Final Results for the year ended 31 December 2025

Summary by AI BETAClose X

15 May 2025

Logistics Development Group plc

("LDG" or the "Company")

Final Results for the year ended 31 December 2025

Logistics Development Group plc, the AIM listed investing company, announces its audited final results for the year ended 31 December 2026.

Year ended 31 December 2025 Results Summary

· For the financial year, the Company reported an underlying EBIT1 profit of £14.6m (2024: profit of £18.4m) and a profit before tax of £15.0m (2024: profit before tax of £19.8m).

· On 10 January 2025, DBAY announced a recommended offer for the entire share capital of Alliance Pharma plc of 62.50p per share representing a 14% increase in value per share compared to LDG's average purchase price and a 37% premium to the valuation as at 31 December 2024. On 10 March 2025, DBAY announced an increase in its offer to 64.75p per share, representing an 18% increase in value per share compared to LDG's average purchase price and a 42% premium to the valuation as at 31 December 2024. The offer, conducted as a scheme of arrangement, became effective on 14 May 2025.

· On 17 March 2025, LDG announced its portfolio data, pursuant to its announced plan to publish quarterly net asset value ("NAV") data. As at 31 December 2024, LDG's unaudited estimated NAV per share was 22.3p. An update on the investments was also provided, along with a distribution update in that LDG intended to launch a tender offer in the coming weeks.

· On 28 March 2025, LDG announced a proposed tender offer to return up to £21.0m to shareholders at a tender price of 19.00p per share (the "Tender Offer") through the purchase, by the Company, of up to 110,526,315 Ordinary Shares or approximately 21.08% of the voting share capital. At a general meeting of the Company, held on 22 April 2025, the Tender Offer approved by the shareholders and the Tender Offer closed that day. Valid tenders were received for basic entitlements in respect of 105,721,869 Ordinary Shares, which were satisfied in full. Valid excess tenders were scaled back such that the Tender Offer was implemented in full. The 110,526,315 Ordinary Shares tendered were repurchased by the Company and subsequently cancelled, pursuant to which the Company's issued share capital comprises 413,824,079 Ordinary Shares.

· On 18 July 2025, LDG announced an investment of £15m into WS Holdco, a private holding company of a group of companies ("the WS Holdco Group") formed by DBAY to create a national logistics platform in the UK. The WS Holdco Group had, to that date, acquired a 78.3% interest in The Alternative Parcels Company Ltd ("APC"), the UK's largest independent parcel delivery network.

· On 6 November 2025, LDG announced the appointment of Singer Capital Markets as its sole Corporate Broker.

· On 29 November, LDG announced its quarterly portfolio data. As at 30 September 2025, LDG's unaudited estimated NAV per share was 26.7p. The NAV was unchanged compared to the prior period being 30 June 2025. An update on the portfolio investments was also provided.

Events subsequent to the financial year end are detailed in the 'Business and financial review' section further below. As at 31 December 2025 LDG's unaudited estimated NAV per share was 26.7 pence.

[1]Underlying EBIT is an alternative performance measure (see Note 3) and is defined as profit/loss before interest and tax adding back exceptional items.

A copy of the full year results are also available to be viewed on, or downloaded from, the Company's corporate website at www.ldgplc.com. References to page numbers in this announcement are to pages in the Annual Report, which will be posted to shareholders in due course.

|

For Enquiries: |

|

Strand Hanson Limited (Financial and Nominated Adviser) +44 (0) 20 7409 34945 James Dance Richard Johnson Abigail Wennington

|

|

Singer Capital Markets (Corporate Broker) +44 (0) 20 7496 3000 James Maxwell - Corporate |

Letter from Chairman

Dear Shareholders

I present the annual report and audited financial statements for Logistics Development Group plc ("LDG") for the year ended 31 December 2025. For the financial year, the Company reported an underlying EBIT1 profit of £14.6m (2024: profit of £18.4m) and a profit before tax of £15.0m (2024: profit before tax of £19.8m).

With all that is going on in the world, there is little point in going into my thoughts for the future, so I will restrict this brief report to the events over the last year which you can see from pages 7 to 8 in the report.

Our Investment Manager, DBAY, have given an update as to the performance of our holdings and this can be found on pages 4 to 6.

I confirm that we continue to have an agreed formula for distributing cash to Shareholders on any future realisations and will continue to publish quarterly unaudited estimated net asset values. As at 31 December 2025 LDG's unaudited estimated net asset value per share was 26.7 pence.

I should also like to thank my fellow Directors for the time they have dedicated over the last year and should also like to thank David Facey, who has notified the Board that he will not be standing for re-election at this year's AGM, and wish him all the best for the future. The Board does not currently expect to seek a replacement director.

Adrian Collins

Chairman

Investment Manager's report

Against the backdrop of substantial macro volatility, Logistics Development Group's ("LDG" or "the Company") portfolio has demonstrated solid growth and strong profitability in 2025. The Company has invested in stable, "infrastructure-like" sectors (e.g. bakeries and consumer health) where AI-innovation is a clear cost reduction tailwind but is highly unlikely to disrupt their business models. With LDG now being fully invested, the focus has turned to driving value creation through improving go-to-market capabilities, right sizing overheads and strengthening management teams across the portfolio. Inorganic growth is also a key value-creation lever, with WS Holdco Limited ("WS Holdco") delivering well against an ambitious plan to scale through complementary bolt-on acquisitions. Overall, LDG's performance demonstrates the merits of a disciplined investment approach focused on cash generation, a degree of asset-backing and entering at attractive valuations.

At the reporting date, the fair value ascribed to the investments was £107.8m (2024: £87.2m) which reflects the current NAV of the underlying investments at the reporting date. Taking the portfolio as a whole, LDG's capital weighted entry multiple is 6.0x EV/EBITDA. As at 31 December 2025 LDG's portfolio is marked at 7.5x EV/EBITDA. We believe this benchmarks favourably against valuations of relevant comparable companies for the underlying assets, which typically transact in the 10-15x EV/EBITDA range.

Valuations for LDG portfolio companies are guided by the internal valuation process of our Investment Manager, which in turn is based on best practices set out by the International Private Equity and Venture Capital ("IPEV") Valuation Guidelines. The Investment Manager takes what it believes to be a conservative judgement by combining valuation and financial data points from a relevant set of comparable public companies and recent transactions. For up to twelve months following a take-private transaction the Investment Manager's policy is to hold the assets at the take-private price, however adequate consideration must be given to the facts and circumstances at the measurement date, including but not limited to, changes in the market or changes in the performance of the asset. Any value uplift is gradually recognised. Given the less certain macro environment, the Investment Manager has intentionally held portfolio company valuations broadly in line with their position 12 months ago. This is despite strong performance in all four businesses, and the attractive defensiveness of their respective end-markets. As a result, the Investment Manager believes that LDG's current valuations contain a significant buffer, leaving material upside to be captured upon eventual realisation of each investment.

The Company has been implementing its broader investing policy since its approval in January 2022. Fixtaia Limited ("Fixtaia") has been set up as the subsidiary vehicle for investments by the Company. All investments are held in Fixtaia. Details of the investments held at 31 December 2025 are listed below.

|

Underlying Investment |

LDG's economic interest % of the asset |

Additions / divestments in the three-month period to 31 December 2025 |

Total Investment at Cost |

Revenue latest financial year |

Latest Employees |

|

Finsbury Food Group Ltd (Private)

|

25.31% |

None |

£14m |

£445m (FY June 2025) |

c. 3,500 |

|

SQLI SA (Private)

|

10.73% |

None |

£13m |

€252m (FY December 2025, Unaudited)

|

c. 2,100 |

|

Alliance Pharma plc (Private)

|

24.54% |

None |

£39m |

£144m (FY December 2025, Unaudited) |

c. 290 |

|

WS Holdco Limited (private) |

42.60% |

None |

£15m |

N/A |

N/A |

|

Other Minority Interests |

2.71% |

None |

£2m |

N/A |

N/A |

Finsbury Food Group Limited ("Finsbury")

Status: Private (delisted) | Staff: ~3,500 | Operations: UK & Europe

FY25 Revenue: £445m (audited)

Take Private Date: Nov-23

Fixtaia Investment: £14m for 25.31% indirect equity stake

Overview

For the year ended 30 June 2025 Finsbury generated revenue of £445m from its speciality bakery business, producing and selling high-quality bread and cakes to food retailers and food service clients across the UK and Europe. Its product portfolio consists largely of either essential bakery products (e.g. organic & artisan bread, buns and rolls) or event-related purchases (e.g. brand-licensed celebration cakes for parties, especially for children).

Finsbury's largest retail bakery clients include supermarkets (e.g. Tesco, Co-op, Waitrose, Sainsbury's) and its largest foodservice clients include restaurants and coffee shops (e.g. KFC, Costa Coffee, Bidfood, Brakes). The company has long-standing licensing relationships manufacturing quality bread and cakes for global brands including Disney, Thorntons and Mars. The company was incorporated in 1925, is based in Cardiff and has 3,500 employees.

Performance & Outlook

For FY25 (30 June 2025), Finsbury reported revenue of £445m, delivering solid profitability. In FY25, revenue softened by 2% due to product rationalisation, but underlying profitability showed improvement year-on-year. The business is benefiting from price recovery, deflation in key inputs, and operational efficiency via the "Operating Brilliance" programme.

Management has reaffirmed its FY26 forecast, with revenue expected to increase both organically as well as inorganically, through the acquisition of Lola's Cupcakes in August 2025 - a premium cupcake and celebration cake business - which marked the company's entry into the direct-to-consumer market. Margins are expected to slightly decrease as the business invests in promotional activity before expanding again in FY27 as new capex projects come online. The company continues to pursue strategic M&A opportunities within the bakery and food manufacturing space.

SQLI S.A. ("SQLI")

Status: Private (delisted) | Employees: ~2,100 | Operations: France, DACH, Benelux, Morocco

FY25 Revenue: €252m (unaudited)

Take Private Date: Feb-22

Fixtaia Investment: £13m for 10.73% indirect equity stake

Overview

SQLI is a pan-European IT services business, with a leading position in e-commerce integration and digital experience (building and maintaining web shops). Addressing a growing market, SQLI differentiates through their technical capabilities and track record successfully serving blue-chip clients such as Nestlé, Airbus, LVMH, Miele, L'Oréal, Richemont, Rolex and Carlsberg. The business is headquartered in Paris, and employs 2,100 people across 13 countries, including an offshore delivery centre in Morocco.

Performance & Outlook

For FY25, SQLI reported unaudited revenue of €252m, up 2% and achieved margins of 10%, up 0.5 percentage points versus the prior year. In the context of a challenging market, SQLI's ability to grow revenues modestly in FY25 was a rare achievement among French and international peers, many of whom experienced declines. This reflects the strength of SQLI's end-to-end offering in e-commerce, and resilience of the company's blue-chip customer base. SQLI also continued to execute on operational improvements to enhance profitability. As a result, H2 2025 delivered the strongest half-year profitability in the company's history.

SQLI is building on this momentum by rolling out the new target operating model for 2026, which will further leverage AI to drive developer efficiency. The FY26 budget targets 3% revenue growth and a further 140bps margin expansion, supported by continued process optimisation and leadership transition momentum.

Alliance Pharma plc ("Alliance")

Status: Private (delisted) | Employees: ~280 | Operations: Global

FY25 Revenue: £144m (unaudited)

Take Private Date: May-25

Fixtaia Investment: £39m for 24.54% indirect equity stake

Overview

Alliance is a global business with c.280 staff engaged in the marketing and distribution of consumer healthcare products focused on scar treatment and healthy aging. Alliance owns market-leading products including Kelo-Cote™ (scar treatment) MacuShield™ (eye supplement) and Nizoral™ (medicated anti-dandruff shampoo), amongst a broad portfolio of other brands. Alliance's business model is asset-light, focused on marketing and distribution. Manufacturing and logistics are fully outsourced, and Alliance does not invest in capital intensive R&D. The Company markets its products in 100+ countries, with core markets being the US, China, UK, France and Germany.

Performance & Outlook

On 10 January 2025, DBAY announced a recommended offer for the entire share capital of Alliance of 62.50p per share representing a 14% increase in value per share compared to LDG's average purchase price and a 37% premium to the valuation as at 31 December 2024. On 10 March 2025, DBAY announced an increase in its offer to 64.75p per share, representing an 18% increase in value per share compared to LDG's average purchase price and a 42% premium to the valuation as at 31 December 2024. The offer, conducted as a scheme of arrangement, became effective on 14 May 2025.

Alliance finished the year in line with its management forecasts. FY25 revenue was £144m (unaudited), which includes the impact of a transaction to dispose of a portfolio of Alliance's small prescription brands to two strategic buyers. The transaction saw Alliance achieve an attractive multiple of revenue and EBITDA for the disposed business by running a competitive auction process. The transaction closed in January 2026, and the Alliance team is now focused on removing stranded costs. Proceeds were used to pay down Alliance debt, de-risking LDG's investment.

Significant progress was also made in optimising Alliance's go-to-market model in China, with the signing of a new domestic distributor for Kelo-Cote. This distributor specialises in e-commerce and is already performing ahead of plan. The budget for 2026 was finalised during Q4 2025 and is in line with DBAY's original investment case.

WS Holdco Limited ("WS Holdco")

Status: Private | Employees: ~1,000 | Operations: UK

FY25 revenue: Operations commenced during 2025

Acquisition Date: Nov-25

Fixtaia Investment: £15m for a 42.6% stake

Overview

As at 31 December 2025, WS Holdco consists of WS & Son (general transport), WS Digital (road forwarding services), APC (parcel delivery services), WS People Providers (logistics staffing agency) and WS Bis Henderson (logistics recruitment services). The vision is to build an end-to-end, integrated logistics service provider in the UK, covering road transport, forwarding, warehousing, fulfilment and parcel delivery services.

Performance & Outlook

Since WS Holdco was set-up in July 2025, the business has grown well, mainly via acquisitions, to reach over £300m of run-rate revenue by March 2026 year-end.

During the year, WS Holdco completed the acquisition of the WS companies (WS & Son, WS Digital and WS Bis Henderson) as per the business plan. After year-end, in March 2026, WS Holdco acquired EV Cargo Solutions and Distributions Limited, the UK managed transportation and contract logistics division of EV Cargo. Following an additional £10m investment by LDG and after this transaction, LDG's interest in WS Holdco is 50.7%.

WS & Son continues to target new potential customers and has further progressed several discussions with customers seeking to contract logistics services in 2026. Management expects to see structural growth in the outsourced logistics market, driven the UK net zero targets. Supply chain emissions are largest share of corporate footprint and are challenging to manage internally, driving business to specialised logistics providers with scale and expertise.

WS People Providers was established to provide staffing services to WS Holdco companies, and has already placed over 130 employees, eliminating the need for third-party staffing agencies and saving that margin. Once scaled, WS People Providers is expected to also target third-party customers.

In APC - the parcel delivery business - the cost saving and process improvement strategy has begun implementation and is expected to be completed by September 2026.

Finally, the business continues to actively evaluate several potential acquisitions that add scale and capabilities to WS Holdco, as the business works to reach its target of over £500m of revenue in the medium-term.

Business and financial review for the 12 Months to 31 December 2025

Review of the period

On 10 January 2025, DBAY announced a recommended offer for the entire share capital of Alliance of 62.50p per share representing a 14% increase in value per share compared to LDG's average purchase price and a 37% premium to the valuation as at 31 December 2024. On 10 March 2025, DBAY announced an increase in its offer to 64.75p per share, representing an 18% increase in value per share compared to LDG's average purchase price and a 42% premium to the valuation as at 31 December 2024. The offer, conducted as a scheme of arrangement, became effective on 14 May 2025.

On 17 March 2025, LDG announced its portfolio data, pursuant to its announced plan to publish quarterly NAV data. As at 31 December 2024, LDG's unaudited estimated NAV per share was 22.3p. An update on the investments was also provided, along with a distribution update in that LDG intended to launch a tender offer in the coming weeks.

On 28 March 2025, LDG announced a proposed tender offer to return up to £21.0m to shareholders at a tender price of 19.00p per share (the "Tender Offer") through the purchase, by the Company, of up to 110,526,315 Ordinary Shares or approximately 21.08% of the voting share capital. At a general meeting of the Company, held on 22 April 2025, the Tender Offer approved by the shareholders and the Tender Offer closed that day. Valid tenders were received for basic entitlements in respect of 105,721,869 Ordinary Shares, which were satisfied in full. Valid excess tenders were scaled back such that the Tender Offer was implemented in full. The 110,526,315 Ordinary Shares tendered were repurchased by the Company and subsequently cancelled, pursuant to which the Company's issued share capital comprises 413,824,079 Ordinary Shares.

On 18 July 2025, LDG announced an investment of £15m into WS Holdco, a private holding company of a group of companies ("the WS Holdco Group") formed by DBAY to create a national logistics platform in the UK. The WS Holdco Group had, to that date, acquired a 78.3% interest in The Alternative Parcels Company Ltd ("APC"), the UK's largest independent parcel delivery network.

On 6 November 2025, LDG announced the appointment of Singer Capital Markets as its sole Corporate Broker.

On 29 November, LDG announced its quarterly portfolio data. As at 30 September 2025, LDG's unaudited estimated NAV per share was 26.7 p. The NAV was unchanged compared to the prior period being 30 June 2025. An update on the portfolio investments was also provided.

Subsequent events

On 22 January 2026 LDG announced that Finsbury, in which LDG holds an economic 25.3% interest through the Company's wholly owned subsidiary Fixtaia, had completed a refinancing and subsequent return of capital. This resulted in £11.4m being received by Fixtaia, de-risking the Company's original capital investment to £2.8m of exposure (original investment: £14.2m). LDG's equity stake in Finsbury remains unchanged.

The Board of LDG agreed the reallocation of £10m (the "Investment") from the Finsbury return of capital to increase its investment in WS Holdco. Under the leadership of William Stobart, WS Holdco Group is pursuing a buy-and-build strategy aimed at creating a UK-focused national logistics platform. WS Holdco Group has also acquired 100% of William Stobart & Son Limited, which provides general transport and warehousing services; a 70% interest in WS Digital Freight Ltd, an asset-light road forwarding business; and a 60% interest in WS Bis Henderson Limited, which specialises in white-collar recruitment for the logistics industry.

The Investment was on the same terms as LDG's original investment of £15m in WS Holdco as detailed in the Company's announcement on 18 July 2025. As at 30 September 2025, LDG's interest in WS Holdco was 42.6% and increased to 51.3% after the further Investment. LDG's interest may change if additional equity is raised by WS Holdco and there is no certainty that LDG will participate in subsequent fundraises.

Alliance, in which LDG has invested £39.0m and holds an economic 24.5% interest, announced in December 2025 that it had disposed of its prescription products portfolio to two strategic buyers. The transaction closed in early January 2026 with proceeds contributing to a net debt reduction from £275m at the end of December 2025 to a forecast c. £175m at 31 March 2026. Following this transaction, the business is a pure-play consumer healthcare platform with market leading brands in damaged skin (especially scar and scalp care) and healthy aging.

On 27 February 2026, LDG announced its quarterly portfolio data. As at 31 December 2025, LDG's unaudited estimated NAV per share was 26.7p. The NAV remains unchanged compared to the prior period being 30 September 2025. The valuations of the portfolio companies mirror the valuations at which the assets are held in the DBAY private funds. Funds managed by DBAY are the lead investor in all LDG portfolio companies, and DBAY's management believes all portfolio companies are held at a conservative valuation. An update on the portfolio investments was also provided.

On 17 March 2026 LDG was notified by WS Holdco, its portfolio company, that it had acquired EV Cargo Solutions and Distribution Limited. Following this transaction, LDG's interest in WS Holdco is 50.7%.

Financial performance

The Directors consider the Company is an investment entity per IFRS 10 and measure its investments at fair value through profit and loss. The Company's investments are all held through Fixtaia.

Had the Company not met the definition of an investment entity; it would be required to prepare consolidated financial statements which involve presenting the results and financial position of the Company and Fixtaia as those of a single economic entity.

At the reporting date, the fair value ascribed to the investments was £107.8m (2024: £87.2m) which reflects the current NAV of the underlying investments at the reporting date. The Directors have reviewed this valuation approach and consider it to be appropriate.

Administrative expenses were broadly in line with the prior year at £1.3m (2024: £1.0m).

The Company's underlying EBIT[i] in the year was a profit of £14.6m (2024: profit of £18.4m) and statutory profit before tax was £15.0m (2024: profit before tax of £19.8m).

[1]Underlying EBIT is an alternative performance measure (see Note 3) and is defined as profit/loss before interest and tax adding back exceptional items.

Net cash

As at the reporting date, the Company has cash and cash equivalents of £2.2m (2024: £29.6m). Related party transactions amounted to £15m (2024: £0.1m). See note 14.

Exceptional items

During the year there were no exceptional items to report.

Tax

The Company is expected to have taxable profits in future periods and will be making use of existing tax losses. Therefore, a deferred tax asset has been recognised on this basis.

A tax liability of £Nil (2024: £0.8m) has been recognised in the period in relation to activities of Fixtaia. See note 7.

Dividends

The Company did not pay an interim dividend (2024: £Nil) and no final dividend is being recommended (2024: £Nil).

Earnings per share[ii]

Underlying basic and diluted earnings per share are both 3.3p (2024: underlying basic and diluted profit per share were both 3.5p). Statutory basic and diluted earnings per share are both 3.4p (2024: statutory basic and diluted profit per share were both 3.6p). See note 3 and 9.

2Earnings per share ("EPS") serves as an indicator of a company's profitability. EPS measures the amount of a company's profit on a per share basis (see notes 3 & 9).

Information about the Investment Manager

DBAY is an Isle of Man based asset management firm with offices in London and Douglas, Isle of Man. Founded in 2011, DBAY is owned by its partners and is licensed by the Isle of Man Financial Services Authority. The firm follows a value investing approach and invests in listed equities across Europe, as well as in private equity style control investments. The core DBAY team, who have worked together for over 20 years, have developed a diversified set of skills from financial and operational backgrounds, with deep insight into a number of industry sectors. DBAY comprises a team of 18 investment and operating professionals. Capital is managed on behalf of institutional investors, endowments, foundations, family offices and pension funds.

Investment Policy and Strategy

The investment objective of the Company is to provide shareholders with attractive total return achieved through capital appreciation and, when prudent, shareholder distributions or dividends.

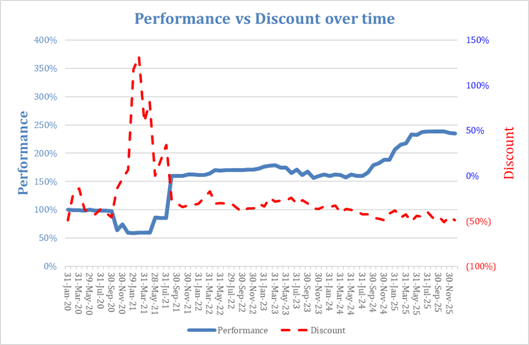

Performance = NAV per share indexed to 1.00 at the start of the series Discount = Share price's premium/discount to NAV per share

The Directors believe that opportunities exist to create significant value for shareholders through the acquisition of, and the implementation of substantial operational improvements in, businesses in the sectors outlined in the Company's Investing Policy.

The Investing Policy can be found on the website www.ldgplc.com.

DBAY is mandated with full authority to manage the Company's assets to deliver the investment strategy in accordance with LDG's Investing Policy set out below, reporting to the Board on a regular basis.

The Investing Policy, approved by shareholders on 31 January 2022, states that the Company will seek to achieve its investment objectives by making investments within the following parameters:

· Characteristics: investment primarily in undervalued companies, with a focus on companies that generate or have the potential to generate significant cash flows, where there is a high degree of revenue visibility and a strong and distinctive market position;

· Investment Type: investment in equity and equity related products, in both quoted and unquoted companies, and in the DBAY Investment Funds;

· Sectors: a broad range of sectors, such as business services including, amongst others, logistics, distribution, technology services, security and manufacturing, or in funds managed by DBAY which invest in the aforementioned sectors;

· Geography: there is no geographical restriction but expected to be primarily within the United Kingdom or the European Union;

· Ownership: will range from a minority position to 100%, non-operating ownership; and

· Restrictions: a maximum of 50% of the Company's NAV at the time the relevant investment is made, using the latest available management accounts of the Company, can be invested in DBAY Investment Funds. Investments made outside of the DBAY Investment Funds will be limited to 10% of NAV per investment (on the same basis), unless approved by the Board.

Investment Management Agreement amendments

An Investment Management Agreement was entered into on 14 January 2022. At the general meeting held on 31 January 2022, the Investment Management Agreement and amended investing policy was approved by shareholders. The changes were:

· DBAY will not receive management or performance fees from LDG in respect of funds committed to the DBAY Investment Funds by the Company. Fees will only be charged by the fund, to ensure there will be no double charging;

· DBAY have made a commitment to ensure that any DBAY Investment Funds in which the Company invests will retain investment policies that are substantially the same as the new investing policy of the Company;

· DBAY has made a commitment that it will provide the Company with an amount which is equal to the Company's reasonable corporate expenses in the given year, provided that such amount shall not exceed the lower of: (i) £800,000; or (ii) the management fees in respect of investments made and/or amounts committed by the Company which are received by DBAY in the relevant year; and

· DBAY will ensure that there is, at all times, a contingency amount of at least £2.0m on the Company's balance sheet to cover any exceptional expenses that may arise in the future.

The Investment Management Agreement was further amended by way of an addendum dated 30 March 2023, to state that, with effect from the beginning of the current financial year, the maximum amount payable would not exceed the lower of (i) £800,000; and (ii) amounts paid to DBAY in respect of investments in DBAY Investment Funds specifically, and not all management fees received by DBAY.

The Investment Management Agreement automatically renews on 14 January 2027 for a further year and on each anniversary thereafter unless terminated with at least 30 days' written notice prior to the anniversary.

Annual general meeting

The Company intends to hold its Annual General Meeting on 18 June 2026 in London. Further details will be set out in the Notice of Meeting to be sent to shareholders in due course and published on our website www.ldgplc.com.

Company Statement of Comprehensive Income

for the year ended 31 December 2025

|

|

|

Year ended 31 December 2025 |

13 month period to 31 December 2024 |

|

|

Note |

£'000 |

£'000 |

|

Gain on investments measured at fair value through profit or loss - net |

10 |

15,862 |

19,336 |

|

Interest income |

4 |

428 |

1,384 |

|

Net finance income |

|

16,290 |

20,720 |

|

|

|

|

|

|

Administrative expenses |

|

(1,267) |

(968) |

|

Total administrative expenses |

|

(1,267) |

(968) |

|

|

|

|

|

|

Profit before tax |

|

15,023 |

19,752 |

|

|

|

|

|

|

Income tax credit/(expense) |

7 |

86 |

(932) |

|

|

|

|

|

|

Profit and total comprehensive income for the period |

|

15,109 |

18,820 |

|

|

|

|

|

|

|

|

|

|

|

Earnings per share |

|

|

|

|

Basic |

9 |

3.4p |

3.6p |

|

Diluted |

9 |

3.4p |

3.6p |

The accompanying notes form part of the financial statements.

Company Statement of Financial Position

as at 31 December 2025

|

|

|

31 December 2025 |

31 December 2024 |

|

|

Note |

£'000 |

£'000 |

|

Assets |

|

|

|

|

Non-current assets |

|

|

|

|

Investments at fair value through profit or loss |

10 |

107,775 |

87,228 |

|

Deferred tax asset |

7 |

514 |

428 |

|

|

|

108,289 |

87,656 |

|

Current assets |

|

|

|

|

Other receivables |

11 |

141 |

106 |

|

Cash and cash equivalents |

11 |

2,211 |

29,613 |

|

|

|

2,352 |

29,719 |

|

Total assets |

|

110,641 |

117,375 |

|

Current liabilities |

|

|

|

|

Amounts owed to related undertakings |

11 |

(1) |

(4) |

|

Current tax liability |

7 |

- |

(794) |

|

Other payables |

11 |

(233) |

(278) |

|

|

|

(234) |

(1,076) |

|

Total liabilities |

|

(234) |

(1,076) |

|

Net assets |

|

110,407 |

116,299 |

|

|

|

|

|

|

Equity |

|

|

|

|

Called up share capital |

12 |

4,138 |

5,244 |

|

Capital redemption reserve |

13 (i) |

1,480 |

- |

|

Retained earnings |

13 (ii) |

104,789 |

111,055 |

|

Total shareholders' funds |

|

110,407 |

116,299 |

|

|

|

|

|

The accompanying notes form part of the financial statements.

The Company Financial Statements on pages 29 to 41 were approved by the Board of Directors on 14 May 2026 and were signed on its behalf by:

Adrian Collins

Director

14 May 2026

Company number 08922456

Company Statement of Changes in Equity

for the year ended 31 December 2025

|

|

|

Share capital |

Capital redemption reserve |

Retained earnings |

Total |

|

|

|

£'000 |

£'000 |

£'000 |

£'000 |

|

Balance at 1 December 2023 |

|

5,331 |

- |

93,182 |

98,513 |

|

Profit for the period |

|

- |

- |

18,820 |

18,820 |

|

Share repurchase |

|

(87) |

- |

(947) |

(1,034) |

|

Balance at 31 December 2024 |

|

5,244 |

- |

111,055 |

116,299 |

|

Profit for the period |

|

- |

- |

15,109 |

15,109 |

|

Share repurchase (note 12) |

|

(1,106) |

- |

(19,895) |

(21,001) |

|

Transfer to capital redemption reserve (note 13) |

- |

1,480 |

(1,480) |

- |

|

|

Balance at 31 December 2025 |

|

4,138 |

1,480 |

104,789 |

110,407 |

The accompanying notes form part of the financial statements.

Company Cash Flow Statement

for the year ended 31 December 2025

|

|

|

Year ended 31 December 2025 |

13 month period to 31 December 2024 |

|

|

Note |

£'000 |

£'000 |

|

Cash flows from operating activities |

|

|

|

|

Profit for the period |

|

15,109 |

18,820 |

|

Adjustments for: |

|

|

|

|

Gain on investments measured at fair value through profit or loss - net |

10 |

(15,862) |

(19,336) |

|

Interest income |

|

(428) |

(1,384) |

|

Income tax (credit)/expense |

7 |

(86) |

932 |

|

Income tax paid |

|

(794) |

- |

|

Changes in: |

|

|

|

|

(Increase)/decrease in other receivables |

11 |

(35) |

191 |

|

Decrease in other payables |

11 |

(45) |

(73) |

|

Net outflow from operating activities |

|

(2,141) |

(850) |

|

Cash flows from investing activities |

|

|

|

|

Purchase of investment |

10 |

(4,685) |

(12,500) |

|

Amounts owed to related undertakings |

11 |

(3) |

(31) |

|

Net cash outflow from investing activities |

|

(4,688) |

(12,531) |

|

Cash flows from financing activities |

|

|

|

|

Share repurchase |

12 |

(21,001) |

(1,034) |

|

Interest income |

4 |

428 |

1,384 |

|

Net cash outflow/inflow from financing activities |

|

(20,573) |

350 |

|

Net decrease in cash and cash equivalents |

|

(27,402) |

(13,031) |

|

Cash and cash equivalents at the start of the financial period |

|

29,613 |

42,644 |

|

Cash and cash equivalents at the end of the financial period |

|

2,211 |

29,613 |

The accompanying notes form part of the financial statements.

Notes to the Company Financial Statements

for the year ended 31 December 2025

1. Basis of accounting

Logistics Development Group plc (the "Company") is a public company limited by shares and incorporated and domiciled in England, United Kingdom. Its registered address is 4th Floor, 3 More London Riverside, London, SE1 2AQ.

Basis of preparation

The Financial Statements were prepared in accordance with UK - adopted International Accounting Standards in conformity with the requirements of the Companies Act 2006 ("IFRS").

The Financial Statements are presented in pounds sterling, rounded to the nearest thousand, unless otherwise stated.

As at 31 December 2025, the Company has one subsidiary, Fixtaia Limited. As the Company is defined under IFRS10 as an Investment Entity, consolidation exemption allows the measuring of controlling interests in another entity at fair value through profit and loss.

The Financial Statements present Company only information for the current and comparative periods.

The Financial Statements were prepared under the historical cost convention, except for financial assets recognised at fair value through profit or loss, which have been measured at fair value. The Company is not registered for VAT and therefore all expenses are recorded inclusive of VAT.

Going concern

The Directors have a reasonable expectation that the Company has sufficient resources to continue in operation for the foreseeable future, a period of at least 12 months from the date of this report. The Directors have prepared a cash flow forecast to May 2027 which demonstrates that the group, LDG and Fixtaia, will have sufficient funds to meet its obligations as they fall due. Accordingly, the Directors consider it appropriate to continue to adopt the going concern basis of accounting in preparing the annual financial statements.

2. Material Accounting Policies

(a) Fair value measurement - the fair value measurement of the Company's investments utilises market observable inputs and data as far as possible. Inputs used in determining fair value measurements are categorised into different levels based on how observable the inputs used in the valuation technique utilised are (the "fair value hierarchy"):

- Level 1: Quoted prices in active markets for identical items (unadjusted);

- Level 2: Observable direct or indirect inputs other than Level 1 inputs; and

- Level 3: Unobservable inputs (i.e. not derived from market data and may include using multiples of trading results or information from recent transactions).

The classification of an item into the above levels is based on the lowest level of the inputs used that has a significant effect on the fair value measurement of the item. Transfers of items between levels are recognised in the period they occur.

(b) Financial instruments

- Financial assets - other receivables and amounts owed to related undertakings. Such assets are recognised initially at fair value plus any directly attributable transaction costs. Subsequent to initial recognition, such assets are measured at amortised cost using the effective interest method, less any impairment losses.

- Cash and cash equivalents - in the Statement of Financial Position, cash includes cash and cash equivalents excluding bank overdrafts. No expected credit loss provision is held against cash and cash equivalents as the expected credit loss is negligible.

(b) Financial instruments (continued)

- Financial liabilities - other payables and amounts owed to related undertakings. Such liabilities are initially recognised on the date that the Company becomes party to contractual provisions of the instrument. The Company derecognises a financial liability when its contractual obligations are discharged, cancelled or expire. Such financial liabilities are recognised initially at fair value less any directly attributable transaction costs. Subsequent to initial recognition, these financial liabilities are measured at amortised cost using the effective interest method.

- Share capital - Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of ordinary shares are recognised as a deduction from equity, net of any tax effects.

(c) Exceptional items - items that are material in size or nature and non-recurring are presented as exceptional items in the Statement of Comprehensive Income. The Directors are of the opinion that the separate recording of exceptional items provides helpful information about the Company's underlying business performance. Events which may give rise to the classification of items as exceptional include restructuring of business units and the associated legal and employee costs, costs associated with business acquisitions, impairments and other significant gains or losses.

(d) Alternative performance measures (APMs) - APMs, such as underlying results, are used in the day-to-day management of the Company, and represent statutory measures adjusted for items which, in the Directors' view, could influence the understanding of comparability and performance of the Company year on year. These items include non-recurring exceptional items and other material unusual items.

(e) Tax - tax expense comprises current and deferred tax. Current tax and deferred tax are recognised in profit or loss except to the extent that it relates to items recognised directly in equity or in other comprehensive income. Deferred tax assets are recognised only to the extent that it is probable that future taxable profit will be available against which the temporary differences can be utilised.

(f) Operating segments - the Company has a single operating segment on a continuing basis, namely investment in a portfolio of assets.

(g) Fund raise costs - transaction costs incurred in anticipation of an issuance of equity instruments are recorded as a deduction from the retained earnings reserve in accordance with IAS 32 and the Companies Act 2006.

(h) Translation of Foreign Currencies - Foreign currencies are translated into sterling at the rates of exchange ruling at the dates of the transactions. Assets and liabilities denominated in foreign currencies are translated into sterling at the rates of exchange ruling at the end of the financial period. Exchange differences are included in the Statement of Comprehensive Income.

New and amended IFRS Accounting Standards that are effective for the current year

The following new and revised accounting standards and amendments are effective for annual periods beginning

1 January 2025 which has been adopted for the first time by the Company.

· Amendments to IAS 21 The Effects of Changes in Foreign Exchange Rates: Lack of Exchangeability (Effective 1 January 2025)

There is no impact as the Company does not deal with any currencies that are not exchangeable.

There are no other standards and amendments that were newly effective during the year that have had a material impact on the Company.

A number of new standards, amendments to standards and interpretations are effective for annual periods beginning after 1 January 2026 and have not been applied in preparing these financial statements. The Company does not plan to early adopt these standards, and they are not thought to have a significant impact on the financial statements.

· Amendments to IFRS 9 and IFRS 7 Amendments to the Classification and Measurement of Financial Instruments (Effective 1 January 2026)

· Amendments to Annual Improvements to IFRS Accounting Standards - Volume 11 (Effective 1 January 2026)

· New accounting standard: IFRS 18 Presentation and Disclosures in Financial Statements* (Effective 1 January 2027)

· New accounting standard: IFRS 19 Subsidiaries without Public Accountability: Disclosures (Effective 1 January 2027)

New and amended IFRS Accounting Standards that are effective for the current year (continued)

*IFRS 18 will replace IAS 1 Presentation of Financial Statements and applies for annual reporting periods beginning on or after 1 January 2027 and introduces a number of new reporting requirements. The Company is still in the process of assessing the impact of the new standard, particularly with respect to the structure of the Company's statement of comprehensive income, the statement of cash flows and the additional disclosures required for management defined performance measures. The Company is also assessing the impact on how information is grouped in the financial statements, including for items currently labelled as 'other'.

None of the above listed changes are anticipated to have a material impact on the Company's financial statements.

Critical judgements in applying the Company's accounting policies

In applying the Company's accounting policies, the Directors have made the following judgements that have the most significant effect on the amounts recognised in the financial statements (apart from those involving estimations, which are dealt with below) and have been identified as being particularly complex or involve subjective assessments.

(i) Measurement of the investments - during the year, the Company measured its investment in Fixtaia at fair value through profit and loss.

The strategy of the Company as an AIM Investing Company is to generate value though holding investments for the short to medium term. Therefore, the Directors believe that the fair value method of accounting for the investment is in line with the strategy of the Company.

If the Company was not an AIM Investing Company, the investments in Fixtaia would have been accounted for as a subsidiary undertaking in consolidated financial statements.

(ii) Fair value of the investments - the Directors have recorded the current year investment in Fixtaia at fair value. All investments have, to date, for structuring purposes been held by Fixtaia. The fair value at the end of the period has been calculated on the basis of the net assets of Fixtaia. The net assets of Fixtaia consist of an investment in a listed entity, together with 4 private companies and cash/cash equivalents. The listed investment is carried at the quoted price as at 31 December 2025.

The Directors believe that this valuation approach represents the price the Company would expect to receive in an orderly transaction between market participants.

Key sources of estimation in applying the Company's accounting policies

If a market for a financial instrument is not active, then the Investment Manager establishes fair value using a valuation technique. Valuation techniques include using recent arm's length transactions between knowledgeable, willing parties (if available), reference to the current fair value of other instruments that are substantially the same, discounted cash flow analyses and option pricing models. The chosen valuation technique makes maximum use of market inputs, relies as little as possible on estimates, incorporates all factors that market participants would consider in setting a price, and is consistent with accepted economic methodologies for pricing financial instruments. Inputs to valuation techniques reasonably represent market expectations and measures of the risk-return factor inherent in the financial instrument. The Investment Manager calibrates valuation techniques and tests them for validity using prices from observable current market transactions in the same instrument or based on other available observable market data.

The best evidence of the fair value of a financial instrument at initial recognition is the transaction price which is the fair value of the consideration given or received, unless the fair value of that instrument is evidenced by comparison with other observable current market transactions in the same instrument (without modification or repackaging) or based on a valuation technique whose variables include only data from observable markets. When transaction price provides the best evidence of fair value at initial recognition, the financial instrument is initially measured at the transaction price and any difference between this price and the value initially obtained from a valuation model is subsequently recognised in the Statement of Comprehensive Income on an appropriate basis over the life of the instrument but not later than when the valuation is supported wholly by observable market data or the transaction is closed out.

3. Alternative performance measures reconciliations

Alternative performance measures (APMs), such as underlying results, are used in the day-to-day management of the Company, and represent statutory measures adjusted for items which, in the Directors' view, could influence the understanding of comparability and performance of the Company year on year. The reconciliation of APMs to the reported results is detailed below:

|

|

|

2025 |

2024 |

|

|

|

£'000 |

£'000 |

|

Profit |

|

15,109 |

18,820 |

|

Interest income |

|

(428) |

(1,384) |

|

Income tax (credit)/expense |

|

(86) |

932 |

|

Underlying EBIT |

|

14,595 |

18,368 |

|

|

|

|

|

|

|

|

2025 |

2024 |

|

|

|

(in thousands) |

(in thousands) |

|

Weighted average number of Ordinary Shares - Basic |

|

448,042 |

526,129 |

|

Weighted average number of Ordinary Shares - Diluted |

|

448,042 |

526,129 |

|

|

|

|

|

|

Underlying Basic earnings per share for total operations |

|

3.3p |

3.5p |

|

Underlying Diluted earnings per share for total operations |

|

3.3p |

3.5p |

4. Interest Income

Interest earned on deposit during 2025 amounted to £428k (2024: £1,384k).

5. Employees and Directors

Staff costs and the average number of persons (including Directors) employed by the Company during the period are detailed below:

|

|

|

|

|

2025 |

2024 |

|

|

|

|

|

£'000 |

£'000 |

|

Staff and Director costs for the Company during the period |

|

|

|

|

|

|

Wages and salaries |

|

|

276 |

255 |

|

|

Social security costs |

|

|

13 |

12 |

|

|

|

|

|

289 |

267 |

|

|

Average monthly number of employees and Directors |

|

|

|

|

|

|

Employees and Directors |

|

|

|

4 |

3 |

A summary of Directors' remuneration (key management personnel) is detailed below:

|

|

|

|

2025 |

2024 |

|

|

|

|

£'000 |

£'000 |

|

Emoluments, bonus and benefits in kind |

|

276 |

255 |

|

|

Total Directors' remuneration |

|

276 |

255 |

|

Remuneration of the highest paid Director is detailed below:

|

|

|

|

2025 |

2024 |

|

|

|

|

£'000 |

£'000 |

|

Emoluments, bonus and benefits in kind |

|

96 |

104 |

|

6. Audit fees

During the period, the Company obtained the following services from the Company's auditors, the costs of which (inclusive of VAT as the Company is not registered for VAT) are detailed below:

|

|

|

|

2025 |

2024 |

|

|

|

|

£'000 |

£'000 |

|

Fees payable for the audit of the Company's annual financial statements |

121 |

103 |

||

|

Fees payable for the audit of the Company's interim financial statements |

|

|

10 |

9 |

|

Total fees payable to Company's auditors |

|

|

131 |

112 |

7. Income tax

In 2025, the deferred tax asset of £514k (2024: £428k) is recognised, resulting in a deferred tax credit of £86k (2024: £932k expense) recognised in the income statement.

The income tax credit for the period included in the statement of comprehensive income can be reconciled to profit before tax multiplied by the standard rate of tax as follows:

|

|

2025 |

2024 |

|

|

£'000 |

£'000 |

|

Profit before tax |

15,023 |

19,752 |

|

Expected tax charge based on an effective corporation tax rate of 25% (2024: 25%) |

3,756 |

4,938 |

|

Effect of expenses not deductible in determining taxable profit |

124 |

21 |

|

Income not taxable |

(3,966) |

(4,834) |

|

Taxable interest income |

- |

795 |

|

Adjustments in respect of prior years |

- |

12 |

|

Income tax (credit)/expense |

(86) |

932 |

The main rate of corporation tax is 25% for the financial year beginning 1 April 2025 (previously 25% in the financial year beginning 1 April 2024). This main rate applies to companies with profits in excess of £250k. For profits below £50k, a lower rate of 19% is generally applicable.

Expenses not deductible consist of legal and professional fees relating to capital items for share buybacks.

Taxable interest income comprises interest income and loan redemption premium received by Fixtaia. As the Company was the original source of the loan, this income was treated as taxable in the UK and brought into charge in the prior period.

8. Dividends

At the date of approving these Financial Statements, no final dividend has been approved or recommended by the Directors (2024: £Nil).

9. Earnings per share

Basic earnings per share amounts are calculated by dividing profit for the period attributable to ordinary equity holders of the Company by the weighted average number of ordinary shares outstanding during the same period.

Diluted earnings per share amounts are calculated by dividing the profit attributable to ordinary equity holders of the Company by the weighted average number of ordinary shares outstanding during the year plus the weighted average number of ordinary shares that would be issued on conversion of all the potentially dilutive instruments into ordinary shares. The Company has no dilutive instruments to be included in the calculation.

|

|

|

2025 |

2024 |

|

|

|

£'000 |

£'000 |

|

Profit attributed to equity shareholders |

|

15,109 |

18,820 |

|

|

|

|

|

|

|

|

2025 |

2024 |

|

|

|

(in thousands) |

(in thousands) |

|

Weighted average number of Ordinary Shares - Basic |

|

448,042 |

526,129 |

|

Weighted average number of Ordinary Shares - Diluted |

|

448,042 |

526,129 |

|

|

|

|

|

|

Basic earnings per share for total operations |

|

3.4p |

3.6p |

|

Diluted earnings per share for total operations |

|

3.4p |

3.6p |

10. Investments at fair value through profit or loss

|

|

|

At 1 January 2025 |

Additions during the period |

Change in fair value |

Total investments |

Fair value level |

|

|

|

|

2025 |

2025 |

2025 |

|

|

|

|

£'000 |

£'000 |

£'000 |

£'000 |

|

|

Fixtaia Limited |

|

87,228 |

4,685 |

15,862 |

107,775 |

3 |

|

|

|

At 1 December 2023 |

Additions during the period |

Change in fair value |

Total investments |

Fair value level |

|

|

|

|

2024 |

2024 |

2024 |

|

|

|

|

£'000 |

£'000 |

£'000 |

£'000 |

|

|

Fixtaia Limited |

|

55,392 |

12,500 |

19,336 |

87,228 |

3 |

Fixtaia is the subsidiary vehicle where all investment transactions are executed and held.

During the current period, the Company received 46.85 shares in Fixtaia for cash consideration of £4.7m. The number of shares held in Fixtaia as at December 2025 was 821.95 (2024: 775.1). At 31 December 2025, the investment in Fixtaia was revalued to £107.8m as per the net asset value of Fixtaia, resulting in a net revaluation gain of £15.9m through profit or loss.

The Company's accounting policy on fair value measurement is disclosed in note 2. The investment is categorised at Level 3 as there is no market activity on the date of measurement as they are a private company. Fixtaia is held at NAV.

Fixtaia holds a portfolio of listed and private assets. The listed assets are categorised as Level 1 and the private assets are categorised as Level 3 investments.

11. Financial assets and liabilities

|

|

|

|

2025 |

2024 |

|

|

|

|

£'000 |

£'000 |

|

Financial assets at fair value through the profit or loss |

|

|

|

|

|

Investments (see note 10) |

|

|

107,775 |

87,228 |

|

Financial assets at amortised cost |

|

|

|

|

|

Other receivables |

|

|

141 |

106 |

|

Total financial assets |

|

|

107,916 |

87,334 |

|

Financial liabilities at amortised cost |

|

|

|

|

|

Amounts owed to related undertakings (see note 14) |

|

|

(1) |

(4) |

|

Current tax liability |

|

|

- |

(794) |

|

Other payables |

|

|

(233) |

(278) |

|

Total financial liabilities |

|

|

(234) |

(1,076) |

|

|

|

|

|

|

|

Cash and cash equivalents |

|

|

2,211 |

29,613 |

|

Net funds |

|

|

2,211 |

29,613 |

The fair value of assets and liabilities approximates their book value.

Other receivables represent receivables, prepayments and accrued interest receivable. Other payables include accruals of £193k (2024: £269k).

The Company's overall risk management programme focuses on reducing financial risk as far as possible and therefore seeks to minimise potential adverse effects on the Company's financial performance. The policies and strategies for managing specific financial risks are summarised as follows:

Market risk

Market price risk is the risk that the market price of a financial instrument will fluctuate due to changes in factors specific to the security or its issuer. This market risk comprises three elements - currency risk, interest rate risk and other price risk.

If the market value of the Company's investments increased/decreased in value by 10% as at 31 December 2025 the effect on the investment portfolio would have been an increase/decrease of £10.8m.

Currency risk

The Company holds one investment, via its subsidiary Fixtaia, denominated in a currency other than Sterling (GBP). Consequently, the Company is exposed to currency risk as the value of the investment denominated in Euro's will fluctuate due to the change in the exchange rate. The Company does not currently engage in currency hedging activities. The Company's cash is held in GBP.

Interest rate risk

Interest rate risk arises from the possibility that changes in interest rates will affect the level of income receivable on cash deposits. The Company's interest-bearing assets are cash and cash on deposit at Royal Bank of Scotland ("RBS"). The Company would be significantly affected by changes in interest rates on cash held on deposit with RBS. Interest rate movements may affect the fair value of investments in fixed interest and equity securities.

Liquidity risk

Liquidity risk is the risk to Company will encounter difficulties in meetings its obligations associated with its financial liabilities. The Company undertakes short-term cash forecasting to monitor its expected cash flows against its cash availability. The Company also undertakes longer-term cash forecasting to monitor its expected funding requirements in order to meet its current business plan. The Company has sufficient cash to cover all outstanding current liabilities at the period end.

Credit risk

The Company's principal exposure to credit risk is in the amounts owed by related undertakings. As at 31 December 2025, £1k is owed to DBAY Advisors Limited. (2024: £4k)

Capital management

Capital comprises share capital of £4.1m (2024: £5.2m).

12. Capital and reserves

|

|

No of shares |

Called up share capital |

|

|

'000 |

£'000 |

|

Ordinary shares of 1p each in issue at 31 December 2024 |

524,350 |

5,244 |

|

Ordinary shares of 1p each in issue at 31 December 2025 |

413,824 |

4,138 |

All ordinary shares in issue referred to in the table above were authorised and are fully paid.

Share repurchase

On 24 April 2025, a tender offer was completed in which 110,526,315 Ordinary Shares were repurchased by the Company for £0.19 each and subsequently cancelled, returning £21.0m to shareholders.

13. Reserves

i. Capital redemption reserve

In relation to share repurchases, a cumulative capital redemption reserve of £1.5m has been recognised in the current year, including £0.4m relating to prior periods which has been recorded in 2025 as the prior period impact is not material.

ii. Retained earnings

|

|

|

31 Dec 2025 |

31 Dec 2024 |

|

|

|

£'000 |

£'000 |

|

At 1 December |

|

111,055 |

93,182 |

|

Profit/(loss) for the period |

|

15,109 |

18,820 |

|

Share repurchase |

|

(19,895) |

(947) |

|

Transfer to capital redemption reserve |

|

(1,480) |

- |

|

At 31 December |

|

104,789 |

111,055 |

14. Related party transactions

|

|

Transactions with related parties |

Amounts owed by related parties |

Amounts owed to related parties |

|||

|

|

2025 £'000 |

2024 £'000 |

2025 £'000 |

2024 £'000 |

2025 £'000 |

2024 £'000 |

|

|

|

|

|

|

|

|

|

Related party |

|

|

|

|

|

|

|

DBAY Advisors Limited |

(6) |

(20) |

- |

- |

(1) |

(4) |

|

WS Holdco Limited |

(15,000) |

- |

- |

- |

- |

- |

|

Total |

(15,006) |

(20) |

- |

- |

(1) |

(4) |

During the period, DBAY Advisors Limited paid for expenses of £6k (2024: £20k) on the behalf of the Company. As at 31 December 2025, £1k is owed to DBAY Advisors Limited (2024: £4k).

On 18 July 2025 the Company announced an investment of £15m into WS Holdco Limited ("WS Holdco") (formerly Framtid Topco Limited), a private holding company of a group of companies formed by DBAY. The Company and WS Holdco share a common investment manager, DBAY.

During the period, Fixtaia accrued performance fees of £475k (2024: £3.15m). The balance outstanding as at 31 December 2025 was £4.35m. (2024: £3.87m). Performance fees become payable to DBAY, by Fixtaia, only upon realisation of an investment.

Monitoring fees, at Fixtaia level, incurred during the period amounted to £1.5m (2024: £1.4m) of which £422k (2024: £335k) was outstanding at the reporting date. Monitoring fees are paid by Fixtaia to DBAY.

The Company did not enter into any other related party transactions.

15. Capital commitments

At 31 December 2025, the Company had no commitments (2024: £Nil).

16. Contingent liabilities

At 31 December 2025, the Company had no contingent liabilities (2024: £Nil).

17. Subsequent events

On 22 January 2026 LDG announced that Finsbury, in which LDG holds an economic 25.3% interest through the Company's wholly owned subsidiary Fixtaia, had completed a refinancing and subsequent return of capital. This resulted in £11.4m being received by Fixtaia, de-risking the Company's original capital investment to £2.8m of exposure (original investment: £14.2m). LDG's equity stake in Finsbury remains unchanged.

The Board of LDG agreed the reallocation of £10m (the "Investment") from the Finsbury return of capital to increase its investment in WS Holdco. Under the leadership of William Stobart, WS Holdco Group is pursuing a buy-and-build strategy aimed at creating a UK-focused national logistics platform. WS Holdco Group has also acquired 100% of William Stobart & Son Limited, which provides general transport and warehousing services; a 70% interest in WS Digital Freight Ltd, an asset-light road forwarding business; and a 60% interest in WS Bis Henderson Limited, which specialises in white-collar recruitment for the logistics industry.

The Investment was on the same terms as LDG's original investment of £15m in WS Holdco as detailed in the Company's announcement on 18 July 2025. As at 30 September 2025, LDG's interest in WS Holdco was 42.6% and increased to 51.3% after the further Investment. LDG's interest may change if additional equity is raised by WS Holdco and there is no certainty that LDG will participate in subsequent fundraises.

Alliance, in which LDG has invested £39.0m and holds an economic 24.5% interest, announced in December 2025 that it had disposed of its prescription products portfolio to two strategic buyers. The transaction closed in early January 2026 with proceeds contributing to a net debt reduction from £275m at the end of December 2025 to a forecast c. £175m at 31 March 2026. Following this transaction, the business is a pure-play consumer healthcare platform with market leading brands in damaged skin (especially scar and scalp care) and healthy aging.

On 27 February 2026, LDG announced its quarterly portfolio data. As at 31 December 2025, LDG's unaudited estimated NAV per share was 26.7p. The NAV remains unchanged compared to the prior period being 30 September 2025. The valuations of the portfolio companies mirror the valuations at which the assets are held in the DBAY private funds. Funds managed by DBAY are the lead investor in all LDG portfolio companies, and DBAY's management believes all portfolio companies are held at a conservative valuation. An update on the portfolio investments was also provided.

On 17 March 2026 LDG was notified by WS Holdco, its portfolio company, that it had acquired EV Cargo Solutions and Distribution Limited. Following this transaction, LDG's interest in WS Holdco is 50.7%.

GLOSSARY

Term Definition

Accounts The financial statements of the Company

Admission The admission of the issued ordinary shares in the Company admitted to trading on AIM that became effective on 31 December 2020

AGM Annual general meeting of the Company

AIM Alternative Investment Market of the London Stock Exchange

AIM Rules The AIM Rules for Companies published by the London Stock Exchange from time to time (including, without limitation, any guidance notes or statements of practice) which govern the rules and responsibilities of companies whose shares are admitted to trading on AIM

AIM Investing Company An Investing Company as defined by the AIM rules

APMs Alternative Performance Measures

Board The Board of Directors of the Company

Company or LDG Logistics Development Group plc, a public limited company incorporated in England and Wales with registered number 08922456

DBAY DBAY Advisors Limited and/or any fund(s) or entity(ies) managed or controlled by DBAY Advisors Limited as appropriate in the relevant context

Directors The Directors of the Company as at the date of this document, as identified on page 13

EPS Earnings per share

Fixtaia Fixtaia Limited, a company incorporated in Jersey (company no. 140806). Fixtaia is the subsidiary investment vehicle. All investments are executed and held in Fixtaia. Registered office is at 2nd Floor, Gaspé House, 66-72 Esplanade, St. Helier, JE1 1GH, Jersey

FY24 Financial period for the 13 months to 31 December 2024

FY25 Financial year ended 31 December 2025

HY25 Six-month period ended 30 June 2025

IAS International Accounting Standards

IFRS International Financial Reporting Standards

Investment Management Agreement An investment management agreement entered into between the Company and DBAY, pursuant to which DBAY has been appointed as the Company's Investment Manager pages 9 and 10pages 9 and 10

Ordinary Shares/Shares Ordinary shares of £0.01 each in the capital of the Company

QCA Quoted Companies Alliance

QCA Governance Code (2023) QCA Corporate Governance Code (2023) for Small and Mid-Size Quoted Companies published by the QCA

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.

Latest directors dealings

- 5 hours ago Metlen Energy & Metals PLC

- 5 hours ago Artemis UK Future Leaders plc

- 5 hours ago Chapel Down Group

- 6 hours ago Eurocell

- 6 hours ago Eurocell