Results for the year ended 31 December 2025

Summary by AI BETAClose X

ELIXIRR INTERNATIONAL PLC

("Elixirr", the "Company" or the "Group")

Results for the year ended 31 December 2025

FY 25 momentum continues: revenue up 34%, adjusted EBITDA up 42%

Elixirr International plc (ELIX.L), an established, global, award-winning challenger consultancy, is pleased to announce its final results for the year ended 31 December 2025.

Financial Highlights

The Group delivered a record financial performance in FY 25, driven by strong demand for its AI-enabled, technology-led advisory services and continued disciplined execution. The Board is also pleased to recommend a final dividend for FY 25 of 15.0p per share, payable in August, bringing the total dividend for the year to 22.6p, a 27% increase on FY 24.

Key highlights include:

|

Metric |

FY 25 |

FY 24 |

Change (%) |

|

Revenue |

£149.6m |

£111.3m |

+34% |

|

Adjusted EBITDA |

£44.3m |

£31.2m |

+42% |

|

Adjusted EBITDA Margin |

29.6% |

28.0% |

+1.6pp |

|

Adjusted Profit Before Tax |

£41.0m |

£29.7m |

+38% |

|

Adjusted Diluted EPS |

58.7p |

43.1p |

+36% |

|

Free Cash Flow |

£31.1m |

£28.1m |

+11% |

|

Total Dividend per Share |

22.6p |

17.8p |

+27% |

|

Year-end Net Cash/(Debt) |

(£24.1m) |

£7.5m |

|

Operating Highlights

· AI and technology are core growth drivers, with AI-enabled work the fastest-growing segment (AI-related revenue up >260% year-on-year) and over 45 internally developed AI tools embedded across workflows to enhance productivity, while Elixirr's senior-led, agile, non-pyramidal model positions it strongly for an AI-enabled consulting market

· Successfully transitioned to the Main Market of the London Stock Exchange, supporting the Group's next phase of growth and ambition for FTSE 250 inclusion, alongside a material improvement in share liquidity and market quality

· Deepened client relationships and revenue quality, with £1m+ clients increasing from 27 in FY 24 to 34 in FY 25, and more than 65% of top 10 clients retained for over three years, reflecting strong repeat business and long-term partnerships

· Delivered strong cross-sell momentum across the platform, with cross-sell contribution exceeding £80m since IPO and over £37m in FY 25 (~25% of Group revenue), demonstrating the strength of the integrated, multi-capability model

· We maintained strong momentum across all four pillars of our growth strategy (stretch existing Partners, hire Partners, promote Partners and acquire complementary businesses), underpinning the scalability of the Group's platform

o Increased revenue per Partner to £4.4m (FY 24: £4.1m), supported by deeper account penetration, cross-sell and disciplined commercial execution

o Continued to strengthen senior leadership and talent density, with two new Partners appointed, three promoted internally and a further four Partner hires already completed in FY 26, adding deep expertise in AI, data and technology transformation

o Expanded capabilities and industry depth through acquisitions, with TRC Advisory enhancing growth strategy, pricing and commercial effectiveness capabilities and increasing exposure to private equity, and Kvadrant establishing a Nordic foothold and strengthening the European platform

· Further strengthened governance, Board capability and controls to reflect the Group's increasing scale, complexity and Main Market status, supporting disciplined growth and enhancing oversight of risk and internal controls

· Delivered our inaugural Capital Markets Day, showcasing AI, data, tech and digital capabilities through live demonstrations and partner-led sessions, reinforcing the depth, integration and scalability of the Group's platform

· Continued external recognition of performance and culture, with the Group featured in leading industry rankings including the Financial Times and Forbes lists

Current Trading & Outlook

Elixirr has entered FY 26 with a record Q1, trading in line with management expectations and providing a solid foundation for the year ahead. The Group's diversification by geography, capability and industry vertical supports resilience across varying market conditions, while continued demand for AI-enabled, technology-led advisory plays to Elixirr's strengths. As AI reshapes how consulting is delivered, the Board believes the Group's senior-led, agile model is well positioned to adapt and capture this opportunity. With strong fundamentals, a scalable platform and a growing, diversified client base, Elixirr remains confident in its ability to deliver sustainable growth and long-term value.

Commenting on the results, Founder & CEO, Stephen Newton, said:

"FY 25 has been a defining year for Elixirr. We delivered record revenues and sustained industry-leading profitability, completed our transition to the Main Market and further strengthened our capabilities, particularly in AI, whilst also expanding our geographic footprint through acquisitions. This performance reflects the strength of our differentiated, equity-backed model, the quality and ambition of our people, and the deep trust we continue to build with our clients.

"As AI reshapes both client demand and the way consulting is delivered, we believe our senior-led, technology-enabled model is becoming even more relevant. AI was the fastest growing part of our business last year. With a scalable platform, diversified client base and strong financial foundations, we enter our next phase with confidence as we progress towards our ambition of FTSE 250 inclusion."

Investor Presentation

A presentation relating to the Company's FY 25 Results will be held via Investor Meet Company on 21 April 2026, 13:00 BST for all existing and potential shareholders.

Investors can sign up to Investor Meet Company for free and request to meet Elixirr International plc via:

https://www.investormeetcompany.com/elixirr-international-plc/register-investor

After the webcast, a recording will be available at https://www.elixirr.com/en-gb/investors/results/

Enquiries:

For enquiries, please refer to the Company's Investor Contacts page:

https://www.elixirr.com/investors/investor-contacts

Elixirr International plc +44 (0)20 7220 5410

Stephen Newton, Chief Executive Officer

Graham Busby, Deputy Chief Executive Officer

Nicholas Willott, Chief Financial Officer and Company Secretary

investor-relations@elixirr.com

Cavendish Capital Markets Ltd (Broker) +44 (0)20 7220 0500

Stephen Keys, Callum Davidson, Isaac Hooper (Corporate Finance),

Sunila de Silva (ECM)

About Elixirr International plc

Elixirr is an award-winning global consulting firm working with clients across a diverse range of industries, markets and geographies. Founded in 2009, the firm set out to be the 'challenger consultancy' and do things differently than the large corporate consultancies dominating the industry: working openly and collaboratively with clients from start to finish, delivering outcomes based on innovative thinking, not methodology, and treating each client's business like their own. Elixirr was quoted on the AIM market of the London Stock Exchange in 2020 and listed on the Main Market of the London Stock Exchange in July 2025. In addition to strong organic growth, Elixirr has acquired nine boutique firms - Den Creative, Coast Digital, The Retearn Group, iOLAP, Responsum, Insigniam, Hypothesis, TRC Advisory, Kvadrant Consulting - to grow the Group's capabilities, diversify the business, expand into new geographies and access new clients.

This announcement contains inside information for the purposes of Article 7 of the Market Abuse Regulation (EU) 596/2014 as it forms part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018 ("MAR"), and is disclosed in accordance with the company's obligations under Article 17 of MAR.

Non-Executive Chairman's Report

Overview

I am pleased to introduce Elixirr's Annual Results for FY 25, a year that marked a significant step forward in the Group's scale, market maturity and long-term growth trajectory. During the year, Elixirr continued to deliver strong growth and profitability while further scaling its differentiated advisory model and completing its transition to the Main Market of the London Stock Exchange.

In an environment where clients remain selective in their investment decisions, the Elixirr group of companies (Group) has delivered impressive financial performance whilst maintaining strong margins. This reflects not only the quality of our client relationships, but also the strength and adaptability of our operating model. Importantly, this performance demonstrates that the Group can grow in scale and broaden its platform while retaining the profitability and discipline that underpin long-term value creation.

During the year, we continued to strengthen our strategic capabilities, particularly in AI and advanced technology advisory. As AI reshapes both client priorities and the consulting market, Elixirr is well positioned to support senior leaders through this change. Our model, which combines strategic insight, technology expertise and practical implementation, is inherently aligned with a more AI-enabled consulting environment, where value is increasingly driven by speed, adaptability and outcome delivery rather than scale of resource.

We are also seeing this translate into the nature of client demand. AI-enabled engagements are typically broader, more strategic and more closely linked to measurable outcomes, reinforcing our focus on high-value mandates. At the same time, AI is enhancing how we deliver, improving productivity and enabling faster execution, which further strengthens our competitive positioning.

We have also continued to deepen and diversify our client base. The number of significant, long-term "gold" client relationships (where clients have generated >£1m revenue in the financial period) has increased. This evolution strengthens the resilience of the business and provides a strong foundation for sustainable future growth.

Strategy

The Board remains confident in Elixirr's growth strategy, which balances organic expansion with disciplined inorganic investment and is underpinned by our entrepreneurial, equity-backed model. This model is particularly well suited to an AI-enabled consulting market, where success is increasingly determined by the ability to combine experienced judgement with technology and deliver outcomes efficiently.

Our differentiated, equity-based structure ensures strong alignment with long-term value creation. During FY 25, we continued to invest in talent development through the promotion of high-performing Principals to Partner, further strengthening our succession pipeline and leadership continuity. We also welcomed new Partner hires and enhanced our Board capability through an additional Non-Executive Director appointment in January 2026, ensuring our governance framework evolves in line with the Group's growth, scale and increasing technological sophistication.

A defining milestone during the year was Elixirr's transition in July 2025 from AIM to the Main Market of the London Stock Exchange. This was an important step in the Group's evolution as a larger and more institutionally relevant listed business. The strategic rationale behind this move was that the Main Market provides a stronger platform to enhance our profile, attract top talent, and compete more effectively with global consulting firms. It also offers access to broader pools of capital, including investors unable to invest in AIM companies, and supports the potential future inclusion in indices such as the FTSE 250, thus improving liquidity and passive investment. Overall, the move is expected to increase visibility, align our valuation more closely with our peers, and reinforce confidence in our long-term performance as we continue on our journey.

Inorganic growth remained an important strategic lever during the year. The acquisitions of TRC Advisory LLC (TRC) in Chicago in September 2025, and subsequently Kvadrant Consulting A/S (Kvadrant Consulting) in Copenhagen after the end of FY 25, further broadened the Group's platform geographically and by capability, including in areas closely aligned to AI-driven transformation. To support continued strategic flexibility, the Group extended its revolving credit facility. We are focused on ensuring that recent acquisitions are fully embedded operationally and culturally, which is central to sustaining earnings quality and unlocking cross-selling opportunities across the Group. The Board is encouraged by the early benefits of this integration and remains disciplined in evaluating future opportunities.

Together, our organic momentum, strengthened capabilities and disciplined M&A approach provide a strong platform for continued growth, with AI acting as both a driver of demand and an enabler of delivery, and positioning Elixirr to benefit from the structural shift underway in the consulting market.

Dividend

The Group policy continues to be to pay two dividends a year, with an interim dividend in February and a final dividend in August. An interim dividend of 7.6p per ordinary share of 0.005p each in the capital of the Company (Ordinary Share) was paid to shareholders on 24 February 2026.

The Board is pleased to recommend a final dividend for FY 25 of 15.0p per Ordinary Share, payable in August 2026 making a total dividend of 22.6p for the FY 25 financial year, a 27% increase on the FY 24 dividend. The final dividend will be recommended to shareholders at the AGM in June 2026. The FY 25 final dividend will have a total cash cost of £7.5 million.

Governance

As a Main Market listed company, Elixirr is committed to maintaining high standards of corporate governance consistent with the UK Corporate Governance Code 2024 (UKCG). The Board recognises that effective governance is fundamental to sustainable long-term success and to maintaining the confidence of shareholders and stakeholders. During FY 25, the Board continued to strengthen its oversight of strategy, risk management and internal controls, while further developing the governance framework needed to support a larger and more complex Group following the transition to the Main Market.

The appointment of an experienced Non-Executive Director (Bill Michael) shortly after the FY 25 reporting period further enhanced the balance of skills, independence and constructive challenge at Board level. The Board remains focused on maintaining a strong control environment, embedding a culture of accountability and transparency, and regularly reviewing governance effectiveness to support long-term value creation.

Outlook

As AI continues to alter the economics and delivery of parts of the consulting market, the Board believes Elixirr's differentiated, senior-led model leaves the Group well positioned to benefit from that shift.

Looking ahead to FY 26, the Board remains confident about Elixirr's trajectory. The Group's continued profitability, expanding capabilities and diversified client base provide a strong foundation for sustained growth and continued progress towards our ambition of FTSE 250 inclusion.

Gavin Patterson

Non-Executive Chairman

17 April 2026

Chief Executive Officer's Report

Overview

FY 25 was a year in which Elixirr delivered strong growth and continued profitability, completed its move to the Main Market and materially broadened the Group's platform both geographically and by capability.

The Group delivered revenue of £149.6 million (FY 24: £111.3 million), representing growth of 34% year-on-year, while maintaining strong Adjusted EBITDA of £44.3 million and a margin of 29.6% (FY 24: 28.0%). This performance reflects the resilience of our model, the sustained demand for high-impact advisory services and the increasing relevance of a delivery model that combines senior strategic judgement with deep data, technology and AI capabilities.

In July 2025, Elixirr moved from AIM to the Main Market of the London Stock Exchange, marking a significant milestone in our evolution as a public company. The move strengthens our market profile, broadens access to institutional capital, supports our ambition for future FTSE 250 inclusion and further reinforces our governance framework. Taken together, these benefits improve visibility and liquidity and strengthen confidence in our long-term growth trajectory.

Expanded US operations, the TRC acquisition, investments in AI and advanced technology, and growth in senior leadership strengthened the Group, whilst strong margins highlighted the resilience and scalability of our model. During the year, we worked with over 250 active clients, with the US accounting for 63% of Group revenue (FY 24: 55%).

Our differentiated proposition that combines strategy-led advisory with deep technology, data and AI expertise continues to resonate across industries and geographies. Increasingly, we are bringing strategy consultants, change experts, AI specialists and engineers together on the same engagements, enabling clients to move from strategic intent to practical execution faster.

Importantly, we continued to diversify our client base during the year. The number of clients generating more than £1 million of annual revenue rose from 27 in FY 24 to 34 in FY 25. This continued broadening of our revenue base, alongside higher levels of repeat client work, strengthens the resilience of the business and supports long-term, high-quality growth.

AI and Advanced Technology

AI is not new to Elixirr. We have been building AI and machine learning capability for more than a decade. Today, it is an increasingly important part of our client offering and a meaningful enabler across our own business. In FY 25, AI-related engagements accounted for a larger share of Group revenue and were the fastest-growing part of the business. These engagements are typically broader in scope, more strategic, and more closely tied to measurable client outcomes.

Our business model is structurally aligned with this shift. As AI reduces the need for repetitive, lower-value tasks, traditional pyramid-based, time-and-materials models are coming under pressure. Elixirr's senior-led, outcome-focused model enables us to integrate AI without disruption and benefit from these changing dynamics.

Additionally, we are seeing clear operational benefits. Supported by more than 45 internally developed AI tools embedded into our workflows, we achieved significant productivity gains in key consulting processes during the year. In proposal generation, for example, work is now taking around 10% of the time it previously required, with similar improvements being tracked in statement-of-work generation and knowledge management. These capabilities accelerate delivery and enhance the quality and consistency of our work.

Client demand continues to shift towards outcome-focused engagements that move from strategy through to execution and delivery of return on investment. AI enables faster, more targeted delivery, aligned with our outcome-based pricing model. For example, we recently worked with a major European bank to redesign its product development lifecycle using an AI-native model. The programme is expected to deliver them over £200 million in benefits over ten years, reduce product development cycles to as little as 2-6 weeks, and deliver an 18% reduction in long-term technology run costs.

Importantly, we have strengthened the data foundations underpinning our own capabilities through an advanced data layer, enabling AI-driven efficiencies across internal processes including proposal development and legal workflows. Furthermore, a key differentiator is our integrated delivery model, combining strategy consultants, industry specialists and AI engineers to move from insight to implementation more effectively. Finally, we continue to expand our capability to build bespoke AI solutions for clients and are developing proprietary AI agents based on our own data, creating potential for scalable, repeatable solutions over time.

AI is driving a structural shift in consulting, increasing the importance of speed, adaptability and outcome delivery. With our agile structure, senior-led model and continued investment in AI, Elixirr is perfectly positioned to capture this opportunity and deliver sustained value for both us and our clients.

FY 25 Performance

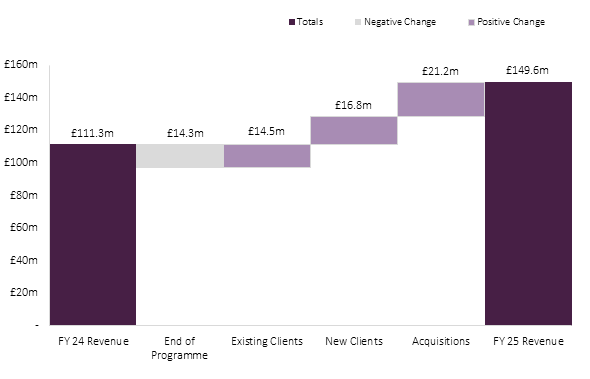

In FY 25 Elixirr generated revenue of £149.6 million - representing a 34% increase on the prior year (£111.3 million). Figure 1 below illustrates the key drivers of revenue growth from £111.3 million in FY 24 to £149.6 million in FY 25.

Figure 1: FY 25 Revenue Bridge (year ending 31 December 2025)

Organic revenue growth increased to 15.3% year-on-year in FY 25 (net +£17 million revenue) compared to a net +£11.1 million in revenue (FY 24: 13% year-on-year) achieved in FY 24. Growth from existing clients accounted for £14.5 million (FY 24: £9.7 million), reflecting deeper account penetration and cross-selling capabilities, while new client wins contributed £16.8 million (FY 24: £11.4 million). This was partially offset by £14.3 million of revenue attrition from end-of-programme projects.

Adjusted EBITDA increased by 42% to £44.3 million (FY 24: £31.2 million), with margin increasing to 29.6% (FY 24: 28.0%). Cash conversion remained strong with free cash flow of £31.1 million and the Group ended the year with net debt of £24.1 million.

To maintain strategic flexibility, we extended the Group's revolving credit facility to £65 million in FY 25 (FY 24: £45 million) and secured a US$20 million term loan, providing additional capacity to support disciplined M&A while limiting equity dilution. At year-end we had £51.0 million of revolving credit facility headroom and our financial covenants (interest cover and leverage ratios) were comfortably within required thresholds.

As we move into FY 26, we are focused on unlocking further cross-capability revenue opportunities, realising operational synergies, and aligning systems across our expanded platform as key drivers of margin sustainability and earnings quality.

Delivering Our Four-Pillar Growth Strategy

Our growth strategy remains grounded in a balanced approach to organic and inorganic expansion, underpinned by our entrepreneurial, equity-backed model. There are four key pillars to our growth strategy:

1. Stretching Existing Partners

Driving productivity and deepening client relationships within our established Elixirr Partner (Partner) cohort remains a core lever of organic growth. In FY 25, revenue per client-facing Partner increased to £4.4 million (FY 24: £4.1 million), reflecting stronger account penetration, cross-selling across capabilities and disciplined rate realisation.

The number of clients generating more than £1 million in annual revenue increased from 27 in FY 24 to 34 in FY 25, demonstrating our ability to scale relationships with strategically important clients. Unlike growth driven primarily by new hires, this pillar reflects the increasing productivity and commercial effectiveness of our established Partner cohort.

2. Hiring New Partners

Selective lateral Partner hiring remains an important contributor to Elixirr's growth. During FY 25, we welcomed two new Partners across key industry verticals and geographies, strengthening our sector depth and expanding our client access.

Stuart Stern joined the Group with over 30 years' experience across consulting and industry. He has held senior leadership roles at Slalom, AWS and Accenture, leading large-scale transformation programmes and complex cloud migrations across sectors including life sciences, insurance, transportation and telecommunications. His experience strengthens our enterprise transformation capability and senior client relationships in priority markets.

We also welcomed Conrad Troy, an expert in ERP strategy and business transformation. He previously led Deloitte's global SAP Transformation Consulting Practice and built Infosys Consulting's European ERP Business Transformation capability. His focus on integrating AI into operating models and developing value-led business cases expands our Enterprise Transformation and AI-enabled advisory proposition.

Early in FY 26, we welcomed Chris Bannocks, Rezwan Shafique, and Hugh Aller as new Partners. Chris brings more than 30 years of experience leading data, analytics and AI transformation across global organisations, including senior roles at ING, Danone and QBE, supporting our continued investment in accelerating the Group's AI capabilities and leadership. Rezwan brings more than 20 years of experience across banking and consulting, adding deep financial services expertise and extensive experience in delivering complex, value-driven transformation. Hugh brings more than 25 years of financial services and consulting experience, including senior leadership roles at Scotiabank and Citi and earlier strategy consulting work at Marakon. He has deep expertise in banking and capital markets having delivered cross-border M&A and large-scale transformation programmes.

Our hiring approach remains disciplined and culturally aligned, ensuring new Partners enhance both capability and long-term value creation. We maintain a strong pipeline of potential candidates as we continue to scale responsibly.

3. Promoting Partners from Within

Internal promotion remains a defining feature of Elixirr's entrepreneurial, ownership-focused model. During FY 25, we promoted three Principal-level employees to Partner (Portia Thornhill, Natasha Rostance and Nicholas Greenwood), reinforcing our leadership pipeline and continuity. Reflecting this continued bench building, two additional Principals, Adam Hofmann and Samuel Alexander, have been promoted to Partner with effect from 1 April 2026. Both Adam and Samuel are key leaders in our AI and data capabilities.

Revenue generated by promoted Partners now represents approximately 32% of total Partner-led revenue, demonstrating the effectiveness of our "grow our own timber" philosophy. This approach strengthens cultural alignment, preserves our performance standards and supports long-term leadership sustainability.

4. Acquiring New Businesses

Inorganic growth continues to play a strategic role in enhancing our capabilities, geographic reach and client access. We target one to two high-quality acquisitions annually, focusing on businesses that are strategically complementary and add meaningful value to the Group. Our dedicated M&A team screened more than 850 potential acquisitions in FY 25, of which approximately 15% progressed to engagement, reflecting our quality bar and disciplined approach.

In September 2025, we completed the acquisition of TRC, further expanding our international footprint. TRC strengthens Elixirr's capabilities across growth strategy and value creation, pricing excellence and commercial effectiveness, complementing our established offering to support clients end-to-end. TRC is performing ahead of our acquisition case.

In January 2026, after the reporting period, the Company acquired Kvadrant Consulting, establishing its first Nordic foothold and strengthening access to Northern Europe and the wider EU market. Kvadrant Consulting is highly complementary to TRC, combining TRC's strengths in growth strategy, value creation, pricing and commercial effectiveness with Kvadrant Consulting's expertise in commercial transformation, go-to market excellence and transaction services. Together, they strengthen the Group's offering to industrial, corporate and private equity clients, broaden cross-sell opportunities across a shared multinational client base, and create a scalable platform for continued European growth.

Our Firm

Our people remain the foundation of Elixirr's success. The entrepreneurial spirit, ownership mindset and commitment to excellence demonstrated across the Group continue to differentiate us in a competitive consulting market. As we scale, preserving this culture remains a strategic priority.

Our equity participation model reinforces alignment between our people and long-term shareholder value creation. Participation in our share schemes remains strong, with 84% of employees in our consulting business enrolled. This broad-based ownership structure fosters accountability, collaboration and a long-term perspective across the firm.

Attracting and retaining high-calibre talent remains central to our strategy. During FY 25, we received over 35,000 applications globally (equating to 417 applicants per hired role) and welcomed 164 new hires into the business, reflecting both the strength of our employer brand and the selectivity of our recruitment process. Our university and professional networks across the UK, US, and Europe continue to provide access to exceptional early-career and experienced talent, facilitated by our growing brand profile.

The way we build teams is also a differentiator. By combining our consultants with digital, data and AI technology specialists on client engagements, we are able to blend commercial insight with technical capability and help clients implement change more effectively. Innovation remains at the heart of how we operate and deliver for clients. We are embedding AI into our internal operations to improve speed and quality across processes such as knowledge management, statement of work generation, and proposal creation. We have developed 45 AI-enabled tools for internal use cases and these are delivering results around 25% faster for our teams, supporting operating leverage, improving responsiveness to clients and enabling more of our time to be focused on higher-value problem solving.

Our commitment to developing future talent and contributing to the communities in which we operate also continued during the year. The Elixirr Data and AI Academy in South Africa, launched in 2024, is progressing well, providing practical training, mentorship and career pathways for high-potential graduates while supporting the development of our global Centre of Excellence capability.

We also remained committed to supporting our communities by developing future talent through our social mobility initiatives. In London, our Early Careers Programme continues in partnership with 26 schools across the Harris Federation, our chosen partner, and we are excited to be progressing plans to launch a similar initiative in South Africa in FY 26 in partnership with Claremont High School.

During the year, the Group's performance and culture continued to receive external recognition across industry rankings and awards, including the Financial Times' Leading UK Management Consultants, Forbes America's Best Management Consulting Firms, and World's Best Management Consulting Firms lists. While we take pride in these achievements, our focus remains firmly on delivering sustainable growth, strengthening our capabilities and creating long-term value for our clients, people and shareholders.

Outlook

Trading in Q1 FY 26 has been in line with management expectations, with record Q1 revenue providing a solid foundation for the year ahead.

Our diversification by geography, capability and industry vertical supports resilience across varying market conditions. While AI and emerging technologies will reshape how consulting is delivered, we believe they are likely to favour firms that can combine trusted human judgement with technical execution in an agile, senior-led model. For Elixirr, this shift supports rather than disrupts our approach. We therefore expect consulting to evolve rather than diminish, with success determined by the ability to adapt quickly.

Clients continue to value independent advice, accountability and contextual understanding, whilst also expecting faster delivery, better use of data and practical implementation. Elixirr's entrepreneurial culture and flexible operating model position us well to embed AI directly into our delivery, enhancing speed, productivity and value creation whilst retaining human insight and judgement at the centre of our work.

Our ambition remains to progress towards inclusion in the FTSE 250, reflecting the increasing scale, liquidity and institutional maturity of our business. Achieving this objective will require profitable growth, continued diversification of our client base and disciplined leadership of our expanded capability platform. With strong fundamentals, a scalable business model, and growing demand for our differentiated approach to solving client challenges, Elixirr is well positioned to deliver sustainable growth and long-term value for its shareholders.

Stephen Newton

Chief Executive Officer & Founder

17 April 2026

Financial Review

Financial results summary

|

|

FY 25 |

FY 24 |

% change |

|

Revenue |

£149.6m |

£111.3m |

+34% |

|

Gross profit |

£49.7m |

£35.8m |

+39% |

|

Adjusted EBITDA* |

£44.3m |

£31.2m |

+42% |

|

Adjusted EBITDA margin* |

29.6% |

28.0% |

+1.6PP |

|

Adjusted profit before tax* |

£41.0m |

£29.7m |

+38% |

|

Adjusted diluted earnings per share* |

58.7p |

43.1p |

+36% |

|

Dividend per share |

22.6p |

17.8p |

+27% |

|

Free cash flow* |

£31.1m |

£28.1m |

+11% |

|

Net cash/(debt) |

(£24.1m) |

£7.5m |

N/A |

* In order to provide better clarity to the underlying performance of the Group, Elixirr uses Adjusted EBITDA, Adjusted profit before tax, Adjusted earnings per share (EPS) and free cash flow as alternative performance measures (APMs). Please refer to note 3 of the Group and Company Financial Statements for further details.

Group Results

The Board is pleased to report another year of strong financial performance for the Group, delivering record revenue, profit and earnings per share in FY 25. The Group achieved double-digit growth across all key financial metrics, reflecting continued strong client demand, the benefits of the Group's differentiated advisory model and the contribution from acquisitions completed during the year.

Revenue increased by 34% to £149.6 million (FY 24: £111.3 million), while Adjusted EBITDA increased by 42% to £44.3 million (FY 24: £31.2 million). Adjusted EBITDA margin improved to 29.6% (FY 24: 28.0%), reflecting operating leverage from strong organic growth and continued cost discipline.

The Group continues to generate strong levels of cash, delivering free cash flow of £31.1 million in FY 25 (FY 24: £28.1 million). Net debt at year end was £24.1 million (FY 24: net cash £7.5 million), reflecting acquisition-related investment and the utilisation of debt facilities to support the Group's growth strategy.

During the year, the Group strengthened its financing platform by extending its revolving credit facility from £45.0 million to £65.0 million and securing an additional US$20 million term loan with National Westminster Bank plc. These facilities provide increased financial flexibility to support the Group's continued organic and inorganic growth strategy, whilst limiting equity dilution. Further details are set out in note 19 of the Group and Company Financial Statements.

Revenue

Revenue increased by 34% to £149.6 million in FY 25 compared with £111.3 million in FY 24. The growth was driven by strong organic growth of 15% across the Group's core consulting capabilities, with the remaining growth from acquisitions.

Organic growth remained robust during the year, reflecting deeper client relationships and continued demand for strategy-led advisory services combined with technology, data and AI expertise. Revenue from existing clients increased through expanded engagements and cross-selling of capabilities, while new client wins continued to contribute meaningfully to growth.

The Group also benefited from the acquisition of TRC during the year, which strengthens the Group's growth strategy, pricing and commercial effectiveness capabilities and expands its presence in the US market.

Revenue growth was achieved across all geographic regions in which the Group operates. The United States continues to represent the Group's largest market and accounted for 63% of Group revenue in FY 25 (FY 24: 55%). This reflects the continued success of the Group's geographic expansion strategy and the increasing scale of its North American operations.

Revenue per client-facing Partner increased to £4.4 million in FY 25 (FY 24: £4.1 million), reflecting stronger account penetration, increased cross-capability selling and the continued productivity of the Group's Partner model.

The Group also continued to diversify its client base. The number of clients generating more than £1 million of revenue increased from 27 in FY 24 to 34 in FY 25. This continued diversification of the revenue base, together with increased levels of repeat client work, enhances the resilience of the business and supports sustainable long-term growth.

Group Profitability

Group gross profit increased by 39% to £49.7 million (FY 24: £35.8 million), reflecting the strong growth in revenue and continued effective management of delivery resources.

Administrative expenses increased during the year primarily as a result of the expansion of the Group through acquisition and the amortisation of intangible assets recognised for those acquisitions.

Adjusted EBITDA increased by 42% to £44.3 million (FY 24: £31.2 million). The Adjusted EBITDA margin improved to 29.6% (FY 24: 28.0%), reflecting operating leverage from the Group's scalable model together with the contribution from acquisitions. The Group continues to deliver industry-leading profitability.

Adjusted EBITDA growth resulted in a 38% increase in adjusted profit before tax to £41.0 million (FY 24: £29.7 million), which includes the finance costs of the revolving credit facility and term loan.

Statutory profit before tax reflects the impact of adjusting items including Main Market Listing and acquisition-related costs, amortisation of intangible assets arising on acquisition, share-based payments and movements in contingent consideration. Further details of adjusting items are set out in note 3 of the Group and Company Financial Statements.

Net Finance Expense

Net finance expense increased during the year reflecting the Group's transition from a net cash position to a net debt position following the expansion of its financing facilities to facilitate the acquisition of TRC.

Finance costs include interest on borrowings under the Group's revolving credit facility and term loan, together with the finance cost associated with contingent consideration liabilities and office lease liabilities. These costs were partially offset by interest income on cash deposits.

The Group maintains prudent leverage levels and retains significant headroom within its financing facilities.

Taxation

The Group's tax charge reflects the geographical mix of profits and the applicable statutory tax rates in the jurisdictions in which the Group operates.

The Group's tax charge for FY 25 was £7.9 million, reflecting a materially consistent effective tax rate on adjusted profit before tax of 24.2% compared with 24.7% in FY 24.

The effective tax rate on adjusted profit before tax is broadly consistent with the UK corporation tax rate, adjusted for overseas tax rates and permanent differences.

Further details on the Group's taxation are provided in notes 7 and 8 of the Group and Company Financial Statements.

Earnings Per Share

Adjusted diluted earnings per share increased by 36% to 58.7p (FY 24: 43.1p).

This increase reflects the strong growth in adjusted profit after tax of 38%, partially offset by the increase in the weighted average number of Ordinary Shares in issue resulting from the acquisition of TRC.

Adjusting items and their tax impacts are set out in note 3 of the Group and Company Financial Statements.

Cash Flow

The Group continues to benefit from strong cash generation driven by the profitability of the business and the asset-light nature of its operating model.

Net debt of £24.1 million represents cash (£5.1 million) net of the revolving credit facility and term loan (£29.1 million). The revolving credit facility and term loan were utilised to facilitate the acquisition of TRC (£29.2 million) and partially fund a combination of net Elixirr International Employee Benefit Trust (EBT) share purchases (£13.7 million) and Elixirr Digital Inc., Elixirr AI Inc., Insigniam LLC and Hypothesis Group, LLC (Hypothesis) earn-out and holdback payments (£7.2 million).

Free cash flow increased by 11% compared to FY 24, a smaller increase than EBITDA, mainly due to a larger FY 25 debtors working capital outflow, reflecting stronger debtor collections at December 2024 (versus December 2023), with the swing in FY 25 coming off a particularly strong base.

Statement of Financial Position

Net assets as at 31 December 2025 totalled £142.5 million (FY 24: £132.1 million). The increase in net assets is as a result of retained earnings for the year of £4.2 million (£19.7 million retained profit, £5.9 million add-back of share-based payment charge and related tax, offset by £8.4 million FY 24 dividend and £13.0 million for exercises of equity awards), a £11.7 million increase in share premium for the share issue associated with the TRC acquisition, net of foreign currency translation losses of £4.4 million, less the increase in cost of shares held by the EBT of £1.1 million.

The Group's balance sheet continues to reflect the value of the intellectual capital and client relationships acquired through its acquisitions, alongside the strong underlying profitability of the business.

The Group remains well capitalised with access to significant liquidity through its extended revolving credit facility and term loan arrangements, providing flexibility to support continued organic and inorganic growth.

Dividends

Elixirr paid an interim dividend in respect of FY 24 of 6.3p per Ordinary Share on 17 February 2025 and a final dividend in respect of FY 24 of 11.5p per Ordinary Share on 20 August 2025, making a total dividend of 17.8p for FY 24.

An interim dividend in respect of FY 25 of 7.6p per Ordinary Share was paid on 24 February 2026. The Board is pleased to recommend a final dividend for FY 25 of 15.0p per Ordinary Share, making a total dividend of 22.6p for the FY 25 financial year, a 27% increase on the FY 24 dividend.

The final dividend will be recommended to shareholders at the AGM in June 2026. The FY 25 final dividend will have a total cash cost of £7.5 million. The dividend payment date, record date and ex-date will be announced in due course.

Group and Company Financial Statements

GROUP STATEMENT OF COMPREHENSIVE INCOME

For the year ended 31 December 2025

|

|

|

Year ended |

Year ended |

|

|

Note |

£'000s |

£'000s |

|

Revenue |

4 |

149,600 |

111,344 |

|

Cost of sales |

4 |

(99,852) |

(75,537) |

|

Gross profit |

|

49,748 |

35,807 |

|

Administrative expenses |

|

(17,664) |

(11,040) |

|

Operating profit before M&A and Main Market-related items |

5 |

32,084 |

24,767 |

|

|

|

|

|

|

Depreciation |

|

1,713 |

1,485 |

|

Amortisation of intangible assets |

|

5,466 |

2,388 |

|

Share-based payments |

|

5,029 |

2,550 |

|

Adjusted EBITDA |

3 |

44,292 |

31,190 |

|

|

|

|

|

|

M&A-related items |

5 |

(878) |

(1,074) |

|

Main Market listing costs |

|

(1,473) |

- |

|

Operating profit |

5 |

29,733 |

23,693 |

|

Finance income |

|

162 |

394 |

|

Finance costs |

|

(2,305) |

(1,198) |

|

Net finance expense |

6 |

(2,143) |

(804) |

|

Profit before taxation |

5 |

27,590 |

22,889 |

|

Taxation |

7 |

(7,894) |

(6,510) |

|

Profit for the year |

|

19,696 |

16,379 |

|

|

|

|

|

|

Other comprehensive income |

|

|

|

|

Items that may be subsequently reclassified to profit or loss: |

|

|

|

|

Currency translation on foreign currency net investments |

|

(4,367) |

1,079 |

|

Other comprehensive income, net of tax |

|

(4,367) |

1,079 |

|

|

|

|

|

|

Total comprehensive income |

|

15,329 |

17,458 |

|

|

|

|

|

|

Basic earnings per Ordinary share (p) |

10 |

41.33 |

34.80 |

|

Diluted earnings per Ordinary share (p) |

10 |

37.18 |

31.64 |

All results relate to continuing operations.

The notes form part of these accounts.

Group and Company Statements of Financial Position

As at 31 December 2025

|

|

|

Group |

Company |

||

|

|

|

|

|

|

|

|

|

Note |

£'000s |

£'000s |

£'000s |

£'000s |

|

Assets |

|

|

|

|

|

|

Non-current assets |

|

|

|

|

|

|

Intangible assets |

12 |

197,319 |

128,809 |

- |

- |

|

Property, plant and equipment |

14 |

4,214 |

4,927 |

- |

- |

|

Investments |

15 |

- |

- |

145,092 |

117,317 |

|

Other receivables |

16 |

3,701 |

3,023 |

3,129 |

2,469 |

|

Loans to shareholders |

16 |

8,566 |

7,399 |

8,566 |

7,399 |

|

Deferred tax asset |

8 |

4,704 |

3,830 |

- |

- |

|

Total non-current assets |

|

218,504 |

147,988 |

156,787 |

127,185 |

|

|

|

|

|

|

|

|

Current assets |

|

|

|

|

|

|

Trade and other receivables |

16 |

26,810 |

18,385 |

44,068 |

782 |

|

Corporation tax receivable |

|

716 |

467 |

311 |

- |

|

Cash and cash equivalents |

17 |

5,054 |

7,527 |

157 |

1,837 |

|

Total current assets |

|

32,580 |

26,379 |

44,536 |

2,619 |

|

|

|

|

|

|

|

|

Total assets |

|

251,084 |

174,367 |

201,323 |

129,804 |

|

|

|

|

|

|

|

|

Liabilities |

|

|

|

|

|

|

Current liabilities |

|

|

|

|

|

|

Trade and other payables |

18 |

30,316 |

25,675 |

16,911 |

13,487 |

|

Loans and borrowings |

19 |

10,589 |

1,530 |

- |

- |

|

Corporation tax |

|

- |

- |

- |

80 |

|

Other creditors |

20 |

22,325 |

5,564 |

21,442 |

- |

|

Total current liabilities |

|

63,230 |

32,769 |

38,353 |

13,567 |

|

|

|

|

|

|

|

|

Net current assets/(liabilities) |

|

(30,650) |

(6,390) |

6,183 |

(10,948) |

|

|

|

|

|

|

|

|

Non-current liabilities |

|

|

|

|

|

|

Loans and borrowings |

19 |

22,933 |

3,366 |

13,970 |

- |

|

Deferred tax liability |

8 |

666 |

833 |

- |

- |

|

Other non-current liabilities |

20 |

21,727 |

5,286 |

18,776 |

- |

|

Total non-current liabilities |

|

45,326 |

9,485 |

32,746 |

- |

|

|

|

|

|

|

|

|

Total liabilities |

|

108,556 |

42,254 |

71,099 |

13,567 |

|

|

|

|

|

|

|

|

Net assets |

|

142,528 |

132,113 |

130,224 |

116,237 |

|

|

|

|

|

|

|

|

Equity |

|

|

|

|

|

|

Share capital |

21 |

52 |

52 |

52 |

52 |

|

Share premium |

21 |

45,384 |

33,702 |

45,384 |

33,702 |

|

Capital redemption reserve |

|

2 |

2 |

2 |

2 |

|

EBT share reserve |

22 |

(4,014) |

(2,897) |

(4,014) |

(2,897) |

|

Merger relief reserve |

21 |

46,870 |

46,870 |

46,870 |

46,870 |

|

Foreign currency translation reserve |

|

(2,910) |

1,457 |

- |

- |

|

Retained earnings |

|

57,145 |

52,927 |

41,930 |

38,508 |

|

Total shareholders' equity |

|

142,528 |

132,113 |

130,224 |

116,237 |

As permitted by Section 408 of the Companies Act, a separate statement of comprehensive income of the parent Company has not been presented. The Company's profit for the year was £20.8 million (FY 24: £18.0 million).

The notes form part of these accounts.

Approval

The Financial Statements were approved by the Board of Directors and were signed on its behalf by:

Stephen Newton

Director & Chief Executive Officer

17 April 2026

Group Statement of Changes in Equity

For the year ended 31 December 2025

|

|

Share capital |

Share premium |

Capital redemption reserve |

EBT share reserve |

Merger relief reserve |

Foreign currency translation reserve |

Retained earnings |

Total |

|

Group |

£'000s |

£'000s |

£'000s |

£'000s |

£'000s |

£'000s |

£'000s |

£'000s |

|

|

|

|

|

|

|

|

|

|

|

As at 31 December 2023 and 01 January 2024 |

52 |

29,922 |

2 |

(1,745) |

46,870 |

378 |

44,083 |

119,562 |

|

|

|

|

|

|

|

|

|

|

|

Comprehensive income |

|

|

|

|

|

|

|

|

|

Profit for the period |

- |

- |

- |

- |

- |

- |

16,379 |

16,379 |

|

Other comprehensive income |

- |

- |

- |

- |

- |

1,079 |

- |

1,079 |

|

Transactions with owners |

|

|

|

|

|

|

|

|

|

Ordinary share issues |

- |

6,402 |

- |

- |

- |

- |

- |

6,402 |

|

Dividends |

- |

- |

- |

- |

- |

- |

(6,907) |

(6,907) |

|

Share-based payments |

- |

- |

- |

- |

- |

- |

2,021 |

2,021 |

|

Deferred tax recognised in equity |

- |

- |

- |

- |

- |

- |

(156) |

(156) |

|

Current tax recognised in equity |

- |

- |

- |

- |

- |

- |

1,419 |

1,419 |

|

Sale of Ordinary Shares |

- |

(2,622) |

- |

10,911 |

- |

- |

(3,912) |

4,377 |

|

Acquisition of Ordinary Shares |

- |

- |

- |

(12,063) |

- |

- |

- |

(12,063) |

|

As at 31 December 2024 and 01 January 2025 |

52 |

33,702 |

2 |

(2,897) |

46,870 |

1,457 |

52,927 |

132,113 |

|

|

|

|

|

|

|

|

|

|

|

Comprehensive income |

|

|

|

|

|

|

|

|

|

Profit for the period |

- |

- |

- |

- |

- |

- |

19,696 |

19,696 |

|

Other comprehensive income |

- |

- |

- |

- |

- |

(4,367) |

- |

(4,367) |

|

Transactions with owners |

|

|

|

|

|

|

|

|

|

Ordinary share issues |

- |

11,682 |

- |

- |

- |

- |

- |

11,682 |

|

Dividends |

- |

- |

- |

- |

- |

- |

(8,402) |

(8,402) |

|

Share-based payments |

- |

- |

- |

- |

- |

- |

3,966 |

3,966 |

|

Deferred tax recognised in equity |

- |

- |

- |

- |

- |

- |

7 |

7 |

|

Current tax recognised in equity |

- |

- |

- |

- |

- |

- |

1,938 |

1,938 |

|

Sale of Ordinary Shares |

- |

- |

- |

22,779 |

- |

- |

(12,986) |

9,793 |

|

Acquisition of Ordinary Shares |

- |

- |

- |

(23,896) |

- |

- |

- |

(23,896) |

|

As at 31 December 2025 |

52 |

45,384 |

2 |

(4,014) |

46,870 |

(2,910) |

57,145 |

142,528 |

The notes form part of these accounts. Please refer to note 28 for explanations of reserve accounts.

Company Statement of Changes in Equity

For the year ended 31 December 2025

|

|

Share capital |

Share premium |

Capital redemption reserve |

EBT share reserve |

Merger relief reserve |

Retained earnings |

Total |

|

Company |

£'000s |

£'000s |

£'000s |

£'000s |

£'000s |

£'000s |

£'000s |

|

|

|

|

|

|

|

|

|

|

As at 31 December 2023 and 01 January 2024 |

52 |

29,922 |

2 |

(1,745) |

46,870 |

29,318 |

104,419 |

|

|

|

|

|

|

|

|

|

|

Comprehensive income |

|

|

|

|

|

|

|

|

Profit for the period |

- |

- |

- |

- |

- |

17,988 |

17,988 |

|

Transactions with owners |

|

|

|

|

|

|

|

|

Ordinary share issues |

- |

6,402 |

- |

- |

- |

- |

6,402 |

|

Dividends |

- |

- |

- |

- |

- |

(6,907) |

(6,907) |

|

Share-based payments |

- |

- |

- |

- |

- |

2,021 |

2,021 |

|

Sale of Ordinary Shares |

- |

(2,622) |

- |

10,911 |

- |

(3,912) |

4,377 |

|

Acquisition of Ordinary Shares |

- |

- |

- |

(12,063) |

- |

- |

(12,063) |

|

As at 31 December 2024 and 01 January 2025 |

52 |

33,702 |

2 |

(2,897) |

46,870 |

38,508 |

116,237 |

|

|

|

|

|

|

|

|

|

|

Comprehensive income |

|

|

|

|

|

|

|

|

Profit for the period |

- |

- |

- |

- |

- |

20,844 |

20,844 |

|

Transactions with owners |

|

|

|

|

|

|

|

|

Ordinary share issues |

- |

11,682 |

- |

- |

- |

- |

11,682 |

|

Dividends |

- |

- |

- |

- |

- |

(8,402) |

(8,402) |

|

Share-based payments |

- |

- |

- |

- |

- |

3,966 |

3,966 |

|

Sale of Ordinary Shares |

- |

- |

- |

22,779 |

- |

(12,986) |

9,793 |

|

Acquisition of Ordinary Shares |

- |

- |

- |

(23,896) |

- |

- |

(23,896) |

|

As at 31 December 2025 |

52 |

45,384 |

2 |

(4,014) |

46,870 |

41,930 |

130,224 |

The notes form part of these accounts. Please refer to note 28 for explanations of reserve accounts.

Group and Company Cash Flow Statements

For the year ended 31 December 2025

|

|

|

Group |

Company |

||

|

|

|

|

|

|

|

|

|

Note |

£'000s |

£'000s |

£'000s |

£'000s |

|

|

|

|

|

|

|

|

Cash flows from operating activities: |

|

|

|

|

|

|

Cash generated from operations |

24 |

39,970 |

35,456 |

17,890 |

11,392 |

|

Taxation paid |

|

(6,964) |

(6,058) |

(411) |

(68) |

|

Net cash generated from operating activities

|

33,006 |

29,398 |

17,479 |

11,324 |

|

|

|

|

|

|

|

|

|

Cash flows from investing activities: |

|

|

|

|

|

|

Purchase of property, plant and equipment |

(73) |

(84) |

- |

- |

|

|

Software development costs |

|

(131) |

(242) |

- |

- |

|

Payment for acquisition of subsidiary, net of cash acquired |

|

(36,358) |

(21,178) |

- |

- |

|

Interest received |

|

41 |

394 |

12 |

303 |

|

Net cash generated/(utilised) in investing activities

|

(36,521) |

(21,110) |

12 |

303 |

|

|

|

|

|

|

|

|

|

Cash flows from financing activities: |

|

|

|

|

|

|

EBT Ordinary share purchases |

|

(20,718) |

(12,178) |

(20,718) |

(12,178) |

|

EBT Ordinary share sales |

|

7,019 |

4,105 |

7,019 |

4,105 |

|

Loans to shareholders |

(2,350) |

(2,500) |

(2,350) |

(2,500) |

|

|

Loans repaid by shareholders |

|

1,198 |

2,592 |

1,198 |

2,592 |

|

s455 tax paid re loans to shareholders |

|

(660) |

(949) |

(660) |

(949) |

|

Proceeds from borrowings |

|

59,999 |

13,723 |

27,150 |

6,800 |

|

Interest and transaction costs paid on borrowings |

|

(1,497) |

(660) |

(1,298) |

(612) |

|

Repayment of borrowings |

|

(31,435) |

(14,419) |

(21,110) |

(6,800) |

|

Lease liability payments |

(1,487) |

(1,103) |

- |

- |

|

|

Interest paid on lease liability |

(249) |

(288) |

- |

- |

|

|

Ordinary share dividends paid to shareholders |

|

(8,402) |

(6,907) |

(8,402) |

(6,907) |

|

Net cash generated/(utilised) in financing activities |

1,418 |

(18,584) |

(19,171) |

(16,449) |

|

|

|

|

|

|

|

|

|

Net decrease in cash and cash equivalents |

(2,097) |

(10,296) |

(1,680) |

(4,822) |

|

|

Cash and cash equivalents at the beginning of the period |

7,527 |

18,130 |

1,837 |

6,659 |

|

|

Effects of exchange rate changes on cash and cash equivalents |

(376) |

(307) |

- |

- |

|

|

Cash and cash equivalents at the end of the period |

5,054 |

7,527 |

157 |

1,837 |

|

The notes form part of these accounts.

NOTES TO THE FINANCIAL STATEMENTS

1. BASIS OF PREPARATION

1.1. General information

Elixirr International plc (the "Company") and its subsidiaries' (together the "Group") principal activities are the provision of consultancy services. The Company is a public company limited by shares incorporated in England and Wales and domiciled in the UK. The address of the registered office is 12 Helmet Row, London, EC1V 3QJ and the Company number is 11723404.

1.2. Basis of preparation

The financial information set out above does not constitute the Company's statutory accounts for the years ended 31 December 2025 or 31 December 2024 but is derived from those accounts. Statutory accounts for 2024 have been delivered to the registrar of companies, and those for 2025 will be delivered in due course. The auditor has reported on those accounts; their reports were (i) unqualified, (ii) did not include a reference to any matters to which the auditor drew attention by way of emphasis without qualifying their report and (iii) did not contain a statement under section 498 (2) or (3) of the Companies Act 2006.

The Group financial statements were prepared in accordance with UK-adopted international accounting standards and the requirements of the Companies Act 2006. Except as described below, the accounting policies applied in the year ended 31 December 2025 are consistent with those applied in the financial statements for year ended 31 December 2024.

1.3. Basis of consolidation

These financial statements consolidate the financial statements of the Company and its subsidiary undertakings as at 31 December 2025.

Subsidiaries are fully consolidated from the date of acquisition, being the date on which the Group obtains control, and continue to be consolidated until the date that such control ceases. The acquisition method of accounting has been adopted. The financial statements of subsidiaries are prepared for the same reporting period as the parent Company, using consistent accounting policies.

All intra-group balances, income and expenses and unrealised gains and losses resulting from intra-group transactions are eliminated in full.

1.4. Measurement convention

The financial statements have been prepared under the historical cost convention, except as otherwise described in the accounting policies.

The preparation of the consolidated financial information in compliance with UK adopted international accounting standards requires the use of certain critical accounting estimates and management judgements in applying the accounting policies. The significant estimates and judgements that have been made and their effects are disclosed in note 2.1.

1.5. Going concern

The Directors have, at the time of approving the financial statements, a reasonable expectation that the Company and the Group have adequate resources to continue in operation for the foreseeable future. The Group's forecasts and projections, taking into account reasonable possible changes in trading performance, show that the Group has sufficient financial resources, together with assets that are expected to generate cash flow in the normal course of business. Accordingly, the Directors have adopted the going concern basis in preparing these consolidated financial statements.

2. MATERIAL ACCOUNTING POLICIES

The principal accounting policies adopted in the preparation of the financial statements of the Group and Company, which have been applied consistently to the period presented, are set out below.

2.1. Judgements and key sources of estimation uncertainty

The preparation of the financial statements requires management to make estimates and judgements that affect the reported amounts of assets, liabilities, costs and revenue in the financial statements. Actual results could differ from these estimates. The judgements, estimates and associated assumptions are based on historical experience and other factors that are considered to be relevant.

In the process of applying the Group's accounting policies, the Directors have made judgements which are considered to have a significant effect on the amounts recognised in the financial statements for the year ending 31 December 2025. These judgements involve estimations for contingent consideration on acquisitions and the recognition of intangibles on acquisitions, including applying the Multi-period Excess Earnings method to estimate the fair value of customer relationships and order books.

The key sources of estimation uncertainty that could cause an adjustment to be required to the carrying amount of assets or liabilities within the next accounting period is contingent consideration arising on business combinations under IFRS 3. Contingent consideration contains estimation uncertainty as the earn-out potentially payable is linked to the future performance of the acquiree. In estimating the fair value of the contingent consideration, at both the acquisition date and financial year end, management has estimated the potential future cash flows of the acquirees and assessed the likelihood of an earn-out payment being made. These estimates could potentially change as a result of events over the coming years. Please refer to note 13 for specifics of the estimation uncertainty relating to the contingent consideration for the acquisition of TRC. As at 31 December 2025, the maximum potential contingent consideration payable for TRC is £47.8 million, of which £39.4 million has been recognised by management.

2.2. Revenue recognition

Revenue is measured as the fair value of consideration received or receivable for satisfying performance obligations contained in contracts with clients, excluding discounts and Value Added Tax. Variable consideration is included in revenue only to the extent that it is highly probable that a significant reversal will not be required when the uncertainties determining the level of variable consideration are resolved.

This occurs as follows for the Group's various contract types:

• Time-and-materials contracts are recognised over time as services are provided at the fee rate agreed with the client where there is an enforceable right to payment for performance or performance-related elements completed to date.

• Fixed-fee contracts are recognised over time, based on the actual service provided to the end of the reporting period as a proportion of the total services to be provided where there is an enforceable right to payment for performance completed to date. This is determined based on the actual inputs of time and expenses relative to total expected inputs.

Where contracts include multiple performance obligations, the transaction price is allocated to each performance obligation based on its stand-alone selling price. Where these are not directly observable, they are estimated based on expected cost-plus margin. Adjustments are made to allocate discounts proportionately relative to the stand-alone selling price of each performance obligation.

Estimates of revenues, costs or extent of progress toward completion are revised if circumstances change. Any resulting increase or decrease in estimated revenues or costs are reflected in the statement of comprehensive income in the period in which the circumstances that give rise to the revision became known.

Fees are normally billed on a monthly basis. If the revenue recognised by the Group exceeds the amounts billed, a contract asset is recognised. If the amounts billed exceed the revenue recognised, a contract liability is recognised. Unbilled revenue is recognised at the fair value of consultancy services provided at the reporting date reflecting the stage of completion determined by costs incurred to date as a percentage of the total anticipated costs of each assignment. Contract assets are reclassified as receivables when billed and the consideration has become unconditional because only the passage of time is required before payment is due.

The Group's standard payment terms require settlement of invoices within 30 days of receipt.

The Group does not adjust the transaction price for the time value of money as it does not expect to have any contracts where the period between the transfer of the promised services to the client and the payment by the client exceeds one year.

2.3. Business combinations, goodwill and consideration

Business combinations

The Group applies the acquisition method of accounting to account for business combinations in accordance with IFRS 3, 'Business Combinations'.

The consideration transferred for the acquisition of a subsidiary is the fair value of the assets transferred, the liabilities incurred and the equity interests issued by the Group. The consideration transferred includes the fair value of any asset or liability resulting from a contingent consideration arrangement. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values at the acquisition date. The excess of the consideration transferred over the fair value of the Group's share of the identifiable net assets acquired is recorded as goodwill. All transaction related costs are expensed in the period they are incurred as operating expenses. If the consideration is lower than the fair value of the net assets of the subsidiary acquired, the difference is recognised in the income statement.

Goodwill

Goodwill is initially measured at cost and any previous interest held over the net identifiable assets acquired and liabilities assumed. If the fair value of the net assets acquired is in excess of the aggregate consideration transferred, the Group re-assesses whether it has correctly identified all of the assets acquired and all of the liabilities assumed and reviews the procedures used to measure the amounts to be recognised at the acquisition date. If the reassessment still results in an excess of the fair value of net assets acquired over the aggregate consideration transferred, then the gain is recognised in the income statement.

After initial recognition, goodwill is measured at cost less any accumulated impairment losses. For the purposes of impairment testing, goodwill is allocated to each of the Group's cash-generating units expected to benefit from the synergies of the combination. Cash-generating units to which goodwill has been allocated are tested for impairment annually, or more frequently when there is an indication that the unit may be impaired.

The Group performs impairment reviews at the reporting period end to identify any goodwill or intangible assets that have a carrying value that is in excess of its recoverable amount. Determining the recoverability of goodwill and the intangible assets requires judgement in both the methodology applied and the key variables within that methodology. Where it is determined that an asset is impaired, the carrying value of the asset will be reduced to its recoverable amount with the difference recorded as an impairment charge in the income statement.

In accordance with IAS 36, the Group has tested goodwill for impairment at the reporting date. No goodwill impairment was deemed necessary as at 31 December 2025. For further details on the impairment review please refer to note 12.

Contingent and non-contingent deferred consideration on acquisition

Contingent and non-contingent deferred consideration may arise on acquisitions. Non-contingent deferred consideration may arise when settlement of all or part of the cost of the business combination falls due after the acquisition date. Contingent deferred consideration may arise when the consideration is dependent on future performance of the acquired company.

Deferred consideration associated with business combinations settled in cash is assessed in line with the agreed contractual terms. Consideration payable is recognised as capital investment cost when the deferred or contingent consideration is not employment-linked. Alternatively, consideration is recognised as remuneration expense over the deferral or contingent performance period, where the consideration is also contingent upon future employment. Where the contingent consideration is settled in a variable number of shares or cash, the consideration is classified as a liability and measured at fair value through profit or loss.

2.4. Taxation

Income tax expense represents the sum of the tax currently payable and deferred tax.

Current tax

The tax currently payable is based on taxable profit for the year. Taxable profit differs from net profits as reported in the income statement because it excludes items of income or expense that are taxable or deductible in other years and it further excludes items that are never taxable or deductible. The Group's and Company's liability for current tax is calculated using tax rates that have been enacted or substantively enacted by the reporting end date.

Deferred tax

Deferred tax is the tax expected to be payable or recoverable on differences between the carrying amounts of assets and liabilities in the financial statements and the corresponding tax bases used in the computation of taxable profit and is accounted for using the balance sheet liability method. Deferred tax liabilities are generally recognised for all taxable temporary differences and deferred tax assets are recognised to the extent that it is probable that taxable profits will be available against which deductible temporary differences can be utilised. Such assets and liabilities are not recognised if the temporary differences arise from goodwill or from the initial recognition of other assets and liabilities in a transaction that affects neither the tax profit nor the accounting profit and at the time of the transaction, does not give rise to equal taxable and deductible temporary differences.

The carrying amount of deferred tax assets is reviewed at each reporting end date and reduced to the extent that it is no longer probable that sufficient taxable profits will be available to allow all or part of the asset to be recovered. Deferred tax is calculated at the tax rates that are expected to apply in the period when the liability is settled or the asset is realised. Deferred tax is charged or credited in the income statement, except when it relates to items charged or credited directly to equity, in which case the deferred tax is also dealt with in equity. Deferred tax assets and liabilities are offset when the Company has a legally enforceable right to offset current tax assets and liabilities and the deferred tax assets and liabilities relate to taxes levied by the same tax authority.

2.5. Foreign currency translation

The presentational currency of these financial statements and the functional currency of the Group is pounds sterling.

Functional and presentational currency

Items included in the financial statements of each of the Group's entities are measured using the currency of the primary economic environment in which the entity operates (the functional currency). The financial statements are presented in 'sterling', which is the Group's and Company's functional currency and presentation currency.

On consolidation, the results of overseas operations are translated into sterling at rates approximating to those ruling when the transactions took place. All assets and liabilities of overseas operations are translated at the rate ruling at the reporting date. Exchange differences arising on translating the opening net assets at opening rate and the results of overseas operations at actual rate are recognised in other comprehensive income.

Transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognised in the income statement.

2.6. Intangible assets

Intangible assets are measured at cost less accumulated amortisation and any accumulated impairment losses.

Software development

Expenditure on software development activities is recognised as an intangible asset when the Group can demonstrate the technical feasibility of completing the software so that it will be available for use or sale; its intention to complete and its ability to use or sell the asset; how the asset will generate future economic benefits; the availability of resources to complete the asset; and the ability to reliably measure the expenditure during development. Capitalised software development costs are amortised on a straight-line basis over the estimated useful life of 3 years.