Final Results

Summary by AI BETAClose X

Surgical Innovations Group plc

("Surgical Innovations", the "Company", or the "Group")

Final Results

Results for the year ended 31 December 2025

Optimising for growth: 2025 as a springboard for future performance

Surgical Innovations Group plc (AIM: SUN), the designer, manufacturer and distributor of innovative medical technology for minimally invasive surgery ("MIS"), reports its audited final results for the year ended 31 December 2025 ("FY25").

Financial highlights:

|

· |

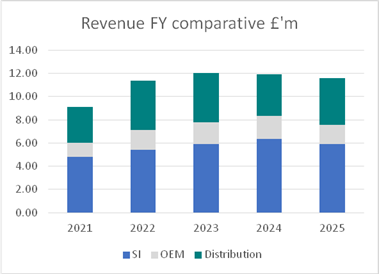

Revenues broadly flat at £11.6m (2024: £11.9m) |

|

|

Ø Overall, SI Branded products decreased 8% to £5.9m (2024: £6.4m), driven by tariff headwinds in the USA and structural sales challenges with our partner in India |

|

|

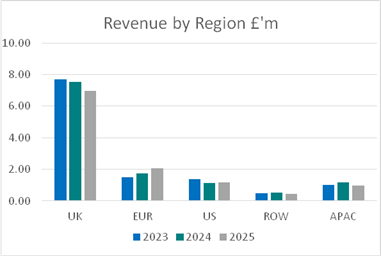

Ø Positively, Europe demonstrated strong growth of 23% with sales reaching £2.1m in 2025 (2024: £1.7m) driven by the continued resonance of the Group's sustainability messaging, a key differentiator for SI Branded products |

|

|

Ø Encouraging increase in UK distribution revenues by 14% to £4.1m (2024: £3.6m) as strategy to add high value devices to portfolio shows dividends |

|

|

Ø OEM sales experienced a decline of 12% to £1.7m in 2025 (2024: £1.9m) as previously indicated as a result of a strong 2024 which included the clearance of prior-year backorders. This was further impacted by supply constraints relating to a component provided by a key OEM partner which has now been resolved |

|

· |

Underlying gross margins increased by 262 bps to 33.73% (2024: 30.65%) as a result of a change in product mix towards Elemental products |

|

· |

Adjusted EBITDA loss in 2025 of £0.4m (2024: profit of £0.05m) |

|

· |

Adjusted EPS loss of 0.08p per share (2024: 0.07p per share loss) |

|

· |

Net cash inflow from operations amounted to £0.6m (2024: outflow of £0.10m) as a result of strong cash management during period |

|

· |

The Group's closing net cash1 balances as of 31 December 2025 amounted to (£0.3m) (as at 31 December 2024: (£0.3m)) |

1 Net cash balances consists of cash at bank, less bank borrowings and invoice financing facilities in use.

Commercial and operational highlights:

|

· |

Focus on working capital management in 2025 positions business well to take advantage of future growth opportunities |

|

· |

Implementation of targeted operational efficiencies and cost-down product initiatives delivering margin improvement across the business |

|

· |

Increased investment in both UK and international sales and marketing capabilities, driving a growing pipeline of opportunities and improved account conversion rates across key markets |

|

· |

Strong performance in UK third party sales underpinning the strategic focus on high-margin, high quality revenue streams and improving the product sales mix |

|

· |

Ongoing alignment of sales strategy with core markets, supporting scalable and profitable growth opportunities |

|

· |

The Board was strengthened during the period with the appointments of Roy Davis as Chair, Andrew Boteler as Senior Independent Director, and Duncan Soukup as Non-Executive Director, bringing a wealth of experience to support and accelerate the Company's growth |

Current trading and outlook:

|

· |

Positive sales performance in Q1 provides a solid start to the year and reinforces confidence in returning the business to growth in 2026 |

|

· |

Continued focus on cost-down initiatives and operational efficiencies is expected to drive further margin improvement, improving profitability and cash generation across the business |

|

· |

Increasing adoption of environmentally friendly procurement solutions by healthcare providers aligns with the Group's sustainability strategy, positioning its products to meet growing market demand and strengthen our competitive advantage |

|

· |

Securing Medical Device Regulation (MDR) certification paves the way for the launch of new devices to expand the product portfolio and support growth in both existing and new markets |

|

· |

Ongoing strategic investments in sales, marketing, and international expansion aim to capitalise on market opportunities, improve account conversion, and deliver long-term value for shareholders |

|

· |

The Board is reviewing the business's strategy with a view to identify options to optimise shareholder value going forward. The Board will update the market in due course |

Chairman of Surgical Innovations, Roy Davis, said: "The Company delivered a resilient performance in what was a challenging year. With a positive start to 2026, a focus on the basics and several strategic initiatives underway, the Company is better positioned for future growth and long-term success. Our focus on sustainability-led market expansion, targeted distribution partnerships, and innovative product additions will continue to strengthen the Company's competitive position. Concurrently, ongoing cost-optimisation initiatives are enhancing profitability and supporting sustainable operations.

"As the year unfolds, the Company remains committed to seizing emerging opportunities, delivering high-quality solutions, and creating lasting value for both our customers and stakeholders. The Board is committed to capitalising on the opportunities ahead and believes the business is well placed to deliver significant long-term shareholder value."

This announcement and investor presentation have been made available online at https://www.sigroupplc.com/investors-centre/.

Investor Presentation

David Marsh, Chief Executive Officer, and Brent Greetham, Chief Financial Officer, will provide a live presentation relating to the final results via the Investor Meet Company platform today, Tuesday 21 April 2026 at 11.00am BST.

The presentation is open to all existing and potential shareholders. Questions can be submitted pre-event via your Investor Meet Company dashboard up until 09.00. the day before the meeting or at any time during the live presentation.

Investors can sign up to Investor Meet Company for free and add to meet Surgical Innovations Group plc via:

https://www.investormeetcompany.com/surgical-innovations-group-plc/register-investor. Investors who already follow Surgical Innovations Group plc on the Investor Meet Company platform will automatically be invited.

For further information please contact:

|

Surgical Innovations Group plc |

|||

|

David Marsh, CEO |

Tel: 0113 230 7597 |

||

|

Brent Greetham, CFO |

|

||

|

|

|

||

|

Singer Capital Markets (Nominated Adviser & Broker) |

Tel: 020 7496 3000 |

||

|

Alex Bond / Graham Hertrich / Anastassiya Eley |

|

||

|

|

|

||

|

Walbrook PR (Financial PR & Investor Relations) |

Tel: 020 7933 8780 or si@walbrookpr.com |

||

|

Paul McManus / Lianne Applegarth |

Mob: 07980 541 893 / 07584 391 303 |

||

About Surgical Innovations Group plc

The Group specialises in the design, manufacture, sale and distribution of innovative, high quality medical products, primarily for use in minimally invasive surgery. Our product and business development is guided and supported by a key group of nationally and internationally renowned surgeons across the spectrum of minimally invasive surgical activity.

We design, manufacture and source our branded port access systems, surgical instruments and retraction devices which are sold directly in the UK home market through our subsidiary, Elemental Healthcare, and exported widely through a global network of trusted distribution partners. Many of our products in this field are based on a "resposable" concept, in which the products are part reusable, part disposable, offering a high quality and environmentally responsible solution at a cost that is competitive against fully disposable alternatives.

Elemental also has exclusive UK distribution for a select group of specialist products employed in laparoscopy, bariatric and metabolic surgery, hernia repair and breast reconstruction.

In addition, we design and develop medical devices for carefully selected OEM partners and have also collaborated with a major UK industrial partner to provide precision engineering solutions to complex problems outside the medical arena.

We aim for our brands to be recognised and respected by healthcare professionals in all major geographical markets in which we operate and provide by development, partnership or acquisition a broad portfolio of cost effective, procedure specific surgical instruments and implantable devices that offer reliable solutions to genuine clinical needs, the Company's resposable portfolio enables healthcare providers to reduce both plastic waste and their CO2 footprint as they strive for net zero.

Further information

Further details of the Group's businesses and products are available on the following websites:

To receive regular updates by email, please contact si@walbrookpr.com

Chairman's Statement

For the year ended 31 December 2025

The Company delivered a resilient performance in what was an exceptionally challenging year. Sales of £11.6 million reflect the strength of our customer relationships and the commitment of our team. In the face of headwinds in global healthcare markets and supply chain pressures, we remained focused on operational discipline and long-term value creation. Encouragingly, the actions we have taken over the past year and our continued focus on the basics, position us well for improvement and we look ahead with confidence that the year ahead will show a return to growth and enhanced performance.

Market overview

In today's market, healthcare systems continue to face the considerable challenge of reducing the backlog of elective procedures, which remains in excess of seven million treatment pathways in the UK alone. At the same time, rising supply chain costs and periodic disruption have resulted in backorders of certain critical components, adversely affecting sales performance. In the UK this has been compounded by ongoing industrial action by doctors, impacting surgical procedures.

Despite these headwinds, the increasing emphasis on environmental sustainability is reshaping procurement priorities across the healthcare sector. Providers are not only seeking to improve efficiency and reduce waiting lists, but also to embed more sustainable practices within their operations and supply chains. In our core markets, this shift is translating into growing demand for solutions that reduce waste and environmental impact without compromising clinical performance.

Against this backdrop, the Company's Resposable™ technology is strongly aligned with evolving customer needs. By combining reusable and single-use elements, it offers a cost-effective and environmentally responsible alternative to fully disposable devices, positioning Surgical Innovations to benefit as surgical backlogs are progressively addressed and sustainability becomes an ever more important purchasing criterion.

Financial overview

The Group recorded revenues of £11.6m (2024: £11.9m), reflecting an 8% decline in SI Branded product sales to £5.9m (2024: £6.4m), offset by an encouraging increase in distribution revenue of 14% to £4.1m (2024: £3.6m).

Tariff headwinds in the USA and a temporary slowdown in India, as our partner rebuilds its in-country sales team, have impacted SI Branded product sales.

In the UK, the market was particularly affected by a reduction in bariatric procedures due to the impact of drug treatments, which notably affected sales of gastric calibration tubes, whilst these new treatments remain popular the Company expects to see a modest increase in procedures during 2026. Also in the UK, sales of third-party products grew substantially to £4.05m (2024: £3.62m), reflecting the effectiveness of our strategy to prioritise high-growth opportunities and foster strong partnerships with leading suppliers. This growth demonstrates our ability to identify and capitalise on market trends, strengthen relationships with key partners, and deliver value to both customers and shareholders, even in a challenging operating environment.

In Europe, SI Branded sales have demonstrated strong growth, reaching £2.08m in 2025 (2024: £1.73m). This increase was driven by the continued resonance of our sustainability messaging, which has struck a chord with healthcare providers and distributors in key European markets. Our focus on environmentally responsible products, combined with targeted marketing and educational initiatives, has reinforced our reputation as a trusted and innovative partner.

The OEM business declined during the year, following a strong 2024 which included the clearance of prior-year backorders. This was further impacted by supply constraints relating to a component provided by a key OEM partner. Looking ahead, the Company expects robust growth in 2026, supported by a strong sales forecast from our long-term partner AMS, underpinned by a new contract that positions us positively for the year. The OEM business has been further strengthened by the development of new relationships with two global instrument manufacturers.

Operational and supply chain challenges have impacted margins and efficiencies, driven by inflationary pressures on key components, extended lead times, and complex regulatory requirements.

Adjusted EBITDA decreased to a loss of £0.4m (2024: profit of £0.05m) due to the operational and supply chain challenges outlined above. Adjusted Loss Per Share amounted to 0.08 pence (2024: £0.07p).

Throughout the financial year, the Group experienced a cash inflow of £0.6m from operations (2024: cash outflow of £0.1m). Capital expenditure remained consistent at £0.2m (2024: £0.1m). Product innovation remains a key strategic pillar, with total investment in research expenses for the year amounting to 10.9% of revenue (2024: 9.6%).

The Group's closing net cash balances as of 31 December 2025 amounted to (£0.3m) (2024: (£0.3m)). This comprises of cash at bank of £0.8m (2024: £0.2m), less bank borrowings of £0.2m (2024: £0.5m), less invoice financing facilities in use of £0.9m (2024: £nil).

Strategy and development

The Group specialises in the design, manufacture, sale and distribution of innovative, high-quality medical devices, principally for use in minimally invasive surgery. We develop, manufacture and source our portfolio of branded port access systems, surgical instruments and retraction devices, which are sold directly in the UK through our subsidiary, Elemental Healthcare, and exported extensively through a well-established global distribution network. A number of our products are founded on a "ResposableTM" concept, combining reusable and disposable elements to deliver high clinical performance in a cost-effective and environmentally responsible manner, offering a compelling alternative to fully disposable solutions.

Elemental Healthcare also holds exclusive UK distribution rights for a carefully selected portfolio of specialist products supporting laparoscopy, bariatric and metabolic surgery, hernia repair, breast reconstruction, upper gastrointestinal and colorectal procedures. In addition, we design and develop medical devices for a number of strategically chosen OEM partners.

Our strategic objective for our brands is to be recognised and trusted by healthcare professionals across all core markets in which we operate. Through sustained internal innovation, disciplined strategic partnerships and targeted acquisitions, we continue to build a comprehensive portfolio of cost-effective, procedure-specific surgical instruments and implantable devices, delivering practical, innovative solutions that address real clinical needs within the operating theatre.

The Board is focused on optimising our business operations, strengthening our product portfolio and growing sales through our direct UK sales force and international distributor partners to deliver improved financial performance. In the short team, we are focussed on delivering on the basics of increasing sales, improving profitability and cash generation. As such the Board is closely examining opportunities to create value for shareholders through a mixture of strategic options.

Regulatory and new product development

The Company successfully achieved certification under the Medical Device Regulation (MDR) in the year. This is a significant milestone that underscores our commitment to the highest standards of quality, safety, and regulatory compliance. Achieving MDR certification not only validates our robust systems and processes but also positions us to accelerate new product development and expand registration into new markets.

In addition, the Company has successfully completed its annual audits for the Medical Device Single Audit Program (MDSAP) and the UKCA mark, further demonstrating our ongoing dedication to regulatory excellence across multiple regions. These achievements reinforce our strong compliance framework and provide a solid foundation for future growth and innovation.

Following the successful completion of our transition to MDR and UKCA certification, we are now well positioned to focus our full attention on strengthening and expanding our product pipeline. The first half of the year will see the addition of LogiTube Lux, Logi Grasp, and Logi Dissect to our portfolio, further enhancing the breadth and competitiveness of our offering.

Investment in new product development underscores our commitment to sustainability, with a strong emphasis on accelerating time-to-market and implementing cost-saving measures to enhance profitability.

In parallel, we have commenced the rollout of targeted cost-reduction initiatives. These projects are expected to deliver meaningful margin improvements across several of our key product lines, supporting both profitability and long-term shareholder growth value.

Operational update

Our operational focus continues to centre on driving efficiency across the facility. Key initiatives include enhanced automation in critical areas, aimed at improving both quality and throughput. These enhancements are helping to standardise processes and ensure consistent product excellence.

In recent years, the Company has made significant progress in reducing its operational cost base. Over the year, focus has shifted towards improving product margins through targeted cost reduction initiatives. Together, these operational improvements strengthen our manufacturing capabilities and support sustainable margin improvement.

Board and executive management update

It was a privilege to join the Board of Surgical Innovations in September 2025, and we welcome both Andrew Boteler and Duncan Soukup, who joined the Board alongside me. Andrew brings considerable financial and governance experience from his executive and non-executive career, and his appointment as Chair of the Audit and Remuneration Committees strengthens our oversight capabilities as we seek to focus on delivering shareholder value. Duncan brings deep investment expertise and a long-term perspective as a significant shareholder, and I believe his alignment with the Company's interests will be a valuable asset to the Board.

At the same time Jonathan Glenn and Keyvan Djamarani stepped down from the Board upon our appointment, I would like to give my sincere thanks to Jon and Keyvan for their contribution to the business.

Separately Brent Greetham has announced his intention to step down from the Board and his role as CFO, I would like to thank him for his contribution to the business. The Company is at an advanced stage of recruiting a CFO and will make further announcement in time.

I am delighted to be working alongside David Marsh and the management team, as well as my fellow non-executive colleagues Andy and Duncan, as we look to build on the foundations that have been laid. The Board is united in its focus on delivering value for shareholders over the medium term, and I look forward to reporting on our progress.

The Board would like to thank Jon and Keyvan for their valued contribution and commitment to the Company during their tenure. I would also like to thank Brent for his efforts during the past year.

As we move forward the Board remains committed to maintaining strong leadership and oversight of the business and is focussed on maximising shareholder value.

Current trading and outlook

Sales during Q1 2026 have been in line with management expectations, with ongoing investment in sales and marketing helping to drive new opportunities across key markets. Several major account conversions are underway, reflecting both the strength of our product offering and growing market interest.

The Company remains well positioned to capitalise on these opportunities, leveraging its innovative solutions, sustainability-led value proposition, and targeted sales initiatives to drive growth across key markets.

Looking ahead, we plan to extend the Logi™ range during the second half of 2026, reinforcing our innovation pipeline and strengthening our presence in this specialist segment. These strategic launches demonstrate our continued commitment to product development and our ability to respond effectively to emerging market opportunities across all key territories.

During 2026, we will deliver a series of targeted cost-reduction initiatives designed to enhance margins across key Resposable™ products. These programmes are centred on optimising material selection, refining component design and introducing functional improvements that reduce manufacturing costs while maintaining, and where possible enhancing, product performance.

Following the successfully renegotiated distribution agreement with Microline Surgical highlighted in last year's results, the revised agreement is valued at an anticipated £9 million over the next five years, reinforces a long-standing partnership and providing a solid foundation for shareholder value.

We also made significant progress with Aspen Surgical, where our agreement delivered over £1 million in first-year sales, with further expansion expected in 2026.

The recent extension of key distribution agreements, along with the establishment of new partnerships, further reinforces Elemental's market presence and growth potential. As the year unfolds, the Company remains committed to seizing emerging opportunities, delivering high-quality solutions, and creating lasting value for both our customers and stakeholders.

We are fortunate to work in a business that helps clinicians deliver positive outcomes to their patients every day. It is a privilege to work with our customers to help them make a difference and I would like to thank all of our customers for their continued use of our products and the trust they place in us to support the work they do.

I would also like to thank our employees and partners around the world for all their hard work. It is their dedication that makes Surgical Innovations the company that it is and I am proud of their efforts in rising to the daily challenges we face as a business in such a positive way.

Finally, I would like to thank our shareholders for their continuing support for the business. I believe we are now moving in the right direction and will be able to deliver on the potential the business has.

I would like to summarise by re-iterating my continued belief and confidence in the Group's ability to capitalise on the opportunities ahead and is well placed to deliver significant long-term shareholder value.

Roy Davis

Chairman

21 April 2026

Operating and Financial Review

New board configuration

During the year, the Board underwent a number of changes which mark an important phase in the development of the Company's governance for the future. This began with the departure of Chris Martin, Chief Financial Officer, in February 2025, followed by the appointment of Brent Greetham. Our largest shareholder, Thalassa, requested Board representation and nominated Duncan Soukup for appointment as a Director. At the same time, Jon Glenn and Keyvan Djamanari informed the Board of their intention to step down as Chairman and Independent Non-Executive Directors respectively. Following these changes, we were pleased to welcome Roy Davis as Chair and Andrew Boteler as Independent Non-Executive Directors.

Roy brings more than 35 years of international leadership experience across the medtech, diagnostics and technology sectors. He currently serves as Chairman of Inspiration Healthcare Group plc and Foster & Freeman Ltd, and as a Non-Executive Director of Futura Medical plc. He is also a Senior Advisor to Moore Walker Partners.

Roy has previously held a number of chair roles within the healthcare sector, including at LunglifeAI plc, Medica Group plc until its sale in 2023, and Edinburgh Molecular Imaging Ltd and RAIR Health Ltd.

Prior to his non-executive career, Roy served as Chief Executive Officer of Optos plc from 2008 to 2016, stepping down following its acquisition by Nikon Corporation. Before that, he was Chief Executive Officer of Gyrus Group plc until its acquisition by Olympus Corporation in 2008, having previously served as Chief Operating Officer and earlier as a Non-Executive Director following its flotation in 1997.

Andrew brings more than 30 years' experience across Executive and Non-Executive roles in the financial sector. He currently serves as Non-Executive Director and Audit Committee Chair at Octopus AIM VCT plc and as Non-Executive Director and Audit Committee Chair at Cake Box Holdings plc. He was previously a Non-Executive Director and Chair of the Remuneration and Audit Committees at LunglifeAI plc, and has been a member of CEN Group Holdings' Advisory Panel since 2021.

Earlier in his executive career, Andrew served as Chief Financial Officer of Gooch & Housego PLC from 2009 to 2019 and as Finance Director of Riverford Organic Farmers from 2019 to 2023.

Roy has assumed the role of Chair of the Nomination Committee and is a member of the Remuneration and Audit Committees. Andrew has been appointed Chair of the Audit and Remuneration Committees and is a member of the Nomination Committee, with immediate effect.

Operational overview

People

Our employees are key to our business strategy, and we aim to attract, retain and develop talented individuals.

Supply chain

Although supply chain disruptions eased to some extent, challenges remained throughout 2025, particularly with prolonged lead times on components affecting production efficiency. However, strengthened relationships with key suppliers, supported by strategic investments in personnel, have led to noticeable improvements. A thorough review of these initiatives will continue into 2026 as part of the ongoing operational improvement plan.

Financial overview

Revenue

|

In 2025, the Group saw year over year revenues reduce to £11.6m, compared to £11.9m in the prior financial year.

Surgical Innovations Branded (SI Branded) product revenues saw a decline of 8% to £5.9m, compared to £6.4m in 2024; as a result of the impact of tariffs in the USA, sales structural challenges with partner in India and decline in bariatric procedures in the UK.

Distribution revenues encompass third-party products that complement the manufactured product portfolio. In 2025, this segment contributed 35% of the revenue, rising from 2024 levels (30%).

OEM sales experienced a projected decline from £1.9m in 2024 to £1.7m in 2025 - the 2024 number included the clearance of the backorder position and was further impacted by a quality issue with a component supplied by an OEM partner. However, a new agreement with long term partner, AMS, and strong forecasts from partners will provide growth in 2026.

|

|

|

Our sustainability messaging continues to drive significant growth across Europe. Strong sales of distribution products in the UK highlight the strength of our relationships with key suppliers and reinforce the success of our strategy to focus on high-quality, complementary technologies. Slower sales in OEM meant an overall decline in the UK.

Tariffs in the US and structural challenges in India have created headwinds in several key markets.

|

|

Margins

|

For margin analysis, the Group has divided the assessment between the underlying gross margin and the overall contribution margin.

The net cost of manufacturing reflects the shortfall in recovering both fixed and variable costs, encompassing both direct and indirect expenses.

The underlying gross margins have increased to 33.73% (2024: 30.65%).

We continue to focus upon our manufacturing operations including our supply chain, on an ongoing basis.

Furthermore, given the mounting pressure on both direct and indirect costs, a thorough review of absorption rates has been undertaken. |

|

Use of adjusted measures

Adjusted KPIs are used by the Board to understand underlying performance and exclude items which distort comparability, as well as being consistent with broker forecasts and measures. The method of adjustments is consistently applied but is not defined in International Financial Reporting Standards (IFRS) and, therefore, are considered to be non-GAAP (Generally Accepted Accounting Principles) measures. Accordingly, the relevant IFRS measures are also presented where appropriate.

|

EBITDA is defined as earnings before interest, taxation, depreciation and amortisation including impairment).

Adjusted EBITDA serves as a key measure of business performance, offering insight into the underlying performance of the Group. This metric excludes items that may distort comparability, such as the charge for share-based payments, which is a non-cash expense typically excluded from market forecasts.

Adjusted EBITDA loss of £0.4m in 2025, compared to an adjusted EBITDA profit of £0.05m in 2024.

|

|

Financial position

Capital expenditure on tangible assets remained consistent with prior year, amounting to £0.2m in 2025 (2024: £0.1m). The Group remains committed to reviewing its capital expenditure and will continue to enhance its investment plans. A review of the business priorities and operational improvements will guide our focus in this area as we move further into 2026.

Investment in new product development continues, with expenditure in the year of £0.2m (2024: £0.3m). While the business remains committed to research and development, in 2025 we recognised an impairment charge of £0.15m against capitalised development costs (2024: £1.16m), bringing the carrying value to £nil at the end of both financial years.

A review of the goodwill arising from the acquisition of Elemental Healthcare Ltd was conducted to assess further impairment. The trading environment in the UK market is strong and based on this assessment, the recoverable amount of the CGU is deemed to exceed it carrying value.

The presence of several impairment indicators within the business this year necessitated a broader consideration of asset impairment beyond goodwill. A review of the CGU of Surgical Innovations Ltd was conducted, and based on the assessment, the amount of the CGU exceeds its recoverable amount.

Working capital

Inventory levels continue to be managed, adopting a lean methodology across operations, whilst ensuring there is no risk to operational output or satisfying customer orders. Inventory holdings were £2.2m at the year-end (2024: £3.0m).

Trade receivables remained consistent at £1.6m at the year-end (2024: £1.7m), with minimal risk associated with overdue balances. Trade payables increased over the same period to £1.4m (2024: £1.1m).

Net cash inflow from operations amounted to £0.6m (2024: £0.1 outflow). The Group concluded the year with net debt balances of (£0.3m) (2024: (£0.3m)). Net cash balances consists of cash at bank, less bank borrowings and invoice financing facilities in use.

The Group recorded a corporation tax credit of £0.05m in the year. (2024: credit of £0.1m). Overall, the Group continues to hold substantial tax losses on which it holds a cautious view, and consequently the Group has chosen not to recognise those losses.

Key Performance Indicators ("KPIs")

The Group considers the key performance indicators of the business to be:

|

|

|

2025 |

2024 |

Target Measure |

|

Underlying Gross Profit Margin |

Gross profit / revenue |

33.7% |

30.6% |

>40% |

|

Direct Gross Profit Margin |

Contribution margin / revenue |

26.3% |

28.8% |

>40% |

|

Net Debt |

Cash less debt |

(£0.3m) |

(£0.3m) |

N/A |

|

Adjusted EBITDA |

|

(£0.4m) |

£0.05m |

NA |

The Group also considers non-financial KPI's as part of its ongoing review of business performance. These include but are not limited to operational efficiencies, employee metrics and environmental metrics, as referenced in the Environmental, Social and Governance section of the Annual Report.

Earnings per share

|

Earnings per share |

2025 |

2024 |

|

Basic EPS |

(0.10p) |

(0.21p) |

|

Loss attributable to shareholders |

(£0.89m) |

(£1.94m) |

|

Add: Share based payments |

£0.00m |

£0.00m |

|

Add: other expense/non-recurring items |

£0.00m |

£0.15m |

|

Add: impairment loss |

£0.15m |

£1.16m |

|

Adjusted loss attributable to shareholders |

(£0.74m) |

(£0.63m) |

|

Adjusted EPS |

(0.08p) |

(0.07p) |

Principal risks and uncertainties

The management of the business and the nature of the Group's strategy are subject to a number of risks which the Directors seek to mitigate wherever possible. The principal risks are set out below.

|

Issue |

Indication of risk on prior year |

Risk and description |

Mitigating actions |

|

Margin constraints due to operational challenges |

Risk increased on prior year |

The Group encountered operational inefficiencies.

|

The Company continues to review its manufacturing operations and supply chain to identify opportunities for improvement. Measures have already been implemented; including an internal restructuring designed to drive operational savings, enhance efficiencies and boost productivity.

|

|

Customer concentration

|

Existing risk remains at the same level from prior year |

The Group exports to over thirty countries and distributors around the world, but certain distributors are material to the financial performance and position of the Group. (As disclosed in note 2 to the financial statements, one customer accounted for 11% of revenue in 2025 and the loss, failure or actions of this customer could have a severe impact on the Group). |

The majority of distributors, including the most significant, are well established and their relationship with the Group spans many years. Credit levels and cash collection is closely monitored by management, and issues are quickly elevated both within the Group and with the distributor. |

|

Regulatory approval

|

Existing risk remains at the same level from prior year |

As an international business a significant proportion of the Group's products require registration from national or federal regulatory bodies prior to being offered for sale. The majority of our major product lines have FDA approval in the US and we are therefore subject to MDSAP audit and inspection of our manufacturing facilities.

There is no guarantee that any product developed by the Group will obtain and maintain national registration or that the Group will always pass regulatory audit of its manufacturing processes. Failure to do so could have severe consequences upon the Group's ability to sell products in the relevant country.

The Group has now received MDR Certification on all products groups. |

The Group has a dedicated Compliance department which assists product development teams with support as required to minimise the risk of regulatory approval not being obtained on new products and ensures that the Group operates processes and procedures necessary to maintain relevant regulatory approvals.

Whilst there is no guarantee that this will be sufficient, the Group has invested in people with the appropriate experience and skills in this area which mitigates this risk significantly.

|

|

Economic factors

|

Existing risk remains at the same level from prior year |

The business has been affected by rising employment costs and raw material expenses, and it is acknowledged that these pressures are likely to persist into 2026.

There are also pressures upon labour costs, because of the 4.1% increase in the National Living Wage in 2026.

Supply chain delays in both raw materials and finished goods have affected the business throughout 2025, though the impact has been less severe compared to the previous year. Some disruption is expected in 2026.

U.S. tariffs introduce near-term complexity.

|

Raw material purchases undergo a continual review, with economies of scale applied. Investment in the supply chain will yield benefits through enhanced supplier relations, while more effective inventory management will mitigate further exposure.

Increases in the cost of goods are mitigated and passed on where possible.

As a result of the introduction of tariffs by the US, and the evolving nature of these tariffs, current global trade realignments are, on balance, creating competitive advantages for our UK-based manufacturing. Our supply chain remains well-positioned to navigate this evolving landscape with minimal disruption anticipated, and the potential for market share gains |

David Marsh

CEO

21 April 2026

|

Consolidated statement of comprehensive income for the year ended 31 December 2025

|

|

|

||

|

|

|

2025 |

2024 |

|

|

|

Notes |

£'000 |

£'000 |

|

|

Revenue |

2 |

11,602 |

11,945 |

|

|

Cost of sales |

|

(8,549) |

(8,509) |

|

|

Gross profit |

|

3,053 |

3,436 |

|

|

Other operating expenses |

|

(3,781) |

(4,227)

|

|

|

Operating loss |

3 |

(728) |

(791) |

|

|

Impairment costs |

|

(150) |

(1,160) |

|

|

Finance costs |

|

(66) |

(99) |

|

|

Loss before taxation |

|

(944) |

(2,050) |

|

|

Taxation credit |

|

49 |

107 |

|

|

Loss and total comprehensive income |

|

(895) |

(1,943) |

|

|

Loss per share, total and continuing |

|

|

|

|

|

Basic |

|

(0.10p) |

(0.21p) |

|

|

Diluted |

|

(0.10p) |

(0.21p) |

|

|

|

|

|

|

|

The Consolidated statement of comprehensive income above relates to continuing operations.

Loss and total comprehensive income relate wholly to the owners of the parent Company.

Consolidated statement of changes in equity

for the year ended 31 December 2025

|

|

|

Share |

Share |

Capital |

Merger |

Retained |

|

||||||

|

|

|

capital |

premium |

reserve |

reserve |

earnings |

Total |

||||||

|

|

|

£'000 |

£'000 |

£'000 |

£'000 |

£'000 |

£'000 |

||||||

|

Balance as at 1 January 2024 |

|

9,328 |

6,587 |

329 |

1,250 |

(7,010) |

10,484 |

||||||

|

Share based payment |

|

- |

- |

- |

- |

- |

- |

||||||

|

Total - transactions with owners |

|

- |

- |

- |

- |

|

|

||||||

|

Profit and total comprehensive income for the period |

|

- |

- |

- |

- |

(1,943) |

(1,943) |

||||||

|

Balance as at 31 December 2024 |

|

9,328 |

6,587 |

329 |

1,250 |

(8,953) |

8,541 |

||||||

|

Share based payment |

|

- |

- |

- |

- |

- |

- |

||||||

|

Total - transactions with owners |

|

- |

- |

- |

- |

- |

- |

||||||

|

Loss and total comprehensive income for the period |

|

- |

- |

- |

- |

(895) |

(895) |

||||||

|

Balance as at 31 December 2025 |

|

9,328 |

6,587 |

329 |

1,250 |

(9,848) |

7,646 |

||||||

|

|

|

|

|

|

|

|

|

|

|||||

The merger reserve arose from a business combination in 2017.

|

Consolidated balance sheet at 31 December 2025 |

|

||

|

|

|

2025 |

2024

|

|

|

|

|

|

|

|

Notes |

£'000 |

£'000 |

|

Assets |

|

|

|

|

Non-current assets |

|

|

|

|

Property, plant, and equipment |

|

632 |

701 |

|

Right-of-use assets |

|

490 |

794 |

|

Intangible assets |

|

5,423 |

5,423 |

|

|

|

6,545 |

6,918 |

|

Current assets |

|

|

|

|

Inventories |

|

2,193 |

2,969 |

|

Trade and other receivables |

|

2,090 |

2,156 |

|

Cash at bank and in hand |

|

813 |

195 |

|

|

|

5,096 |

5,320 |

|

Total assets |

|

11,641 |

12,238 |

|

Equity and liabilities |

|

|

|

|

Equity attributable to equity holders of the parent company |

|

|

|

|

Share capital |

|

9,328 |

9,328 |

|

Share premium account |

|

6,587 |

6,587 |

|

Capital reserve |

|

329 |

329 |

|

Merger reserve |

|

1,250 |

1,250 |

|

Retained earnings |

|

(9,848) |

(8,953) |

|

Total equity |

|

7,646 |

8,541 |

|

Non-current liabilities |

|

|

|

|

Borrowings |

5 |

- |

150 |

|

Dilapidation provision |

|

270 |

165 |

|

Lease liability |

|

291 |

547 |

|

|

|

561 |

862 |

|

Current liabilities |

|

|

|

|

Trade and other payables |

6 |

2,804 |

1,603 |

|

Accruals |

|

256 |

689 |

|

Borrowings |

5 |

150 |

352 |

|

Lease liability |

|

224 |

191 |

|

|

|

3,434 |

2,835 |

|

Total liabilities |

|

3,995 |

3,697 |

|

Total equity and liabilities |

|

11,641 |

12,238 |

|

|

|

|

|

The accompanying accounting policies and notes form part of the financial statements.

|

Consolidated cash flow statement for the year ended 31 December 2025 |

|

|

|

|

|

|

2025

|

2024

|

|

|

|

£'000 |

£'000 |

|

Cash flows from operating activities |

|

|

|

|

Loss after tax for the year |

|

(895) |

(1,943) |

|

Adjustments for: |

|

|

|

|

Taxation |

|

(49) |

(107) |

|

Finance costs |

|

66 |

99 |

|

Depreciation of property, plant and equipment |

|

226 |

265 |

|

Amortisation and impairment of intangible assets |

4 |

166 |

1,374 |

|

Depreciation Right-of-Use assets |

|

266 |

213 |

|

Share-based payment charge |

|

- |

- |

|

Foreign exchange |

|

(3) |

(18) |

|

Decrease/(Increase) in inventories |

|

776 |

(115) |

|

Decrease/(Increase) in trade and other receivables |

|

66 |

(133) |

|

(Decrease)/Increase in payables and lease liabilities |

|

(33) |

283 |

|

Net cash generated from operations |

|

586 |

(82) |

|

Taxation received |

|

49 |

107 |

|

Interest paid |

|

(66) |

(99) |

|

Net cash (used in) / generated from operating activities |

|

569 |

(74) |

|

Cash flows from investing activities |

|

|

|

|

Payments to acquire property, plant and equipment |

|

(61) |

(67) |

|

Development cost additions |

4 |

(166) |

(268) |

|

Net cash used in investing activities |

|

(227) |

(335) |

|

|

|

|

|

|

Repayment of CBILS |

5 |

(352) |

(353) |

|

Drawdown on invoice financing facility |

5 |

936 |

- |

|

Repayment of lease liabilities |

|

(313) |

(273) |

|

Net cash used in financing activities |

|

(271) |

(626) |

|

|

|

|

|

|

Net decrease in cash and cash equivalents |

|

615 |

(1,035) |

|

Cash and cash equivalents at beginning of year |

|

195 |

1,212 |

|

Effective exchange rate fluctuations on cash held |

|

3 |

18 |

|

Cash and cash equivalents at end of year |

|

813 |

195 |

Notes to the consolidated financial statements

1. Group accounting policies under IFRS

(a) Basis of preparation

Surgical Innovations Group PLC (the "Company") is a public AIM listed company incorporated, domiciled and registered in England in the UK. The registered number is 02298163 and the registered address is Clayton Wood House, 6 Clayton Wood Bank, Leeds, LS16 6QZ.

The consolidated financial statements have been prepared in accordance with UK-adopted international accounting standards and with the requirements of the Companies Act 2006 and as applicable to companies reporting under IFRS. The preparation of financial statements in conformity with IFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the Group's accounting policies. The financial statements have been prepared under the historical cost convention, are presented in Sterling and are rounded to the nearest thousand.

Going concern

The Directors continue to adopt the going concern basis in the preparation of the financial statements.

The Directors have prepared forecasts for the period to April 2027 based on a full evaluation of the Group's trading activities and costs base, sensitised to reflect a rational judgement of the level of inherent risk.

The Board is satisfied that there is headroom including testing any sensitivities under reasonably possible scenarios, and the Directors conclude that it continues to be appropriate to prepare the Annual Report and Accounts on a going concern basis.

2. Segmental reporting

Information reported to the Board, as Chief Operating Decision Makers, and for the purpose of assessing performance and making investment decisions is organised into three operating segments. The Group's operating segments under IFRS 8 are as follows:

|

SI Brand |

- |

the research, development, manufacture and distribution of SI Branded minimally invasive devices. |

|

OEM |

- |

the research, development, manufacture and distribution of minimally invasive devices for third party medical device companies through either own label or co-branding. As well as Precision Engineering, the research, development, manufacture and sale of minimally invasive technology products for precision engineering applications. |

|

Distribution |

_ |

Distribution of specialist medical products sold through Elemental Healthcare Ltd.

|

The measure of profit or loss for each reportable segment is gross margin less amortisation of product development costs. Assets and working capital are monitored on a Group basis, with no separate disclosure of asset by segment made in the management accounts, and hence no separate asset disclosure is provided here. The following segmental analysis has been produced to provide a reconciliation between the information used by the chief operating decision maker within the business and the information as it is presented under IFRS

|

Year ended 31 December 2025 |

SI Brand £'000 |

Distribution |

OEM £'000 |

Total* |

|

Revenue |

5,891 |

4,054 |

1,657 |

11,602 |

|

Expenses |

(5,096) |

(2,134) |

(1,480) |

(8,710) |

|

Segment result |

795 |

1,920 |

177 |

2,892 |

|

Unallocated expenses |

|

|

|

(3,770) |

|

Other Income |

|

|

|

- |

|

Loss from operations |

|

|

|

(878) |

|

Finance income |

|

|

|

- |

|

Finance costs |

|

|

|

(66) |

|

Loss before taxation |

|

|

|

(944) |

|

Tax credit |

|

|

|

49 |

|

Loss for the year |

|

|

|

(895) |

|

*There were no revenues transactions between the segments during the year.

Included within the segment results are the following significant non-cash items:

cash items: |

|

|

|

|

|

Year ended 31 December 2025 |

SI Brand £'000 |

Distribution £'000 |

OEM £'000 |

Total £'000 |

|

Amortisation of intangible assets |

16 |

- |

- |

16 |

|

Impairment of intangible assets |

150 |

- |

- |

150 |

|

|

|

|

|

|

Unallocated expenses for 2025 include sales and marketing costs (£504,000), research and development costs (£1,263,000), central overheads (£1,230,000), Direct (Elemental Healthcare) sales & marketing overheads (£773,000), share based payments (£nil) and Other expensed/Non-recurring (£nil).

|

Year ended 31 December 2024 |

SI Brand £'000 |

Distribution |

OEM £'000 |

Total* £'000 |

|

Revenue |

6,373 |

3,625 |

1,947 |

11,945 |

|

Expenses |

(5,765) |

(2,171) |

(1,786) |

(9,722) |

|

Segment result |

608 |

1,454 |

161 |

2,223 |

|

Unallocated expenses |

|

|

|

(4,173) |

|

Other income |

|

|

|

- |

|

(Loss) from operations |

|

|

|

(1,950) |

|

Finance income |

|

|

|

- |

|

Finance costs |

|

|

|

(99) |

|

(Loss) before taxation |

|

|

|

(2,049) |

|

Tax charge |

|

|

|

107 |

|

(Loss) for the year |

|

|

|

(1,943) |

*There were no revenues transactions between the segments during the year.

|

Included within the segment results are the following significant non-cash items: |

|

|||

|

Year ended 31 December 2024 |

SI Brand £'000 |

Distribution £'000 |

OEM £'000 |

Total £'000 |

|

Amortisation of intangible assets |

214 |

- |

- |

214 |

|

Impairment of intangible assets |

1,160 |

- |

- |

1,160 |

Unallocated expenses for 2024 include sales and marketing costs (£664,000), research and development costs (£1,149,000), central overheads (£1,298,000), Direct (Elemental Healthcare) sales & marketing overheads (£909,000), share based payments (£nil) and Other expensed/Non-recurring (£153,000).

Disaggregation of revenue

The Group has disaggregated revenues in the following table:

|

Year ended 31 December 2025 |

SI Brand £'000 |

Distribution £'000 |

OEM £'000 |

Total £'000 |

|

United Kingdom |

1,604 |

4,054 |

1,291 |

6,949 |

|

Europe |

2,082 |

- |

- |

2,082 |

|

US |

793 |

- |

366 |

1,159 |

|

APAC1 |

969 |

- |

- |

969 |

|

Rest of World |

443 |

- |

- |

443 |

|

Total |

5,891 |

4,054 |

1,657 |

11,602 |

|

Year ended 31 December 2024 |

SI Brand £'000 |

Distribution £'000 |

OEM £'000 |

Total £'000 |

|

United Kingdom |

1,998 |

3,625 |

1,779 |

7,402 |

|

Europe |

1,726 |

- |

- |

1,726 |

|

US |

957 |

- |

168 |

1,125 |

|

APAC1 |

1,158 |

- |

- |

1,158 |

|

Rest of World |

534 |

- |

- |

534 |

|

Total |

6,373 |

3,625 |

1,947 |

11,945 |

1. APAC-Asia Pacific

Revenues are allocated geographically on the basis of where revenues were received from and not from the ultimate final destination of use. During 2025 £1,284,000 (11.0%) of the Group's revenue depended on one distributor in the OEM segment (2024: £1,788,000 (15.0%)), and £783,000 (7.0%) in the SI Brand segment (2024: £840,000 (7.0%)).

Sales of goods were £11,602,000 (2024: £11,945,000) and sales relating to services in the UK were £Nil (2024: £Nil).

|

3. Operating loss

The operating loss for the year is stated after charging/(crediting): |

|

|

|

|

2025 £'000 |

2024 £'000 |

|

Depreciation of owned assets |

226 |

265 |

|

Amortisation of capitalised development costs |

166 |

214 |

|

Depreciation of Right-of-use assets |

266 |

213 |

|

Research expenses |

1,263 |

1,149 |

|

Foreign exchange losses |

(3) |

(18) |

|

Auditor's remuneration: |

|

|

|

- fees payable to the Company's auditor for the audit of the Company's annual financial statements |

70 |

54 |

|

Other expensed items - non-recurring costs |

- |

153 |

Other expensed items

These are expenses or a group of expenses that are considered non-recurring in nature, as determined by the Directors. They are believed to warrant separate identification in the financial statements to provide readers with a clear understanding of the underlying trading performance of the business.

Non-recurring costs

Severance costs related to restructuring activities in 2024 of £153,000.

|

Other operating expenses comprised: |

|

2024 |

|

|

£'000 |

£'000 |

|

|

|

|

|

Sales & marketing |

504 |

664 |

|

Direct (Elemental Healthcare) sales & marketing overheads |

773 |

909 |

|

Administrative expenses |

1,225 |

1,138 |

|

Research expenses |

1,263 |

1,149 |

|

Other expensed items- nonrecurring |

- |

153 |

|

Share based payments |

- |

- |

|

Amortisation |

166 |

214 |

|

Total |

3,931 |

4,227 |

|

4. Intangible assets |

Capitalised development costs |

Single use product knowledge transfer |

Goodwill |

Exclusive Supplier Agreements |

Total |

|

|

£'000 |

£'000 |

£'000 |

£'000 |

£'000 |

|

Cost |

|

|

|

|

|

|

At 1 January 2024 |

14,970 |

225 |

8,180 |

1,799 |

25,174 |

|

Additions |

268 |

- |

- |

- |

268 |

|

At 1 January 2025 |

15,238 |

225 |

8,180 |

1,799 |

25,442 |

|

Additions |

166 |

- |

- |

- |

166 |

|

At 31 December 2025 |

15,404 |

225 |

8,180 |

1,799 |

25,608 |

|

|

|

|

|

|

|

|

Accumulated amortisation and impairment |

|

|

|

|

|

|

At 1 January 2024 |

(13,864) |

(225) |

(2,757) |

(1,799) |

(18,645) |

|

Charge for the year

|

(214) |

- |

- |

- |

(214) |

|

Impairment loss |

(1,160) |

- |

- |

- |

(1,160) |

|

At 1 January 2025 |

(15,238) |

(225) |

(2757) |

(1,799) |

(20,019) |

|

Charge for the year |

(16) |

- |

- |

- |

(16) |

|

Impairment loss |

(150) |

- |

- |

- |

(150) |

|

At 31 December 2025 |

(15,404) |

(225) |

(2757) |

(1,799) |

(20,185) |

|

Carrying amount |

|

|

|

|

|

|

At 31 December 2025 |

- |

- |

5,423 |

- |

5,423 |

|

At 31 December 2024 |

- |

- |

5,423 |

- |

5,423 |

Goodwill and intangibles are allocated to the cash generating unit (CGU) that is expected to benefit from the use of the asset.

Capitalised development costs

Capitalised development costs represent expenditure incurred in developing new products that fulfil the requirements met for capitalisation as set out in paragraph 57 of IAS38. These costs are amortised over the future commercial life of the product, commencing on the sale of the first commercial item, up to a maximum product life cycle of ten years, and taking account of expected market conditions and penetration.

Goodwill

The Group tests goodwill at each reporting date for impairment and whenever events or changes in circumstances indicate that the carrying value may not be recoverable. The recoverable amount of a cash generating unit (CGU) is determined based on value in use calculations. These calculations use cash flow projections based on five-year financial budgets approved by management. Cash flows beyond the five-year period are extrapolated using estimated long term growth rates.

An impairment review is carried out annually for goodwill. Goodwill arose on the acquisition of Elemental Healthcare Limited in 2017 and is related to both the Distribution and SI Brand segments of the Group. Elemental Healthcare Limited is considered to be a separate cash-generating unit (CGU) of the Group whose recoverable amount has been calculated on a value in use basis by reference to discounted future cash flows over a five-year period plus a terminal value. Principal assumptions underlying this calculation are the growth rate into perpetuity of 2.5% and a pre-tax discount rate of 17% (2024:18%) applied to anticipated cash flows. In addition, the value in use calculation assumes a gross profit margin of 45% increasing to 47% over the 5-year period using past experience of sales made and future sales that were expected at the reporting date based on anticipated market conditions.

The Group has conducted a sensitivity analysis on the impairment test of the CGU. Assuming no change to other assumptions, the discount rate can increase by 15% before an impairment would result.

Impairment losses in the year

During the year, as a result of losses in the Surgical Innovations Limited cash generating unit ('CGU'), the group carried out a review of the recoverable amount of the assets in this CGU. This CGU comprises the SI Brand and OEM segments. Based on the results of the CGU impairment assessment which has been undertaken using a value in use model, an impairment loss in respect of the capitalised development costs of £0.15m (2024: £1.16m) was recognised. The other assets in scope of the impairment assessment, being the property plant and equipment, were concluded to have a fair value less cost of disposal in excess of the carrying value and no impairment in respect of these assets has been recognised. Principal assumptions underlying this calculation are the growth rate into perpetuity of 2.5% and a pre-tax discount rate of 17% applied to anticipated cash flows. In addition, the value in use calculation assumes a gross profit margin of 21% increasing to 26% over the 5 year period using past experience of sales made and future sales that were expected at the reporting date based on anticipated market conditions.

|

5. Borrowings |

2025 |

2024 |

|

Bank Loan |

£'000 |

£'000 |

|

Current liabilities |

150 |

352 |

|

Non-current liabilities |

- |

150 |

|

Lease liabilities |

|

|

|

Current liabilities |

224 |

191 |

|

Non-current liabilities |

291 |

547 |

|

Total |

665 |

1,240 |

Borrowings include the following:

· CBILS repayable in May 2026. Interest is calculated at rate of 2.94% repayable monthly over the Bank of England base rate.

· Covenants attached to the CBILS comprise of EBITDA to debt servicing costs at a minimum of 1.25x.

· Invoice Discounting facility of £1.0m across the Group. 2.5% on margin with a maximum of nominal administration fee of a maximum of £0.018m if not utilised.

· In March 2024, the bank extended its support by resetting the testing parameters. They excluded 31 March 2024 and initiated the rolling test from June 2024, based on EBITDA being 1x the debt service. Subsequent testing periods included September 2024 (1x, on a 6-month rolling basis), December 2024 (1.25x, on a 9-month rolling basis), and then on a 12-month rolling basis thereafter.

|

Changes in liabilities arising from financing activities |

Non-current loans and borrowings

£'000 |

Current loans and borrowings

£'000 |

Total

£'000 |

|

|

|

|

|

|

At 1 January 2024 |

502 |

353 |

855 |

|

Cash flows for repayment of CBILS |

- |

(353) |

(353) |

|

Transfer between non-current and current |

(352) |

352 |

- |

|

Interest paid in the period |

- |

(59) |

(59) |

|

Interest accrued in the period |

- |

59 |

59 |

|

At 31 December 2024 |

150 |

352 |

502 |

|

Cash flows for repayment of CBILS |

- |

(352) |

(352) |

|

Transfer between non-current and current |

(150) |

150 |

- |

|

Interest paid in the period |

- |

(28) |

(28) |

|

Interest accrued in the period |

- |

28 |

28 |

|

At 31 December 2025 |

- |

150 |

150 |

|

6. Trade and other payables |

2025 £'000 |

2024 £'000 |

|

Trade payables |

1,416 |

1,137 |

|

Other tax and social security |

152 |

193 |

|

Other payables |

298 |

238

|

|

Invoice financing |

938 |

35 |

|

Total |

2,804 |

1,603 |

The Group and Company's financial liabilities have contractual maturities (including interest payments where applicable) which are summarised below.

|

|

Amounts due in |

Amounts due in |

Amounts due in |

|

|

As at 31 December 2025 |

less than 1 year £'000 |

2-5 years

£'000 |

5-10 years

£'000 |

Total financial liabilities £'000 |

|

Trade payables |

1,416 |

- |

- |

1,416 |

|

Invoice financing facility |

938 |

- |

- |

938 |

|

Bank borrowings-Current |

150 |

- |

- |

150 |

|

Bank borrowings-Non-current |

- |

- |

- |

- |

|

Total |

2,504 |

- |

- |

2,504 |

|

|

Amounts due in |

Amounts due in |

Amounts due in |

|

|

As at 31 December 2024 |

less than 1 year £'000 |

2-5 years

£'000 |

5-10 years

£'000 |

Total financial liabilities £'000 |

|

Trade payables |

1,137 |

- |

- |

1,137 |

|

Other payables |

238 |

- |

- |

238 |

|

Bank borrowings-Current |

352 |

- |

- |

352 |

|

Bank borrowings-Non-current |

- |

150 |

- |

150 |

|

Total |

1,727 |

150 |

- |

1,877 |

15. Share capital

|

|

2025 £'000 |

2024 £'000 |

|

Authorised, allotted, called up and fully paid 932,816,177 ordinary shares of 1p each (2024: 932,816,177) |

9,328 |

9,328 |

|

|

|

|

Shares in issue reconciliation:

|

|

2025 |

2024 |

|

Opening no of shares in issue |

932,816,177 |

932,816,177 |

|

Issued in satisfaction of share options exercised |

- |

- |

|

Closing number of shares in issue |

932,816,177 |

932,816,177 |

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.

Latest directors dealings

- 26 minutes ago Redcentric

- 1 hour ago Ocado Group

- 1 hour ago RWS Holdings

- 2 hours ago Molten Ventures

- 3 hours ago Sunda Energy