Half Year Trading Statement

Summary by AI BETAClose X

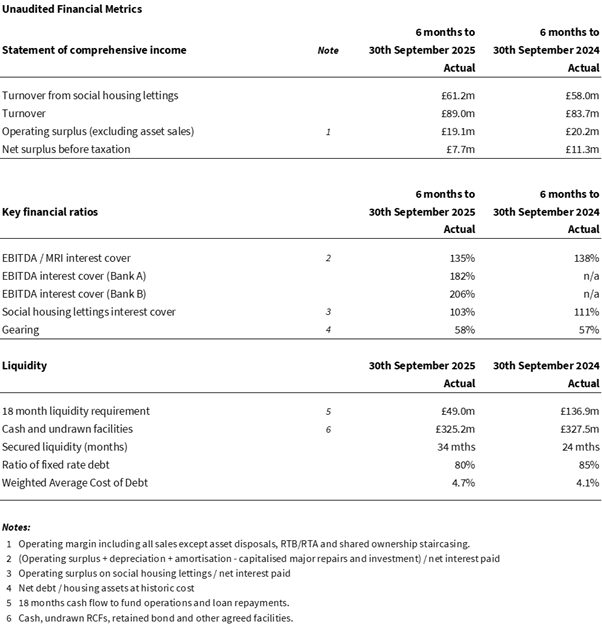

Yorkshire Housing Group (including YH Finance plc) trading update for the 6 months to 30th September 2025.

- Yorkshire Housing Group (YH) is today issuing its consolidated trading update for the 6 months ended 30th September 2025.

- These figures are unaudited and for information purposes only.

Highlights for the period ending 30th September 2025.

- YH own and manage 19,279 homes.

- YH has a regulatory rating of G1/V2.

- YH has a credit rating with Moody's of A3 Stable.

- Operating surplus for the period was £19.1m (2024: £20.2m)

- Net surplus before taxation was £7.7m (2024: £11.3m)

- EBITDA / MRI interest cover was 135% (2024: 138%)

- Social Housing Lettings Interest Cover was 103% (2024: 111%)

- Gearing was 58% (2024: 57%)

Rob Parkes, Executive Director Finance and Governance commented:

"Yorkshire Housing improved financial performance last year. As anticipated, we've had a slight dip in performance into the first half of this year. The main driver is lower margins experienced on shared ownership sales because of the mix of schemes coming to market. However, our operating surplus remains ahead of budget for the period.

Repairs and maintenance costs have stabilised after an increase last year following a sector-wide trend of increased demand. It remains our biggest cost area and the movement this year is largely aligned with inflation. We've also improved our repairs efficiency and service standards through transforming systems, processes and organisational design.

Depreciation and amortisation has increased by 14%. This is due to continued investment in our existing homes and because we've started to amortise the investment we've made in technology. We've also seen a 10% increase in corporate overheads caused by higher insurance and employment costs. However, these were exceptions and overall operating costs were limited to just under 7%.

Rental income has increased by 6% due to rent increases and the development of new homes. This has helped us manage overall financial performance. Sales of shared ownership remain strong, with 109 first tranche sales completed in the first half of the year (123 last year). Market sales have also been positive with 20 outright sales in the first 6 months compared to 13 for the same period last year.

Arrears levels have seen a modest increase as customers continue to face significant cost of living pressures and more customers transition to Universal Credit. The work of our Money and Tenancy Coaches in supporting customers with their finances so far this year has helped limit the impact on arrears levels. We've been able to maintain our empty homes levels at a consistent rate throughout the period.

We've expanded our commitment to being a sustainable organisation and launched our "Yorkshire Homes 2.0" standard. This includes a number of low-regret investments to improve the energy efficiency of our homes. And 85% of our homes are EPC C level or above.

External operating conditions are moving in a more favourable direction with inflation reducing and the Bank of England base rate steadily coming down. The cost of new debt remains higher than the weighted average of our portfolio of funding. To counter this we've carefully maintained strong liquidity whilst balancing the cost, interest rate risk and refinancing risk with new transactions.

We continue to manage our investment in technology, existing and new homes so that we can keep improving the experience of our customers and provide more quality homes across Yorkshire to the people who need them."

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.

Latest directors dealings

- 10 hours ago Gran Tierra Energy Inc. (CDI)

- 11 hours ago Polar Capital Holdings

- 11 hours ago PZ Cussons

- 12 hours ago Grainger

- 12 hours ago Molten Ventures VCT