POSITIVE PRE-FEASIBILITY STUDY FOR DOUTA PROJECT

Summary by AI BETAClose X

This announcement contains inside information as defined in the UK version of the Market Abuse Regulation (EU) No.596/2014, which is part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018. Upon the publication of this announcement via a Regulatory Information Service, such inside information will be considered to be in the public domain.

NEWS RELEASE

NOT FOR DISSEMINATION IN THE UNITED STATES OR FOR

DISTRIBUTION TO U.S. WIRE SERVICES

FOR IMMEDIATE RELEASE TSXV / AIM: THX

January 26, 2026

Vancouver, British Columbia

THOR EXPLORATIONS ANNOUNCES POSITIVE PRE-FEASIBILITY STUDY FOR THE DOUTA GOLD PROJECT, SENEGAL

Thor Explorations Ltd. (TSXV / AIM: THX) ("Thor" or the "Company") is pleased to announce the results of its Pre‑Feasibility Study ("PFS"), an updated Mineral Resource Estimate (the "Douta Resource" or "MRE") and a maiden Mineral Reserve prepared in accordance with National Instrument 43-101 Standards of Disclosure for Mineral Projects ("NI 43-101") for the 100% owned Douta Gold Project in Senegal ("Douta Project" or the "Project").

The PFS confirms a robust, long‑life gold project with strong economics, a substantial Mineral Reserve base, and a clear, accelerated pathway to development - underpinned by significant potential for further resource expansion.

PFS HIGHLIGHTS

· Pre-tax project NPV5% of US$908 million and IRR of 73% (100% equity basis) at a long-term gold price assumption of US$3,500/oz.

· Post-tax project NPV5% of US$633 million and IRR of 61% (100% equity basis) at a long-term gold price assumption of US$3,500/oz calculated using statutory Senegalese tax rates and excluding any fiscal incentives expected to be granted under the Mining Convention.

· Strong early cashflow, with gold production of 411koz in the first four years of oxide and transitional ore feed ("Oxide Ore Phase") at an all-in sustaining cost ("AISC") of US$1,493/oz, generating a pre-tax cashflow of US$814 million resulting in US$561 million of net cashflow post repayment of Project capital with an anticipated payback period of 11 months following the start of processing.

· Significant leverage to higher gold prices - at recent spot gold prices of circa US$4,250/oz the pre-tax NPV5% increases to US$1.43 billion (100% equity basis) with an IRR of 102% and an anticipated payback of nine months from the start of processing.

· Long-life production profile delivering 1.0 million ounces ("Moz") of gold from 37 million tonnes ("Mt") of mill feed grading an average of 1.03 grammes per tonne gold ("g/t Au") (containing 1.2Moz) over 12.6 years of operations.

· Two phase production profile comprised of the Oxide Ore Phase and the Primary Ore Phase.

· Low initial project capital of US$254 million and Life of Mine ("LOM") AISC of ~US$1,890/oz, supporting strong margins throughout the LOM.

· Project is to be entirely funded from the Company's cash reserves and project financing.

· The Ministry of Environment approved the Environmental and Social Impact Assessment ("ESIA") in January 2026.

· Signed a binding sale and purchase agreement with its Douta-West Permit joint venture partner, Birima Resources SARL ("Birima"), to acquire Birima's entire remaining outstanding 30% in the Douta West Permit for a cash payment of US$1.5 million at signing, a further US$3.5 million at decision to mine and a 1.25% Net Smelter Royalty capped at US$7 million.

· Next steps include finalisation of the Mining Convention with the Government of Senegal, commencement of detailed design, ordering of long-lead items and EPC contract award in H1 2026.

· The PFS positions Thor to advance its next development project, paving the way to become a multi‑asset producer operating across two countries, with first production from Douta targeted for early 2028.

MRE HIGHLIGHTS

· Updated Douta MRE constrained within optimised pit shells and comprised of:

o Indicated Mineral Resource of 50.6 Mt grading at an average of 1.04 g/t Au for 1.7Moz Au using a long-term gold price of US$4,000; and

o Inferred Mineral Resource of 9.3 Mt grading an average of 0.92g/t Au for 273,000oz Au using a long-term gold price of US$4,000.

o MRE constitutes a Probable Reserve of 36.6 Mt grading at an average grade of 1.03 g/t Au for 1.2 Moz Au using a long-term gold price of US$3,000 per troy ounce for all mining areas

o The MRE encompasses the Makosa, Makosa Tail and currently, the initial results from the recently discovered Baraka 3 prospects, all of which remain open along strike and down dip.

· Ongoing exploration across other prospects, with 40,000 metre drilling program continuing throughout 2026 to delineate additional oxide ore. Mineralisation remains open along strike between the known prospects with further growth potential along the under-explored prospective strike length covered by the Douta permit together with the Douta West and Bousankhoba Permits.

Segun Lawson, President & CEO, stated:

"We are delighted with the results of the Douta PFS which represents a major milestone in our strategy to become a multi-asset gold miner. The results confirm Douta as a high‑quality gold project with strong economics, a short payback period and long-term leverage to the gold price through its significant Indicated Resource base.

"The Oxide Ore Phase will produce approximately 413koz in the first four years, during which, the project will have an average annual gold production of over 111koz at an AISC of US$1,469/oz in the first three years.

"At a gold price assumption closer to today's prices (US$4,250/oz) the pre-tax NPV5% and IRR of the Douta Project is approximately US$1.43 billion and 102% respectively (on a 100% basis), paying back the construction capital cost of US$254 million in nine months.

"As per the PFS, Douta will produce approximately 82koz per annum for over 12.6 years at an average AISC of US$1,890/oz.

"In addition to the strong economics, the Project is positioned for further near-term growth in its resource and reserve inventory. Several drilling targets have been delineated through soil, rock chip and auger sampling, and aggressive drilling programs are ongoing, targeting additional oxide resources in the recently acquired contiguous Douta West and Bousankhoba Permits. The continued growth of the Makosa trend and inclusion of the first ounces from the Baraka 3 discovery underscore the district‑scale potential of the Douta Project.

"We are currently undertaking our 2026 budgeted 40,000 metre drilling program and aim to update the resource in Q3 this year. We look forward to providing periodic updates of our drilling results.

"Having finished 2025 with a strong cash balance of approximately US$137 million and our continued growing balance sheet in this high gold price environment, we are positioned to fund the construction of Douta without any shareholder dilution and have commenced high level financing discussions with interested parties.

"With simple, low‑cost oxide processing in the Oxide Ore Phase, an approved ESIA, and active exploration across multiple prospects, we are strongly positioned to advance Douta towards development while continuing to unlock value across the broader license package.

"We are also pleased to have agreed terms this month and signed a binding agreement with Birima, our Douta-West permit joint venture partner. This acquisition positions us to own the entire Douta Project consisting of the Douta and Douta-West licences on a 100% equity basis and allows for an efficient development process and full exposure to the project economics prior to the Government of Senegal's 10% free carried interest.

"In completing this PFS, we have undertaken a significant amount of work alongside our EPC Contractor, giving us comfort in the EPC pricing and positioning us to fast track to an updated feasibility study. We now look forward to the next steps in developing the Project which include finalisation of our Mining Convention with the Government of Senegal and ordering of the Project's long lead items."

DOUTA PROJECT OVERVIEW

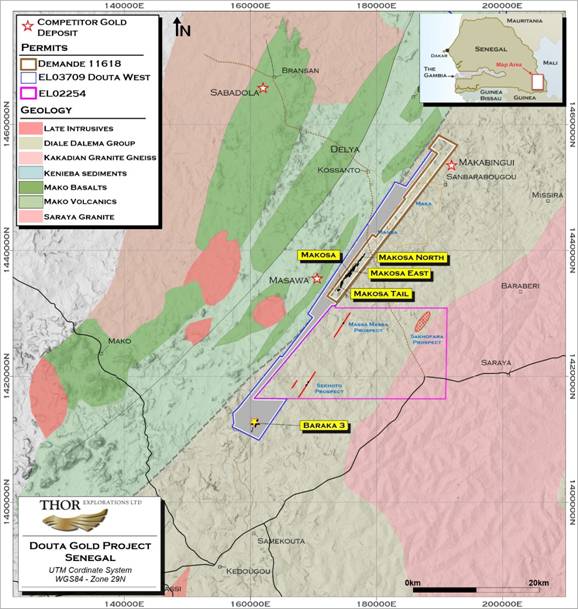

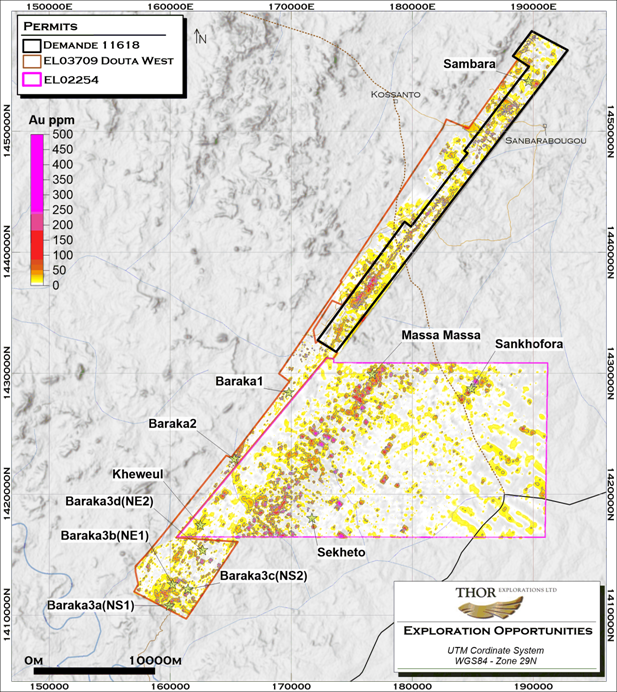

The Douta Project is located within the Birimian rocks of the Kéniéba inlier, in eastern Senegal and comprises the northeast trending mining lease application, De11618 that covers an area of 58 square kilometres ("km2") together with the Douta-West (EL03709) and Bousankhoba (EL02254) exploration permits.

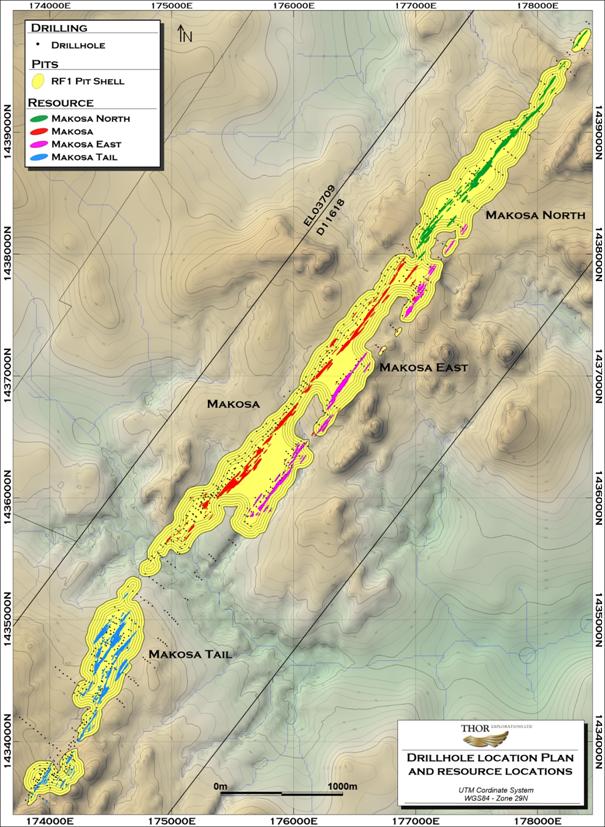

Thor, through its wholly owned subsidiary African Star Resources Incorporated ("African Star"), has a 100% economic interest in both DE11618 and EL03709 which, together, encompass all the known resources that have been defined to date. The recently acquired Bousankhoba permit, in which Thor has 65% interest, covers additional prospective geology along strike from the recently discovered Baraka 3 deposits (Figure 1).

Thor acquired its initial interest in the Douta Project in 2011 and drilled the discovery hole in the deposit in 2012.

Figure 1: Douta Project Location Map

PROJECT OVERVIEW

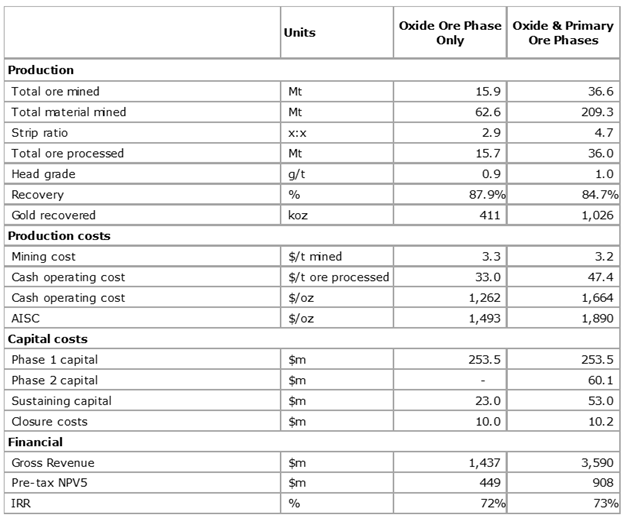

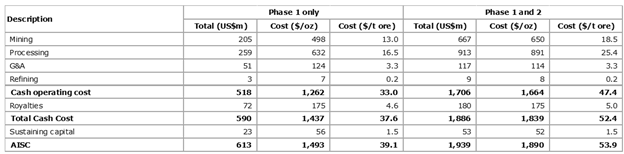

Table 1 includes operational and financial highlights at a flat long-term base-case gold assumption of US$3,500/oz.

Table 1: Economic Summary at US$3,500/oz

Conventional open‑pit mining is scheduled to commence at the end of 2027, with plant commissioning and ramp‑up during the first quarter of 2028. The Project envisages a 12.6 year LOM, comprising two phases:

· Oxide Ore Phase currently spans four years of mining and processing oxide and transitional ores through a conventional Carbon In Leach ("CIL") circuit, delivering average annual production of 103koz.

· Primary Ore Phase continues operations for a further 7.8 years, during which fresh ore will be mined and processed through the same CIL circuit enhanced by a suspension roaster, producing an average of 61koz per annum. An additional 2.3 million tonnes of oxide and transitional material, mined during the excavation of the Primary Ore Phase fresh ore pits, is processed for seven months at the end of the mine life, yielding 47koz.

Thor has a strong track record of resource growth at Douta. Ongoing exploration will initially focus on identifying additional oxide material with the aim of extending and enhancing the LOM. If successful, this additional material would likely supplement the Oxide Ore Phase feed and be processed ahead of the Primary Ore Phase.

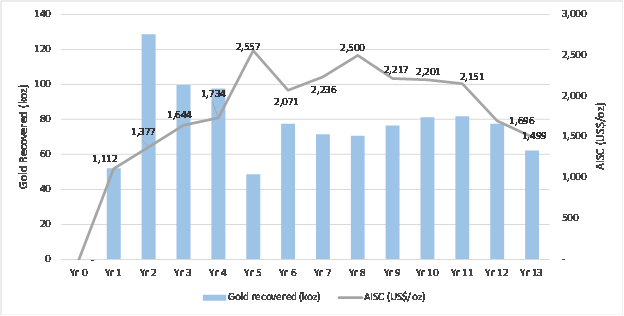

Figure 2: Production Profile and AISC (US$/oz)

In the first four years of oxide and transitional ore feed, production is 413koz at an AISC of US$1,493/oz. At the base case gold assumption of US$3,500/oz and with a first 18-month production of 180koz, payback would be achieved in one year.

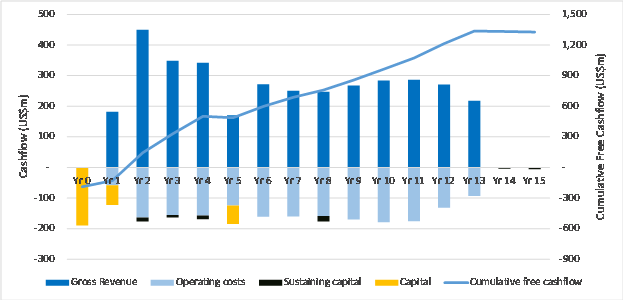

Figure 3: Free Cash Flow Profile (US$m)

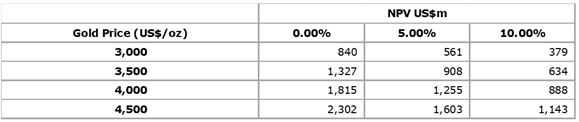

The pre-tax NPV sensitivity comparing varying discount rate percentages and gold price is presented in Table 2. The base case result for the Project is highlighted in bold.

Table 2: Sensitivity of pre-tax NPV5% (US$M) to Discount Rate and Gold Price (US$/oz)

(Base case US$3,500/oz)

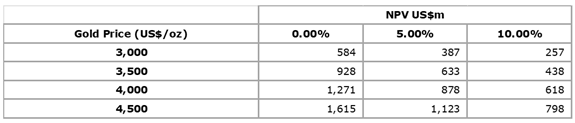

The post-tax NPV sensitivity comparing varying discount rate percentages and gold price is presented in Table 3. The base case result for the Project is highlighted in bold.

Table 3: Sensitivity of post-tax NPV5% (US$M) to Discount Rate and Gold Price (US$/oz)

(Base case US$3,500/oz)

The Post‑tax results exclude fiscal incentives expected under the Mining Convention. Tax has been modelled using a standard loss‑pool approach with the statutory 30% corporate tax rate. The 10% State free‑carried interest required under Senegalese law is not yet applied and will be incorporated after the Mining Convention is agreed.

MINERAL RESOURCES AND RESERVES ESTIMATES

MINERAL RESOURCE ESTIMATE

The MRE encompasses the Makosa, Makosa Tail and Baraka 3 Prospects, which are collectively referred to as the Douta Project.

The MRE is based on data obtained from a total of 69,598 metres ("m") of drilling comprising 2,936m of diamond drilling and 66,662m of Reverse Circulation ("RC") drilling.

The MRE is reported at a cut-off grade of 0.3g/t Au within optimised shells using a gold price of US$4,000.

|

Classification |

Tonnes (Mt) |

Grade (g/tAu) |

Contained Gold (Moz) |

|

Indicated |

50.6 |

1.04 |

1.7 |

|

Inferred |

9.3 |

0.92 |

0.27 |

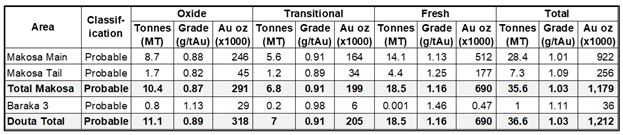

Table 4: Douta Gold Project Total Classified Mineral Resource Estimate Summary, January 2026 (reported at cut-off grade of 0.3g/t Au)

Table 5: Douta Gold Project Total Classified Mineral Resource Estimate Summary by Weathering Zone, January 2026 (reported at cut-off grade of 0.3g/t Au)

Table 6: Douta Gold Project Mineral Resource Estimate by Area, January 2026 (reported at cut-off grade of 0.3g/t Au

Table 7: Douta Gold Project Mineral Resource Estimate by Area and Weathering Zone, January 2026 (reported at cut-off grade of 0.3g/t Au) · Open Pit Mineral Resources are reported in situ at a cut-off grade of 0.30 g/t Au. An optimised Whittle shell (US$4,000) was used to constrain the resources. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

· The Mineral Resource is considered to have reasonable prospects for economic extraction by open pit mining methods above a 0.30 g/t Au and within an optimised pit shell. · Cut-off grade varied from 0.27 g/t to 0.30 g/t in a pit shell based on mining costs, metallurgical recovery, milling costs and G&A costs. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

· Metallurgical and mining recovery factors have been applied. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

· Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

· Totals may not add exactly due to rounding. · Resources reported as totals, minor equity portion is not deducted. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

· The statement used the terminology, definitions and guidelines given in the CIM Standards on Mineral resources and Mineral Reserves (May 2014) as required by NI 43-101. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

· Bulk density is assigned according to weathering profile with a weighted average of 2.78. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

· The resource estimate was prepared by Mr Alfred Gillmam, who is a qualified person ("QP") under NI 43-101and is not independent of the Company. |

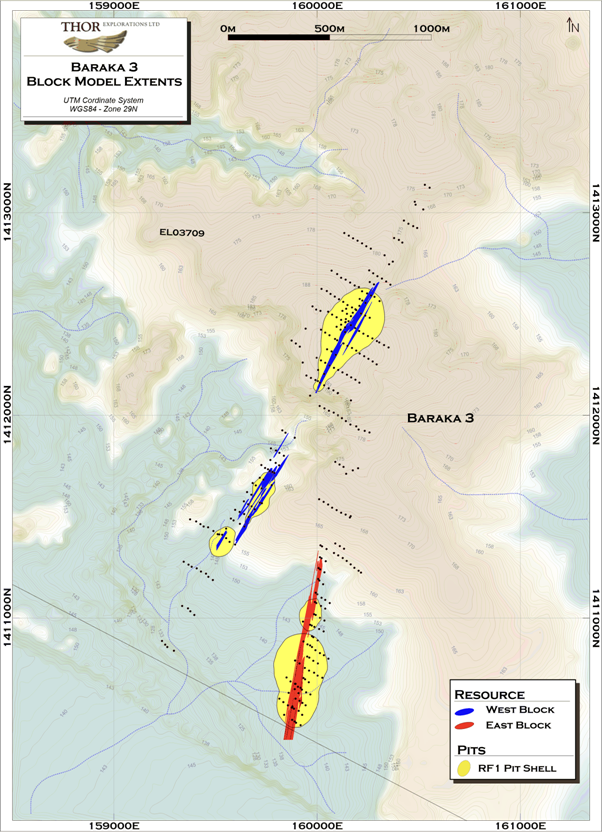

Mineral Resources for the Douta Project are estimated for five gold deposits and prospects located on the Douta and the Douta West exploration permit (Figure 1). Separate blocks models cover the Makosa, Makosa Tail, and Baraka 3 deposits. The Makosa block model encompasses the Makosa, Makosa North, and Makosa East deposits. Mineral Resources are reported inclusive of Mineral Reserves at an effective date of 24 January 2026 (Table 4).

The methods, parameters, assumptions, and support data used for the Douta block models, which date back to 2023, were reviewed to ensure they remain current. Models have been updated as required to either include new information or revised cost assumptions such as gold price and operation costs.

The same overall approach was used for each model whereby block grade and density estimates are constrained by domains representing the mineralisation, lithology, and weathering surfaces. Mineral Resources are reported within pit shells generated by AMC Consultants. Only classified blocks greater than or equal to the open pit cut-off grades and within the open pit shells are reported.

MINERAL RESERVE

Table 8 shows a summary of the Douta Project Mineral Reserves, which have been reported in accordance with CIM standards.

Table 8: Summary of Mineral Reserve Estimate for the Douta Project

|

· CIM Definition Standards for Mineral Resources and Mineral Reserves (CIM, 2014) were used for reporting of Mineral Reserves. · Mineral Reserves are estimated using a long-term gold price of US$3,000 per troy ounce for all mining areas. · Mineral Reserves are stated in terms of delivered tonnes and grade before process recovery. · Mineral Reserves are defined by pit optimisation and engineered pit design. · Mineral Reserves are based on variable break-even cut-offs as generated by metallurgical recoveries and costs. Baraka 3 also incurs an ore haulage cost due to its distance from the proposed processing plant. · Cut-off grades range from 0.28 g/t to 0.51 g/t for Makosa and 0.35 g/t to 0.43 g/t for Baraka 3. · Metal recoveries are variable dependent on material type and mining area. · Open-pit dilution and geological ore loss is applied through the regularisation of the Mineral Resource model to pre-determined Selective Mining Unit (SMU) blocks. · The Mineral Reserve estimate was undertaken using the Deswik mine planning software (Version 2025.2) and demonstrated that mining of the Makosa, Makosa Tail and Baraka 3 deposits at the Douta project is practical and economically viable. · The effective date of Mineral Reserves is January 2026. · Tonnage and grade measurements are in metric units. Contained Au is reported as troy ounces. · The Mineral Reserve estimate was prepared by Mr Dominic Claridge of AMC Consultants, who is a qualified person ("QP") under NI 43-101and is independent of the Company. |

TECHNICAL AND MODIFYING FACTORS

Sample Analysis and Database

Drilling has been almost exclusively sampled on 1m intervals with the main laboratory for analysis being ALS Global's laboratory in Bamako, Mali. Split samples ranging in weight from 0.5 kilogram ("kg") to 3.5kg, with an average of 2.3kg were collected for analysis. After the sample preparation a fire assay with an atomic absorption finish on a 50 grammes subsample of the pulp (AA26), was completed. Standard QA/QC protocols were followed with inserts of certified standards, blanks and duplicates representing approximately 10% of all analyses. The Company's DataShed5 database is maintained by MaxGeo (Western Australia).

Estimation Parameters

An Inverse Distance grade estimation was carried out within hard geological boundaries defined by a numerical model. Ordinary Kriging has been used to validate the Inverse Distance estimation results.

Separate numerical models were generated for Makosa Tail, Makosa North and East and Baraka 3.

A weathering model was developed to assign bulk densities based on weathering state.

Managing High Grade Samples

A capping level (top cut) of 10g/t Au is applied to all Makosa domains. An 8g/t Au top cut was applied to the Baraka 3 grade estimates.

Figure 4: Makosa Resource Area Location Map

Figure 5: Baraka 3 Resource Area Location Map

Estimation Methodology

Block grades were estimated using the inverse distance squared (ID2) method. All estimates used a single-pass approach with sufficiently large search ellipses to ensure all blocks within the domains were filled. Only diamond core and reverse circulation drilling data was used to estimate block grades. The Ordinary Kriging (OK) interpolation was used to compare with the ID2 method. Variogram models were generated for use in domains estimated by Ordinary Kriging.

Classification

Mineral Resource classifications have been reported in accordance with the CIM Definition Standards for Mineral Resources and Mineral Reserves (CIM, 2014). Resource classification is primarily based on drillhole spacing and grade continuity and is manually assigned using resource classification wireframes. Portions of the resources that are drilled at intervals between 25m and 50m are classified as Indicated. Areas where drillhole spacing exceeds 50m are classified as Inferred.

Mineral Resource and Reserve Constraints

To test the reasonable prospects for eventual economic extraction, the Douta Mineral Resource is constrained by an optimised pit shell (revenue factor of 1) defined by the parameters shown in Table 9.

The Mineral Reserve was constrained by pit designs developed from optimised pit shells using the same inputs, with the exception of the gold price.

It should be noted that Mining Recovery and Mining Dilution were not applied in the optimisation as they were applied to the geological model prior to the optimisation process.

|

Parameter |

Value |

|

Mining Costs (all deposits) |

|

|

Fixed Mining Cost - Oxide ($/t mined) |

$2.75 |

|

Fixed Mining Cost - Transitional ($/t mined) |

$2.75 |

|

Fixed Mining Cost - Fresh ($/t mined) |

$2.90 |

|

Total Ore Mining Cost - Oxide ($/t ore) |

$2.00 |

|

Total Ore Mining Cost - Transitional ($/t ore) |

$2.00 |

|

Total Ore Mining Cost - Fresh ($/t ore) |

$2.00 |

|

Mining Recovery - Makosa |

100% |

|

Mining Dilution - Makosa |

0% |

|

Mining Recovery - Baraka 3 |

100% |

|

Mining Dilution - Baraka 3 |

0% |

|

Ore Haulage |

|

|

Variable Ore Haulage Cost ($/tkm) |

$0.15 |

|

Ore Haulage Distance -Baraka (km) |

35 |

|

Fixed Ore Haulage Cost ($/t ore) |

$0.50 |

|

Processing Costs - Makosa |

|

|

Oxide ($/t processed) |

$17.50 |

|

Transitional ($/t processed) |

$17.50 |

|

Makosa Main Fresh ($/t processed) |

$35.76 |

|

Makosa Tail Fresh ($/t processed) |

$35.76 |

|

Processing Costs - Baraka 3 |

|

|

Oxide ($/t processed) |

$17.50 |

|

Transitional ($/t processed) |

$17.50 |

|

Fresh ($/t processed) |

$18.50 |

|

General & Administration Costs |

|

|

G&A Cost - All ($/t processed) |

$3.25 |

|

Processing Recovery - Makosa |

|

|

Oxide |

92.50% |

|

Transitional (excluding Makosa East) |

82.65% |

|

Transitional Makosa East |

72.80% |

|

Makosa Main Fresh |

81.00% |

|

Makosa Tail Fresh |

88.00% |

|

Processing Recovery - Baraka 3 |

|

|

Oxide |

92.50% |

|

Transitional |

90.00% |

|

Fresh |

76.00% |

|

Geotechnical Parameters (overall pit wall angles) - Makosa |

|

|

SOX and MOX |

34 degrees |

|

WOX |

36 degrees |

|

Fresh Rock - hanging wall |

51 degrees |

|

Fresh Rock - Makosa Main footwall |

44 degrees |

|

Fresh Rock - Makosa Tail footwall |

39 degrees |

|

Geotechnical Parameters (overall pit wall angles) - Baraka 3 |

|

|

SOX and MOX |

34 degrees |

|

WOX |

36 degrees |

|

Fresh - Hanging wall |

51 degrees |

|

Fresh - Footwall |

39 degrees |

|

Revenue Parameters |

|

|

Reserve Gold Price |

$3,000 |

|

Reserve Material Considered |

Indicated |

|

Resource Gold Price |

$4,000 |

|

Resource Material Considered |

Indicated & Inferred |

|

Government Royalty |

5% |

|

TCRC Costs - fixed |

$15/oz |

|

TCRC Costs - Variable |

0.4% gold value |

Table 9: Open Pit Optimisation Parameters

STUDY OVERVIEW

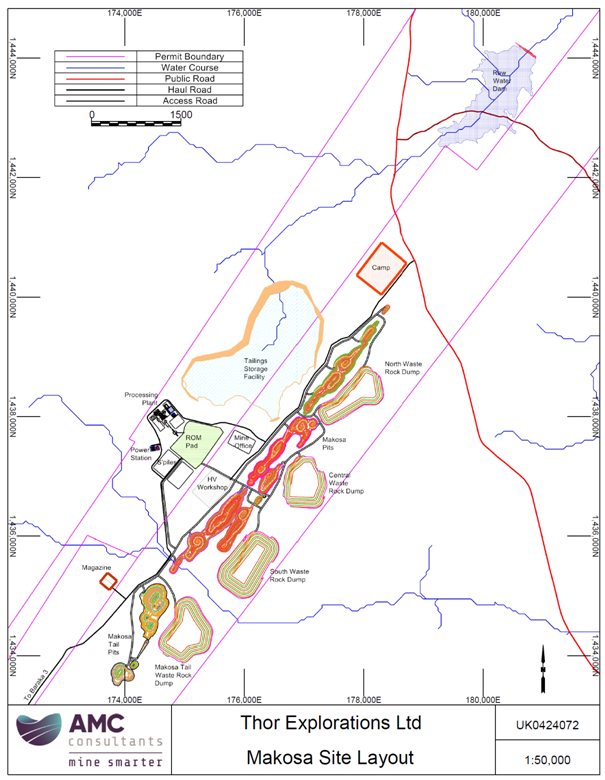

The PFS is based on five open-pit gold deposits feeding a central gold processing facility (Figure 6)

Figure 6 Douta Gold Project Site Layout

Mining

The deposits at the Douta project will be mined by conventional truck / shovel open pit operations. Pit optimisations were conducted using the Mineral Resource geological models and other factors. This exercise produced the optimal economic pit shells under the given parameters. Engineered pit designs were constructed based on the RF=1.0 shell for each deposit. These designs incorporated geotechnical and practical aspects such as ramp access.

Mining costs were estimated based on existing contracts and feedback from potential contractors which align with values for similar West African operations. Costs varied for different oxidation states with additional costs applied to ore mining.

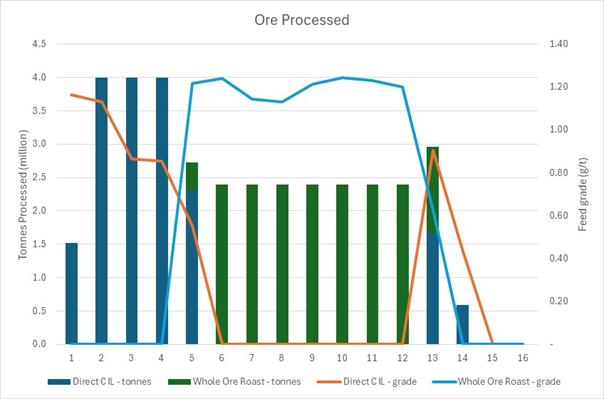

A mining and processing schedule was developed to demonstrate that the Mineral Reserve material could be successfully mined both practically and economically. Figure 7 shows the ore processed on an annual basis over the course of the mining schedule.

Figure 7: Ore processed during the life of the project

METALLURGICAL

The recoveries were developed from test work completed at IMO, Perth and North East University (NEU), China. IMO tested samples supplied by Thor from single RC drillholes and diamond drillholes. Samples were selected by ore types classified as oxide, transition, and fresh and by orebody location. Sub samples of two master composites of fresh ore type were delivered to NEU, China for testing of the suspension roasting process after determination by IMO of the low recovery performance of the fresh ores to cyanide leaching.

IMO characterised the ores by four acid digestion with ICP-OES finish and fire assay for gold, mineralogical analysis, diagnostic leaching and determination of preg-robbing indices. Oxide ores were characterised by low sulphur content. Fresh ores had sulphur contents up to approximately 3%. Transition ores had intermediate sulphur contents. The organic carbon content (graphitic) was variable across all ore types but most strongly associated with fresh ores and exhibited preg-robbing properties aligned with the organic carbon content.

Diagnostic leaching demonstrated that gold in the oxide ores was amenable to cyanide leaching, The gold in fresh ores was distributed in the general ore matrix, in sulphides and locked in silicates. Gold in sulphides and silicates was not recoverable by cyanide leaching. Transition ores exhibited intermediate behaviour due to intermediate sulphide content and variable silicate mineral content.

IMO test work optimised gravity and CIL process parameters and recoveries for oxide and transition ore types. Oxide ores showed total recoveries consistently more than 90% with low variation by ore body. All results were averaged to determine the final recovery. Transition ore types exhibited CIL recovery variation between Makosa and Makosa East locations. Recoveries from multiple tests were averaged for each of the two locations. Both oxide and transition ore types exhibited preg robbing behaviour that was mitigated by the addition of carbon to the cyanide leach.

IMO testing of fresh ore types gave low and variable results by CIL. These were deemed not amenable to conventional CIL processing and excluded from further direct CIL test work.

Fresh ores from Makosa and Makosa Tail were tested by suspension roasting and cyanide leach extraction of the calcined product by NEU. Results were consistently higher than methods tested by IMO and have been utilised as recoveries for fresh ores processed by suspension roasting - CIL extraction in pit optimisations. Recoveries of 81% and 88% were achieved for fresh Makosa and Makosa Tail ores respectively.

PROCESSING

The process plant design for the Project is based on a robust metallurgical flowsheet designed for optimum recovery with minimum operating costs. A two-stage process has been designed. Stage 1 focuses on the recovery of cyanide-soluble gold and Stage 2 focuses on the recovery of gold hosted in sulphides and silicates (refractory gold).

The proposed Oxide Ore Phase process plant design is based on a proven and established gravity/carbon-in-leach ("CIL") technology, which consists of crushing, milling, and gravity recovery of free gold, followed by leaching/adsorption of gravity tailings, elution and gold smelting, and tailings disposal. A roasting circuit treating the comminution product stream will be added to the flowsheet for the Primary Ore Phase. The suspension roasting process will expose refractory gold particles prior to cyanide leaching. The circuit will consist of a pre-roasting dewatering stage, pre-roasting product storage silo, suspension roasting, calcine repulping and regrinding.

Services to the process plant will include reagent mixing, storage and distribution, water, and air services. The plant will treat 4 million tonnes per annum ("Mtpa") of oxide ore for four years to produce an average of 103 koz per annum. In Stage 2, the plant will treat 2.4 Mtpa of fresh, sulphide ore for approximately 7.8 years, producing an average of 61 koz per annum. The final seven months will treat 2.3 Mt of mixed oxide and transitional ore mined and stockpiled during mining of the sulphide ore to produce 47 koz of gold.

POWER

Power requirements for the Project will be met through a dedicated Heavy Fuel Oil (HFO) power plant to be constructed, owned, and operated by an independent power provider under a long‑term power supply agreement. The contracted facility will deliver reliable baseload power to support all processing and infrastructure needs.

TAILINGS

The TSF will comprise of a single cell confined by a cross-valley embankment which will be staged in three downstream raises.

The TSF basin will be lined with HDPE within the normal operating pond areas to minimise seepage. In addition, a system of basal drainage, embankment drainage, embankment drainage and sub-liner drainage will be constructed to mitigate seepage, infiltration and aid consolidation of the tailings.

Water will be extracted from the decant pond using floating intake lines to position the pumps above the pond elevation.

The TSF will be closed and rehabilitated at the end of the LOM. Closure spillways will be formed to prevent water accumulating on the facilities and the tailings will be re-profiled prior to lining, topsoiling and revegetation.

ENVIRONMENTAL

The Douta exploration licence consists of a modified environment as a result of human activities including harvesting forest flora and burning vegetation as part of sporadic and unregulated historic artisanal mining activity.

No impediments with respect to reserves, parks or other areas of significance have been identified on the project area.

Development of the Project will not require any physical resettlement.

The Environment and Social Impact Assessment ("ESIA") was approved in January 2026.

PERMITTING

Development of the Project will be subject to negotiation of a Mining Convention.

Based on current expectations, Thor believes the Mining Convention will be finalised in H1 2026.

CAPITAL COSTS

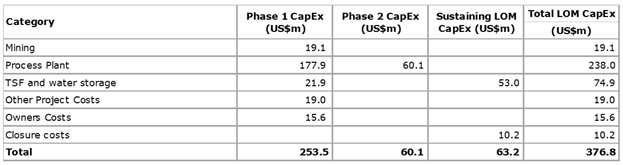

The initial Project capital cost is estimated at US$253.5m and incurred over an 18-month period. Primary Ore Phase capital cost is estimated at US$60.1m and expected to occur in 2031. Sustaining capital cost is estimated at US$63.2m, giving a LOM total capital cost of US$376.8m. The LOM capital cost is summarised in Table 10.

Table 10: LOM Capital Cost Estimate Summary

Capital Cost estimates presented in this section reflect total project costs from July 2026 to end of mine life. Mining activities are to be undertaken by a mining contractor with equipment costs contained within the mining operating costs.

The capital cost estimate was developed in collaboration with Norinco International, the Company's EPC turnkey partner at its Segilola project, using a methodology consistent with the proven approach adopted for that project. The estimate incorporates EPC turnkey components, providing strong cost definition and execution certainty. On a dollar‑per‑tonne basis, the projected capital intensity is highly competitive and broadly aligned with the benchmarks achieved at Segilola.

A contingency of 10% has been applied and included in all capital items above with the exception of the Processing Plant and TSF capex which have a 5% contingency allowance included.

OPERATING COSTS

The LOM Operating cost estimates are summarised in Table 11.

Table 11: LOM Operating Cost Estimate Summary

Mining Costs

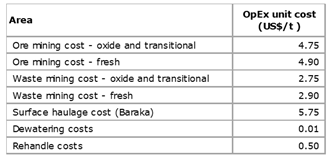

Mining operating costs were provided by a mining contractor and used across the LOM schedule as summarised in Table 12. Surface haulage costs were based on contractor rates for Baraka material based on a 35 km haul distance and dewatering costs estimated pumping requirements for in-pit and ex-pit dewatering using diesel rates of US$1.00/L and electricity rates of US$0.21/kwh.

Table 12: Mining Operating Unit Cost Summary

Processing Costs

Processing operating costs were estimated for the different ore types to be treated during the Oxide Ore Phase and the Primary Ore Phase of the operation. These are summarised in Table 13. Tailings monitoring and management costs were estimated at ~US$880k per year and included in the processing costs, equating to an additional US$0.25/t ore processed.

Table 13: Processing Unit Costs by ore type and area

Other Costs

Total fixed mine level general and administration ("G&A") costs are estimated at US$3.25/t ore

Refining and transport costs were based on current contracts at Segilola and total US$3.07/oz.

Royalties of 5% were applied to the gross revenue of gold produced.

Financial Analysis

An economic evaluation of the Project has been completed using a detailed cash‑flow model. The model is based on annual cash flows and incorporates processed tonnages and grades for the CIL feed, metallurgical recoveries, metal prices, operating costs, refining charges, royalties, and both initial and sustaining capital expenditures. Gold revenues are calculated using a payable factor of 99.90%. The analysis applies a base gold price of US$3,500 per ounce.

The Project has been assessed on a "100% equity" basis, with all debt and equity financing considerations excluded. Inflation has not been factored into the assessment. Discounting and IRR calculations commence at the start of construction, using a 5% discount rate.

The Company notes that the Mining Convention for the Project is yet to be negotiated with the Government of Senegal. As a result, it is not currently possible to incorporate the expected fiscal incentives and tax exonerations that are typically granted under such agreements into the calculation of the post tax NPV. For the purposes of this PFS, we have therefore applied a standard approach whereby exploration expenditure and project development capital are accumulated into a tax loss pool, against which future taxable income is fully offset, with the Senegalese statutory corporate tax rate of 30% applied thereafter. The Company anticipates an improved post-tax economic outcome once the Mining Convention is finalised, as such agreements customarily provide additional tax incentives that enhance project value.

The Company also notes that Senegalese mining legislation provides for a 10% State free‑carried interest, which will be formally awarded to the State upon finalisation of the Mining Convention. This interest has not been incorporated into the current economic analysis, which is presented on a "100% equity" basis and will be reflected in future evaluations once the Mining Convention has been agreed.

Exploration Opportunities

The Douta Project hosts a large but underexplored regional-scale gold system with strong potential to expand the Mineral Resources. Existing mineralisation, prospects, and targets remain open along strike and at depth within major structural corridors and the extensive area between them.

The Project comprises permits covering approximately 538 km² within the highly prospective Birimian Dialé metasediments. Key deposits are located along the Main Transcurrent Shear Zone ("MTZ") (hosting the Makosa Tail, Makosa, Makosa North and Makosa East deposits). Approximately 30km of the MTZ lie within the Project area.

Additional mineralisation potential exists within and adjacent to these structures, where early-stage exploration has identified numerous prospects along secondary and tertiary structural zones.

Extensive datasets support ongoing target generation, including drilling, soil and termite mound sampling. Aeromagnetic and electromagnetic surveys are planned to generate further exploration targets. Beyond the defined Mineral Resources, there are numerous prospects that have yet to be drill tested. A phased, property-wide exploration program is ongoing, with data review, target evaluation, and drill prioritisation currently underway.

There is a succession of targets and potential deposits in the "pipeline" and it will be important to continue to rank and upgrade these. There is significant potential to add to the Mineral Resources with the current exploration program.

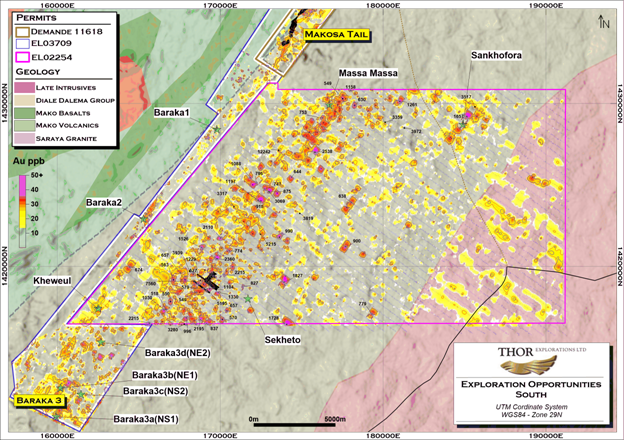

The acquisition of both the Douta West and Bousankhoba permits has allowed for a regional-scale exploration strategy that is largely underpinned by a comprehensive geochemical database (Figures 8 and 9). It is evident that, particularly in the southern regions, there are numerous geochemical targets of which only a few have been drill tested (Figure 4).

Extensive first stage exploration, completed over the Bousankhoba permit, has identified numerous geochemical targets associated with a major shear zone over an 18km strike length. Two prospects, Massa Massa and Sekhoto, are located along this zone. An additional prospect known as the Sakhofara is located 7km east of Massa Massa in the northern part of the permit and is defined by a 3.5km north-east trending geochemical anomaly.

To date follow-up Rotary Air Blast (RAB) drilling has been confined to the Sekhoto Prospect. The significant intersections obtained in the RAB drilling are yet to be followed up with systematic reverse circulation (RC) drilling.

The prospectivity of the permit is further enhanced by its location between Baraka 3 to the south and Basari Resource's Makabingui deposit to the north. It is possible that the mineralised shear zone extends through all three gold occurrences.

For 2026, Thor has budgeted US$9,000,000 for exploration in Senegal incorporating a minimum of 40,000 metres of drilling. The next results are expected later in Q1 2026, with a resource updated scheduled for Q3 2026 which will address further resources at Baraka 3.

Thor considers both the Bousankhoba and Douta West permits to be highly prospective with the potential to provide satellite resources that will complement the Douta Gold Project.

FINANCING

Thor intends to use its existing balance sheet to progress Douta into construction which is expected in 2026. The Company continues to generate strong cash flows from its Segilola mine and at the end of 2025 had a cash balance of US$137 million.

In addition to using its internal cash flows, the Company is in discussions with potential funding parties to support the construction of the Project.

A comprehensive financing strategy will be communicated alongside the Douta Investment Decision expected in H1 2026.

NEXT STEPS

Thor will continue engaging with the Senegalese government and progressing Douta towards start of construction in 2026 to achieve first gold in 2028.

Key next steps include:

· Commencement of detailed design

· Finalisation of Mining Convention

· Finalisation of financing package

· Ordering of long lead items

· Award of the EPC contract

· Continue evaluation and refinement of the metallurgical recoveries of the oxide, transitional and refractory ores

Figure 8: Project Area Showing Geochemical Anomalies and Exploration Opportunities

Figure 9: Southern Areas Showing Geochemical Anomalies and Exploration Opportunities

QUALIFIED PERSONS

The technical content of this news release has been reviewed and approved by the following Qualified Persons pursuant to NI 43-101 and the AIM Rules:

|

Mineral Resources: |

Alfred Gillman FAusIMM (CP), a full-time consultant to Thor and not independent |

|

Mineral Reserves: |

Dominic Claridge FAusIMM, AMC Consultants who is Independent of the Company |

|

Metallurgy and Processing: |

Robert Chesher FAusIMM (CP), AMC Consultants who is Independent of the Company |

Each QP has reviewed the relevant information in this release and consents to its publication.

ADDITIONAL TECHNICAL INFORMATION

The full NI 43-101 Technical Report supporting the PFS will be filed on SEDAR+ within 45 days of this release.

GLOSSARY OF TECHNICAL TERMS

All-in Sustaining Cost (AISC) - A comprehensive measure of the total cost of producing an ounce of gold (or another commodity) at a mine, which includes direct production costs, sustaining capital expenditures, and other ongoing operational costs required to maintain current production levels. AISC is used to provide a more complete picture of the economic sustainability of a mining operation.

Alternative Investment Market (AIM) - A sub-market of the London Stock Exchange designed for smaller, high-growth companies seeking to raise capital. AIM provides a platform for businesses that may not meet the full listing requirements of the main market, offering greater flexibility and lower regulatory burden. It is often used by mining, technology, and other emerging industries to access public investment.

Au - chemical symbol for gold.

AusIMM - Australian Institute of Mining and Metallurgy.

Block Model - A three-dimensional grid-based model of a mineral deposit, wherein each block represents estimated values such as grade, tonnage, and density derived through geostatistical methods.

CDIs - Chess Depositary Interests.

Circa (c.) - A term used to indicate that a specific date, number, or event is approximate or estimated.

CIL - Carbon in Leach processing.

CIM Definition Standards Guidelines - The CIM Definition Standards refer to a set of guidelines developed by the Canadian Institute of Mining, Metallurgy and Petroleum (CIM) for the classification and reporting of mineral resources and reserves. These standards provide a consistent framework for how mineral deposits should be defined, classified, and reported in Canada, ensuring that the information is both reliable and transparent. The CIM Definition Standards are aligned with the National Instrument 43-101 (NI 43-101) and are intended to guide the preparation of technical reports on mineral projects.

CP - Chartered Professional (of the AusIMM) An AusIMM Chartered Professional undergoes an accreditation process through the AusIMM Chartered Professional Program. Chartered status represents excellence within a relevant discipline and assurance of standards and professionalism for the mining industry.

Cut-off Grade - The lowest grade, or quality, of mineralised material that qualifies as economically mineable and available in a given deposit. May be defined on the basis of economic evaluation, or on physical or chemical attributes that define an acceptable product specification.

Diamond Drilling (DDH) - A method of drilling that produces cylindrical core samples using a diamond-impregnated bit; essential for detailed geological and structural interpretation.

Felsic- Felsic refers to silicate minerals, magma, and rocks which are enriched in the lighter elements such as silicon, oxygen, aluminium, sodium, and potassium.

Fire Assay - Fire assay is a traditional and highly precise method used to determine the gold content of a sample. In the Au-GRA21 method, the sample is first subjected to a high-temperature fusion process, where it is mixed with fluxes (such as lead oxide) and heated in a furnace to separate the gold. After the fusion, the resulting lead bead, which contains the gold, is separated and weighed. The gravimetric finish involves measuring the weight of the bead and calculating the gold content based on this weight. This method is considered one of the most accurate for determining gold content in ore samples.

General and Administrative (G&A) - Refers to the overhead costs associated with running a business or operation that are not directly tied to production or manufacturing. These costs typically include salaries of senior management, office supplies, legal fees, accounting services, and other corporate expenses that support the day-to-day operations but do not contribute directly to the production of goods or services.

Grade - Any physical or chemical measurement of the characteristics of the material of interest in samples or product. Note that the term quality has special meaning for diamonds and other gemstones. The units of measurement should be stated when figures are reported.

g/t - Grams per tonne; a standard unit expressing the concentration of precious metals in rock.

High Grade (HG) - Ore that contains a high concentration of gold compared to the surrounding mineralisation.

"In-Pit Resources" - Resources which are constrained by optimisation pit shells, with "current" economic inputs, which define minable mineralisation, and demonstrates reasonable prospects for eventual economic extraction.

Inverse Distance Squared (ID²) - A spatial interpolation technique used in geostatistics and geospatial analysis, where the value at a given point is estimated as a weighted average of values from nearby known points. The weighting decreases with increasing distance, with closer points contributing more to the estimate than those farther away.

Indicated Resource - An 'Indicated Mineral Resource' is that part of a Mineral Resource for which quantity, grade (or quality), densities, shape and physical characteristics are estimated with sufficient confidence to allow the application of Modifying Factors in sufficient detail to support mine planning and evaluation of the economic viability of the deposit.

Inferred Resource - An 'Inferred Mineral Resource' is that part of a Mineral Resource for which quantity and grade (or quality) are estimated on the basis of limited geological evidence and sampling. Geological evidence is sufficient to imply but not verify geological and grade (or quality) continuity. It is based on exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes.

Initial Rate of Return (IRR) - A financial metric used to evaluate the profitability of an investment or project. The Initial Rate of Return (IRR) represents the percentage return expected from the investment based on initial capital expenditures and projected future cash flows. It is often used in project evaluation to determine whether the expected returns justify the investment.

km - Kilometres.

Kriging (Kr) - A geostatistical interpolation technique used to predict the value of a spatially distributed variable at unsampled locations, based on observed values at nearby locations.

Life of Mine (LOM) - The total period during which a mining operation is expected to be economically viable, from the commencement of extraction to the depletion of the mineral resource or ore body. It is determined based on the size of the resource, extraction rate, and economic factors such as market conditions and operational costs.

m - Metres.

Fellow of the Australasian Institute of Mining & Metallurgy (FAusIMM) - FAusIMM is a professional designation conferred by the Australasian Institute of Mining & Metallurgy (AusIMM) to individuals who have met the requisite qualifications and experience in the mining and resources sector. This membership grade signifies a commitment to professional development, adherence to industry standards.

Mineralisation - Any single mineral or combination of minerals occurring in a mass, or deposit, of economic interest. The term is intended to cover all forms in which mineralisation might occur, whether by class of deposit, mode of occurrence, genesis or composition.

Mineral Resource Estimate (MRE) - A quantitative estimate of the quantity, quality, and grade of a mineral deposit, typically based on geological data, sampling, and modelling techniques. MREs are classified according to confidence levels, ranging from Inferred to Indicated and Measured resources, with higher confidence estimates being supported by more extensive data and detailed analysis.

Mining - All activities related to extraction of metals, minerals and gemstones from the earth whether surface or underground, and by any method (e.g. quarries, open cast, open cut, solution mining, dredging, etc).

Modifying Factors - are considerations used to convert Mineral Resources to Ore Reserves. These include, but are not restricted to, mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social and governmental factors.

Moz - Million ounces.

MT - Million tonnes.

Net Present Value (NPV) - The post-tax, pre-debt real cash flow measure derived by discounting future cash flows-accounting for operating costs, capital expenditures, and forecast macro-economic parameters-to present value.

NI 43-101 - The National Instrument 43-101 (NI 43-101) is a Canadian regulation that establishes standards for the disclosure of mineral exploration, resource estimation, and mining technical information. It was implemented by the Canadian Securities Administrators (CSA) to ensure that all public companies in Canada adhere to consistent, rigorous scientific and technical standards when reporting on mineral projects. NI 43-101 is widely used in the mining industry for the preparation of technical reports, particularly regarding mineral resources and reserves, to ensure the accuracy and reliability of data presented to investors and stakeholders.

Open Pit - A surface mining method involving excavation of ore from an open cut, applied in several Ariana projects such as Kiziltepe and Tavsan.

Ordinary Kriging (OK) - A commonly used geostatistical estimation method assuming constant mean within a domain, producing optimal grade predictions based on sample data. See Kriging.

Ore Reserve - An 'Ore Reserve' is the economically mineable part of a Measured and/or Indicated Mineral Resource. It includes diluting materials and allowances for losses, which may occur when the material is mined or extracted and is defined by studies at Pre-Feasibility or Feasibility level as appropriate that include application of Modifying Factors. Such studies demonstrate that, at the time of reporting, extraction could reasonably be justified.

Ore Loss - The portion of ore that is not recovered during the mining process, typically due to inefficiencies in extraction, handling, or processing. Ore loss can occur due to geological factors, equipment limitations, or operational constraints and is a key consideration in determining the overall efficiency and profitability of a mining operation.

oz - Troy ounce; a unit of weight used for precious metals, equivalent to 31.1035 grams.

Pre-Feasibility Study (PFS) - A Preliminary Feasibility Study (Pre-Feasibility Study) is a comprehensive study of a range of options for the technical and economic viability of a mineral project that has advanced to a stage where a preferred mining method, in the case of underground mining, or the pit configuration, in the case of an open pit, is established and an effective method of mineral processing is determined. It includes a financial analysis based on reasonable assumptions on the Modifying Factors and the evaluation of any other relevant factors which are sufficient for a Competent Person, acting reasonably, to determine if all or part of the Mineral Resources may be converted to an Ore Reserve at the time of reporting. A Pre-Feasibility Study is at a lower confidence level than a Feasibility Study.

Probable Ore Reserves - A Probable Ore Reserve is the economically mineable part of an Indicated, and in some circumstances, a Measured Mineral Resource. The confidence in the Modifying Factors applying to a Probable Ore Reserve is lower than that applying to a Proved Ore Reserve.

Proved Ore Reserves - A Proved Ore Reserve is the economically mineable part of a Measured Mineral Resource. A Proved Ore Reserve implies a high degree of confidence in the Modifying Factors.

QA/QC - Quality Assurance and Quality Control; systematic procedures used to ensure the integrity, precision, accuracy, and reproducibility of sampling and analytical results.

Recovery - The percentage of material of interest that is extracted during mining and/or processing. A measure of mining or processing efficiency.

Shear Zone - A structural feature comprising intensely deformed rock due to differential movement, often serving as a conduit for mineralising fluids.

t - Metric Tonnes. An expression of the amount of material of interest irrespective of the units of measurement.

Waste - The unintentional mixing of waste material with ore during the mining process, leading to a decrease in the overall grade of the mined ore. Waste dilution typically occurs during drilling, blasting, or handling, and can affect the quality of the final product and the overall economics of a mining operation.

ABOUT THOR

Thor Explorations Ltd. is a mineral exploration company engaged in the acquisition, exploration, development and production of mineral properties located in Nigeria, Senegal, Cote d'Ivoire and Burkina Faso. Thor Explorations holds a 100% interest in the Segilola Gold Project located in Osun State, Nigeria, a 100% economic interest in the Douta Gold Project located in south-eastern Senegal and a 100% interest in the Guitry Gold Project in Cote d'Ivoire. Thor Explorations trades on AIM and the TSX Venture Exchange under the symbol "THX".

CONTACT

Thor Explorations Ltd

Email: info@thorexpl.com

Canaccord Genuity (Nominated Adviser & Broker)

James Asensio / Henry Fitzgerald-O'Connor / Harry Rees

Tel: +44 (0) 20 7523 8000

Hannam & Partners (Broker)

Andrew Chubb / Matt Hasson / Jay Ashfield / Franck Nganou

Tel: +44 (0) 20 7907 8500

BlytheRay (Financial PR)

Tim Blythe / Megan Ray / Said Izagaren

Tel: +44 207 138 3203

Yellow Jersey PR (Financial PR)

Charles Goodwin / Shivantha Thambirajah

Tel: +44 (0) 20 3004 9512

CAUTIONARY STATEMENT

This news release contains forward‑looking statements and forward‑looking information. All statements herein, other than statements of historical fact, relate to future events, results, outcomes or performance and are based on expectations, estimates and projections as of the date of this release. Forward‑looking statements include, without limitation, statements regarding the results of the PFS, anticipated capital and operating costs, projected economic outcomes, the ability to finance the Project, the timing and advancement of development activities, the potential to bring the Project into operation, future production expectations, and the intended use of proceeds.

Forward‑looking statements are often identified by words such as "may", "could", "should", "would", "suspect", "outlook", "believe", "anticipate", "estimate", "expect", "intend", "plan", "target", and similar expressions, or by discussions of events or conditions that may occur in the future. Such statements are subject to a variety of risks, uncertainties and assumptions-many of which are beyond the Company's control-that could cause actual results or events to differ materially from those expressed or implied. These risks and uncertainties include, but are not limited to, changes in economic conditions, variations in PFS assumptions, metallurgical performance, permitting timelines, availability of financing, construction and operational risks, commodity price fluctuations, and other factors that could affect the Project's development.

Readers are cautioned that a PFS is preliminary in nature, includes assumptions that may be refined through further technical work, and cannot provide certainty that the Project will be realised as contemplated. Forward‑looking statements speak only as of the date of this release. The Company does not undertake any obligation to update or revise such statements except as may be required by applicable law.

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.

Latest directors dealings

- 21 minutes ago 3i Group

- 30 minutes ago Jardine Matheson Holdings Ltd (Singapore Reg)

- 37 minutes ago Marks & Spencer Group

- 1 hour ago Focusrite

- 3 hours ago BHP Group Limited NPV (DI)