continues as per current forecasts, albeit at a lesser level than in previous years. Throughout the severe but plausible downside scenario the Group would remain within its facility limits and in compliance with the relevant covenants, with further cash mitigation opportunities available through capital expenditure, spirit and wood investment.

The Directors are mindful of the potential impacts to macro-economic conditions and further risk of disruption to supply chains that the ongoing geopolitical uncertainty including conflict in the Middle East presents, the role of significant cask sale cash inflows, and the subjectivity of future forecasts to changing customer demand, and after assessing the risks do not believe there to be a material risk to going concern. Based on the above, the Directors are confident that the Group and Company will have sufficient funds to continue to meet their liabilities as they fall due for at least 12 months from the date of approval of the financial statements, and therefore the Directors believe it remains appropriate to prepare the financial statements on a going concern basis.

4) Principal risks and uncertainties

The principal risks and uncertainties affecting the Group are separately disclosed in the Annual Report & Accounts.

5) Dividends

No dividend was declared or paid during the period (prior period £nil).

6) Operating Segments

As the business has grown the level of information presented to the chief operating decision maker has continued to develop to better support business needs and inform decision making. The geographical markets in which the Group operates are allocated to a business segment, consistent with the internal reporting provided to the chief operating decision-maker.

The chief operating decision maker has been identified as the Board of Directors, which is responsible for developing strategy and leading its execution. The Board includes the Chief Executive Officer, Chief Financial Officer, Chair and Non-Executive Directors.

The Group is organised in three distinct geographical segments for which summarised management information is available to the Board plus a fourth segment which makes up the rest of the world. These geographical markets as set out in the table overleaf represent the operating segments of the Group. Australia, New Zealand and South Africa, which do not sit within the identified geographical segments, are aggregated and presented within Other. Whilst Central costs are not considered at an operating segment level, they are reported to the Board and are included to aid reconciliation to the Consolidated Statement of Comprehensive Income. Sales are allocated to the geographical market in which the sale is fulfilled. The Board receives monthly financial information to a Gross Profit level, in addition to Central Costs, and utilise this information to monitor performance and allocate resources.

|

2025 |

Europe £'000 |

Asia £'000 |

Americas £'000 |

Other £'000 |

Group £'000 |

|

Revenue |

14,596 |

3,144 |

1,268 |

860 |

19,867 |

|

Cost of Sales |

(6,108) |

(1,102) |

(990) |

(397) |

(8,596) |

|

Gross Profit |

8,488 |

2,042 |

277 |

464 |

11,271 |

|

Selling & distribution costs |

|

|

|

|

(4,317) |

|

Administrative costs |

|

|

|

|

(11,595) |

|

Finance Costs |

|

|

|

|

(2,448) |

|

Other income |

|

|

|

|

59 |

|

Loss before tax |

|

|

|

|

(7,030) |

|

Taxation |

|

|

|

|

(218) |

|

Net Loss |

|

|

|

|

(7,248) |

|

2024 |

Europe £'000 |

Asia £'000 |

Americas £'000 |

Other £'000 |

Group £'000 |

|

Revenue |

13,785 |

4,191 |

4,657 |

968 |

23,601 |

|

Cost of Sales |

(5,826) |

(1,243) |

(1,086) |

(421) |

(8,576) |

|

Gross Profit |

7,959 |

2,948 |

3,571 |

547 |

15,025 |

|

Selling & distribution costs |

|

|

|

|

(5,114) |

|

Administrative costs |

|

|

|

|

(10,628) |

|

Finance Costs |

|

|

|

|

(2,461) |

|

Other income |

|

|

|

|

36 |

|

Loss before tax |

|

|

|

|

(3,142) |

|

Taxation |

|

|

|

|

(109) |

|

Net Loss |

|

|

|

|

(3,251) |

The Board does not receive a segmental breakdown of assets and liabilities, depreciation or capital expenditure.

Within Europe, the UK represents the largest market, split UK Online and UK Venues, delivering £2.9 million (2024: £3.2 million) and £4.4 million (2024: £4.1 million), respectively.

In the Americas region, the largest market being the USA, shipment sales of £0.6 million were 86% lower than the prior year (2024: £4.0 million), with in-market depletions 17% lower than the prior year.

China represents the largest market in Asia, revenue in the year of £1.9 million (2024: £2.4 million) was a 18% decline on the prior year, impacted by the economic headwinds within the market.

Other is predominantly represented by Australia, with revenue of £0.7 million (2024: £0.8 million).

An analysis of the Group's revenue by product category is as follows.

|

|

2025 £'000 |

2024 £'000 |

|

Revenue from sale of whisky |

14,399 |

18,291 |

|

Membership income |

1,611 |

1,794 |

|

Revenue from sale of other spirits |

178 |

125 |

|

Member rooms |

2,359 |

2,218 |

|

Events and tastings |

1,091 |

953 |

|

Other |

228 |

220 |

|

Total revenue |

19,867 |

23,601 |

Other includes revenue from sales of merchandise, rental income from investment properties, shipping charges billed to customers, and income from bottling services provided to third parties. Membership income is recognised evenly over the membership period.

7) Loss for the year

The Group measures its performance using EBITDA and Adjusted EBITDA, which are non-GAAP measures. EBITDA and adjusted EBITDA are reconciled to statutory loss before tax as below:

|

|

2025 £'000 |

2024 £'000 |

|

Operating loss is stated after charging: |

|

|

|

Amortisation of intangible assets |

223 |

321 |

|

Depreciation on tangible assets |

1,397 |

1,308 |

|

Cost of inventories recognised as an expense |

6,165 |

6,000 |

|

Net foreign exchange loss |

419 |

58 |

|

Reconciliation of adjusted EBITDA: |

|

|

|

Loss on ordinary activities before taxation |

(7,030) |

(3,142) |

|

Add back; Net foreign exchange loss |

419 |

- |

|

Add back; Depreciation of tangible assets |

1,397 |

1,308 |

|

Add back; Depreciation of production assets within cost of sales |

156 |

123 |

|

Add back; Amortisation of intangible assets |

223 |

321 |

|

Add back; Finance Costs - interest on loans |

2,278 |

2,293 |

|

Add back; Finance Costs - leases |

154 |

151 |

|

EBITDA |

(2,403) |

1,055 |

|

Exceptional and non-recurring costs (Note 10) |

478 |

- |

|

Adjusted EBITDA |

(1,925) |

1,055 |

Adjusted EBITDA and loss for the year are stated after including £nil (2024: £0.1m) of share based payment costs. Finance costs as stated above total £2,432k and exclude £16k of provision discount unwind costs, included within finance costs in the Income Statement.

8) KPI's

|

2025 |

Revenue1 £'000 |

Year End Members |

Average Members |

Annual Revenue/ Member £ |

Annual Contribution/ Member £2 |

Retention % |

Expected Years3 |

LTV (Members) £4 |

|

Europe |

9,566 |

24,715 |

26,670 |

359 |

174 |

66% |

3.0 |

514 |

|

Asia |

3,051 |

5,157 |

5,140 |

594 |

381 |

64% |

2.8 |

1,071 |

|

Americas |

707 |

8,085 |

7,929 |

89 |

(4) |

64% |

2.8 |

(12) |

|

Other |

822 |

1,699 |

1,765 |

466 |

241 |

75% |

4.0 |

954 |

|

Total |

14,145 |

39,656 |

41,504 |

341 |

168 |

66% |

2.9 |

492 |

|

Change vs prior year |

(26%) |

(7%) |

2% |

(28%) |

(38%) |

(7%) |

(15%) |

(47%) |

|

2024 |

Revenue1 £'000 |

Year End Members |

Average Members |

Annual Revenue/ Member £ |

Annual Contribution/ Member £2 |

Retention % |

Expected Years3 |

LTV (Members) £4 |

|

Europe |

9,911 |

27,359 |

24,979 |

397 |

183 |

74% |

3.9 |

705 |

|

Asia |

4,166 |

5,455 |

5,265 |

791 |

552 |

75% |

4.0 |

2,187 |

|

Americas |

4,179 |

8,041 |

8,410 |

497 |

345 |

63% |

2.7 |

943 |

|

Other |

968 |

1,867 |

1,917 |

505 |

281 |

72% |

3.5 |

997 |

|

Total |

19,224 |

42,722 |

40,571 |

474 |

269 |

71% |

3.4 |

927 |

1 Total revenue excludes sales totalling £5,722k (2024: £4,377k) which relate to trade cask sales, Artisan Casks, JG Thomson and Single Cask Nation, and are unrelated to membership proposition.

2 Contribution is a non-IFRS measure, and is defined by Management as Gross Profit less Commission paid on sales.

3 Expected Years is a non-IFRS measure, and is defined by Management as one divided by one minus retention 1/(1-r%).

4 Lifetime Value (LTV) is a non-IFRS measure, and is defined as Annual Gross Profit per member, multiplied by expected years.

9) Other operating income

|

|

2025 £'000 |

2024 £'000 |

|

Other income |

59 |

36 |

|

|

59 |

36 |

Other income in 2025 and 2024 relate to refunds of previously overpaid expenses in SMWS China.

10) Exceptional and non-recurring costs

|

|

2025 £'000 |

2024 £'000 |

|

US operating expense |

478 |

- |

|

|

478 |

- |

For the year ended 31 December 2025, non-recurring costs of £478k were incurred in relation to taking more direct management of the Group's SMWS America Business. The cost incurred incorporates the cost to compensate the previous supplier for finding and training revenue‑generating employees.

11) Taxation

|

|

2025 £'000 |

2024 £'000 |

|

Current income tax |

|

|

|

UK corporation tax |

|

|

|

Adjustment in respect to prior periods |

- |

- |

|

Foreign tax |

218 |

109 |

|

Current tax charge |

- |

- |

|

Deferred tax |

|

|

|

Deferred tax charge |

- |

- |

|

Tax on ordinary activities |

218 |

109 |

12) Earnings per Shares (EPS)

|

|

2025 £'000 |

2024 £'000 |

|

Earnings used in calculation |

(7,274) |

(3,320) |

|

Number of shares |

70,732,443 |

70,559,774 |

|

Basic EPS (p) |

(10.3p) |

(4.6p) |

|

Number of dilutable shares |

75,438,906 |

76,058,111 |

|

Diluted EPS (p) |

(10.3p) |

(4.6p) |

All dilutable potential shares relate to share options. A loss per share is not diluted. The number of shares and number of dilutable shares shown represent the weighted average for the period.

13) Property, plant and equipment

|

|

Land and buildings freehold £'000 |

Land and buildings leasehold £'000 |

Leasehold improvements £'000 |

Fixtures, fittings and equipment £'000 |

Cask wood £'000 |

Right-of use asset £'000 |

Total £'000 |

|

Cost or valuation |

|

|

|

|

|

|

|

|

As at 31 December 2023 |

678 |

1,441 |

503 |

4,962 |

4,289 |

4,505 |

16,378 |

|

Additions |

- |

- |

25 |

144 |

779 |

1,159 |

2,107 |

|

Disposals |

- |

- |

- |

(19) |

- |

- |

(19) |

|

As at 31 December 2024 |

678 |

1,441 |

528 |

5,087 |

5,068 |

5,664 |

18,466 |

|

Reallocation |

1 |

1 |

(1) |

- |

1 |

1 |

3 |

|

Additions |

- |

25 |

- |

35 |

658 |

- |

718 |

|

Disposals |

- |

- |

- |

(50) |

- |

(10) |

(60) |

|

As at 31 December 2025 |

679 |

1,467 |

527 |

5,072 |

5,727 |

5,655 |

19,127 |

|

|

|

|

|

|

|

|

|

|

Accumulated depreciation |

|

|

|

|

|

|

|

|

As at 31 December 2023 |

196 |

1,167 |

353 |

2,019 |

662 |

1,555 |

5,952 |

|

Charge for the year |

15 |

53 |

51 |

844 |

237 |

579 |

1,779 |

|

As at 31 December 2024 |

211 |

1,220 |

404 |

2,863 |

899 |

2,134 |

7,731 |

|

Charge for the year |

25 |

73 |

29 |

830 |

262 |

639 |

1,858 |

|

Reallocation/remeasurement |

- |

- |

(8) |

7 |

- |

5 |

4 |

|

Released on disposal |

- |

- |

- |

(47) |

- |

- |

(47) |

|

As at 31 December 2025 |

236 |

1,293 |

425 |

3,653 |

1,161 |

2,778 |

9,546 |

|

Net book value |

|

|

|

|

|

|

|

|

As at 31 December 2024 |

467 |

221 |

123 |

2,224 |

4,169 |

3,530 |

10,734 |

|

As at 31 December 2025 |

443 |

174 |

102 |

1,419 |

4,566 |

2,877 |

9,581 |

£262k (2024: £226k) of the depreciation charge for cask wood, alongside £90k (2024: £62k) of the depreciation charge for fixtures, fittings and equipment and £66k (2024: £66k) of the depreciation charge for right-of-use assets have been capitalised as costs of stock. The remaining balance has been expensed to the Statement of Comprehensive Income.

Leases are in relation to the Group's supply chain facility at Masterton Bond, the Group's Head Office in Edinburgh, and venues at Queen Street in Edinburgh and Bath Street in Glasgow.

Right of use assets included in the Consolidated Statement of Financial Position were as follows.

|

|

Venues |

Supply Chain Facility |

Head office |

Total |

|

As at 31 December 2023 |

1,145 |

1,805 |

- |

2,950 |

|

Additions |

75 |

- |

1,084 |

1,159 |

|

Depreciation |

(201) |

(232) |

(146) |

(579) |

|

At 31 December 2024 |

1,019 |

1,573 |

938 |

3,530 |

|

Remeasurement/reallocation |

- |

- |

(14) |

(14) |

|

Depreciation |

(209) |

(232) |

(198) |

(639) |

|

At 31 December 2025 |

810 |

1,341 |

725 |

2,877 |

Lease Liabilities included in the Consolidated Statement of Financial Position were as follows.

|

|

Venues |

Supply Chain Facility |

Head office |

Total |

|

As at 31 December 2023 |

1,131 |

1,828 |

- |

2,959 |

|

Additions |

37 |

- |

789 |

826 |

|

Interest payment |

63 |

44 |

44 |

151 |

|