Final Results

Summary by AI BETAClose X

15 January 2026

Safestore Holdings plc

("Safestore", "the Company" or "the Group")

Results for the year ended 31 October 2025

Strong operational performance, investment in future growth and earnings at an inflection point

|

|

2025 |

2024 |

Change (Total) |

Change (CER)2 |

|

FINANCIAL METRICS |

|

|

|

|

|

Total Revenue (£'m) |

234.3 |

223.4 |

4.9% |

5.0% |

|

LFL14 Revenue (£'m) |

228.7 |

221.9 |

|

3.1% |

|

Underlying EBITDAR4 (£'m) |

137.0 |

135.4 |

1.2% |

1.3% |

|

Operating Profit (£'m) |

159.3 |

425.8 |

(62.6%) |

|

|

Underlying Profit before Tax5 (£'m) |

92.9 |

97.0 |

(4.2%) |

|

|

Statutory Profit before Tax (£'m) |

127.1 |

398.6 |

(68.1%) |

|

|

Adjusted Diluted EPRA EPS11 (pence) |

40.3 |

42.3 |

(4.7%) |

|

|

Dividend per share (pence) |

30.70 |

30.40 |

1.0% |

|

|

Balance Sheet Metrics |

|

|

|

|

|

EPRA Basic NTA13 per Share (pence) |

1,129 |

1,091 |

3.5% |

|

|

Net Assets (£'m) |

2,288.4 |

2,226.8 |

2.8% |

|

|

Net cash inflow from operating activities (£'m) |

99.9 |

95.9 |

4.2% |

|

|

Net debt (£'m) |

1,058.6 |

899.5 |

17.7% |

|

|

Loan to value ratio (LTV) %16 |

28.1% |

25.1% |

3.0ppt |

|

|

OPERATING METRICS |

|

|

|

|

|

Maximum Lettable Area ("MLA")8 m sq ft |

9.3 |

8.6 |

8.0% |

|

|

Current Lettable Area ("CLA")3 m sq ft |

8.5 |

8.2 |

3.9% |

|

|

Closing Occupancy7 (% of CLA) |

78.1% |

78.0% |

0.1ppt |

|

|

LFL Closing Occupancy (% CLA) |

81.2% |

80.0% |

1.2ppt |

|

|

Group REVPAF10 (£ / sq ft) |

27.47 |

27.77 |

(1.1%) |

(1.0%) |

|

LFL REVPAF (£ / sq ft) |

28.93 |

28.12 |

|

2.9% |

.

HIGHLIGHTS

Financial and operational progress

· Group revenue at constant exchange rates (CER) up 5.0% to £234.3 million, with 3.1% LFL growth; positive LFL growth across all geographies and increasing contribution from non-LFL stores:

- UK revenue +3.3% improved through the year reaching £167.5 million, with increasing domestic occupancy, unit partitioning and higher average storage rates9 driving LFL growth of 2.4%

- Paris revenue of €52.6 million +2.5% reflects solid LFL growth of 1.3% with increasing occupancy and flat average rates

- Expansion Markets15 total revenue of €26.2 million +27.0%; strong growth in LFL (+13.5%) and non-LFL stores; Spain, Netherlands and Belgium all performed well;

· Underlying store EBITDAR increased by 3.1% to £155.9 million; inflationary cost pressures were partially offset by internal efficiencies, resulting in LFL cost of sales increase of 4.4%, broadly in line with sales and below the previously guided rise of 7-8%

· Underlying EBITDAR was £137.0 million, up 1.2%, lower growth than store EBITDAR growth due to higher administrative costs

· Operating profit down 62.6% to £159.3 million due to lower property revaluation gains of £23.1 million in FY 2025 (FY 2024: £292.2 million)

· Underlying net finance costs increased by £5.0 million to £26.4 million due to increased borrowings to support the store expansion programme

· Underlying profit before tax of £92.9 million declined by 4.2% reflecting the higher interest charge. The resulting Adjusted Diluted EPRA EPS was 40.3p, in line with consensus estimates. Statutory profit before tax of £127.1 million and Basic EPS of 50.9 pence declined 68.1% and 70.1% respectively, as a result of lower fair value gains on investment properties than in FY 2024

· Dividend per share of 30.70p, up 1%, underpinned by robust cash flow from operating activities, in line with progressive dividend policy and reflecting confidence in future prospects

· Balance sheet remained strong with £2.3 billion of net assets growing 2.8% in the year. LTV ratio of 28.1% and interest cover ratio ("ICR")17 of 4.0x; capital structure underpinned by investment property valuation of £3.5 billion

Strategy on track, with pipeline being executed as planned

· Continued focus on REVPAF to optimise trading in our existing store portfolio where we see significant potential to drive further EBITDA growth from both LFL and non-LFL stores. Recently opened (non-LFL) stores on track to meet 10% yield on cost18 hurdle, with stores opened 2016-2021 achieving between 10%-20%

· £80 million investment in store development resulted in MLA growing by a further 8% or 0.7 million sq ft to 9.3 million sq ft in FY 2025, with the addition of 13 new stores and 1 extension, representing the largest organic space increase in our recent history. In total since FY 2023 we have added 1.5 million sq ft, a 19% uplift to MLA

· £38.9 million investment in Italy through a new 50:50 joint venture with Nuveen established in December 2024 with stores performing in line with expectations

· Further enhancement of our technology-led operating model that combines centralised efficiency and local expertise with accelerated AI integration across marketing, pricing, and sales to optimise revenue performance

· We continue to make good progress towards our target of operational net zero with a 22% reduction in emissions intensity to 0.64 kgCO2e/ m2

Outlook and guidance

· Q1 trading to date has shown a continuation of the trend in LFL growth from FY 2025 across all our markets

· FY 2026 outlook: cautiously optimistic with a return to earnings growth

o Underlying LFL cost of sales growth expected to be 3%-6%

o Underlying net finance costs projected to increase by £1-£2 million

o Capital expenditure on new stores of £86 million

o 417k sq ft of additional MLA with a further 678k sq ft MLA in FY 2027 and beyond.

· On track to deliver the £35-£40 million of incremental EBITDA from non-LFL stores and pipeline on stabilisation

Frederic Vecchioli, Safestore's Chief Executive Officer, commented:

"Safestore's performance in FY 2025 reflects strong operational execution and investment in future growth. I want to thank our teams across the business for their hard work and commitment throughout the year. We continued to drive REVPAF and optimise trading across the like-for-like estate, which remains a key engine of profit growth for the Group. We also demonstrated good cost control, and this continues to be a focus. The dividend was up 1%, an important part of the total return for our shareholders.

Our new and recently opened stores are performing well across the portfolio, and, together with the development pipeline of a further 20 stores, are expected to contribute an additional £35-£40 million of EBITDA to the Group upon stabilisation.

We have entered the new financial year with confidence, and on the back of solid trading in the first quarter to date. Safestore is now at an inflection point, where the significant investment we have made in MLA expansion is driving revenue growth and is set to translate into meaningful growth in earnings and long term value creation."

For further information, please contact:

|

Safestore Holdings PLC |

|

|

Frederic Vecchioli, Chief Executive Officer Simon Clinton, Chief Financial Officer |

020 8732 1500 |

|

|

|

|

|

|

|

|

|

|

FTI Consulting |

|

|

Dido Laurimore |

020 3727 1000 |

|

Richard Gotla Oliver Parsons |

safestore@fticonsulting.com |

Analyst and investor presentation

An analyst and investor presentation will be held at 9:30am GMT today, 15 January 2026.

Notes to Editors

· Safestore is the UK's largest self-storage group with 211 stores on 31 October 2025 comprising:

o 139 in the UK (78 in London and the South East, 61 in key metropolitan areas including Manchester, Birmingham, Glasgow, Edinburgh, Liverpool, Sheffield, Leeds, Newcastle, and Bristol)

o 34 in the Paris region

o 16 in Spain

o 15 in the Netherlands

o 7 in Belgium.

o Joint ventures: 7 stores in Germany under a joint venture agreement with Carlyle and 12 stores in Italy under a joint venture agreement with Nuveen.

· As of 31 October 2025, Safestore had a maximum lettable area ("MLA") of 9.28 million sq ft (excluding the expansion pipeline stores) of which 6.67 million sq ft was occupied.

· Safestore was founded in the UK in 1998 and acquired "Une Pièce en Plus" ("UPP") in France in 2004 which was founded in 1998 by the current Safestore Group CEO Frederic Vecchioli.

· Safestore has been listed on the London Stock Exchange since 2007 and entered the FTSE 250 index in October 2015.

· The Group provides storage to around 105,000 personal and business customers and employs over 850 people across the Safestore Group.

Notes

We prepare our financial statements using IFRS but we also use a few adjusted measures in assessing and managing the performance of the business. These measures are not defined under IFRS and they may not be directly comparable with other companies' adjusted measures and are not intended to be a substitute for, or superior to, any IFRS measures of performance. These include like-for-like figures, to aid in the comparability of the underlying business as they exclude the impact on results of purchased, sold, opened or closed stores; and constant exchange rate ("CER") figures are provided to present results on a more comparable basis, removing FX movements. These metrics are disclosed because management review and monitor performance of the business on this basis. We also include a few measures defined by the European Public Real Estate Association ("EPRA"), which are designed to enhance transparency and comparability across the European Real Estate sector; see notes 11 and 13 below and 'Non-GAAP financial information' in the notes to the financial statements.

1 - Where reported amounts are presented either to the nearest £0.1 million or to the nearest 10,000 sq ft, the effect of rounding may impact the reported percentage change.

2 - CER is Constant Exchange Rate (Euro denominated results for the current period are retranslated at the exchange rate effective for the comparative period. Euro denominated results for the comparative period are translated at the exchange rates effective in that period, in order to present the reported results for the current period on a comparable basis).

3 - CLA is Current Lettable Area excludes space not yet fitted out and space which is operationally unavailable from MLA (Maximum Lettable Area). Measured in square feet ("sq ft").

4 - Underlying EBITDAR was previously termed Underlying EBITDA. It is defined as Operating Profit before exceptional items, share-based payments, corporate transaction costs, change in fair value of derivatives, gain/loss on investment properties, depreciation, the net profit from joint ventures and associates, interest and tax. It has been renamed to ensure the name more closely reflects the nature of the financial measure.

5 - Underlying profit before tax is defined as underlying EBITDAR less leasehold costs6, depreciation charged on property, plant and equipment, net profit from joint ventures and associates, and net finance charges relating to bank loans and cash.

6 - Leasehold costs reflect the rental expense and therefore include both the lease liability interest element and the fair value re-measurement of lease liabilities.

7 - Occupancy excludes offices but includes bulk tenancy.

8 - MLA is Maximum Lettable Area. Measured in square feet ("sq ft").

9 - Average storage rate is calculated as the revenue generated from self-storage divided by the average square footage occupied during the period in question.

10 - Revenue per Available Square Foot ("REVPAF") is an alternate performance measure used by the business and is considered by management as the best KPI of economic performance of a mature self-storage asset as it is the net outcome of the occupancy/rate mix plus ancillary sales. It is calculated by dividing revenue for the period by weighted average available square feet for the same period.

11 - Adjusted Diluted EPRA EPS is based on EPRA's definition of Earnings and is defined as profit or loss for the period after tax but excluding corporate transaction costs, change in fair value of derivatives, gain/loss on investment properties and the associated tax impacts. The Company then makes further adjustments for the impact of exceptional items, IFRS 2 share-based payment charges, exceptional tax items, and deferred tax charges. This adjusted earnings is divided by the diluted number of shares. The IFRS 2 cost is excluded as it is written back to distributable reserves and is a non-cash item (with the exception of the associated National Insurance element). Therefore, neither the Company's ability to distribute nor pay dividends are impacted (with the exception of the associated National Insurance element). The financial statements will disclose earnings on a statutory, EPRA and Adjusted Diluted EPRA basis and will provide a full reconciliation of the differences in the financial year in which any LTIP awards may vest.

12 - Cash flow before investing activities is defined as net cash inflow from operating activities less leasehold cost payments..

13 - EPRA's Best Practices Recommendations guidelines for Net Asset Value ("NAV") metrics are EPRA Net Tangible Assets ("NTA"), EPRA Net Reinstatement Value ("NRV") and EPRA Net Disposal Value ("NDV"). EPRA NTA is considered to be the most relevant measure for the Group's business which provides sustainable long term progressive returns and is now the primary measure of net assets. The basis of calculation, including a reconciliation to reported net assets, is set out in note 15 to the financial statements.

14 - Like‐for‐like ("LFL") information includes only those stores which have been open throughout both the current and prior financial years, with adjustments made to remove the impact of new and closed stores, as well as corporate transactions.

15 - Expansion Markets comprise Spain, the Netherlands and Belgium plus income earned in relation to the associate in Germany and the joint venture in Italy.

16 - LTV ratio is loan to value ratio, which is defined as net debt (excluding lease liabilities) as a proportion of the valuation of investment properties and investment properties under construction (excluding lease liabilities).

17 - ICR is interest cover ratio and is calculated as the ratio of underlying EBITDA after leasehold costs to underlying finance charges.

18 - Yield on cost is defined as incremental EBITDA divided by the initial investment in a new store.

Reconciliations between underlying metrics and statutory metrics can be found in the financial review and financial statements sections of this announcement.

CEO REVIEW

Group Summary

Safestore delivered an encouraging performance in FY 2025, with LFL growth improving through the year, a strong non-LFL revenue contribution and further delivery of our store expansion programme. We achieved this against a backdrop of lacklustre GDP growth, demonstrating the resilience of the underlying demand for our self-storage offer. Revenue growth and store EBITDAR performance were robust across all our geographies, notwithstanding the anticipated inflation-driven cost challenges and the profit drag impact of a higher number of new store openings. The slight decline in underlying profit before tax and adjusted diluted EPRA EPS was driven by increased debt to fund the store development programme, which we are confident will contribute significantly to future earnings growth. Overall, the results for the year reflect progress against our strategy to optimise the trading performance of the existing store portfolio and take advantage of selective expansion opportunities, whilst maintaining a strong balance sheet.

Financial summary

Group revenues grew 5.0% (CER) in total to £234.3 million, with LFL sales growth of 3.1% and newly opened (non-LFL) stores contributing £5.9 million of revenue, up from £1.5 million in the prior year. Underlying store EBITDAR was £155.9 million, up 3.2% (CER), a good performance as we absorbed well-documented inflationary cost increases and the incremental costs of rolling out new stores. The underlying LFL cost of sales increase of 4.4% was below our previously guided rate of 7%-8%, helped by operational efficiencies identified during the year which will continue to flow through in FY 2026. LFL store EBITDAR margins remained strong at 67.6%.

Underlying central administrative costs increased by £3.1 million or 19.6% to £18.9 million due to investments in technology capabilities to enhance our data-led customer service and to support our larger portfolio as well as re-established variable pay for Head Office colleagues. This resulted in underlying EBITDAR of £137.0 million, up 1.3% (CER). Net finance costs rose by £5.0 million to £26.4 million due to an increase in borrowings to fund the store expansion programme. This impacted underlying PBT, which declined by 4.2% to £92.9 million. In turn, Adjusted Diluted EPRA EPS fell by 4.7% to 40.3 pence.

Statutory profit before tax was £127.1 million (FY 2024: £398.6 million) reflecting a lower gain on investment properties compared to the prior year. Basic EPS was 50.9 pence (FY 2024: 170.5 pence).

Cash flow before investing activities12 grew to £89.6 million (FY 2024: £86.2 million). We incurred total capex of £109.2 million, including £80 million on new store development compared to £81 million in FY 2024. FY 2025 represented the peak MLA opening year for the current pipeline development which runs to FY 2027 and beyond. Net debt increased by £159.1 million to fund the store programme as planned, with a new five-year term loan of €77.5 million and a new eight-year €70.0 million USPP arranged to refinance a portion of the drawn RCF. The average blended cost of debt fell by 0.5ppt to 3.46% due to lower rates on floating debt facilities and a higher proportion of Euro denominated borrowings following the pro-active conversion of €150 million of drawn facilities from GBP to EUR. Our balance sheet remains strong: interest cover was 4.0x (FY 2024: 4.3x) and LTV stood at 28.1% (FY 2024: 25.1%).

Safestore's capital structure is underpinned by the valuation of our investment properties which was £3,245.9 million (FY 2024: £3,052.9 million) at the year-end reflecting the stable valuation of the LFL estate and growth from the value created by our new store development.

Trading summary

Stores in our LFL portfolio (>two years old and 89% of MLA) delivered revenue growth of 3.1% year on year. LFL closing occupancy was 81.2%, up 1.2ppt, and LFL REVPAF at a Group level was up 2.9% to £28.93. This is a pleasing performance and reflects our relentless focus on optimising trading in our existing store base.

Within the LFL estate, our mature stores (>five years old and 79% of MLA) delivered 1.9% revenue growth through improvements in average storage rate. Also within the LFL estate, our stabilising stores (sites two-five years old and 10% of MLA), delivered good occupancy and REVPAF growth, contributing 1.2ppt of the total 3.1% LFL growth. Their performance underlines the opportunity to drive highly profitable growth as they trade towards more mature occupancy levels.

Non-LFL stores (<two years old and 11% of MLA) delivered strong revenue growth, contributing an additional £4.4 million of sales to the Group (CER) as they quickly grow their occupancy and build REVPAF.

From a geographic perspective, in the UK our performance was driven by higher domestic customer demand and the continued conversion of space to smaller units that command higher rates. The UK business produced encouraging LFL revenue growth of +2.4% and successfully offset inflationary cost pressures and the impact of new store investment to achieve a stable store EBITDAR margin for the year. In Paris, economic conditions remained tough, but the business still produced robust revenue and store EBITDAR growth and demonstrated excellent cost control. Our stores in Expansion Markets (Spain, the Netherlands and Belgium) delivered a strong trading performance and also a significant increase in store EBITDAR as newer stores started covering their costs.

Portfolio and pipeline

We continued to deliver successfully on our new space programme. MLA at the year end was 9.3 million sq ft, an 8% or 0.7 million sq ft increase over the year with 13 new stores added. Our owned portfolio has a total of 211 stores across five geographies with significant strength in dense, metropolitan areas that hold high barriers to entry for new site development. We opened two stores in the UK (+1.7% to regional MLA), four in Paris (+16.8% to regional MLA) and four stores in Spain (taking the number there to 16 and adding 45.5% to regional MLA). New stores are trading in line with our expectations and are on track to meet our hurdle yield on cost return rate of 10%, the highest in the industry. In addition, our newly established joint venture with Nuveen in Italy is performing well and together with our track record gives us confidence that these joint venture relationships provide an excellent route to grow our network.

Looking ahead, we are on track to deliver an additional 416,600 sq ft in FY 2026, a 4.5% uplift to Group MLA. The total pipeline of new space remains at 1.1 million sq ft as at the end of FY 2025, with three further sites added to the pipeline since the half year results.

Platform and technology highlights

We made good progress in building our digital scale and the value of our proprietary 27-year data set of over 2 million lets, further strengthening our competitive advantage. In FY 2025 we accelerated the integration of advanced AI across marketing, pricing and property development capabilities that smaller operators cannot replicate. Major initiatives in marketing - including refining expenditure allocation through a proprietary AI-driven Customer Value Model that optimises pay-per-click spend, the use of Google reviews sentiment tracking and AEO search visibility partnerships - helped to maintain our overall marketing spend at 4.1% of revenues whilst enhancing enquiry capture. In pricing architecture, we developed our predictive modelling which anticipates occupancy trends and churn risks. This enables more proactive revenue management, for example through targeted discounting for low conversion segments. The operational productivity of our sales teams continued to improve with the use of enquiry conversion scoring models and automated sales calls transcript analysis to drive performance coaching and ultimately revenue generation.

Our priorities in FY 2026 are to grow REVPAF across all our stores, continue our efforts to minimise cost growth and find efficiencies, deliver the pipeline of new stores on time and on budget, maintain our disciplined approach to investment and continue with our proactive debt management. Together, we expect these core elements of our strategy will generate long term, sustainable growth in earnings.

Dividend

The Board is pleased to increase the dividend by 1% to 30.70 pence for the full year, of which 20.60 pence is payable as a final dividend in April. We will continue to pursue a progressive dividend policy whilst rebuilding dividend cover over the medium term.

Outlook

We are cautiously optimistic about the year ahead, in which we expect earnings per share growth to resume. Q1 like-for-like growth to date is tracking last year's trends, despite the lacklustre economic environment in many of our markets. We expect the inflationary cost pressures incurred in FY 2025 to ease in FY 2026, alongside further support from cost saving actions. We also anticipate a reduced earnings drag from new stores in FY 2026 as a fewer number of stores will be opened compared to FY 2025.

In FY 2026 we expect:

· LFL cost of sales growth of 3-6%;

· Underlying net finance costs increasing £1-£2 million;

· Year-on-year MLA growth of 4.5% (0.4 million sq ft) in FY 2026 with a further 7.3% MLA in FY 2027 and beyond; and

· Capital expenditure on new stores of £86 million.

Looking ahead, the Board is confident that the market dynamics for self-storage in the UK and Europe remain positive with our portfolio well positioned to deliver growth. We will continue to leverage and finesse our marketing and operational expertise to drive REVPAF and earnings. Growth will be driven by:

· EBITDA growth from LFL stores:

o Mature LFL stores (>five years old), which represent 79% of MLA, through rate improvements, benefits from UK partitioning, and cost inflation easing.

o Contribution from fully invested stabilising LFL stores (between two and five years old), which currently represent 10% of MLA, as they continue up the maturity curve, increase occupancy and build profitability.

· Increasing contribution from our non-LFL stores (1.0 million sq ft or 11% of MLA and < two years old) and our current pipeline of 1.1 million sq ft projected to open over the next few years. This 2.1 million sq ft of space will contribute increasingly to earnings as stores fill occupancy and cover their fixed costs. These stores are expected to generate an incremental £35-£40 million of EBITDA upon stabilisation.

· Our joint ventures in Germany and Italy present an opportunity to expand from a small footprint of stores with a lower initial capital outlay and management fee income. We see the potential for other opportunities with this model to drive longer term portfolio growth.

Trading and Operational Review

|

Trading Data* |

TOTAL |

LIKE-FOR-LIKE |

||||

|

Revenue metrics |

2025 |

2024 |

Change |

2025 |

2024 |

Change |

|

Revenue (millions) |

|

|

|

|

|

|

|

Group (GBP) |

£234.3 |

£223.4 |

4.9% |

£228.7 |

£221.9 |

3.1% |

|

UK (GBP) |

£167.5 |

£162.2 |

3.3% |

£164.8 |

£161.0 |

2.4% |

|

Paris (EUR) |

€52.6 |

€51.3 |

2.5% |

€51.9 |

€51.2 |

1.3% |

|

Expansion Markets (EUR) |

€26.2 |

€20.5 |

27.0% |

€23.0 |

€20.1 |

13.5% |

|

|

|

|

|

|

|

|

|

Average rate (per sq ft) |

|

|

|

|

|

|

|

Group (GBP) |

£30.20 |

£29.85 |

1.2% |

£30.58 |

£29.90 |

2.3% |

|

UK (GBP) |

£30.68 |

£29.94 |

2.5% |

£30.71 |

£29.95 |

2.5% |

|

Paris (EUR) |

€41.81 |

€42.28 |

(1.1%) |

€42.51 |

€42.33 |

0.4% |

|

Expansion Markets (EUR) |

€24.30 |

€23.28 |

4.4% |

€25.29 |

€23.44 |

7.9% |

|

|

|

|

|

|

|

|

|

REVPAF (per sq ft) |

|

|

|

|

|

|

|

Group (GBP) |

£27.47 |

£27.77 |

(1.1%) |

£28.93 |

£28.12 |

2.9% |

|

UK (GBP) |

£29.24 |

£28.85 |

1.3% |

£29.56 |

£28.77 |

2.8% |

|

Paris (EUR) |

€37.33 |

€39.13 |

(4.6%) |

€39.04 |

€39.39 |

(0.9%) |

|

Expansion Markets (EUR) |

€18.79 |

€18.48 |

1.7% |

€23.00 |

€20.38 |

12.9% |

|

|

|

|

|

|

|

|

|

Space and occupancy metrics |

2025 |

2024 |

Change |

2025 |

2024 |

Change |

|

Closing occupancy (million sq ft) |

|

|

|

|

|

|

|

Group |

6.67 |

6.41 |

4.0% |

6.33 |

6.34 |

(0.1%) |

|

UK |

4.52 |

4.54 |

(0.4%) |

4.43 |

4.51 |

(1.8%) |

|

Paris |

1.19 |

1.09 |

8.4% |

1.12 |

1.09 |

3.2% |

|

Expansion Markets |

0.96 |

0.78 |

23.4% |

0.78 |

0.74 |

5.8% |

|

|

|

|

|

|

|

|

|

Closing occupancy (% of CLA) |

|

|

|

|

|

|

|

Group |

78.1% |

78.0% |

0.1ppt |

81.2% |

80.0% |

1.2ppt |

|

UK |

79.9% |

79.6% |

0.3ppt |

80.6% |

80.3% |

0.3ppt |

|

Paris |

81.2% |

81.9% |

(0.7ppt) |

84.8% |

82.7% |

2.1ppt |

|

Expansion Markets |

67.3% |

65.5% |

1.8.ppt |

79.7% |

74.4% |

5.3ppt |

|

|

|

|

|

|

|

|

|

MLA (million sq ft) |

|

|

|

|

|

|

|

Group |

9.28 |

8.59 |

8.0% |

8.24 |

8.23 |

0.1% |

|

UK |

5.98 |

5.88 |

1.7% |

5.79 |

5.81 |

(0.3%) |

|

Paris |

1.66 |

1.42 |

16.8% |

1.40 |

1.37 |

2.1% |

|

Expansion Markets |

1.64 |

1.29 |

27.1% |

1.05 |

1.05 |

- |

|

|

|

|

|

|

|

|

|

CLA (million sq ft) |

|

|

|

|

|

|

|

Group |

8.54 |

8.22 |

3.9% |

7.80 |

7.92 |

(1.6%) |

|

UK |

5.66 |

5.70 |

(0.8%) |

5.49 |

5.61 |

(2.1%) |

|

Paris |

1.46 |

1.34 |

9.3% |

1.32 |

1.31 |

0.6% |

|

Expansion Markets |

1.42 |

1.19 |

20.1% |

0.99 |

1.00 |

(1.2%) |

*all total numbers reported using the reported exchange rate. LFL measures all reported at CER where applicable.

Geographic underlying performance - P&L in Local Currencies

|

|

FY 2025 |

FY 2024 |

||||||

|

Underlying performance |

UK |

Paris |

Exp Mkt |

Total (CER) |

UK |

Paris |

Exp Mkt |

Total (CER) |

|

|

£'m |

€'m |

€'m |

£'m |

£'m |

€'m |

€'m |

£'m |

|

|

|

|

|

|

|

|

|

|

|

LFL |

164.8 |

51.9 |

23.0 |

228.7 |

161.0 |

51.2 |

20.1 |

221.9 |

|

Non-LFL |

2.7 |

0.7 |

3.2 |

5.9 |

1.2 |

0.1 |

0.4 |

1.5 |

|

Total revenue |

167.5 |

52.6 |

26.2 |

234.6 |

162.2 |

51.3 |

20.5 |

223.4 |

|

|

|

|

|

|

|

|

|

|

|

LFL |

109.1 |

39.4 |

14.1 |

154.6 |

108.8 |

37.6 |

11.6 |

150.8 |

|

Non-LFL |

1.0 |

(0.4) |

0.9 |

1.4 |

0.7 |

- |

(0.5) |

0.4 |

|

Total store EBITDAR |

110.1 |

39.0 |

15.0 |

156.0 |

109.5 |

37.6 |

11.1 |

151.2 |

|

LFL store EBITDAR margin |

66.2% |

75.9% |

61.3% |

67.6% |

67.6% |

73.4% |

57.7% |

68.0% |

UK (64% of MLA, 139 stores)

Our operational performance in the UK reflects a continuously improved revenue trajectory through the year. Total revenue was up 3.3% to £167.5 million with LFL growth of 2.4% to £164.8 million.

Driven by increased product adoption, demand from domestic customers remained robust throughout the year, with space occupied up 3.4% at year-end, enabling us to accelerate our partitioning programme by converting larger units into smaller units better suited to domestic customer demand.

The programme is reducing our historical overweight to larger units (>250 sq ft) within our UK portfolio, resulting in more smaller and higher yielding configurations and enabling a more typical 70/30 domestic/business customer split in terms of space occupied. We intend to convert a total of 500,000 sq ft (out of an initial total of approximately 1 million sq ft) of larger units into smaller units over two years and made good progress in FY 2025 with 190,000 sq ft completed. We expect to convert the balance in FY 2026 and 2027. As smaller units have a higher rental value/sq ft, this has a positive impact on the average rate we achieve and ultimately will drive REVPAF growth.

LFL occupancy closed broadly flat year on year at 80.6% with occupied space in units smaller than 250 sq ft increasing 1.4% and occupied space in larger units decreasing by 132,000 sq ft (15.7%). Business occupied space is down 6.2% on FY 2024, with the level impacted by the unit partitioning programme described above. This change in mix to smaller units and domestic customers contributed to the increase of 2.5% in the achieved rate for LFL stores, reflecting the Group's strategy to optimise REVPAF.

In the year there were eleven UK stores still stabilising and included in LFL. These stores, which are between two and five years old, increased their occupancy and provided a meaningful contribution to LFL revenue growth. We expect stabilised occupancy of 85%-90% in our UK LFL portfolio, compared to the 80.6% achieved in FY 2025, with further occupancy growth in stabilising stores expected to be a contributing driver in closing this gap.

In addition to our LFL portfolio we have opened six stores since the end of FY 2023 which are currently classified as non-LFL. These stores contributed £1.5 million to year-on-year revenue growth in the financial year and are performing in line with their expected maturity curve.

The UK LFL store EBITDAR margin fell to 66.2% (FY 2024: 67.6%). This was due to an increase in the LFL cost of sales base of 6.9% to £55.7 million driven largely by inflation-linked increases in the National Living Wage and National Insurance impacting employee costs, and a 10.2% increase in business rates partially offset by savings from integrating call centre activities in stores and improved insurance costs. As a result, UK LFL store EBITDAR increased only slightly by £0.3 million to £109.1 million for the financial year.

The strong growth in revenue from non-LFL stores in the UK led to total EBITDAR for the UK to increase £0.6m or 0.5% year-on-year.

The mix of our customer base is depicted in the table below. The combined impacts of stronger demand from domestic customers and the partitioning of larger units, resulted in the proportion of domestic customers in the UK increasing to 63% of occupied sq ft at the end of FY 2025 (FY 2024: 59%).

|

|

|

|

|

|

|

|

|

Business and domestic Customers FY 2025 |

UK |

Paris |

Exp Mkt |

|

|

|

Domestic Customers |

|

|

|

|

|

|

Numbers (% of total) |

79% |

82% |

90% |

|

|

|

Sq ft occupied (% of total) |

63% |

66% |

83% |

|

|

|

Average length of stay (months) |

17.3 |

22.9 |

21.6 |

|

|

|

|

|

|

|

|

|

|

Business Customers |

|

|

|

|

|

|

Numbers (% of total) |

21% |

18% |

10% |

|

|

|

Sq ft occupied (% of total) |

37% |

34% |

17% |

|

|

|

Average length of stay (months) |

26.0 |

26.4 |

30.4 |

|

|

|

|

|

|

|

|

Paris (18% of MLA, 34 stores)

Our Paris business delivered €52.6 million revenue with LFL growth of 1.3% and non-LFL delivering €0.7 million of revenue. This was a steady result in context of the weaker economic conditions of the region in FY 2025.

On a LFL basis, closing occupancy increased 2.1ppt to 84.8% in the year, reflecting the strength of our unique portfolio of stores located in both city centre and suburban areas and our skills at driving and converting online enquires. The LFL average rate achieved was up 0.4% and LFL REVPAF was down slightly (0.9%) due to an additional 30,000 sq ft of CLA from two store extensions opened in the last 18 months. These extensions will support LFL revenue growth in Paris as they mature.

In FY 2024 and FY 2025, we opened a total of four new stores and one extension in Paris, with a further four in the pipeline which will take the number of stores in the market to 38. Non-LFL stores contributed €0.6 million to year-on-year revenue growth. This 31% growth in MLA means that our portfolio density within central Paris will increase substantially and whilst we expect that the new stores will be significant contributors to growth as they mature in the years ahead, we anticipate that performance of LFL stores may be impacted due to our approach of giving customers choice of storage locations and prices with cross-network space allocation.

The LFL Store EBITDAR margin rose to 75.9% mainly due to LFL cost of sales in Paris falling 8.1% year on year. This reflected a normalising bad debt provision and continued tight cost control, particularly in the dynamic management of staffing including lower store variable pay, together with savings in utilities through using Group procurement.

As a result, LFL store EBITDAR for Paris increased by a healthy 4.8% year on year to €39.4 million. Total store EBITDAR increased at a slightly lower rate of 3.7% reflecting the impact of new store openings.

Expansion Markets (18% MLA, 38 stores)

Our Expansion Markets continued to be a strong contributor to Group growth with LFL revenue increasing 13.5% to €23.0 million year on year and total revenue increasing 27.0% to €26.2 million.

Performance in each market was strong. In Spain (16 stores) revenue grew 22.9% on a LFL basis to €7.7m through both occupancy and rate improvements with growth supported by seven stabilising stores. LFL revenue in the Netherlands (15 stores) of €9.1m and Belgium (7 stores) of €5.5m grew by 10.1% and 13.0% respectively, achieved through both occupancy and rate increases.

LFL closing occupancy increased from 74.4% to 79.7% with the growth in particular coming from stabilising stores in the Netherlands and Spain as they fill up towards the Mature LFL store average level of 85.8% (FY 2024: 84.5%).

New stores and expansions contributed €3.2 million of non-LFL revenue, with growth of €2.8 million in the year, largely through openings in Spain.

Management fees from our joint ventures in Germany and Italy contributed €1.7 million to Expansion Market revenue (FY 2024: €0.8 million).

The LFL store EBITDAR margin increased to 61.3%, up 3.6ppts. LFL costs of sales for Expansion Markets increased 4.7%, reflecting a mix of normal inflationary increases and the timing of maintenance expenses. As a result, Expansion Markets LFL store EBITDAR increased 21.6% with store EBITDAR including non-LFL stores increasing 35.1% year-on-year.

Joint ventures and associates

We have an associate investment with Carlyle in Germany and a joint venture with Nuveen in Italy. These joint ventures represent a route for the Group to access new geographies and expand our managed portfolio with diluted risk and with lower capital deployed. We earn management fees which are recorded in Expansion Market revenue together with our share of the results of the joint ventures themselves.

Our associate in Germany has seven stores totalling 327,000 sq ft with a further five in its pipeline. Safestore owns 10% of the associate. The underlying share of losses for FY 2025, a £0.6 million loss (FY 2024: £nil), reflects one-off professional fees related to the establishment of the business and normalisation of leases.

We entered into the joint venture in Italy in December 2024 through the acquisition of a 50% share in EasyBox at a cost of £38.9 million. EasyBox comprises twelve stores (of which two opened in FY 2025) and is a leading platform in the emerging Italian storage market where the supply of self-storage is equivalent to 3% of that in the UK. The stores are located in the key economic centres of Rome, Florence and northern Italy, and total 821,675 sq ft. and are performing in line with our expectations. The underlying share of profit for FY 2025, a £0.5 million gain (FY 2024: £nil), reflects the profit for the first nine months of the 2025 calendar year.

MLA and CLA space and occupancy by geography

When developing new stores, we occasionally delay the full fit out of the interior of our stores to reflect the phasing of occupancy increases. In addition, through the partitioning programme space can be held as unavailable until it is converted. Together these areas which are still to be fitted out are not available to be leased and are hence excluded from CLA.

|

|

|

|

|

|

|

|

|

|

|

|

|

MLA (m sq ft) |

To be fitted out (m sq ft) |

Operationally unavailable (m sq ft) |

CLA (m sq ft) |

% Occupancy of MLA |

% Occupancy of CLA |

|

|

|

|

|

|

|

|

|

|

|

|

|

UK |

6.0 |

(0.2) |

(0.2) |

5.6 |

75.6% |

79.9% |

|

|

|

Paris |

1.7 |

(0.2) |

(0.0) |

1.5 |

71.3% |

81.2% |

|

|

|

Exp Mkt |

1.6 |

(0.2) |

(0.0) |

1.4 |

58.5% |

67.3% |

|

|

|

Total |

9.3 |

(0.6) |

(0.2) |

8.5 |

71.8% |

78.1% |

|

|

|

|

|

|

|

|

|

|

|

Pan-European platform for growth

Our operating model combines the benefits of centralised expertise with targeted local execution. Core strategic functions, including Marketing, IT, Revenue Management, Finance, and Construction Analytics, are delivered from our UK headquarters enabling efficient, consistent execution across all markets. This platform is integrated with local operational support teams which are deployed specifically in markets where on-the-ground expertise generates incremental value and enhances asset performance.

Digital platform capabilities serve as a critical differentiator within our industry for new lease enquiry generation and revenue optimisation. Our centralised, in-house teams of specialists together with our proprietary data set of years of historical leases enable the development of advanced marketing tools and machine-learning algorithms to drive performance. This provides us with a distinct competitive advantage over most of the market, which consists largely of smaller operators lacking the data depth required to replicate our price/occupancy optimisation approach.

During the year, we accelerated the integration of artificial intelligence ("AI") across our key business functions to drive operational efficiency, optimise revenue generation and enhance investment rigour. This includes in marketing, where we have refined expenditure allocation through a proprietary AI-driven Customer Value Model that optimises pay-per-click spend by feeding enquiry value data back to Google, alongside deploying generative AI to scale multi-lingual content effectively. We further strengthened our digital presence through Google reviews, sentiment tracking and AEO search visibility partnerships, while testing AI-led campaign expansion tools to monitor visibility and sentiment across emerging search platforms. In FY 2025 these initiatives enabled us to enhance our enquiry capture whilst maintaining a stable marketing cost of 4.1% of revenue (FY 2024: 4.1%).

We have further improved our pricing architecture through predictive modelling which anticipates occupancy trends and churn risks, enabling proactive revenue management. This includes targeted discounting for low conversion segments and elasticity modelling to optimize the timing and magnitude of rate management.

The operational productivity of our sales teams continued to improve with the use of enquiry conversion scoring models and automated sales calls transcript analysis to drive performance coaching. Additionally, the imminent rollout of custom AI agents will streamline internal procedural queries and credit control authorisations.

Finally, we bolstered our property development capabilities with demand and rate prediction models that analyse critical site attributes and provide data-driven validation for new site selection, significantly mitigating risk in untested markets and ensuring robust capital deployment.

The Safestore portfolio comprises both automated and staffed facilities. Through our technology platform, we are able to offer customers the option to choose a unit, start a contract fully online, and access their space all without human intervention.

Nevertheless, our data consistently demonstrates that staffed interactions drive superior financial outcomes, including higher conversion rates and better rental yields. In the UK, spontaneous adoption of a fully automated customer journey remained stable at approximately 8%. While 60% of our customers execute their contracts remotely, the majority, particularly first-time users, prioritise interaction with our professional teams before completing their e-contract. This consultative approach helps customers to select the correct unit size (preventing the 'over-estimation' common in self-service) and ensure they have the right level of customer goods protection, and which also supports our yield optimisation. Balancing automation with high value human interaction translates into both an industry-leading ancillary sales contribution (16.1% of total revenue in FY 2025) and REVPAF levels among the highest in the sector, growing by 2.9% on a LFL basis in the year.

We continue to make good progress towards our target of operational net zero with a 22% reduction in emissions intensity to 0.64 kgCO2e/ m2. We now have all stores powered by certified zero-carbon electricity with in-store improvements including fitting high efficiency lighting to customer units and removal of gas heating appliances making further contributions. We install solar panels on new openings where possible and increased our capacity by over 450kWp in FY 2025, and we expect this to further expand in FY 2026 to include fitting panels on mature stores.

Portfolio Review

Our store expansion model

We develop and acquire stores only when opportunities are expected to hit our hurdle rate of return and the investment ensures we remain within our balance sheet parameters through economic cycles. This disciplined approach has served us well, creating a portfolio that is hard to replicate and one that has driven a strong track record of growth whilst navigating the macroeconomic and interest rates cycles.

We focus on acquiring sites in dense, urban areas where we can leverage our scale and operational expertise, and where barriers to entry are high as supply is constrained by strict zoning regulations and a scarcity of suitable development land. This strategy is reflected in our recent development activity: of the 30 stores developed since 2023, three are located in London, five in Paris, ten in Barcelona and Madrid, and six in the Randstad in the Netherlands, reinforcing our market leadership in Europe's most valuable real estate territories. Over time it is expected that these locations will benefit from significant first-mover advantages as prime urban assets are largely irreplicable in today's planning environment, providing strong defensive characteristics in markets with deep and growing demand.

Development programme progress

In recent years we have stepped up our organic development programme to take advantage of new space opportunities and ensure longer term earnings growth for the portfolio. Since the beginning of FY 2023 we have developed 30 new stores totalling 1.4 million sq ft of new space through investing £222 million in new store capital expenditure, expanding the Group's MLA by 19.4% to 9.3 million sq ft.

Included in this, in FY 2025 we opened 13 new stores, adding 0.7 million sq ft to the portfolio which reached 211 stores. These openings mark a third consecutive year of opening eight or more new stores to generate long term growth.

The openings in the year include two in London, four in Paris and seven in Expansion Markets (Spain four stores, the Netherlands two stores, Belgium one store). New store locations are focused on key metropolitan areas in each country.

With these openings, we now have 38 stores in Expansion Markets reflecting our investment in countries where there are relatively low levels of supply and positioning our portfolio to capture the opportunity as these markets grow.

New stores opened added 662,200 sq ft of new space with an additional 15,400 sq ft of new space from the extension. This added 677,600 sq ft of space in total taking Group MLA at 31 October 2025 to 9.3m sq ft.

|

|

|

|

|

|

|

|

|

FY 2025 Stores Opened |

FH/LH |

MLA |

Development Type |

|

|

|

London - Lea Bridge |

FH |

80.9 |

New Build |

|

|

|

London - Walton |

FH |

20.7 |

Conversion |

|

|

|

Paris - East 1 (Noisy-le-Grand) |

FH |

60.0 |

Conversion |

|

|

|

Paris - West 3 (Mantes Buchelay) |

FH |

58.0 |

New Build |

|

|

|

Paris - North West 1 (Taverny) |

FH |

54.0 |

Conversion |

|

|

|

Paris - La Défense |

FH |

38.9 |

New Build |

|

|

|

Pamplona |

FH |

64.5 |

Conversion |

|

|

|

Madrid - North East (Barajas) |

FH |

57.2 |

Conversion |

|

|

|

Madrid - South West (Carbanchel) |

FH |

45.4 |

Conversion |

|

|

|

Barcelona - Central 2 (Manso) |

LH |

19.8 |

Conversion |

|

|

|

Randstad - Amsterdam |

FH |

65.4 |

New Build |

|

|

|

Randstad - Utrecht |

FH |

50.0 |

Conversion |

|

|

|

Brussels - Zaventem |

FH |

47.4 |

New Build |

|

|

|

Extensions |

|

|

|

|

|

|

Paris - Pyrénées |

LH |

15.4 |

Extension |

|

|

|

Total openings and extensions in 2025 |

|

677.6 |

|

|

|

|

|

|

|

|

|

Our portfolio at the end of FY 2025 is shown in the table below.

|

Store Portfolio |

Number of stores |

MLA (m sq ft) |

% of Group MLA |

FY 2025 % increase in MLA |

|

London & South East England |

78 |

3.18 |

34% |

+4.2% |

|

Rest of UK |

61 |

2.80 |

30% |

|

|

UK Total |

139 |

5.98 |

64% |

+1.7% |

|

Paris |

34 |

1.66 |

18% |

+17% |

|

Expansion Markets |

38 |

1.64 |

18% |

+27% |

|

Total Group |

211 |

9.28 |

100% |

+8.0% |

|

Joint ventures (Italy & Germany) |

19 |

1.15 |

|

+251.3% |

|

Total group managed MLA (including joint ventures) |

230 |

10.43 |

|

+17.0% |

The valuation of our portfolio of investment properties increased £193.1 million in the year primarily driven by the completion of developments in the year, with the valuation at year end of £3.25 billion. We have financed our development programme through a combination of retained earnings and debt and as a result, net debt increased in the year by £159.1 million to £1,058.6 million, with the balance sheet remaining strong and comfortably within our covenants. This disciplined approach to capital allocation has allowed us to add 2.5 million sq ft to the portfolio over the last ten years without the need for any equity increases.

Development pipeline

There is a further 1.1 million sq ft of space (20 stores) in the current development pipeline to be delivered from FY 2026 with total associated capex of £219 million (of which £116 million was still to go at the end of FY 2025). Within this are three new sites that have been identified and secured since the FY 2025 half year results. The pipeline continues to reflect our focus on key metropolitan areas across our markets and includes eleven stores in London and SE England, four stores in Paris and one in each of Barcelona and Madrid. In FY 2026 to date, one store has been opened in Paris and one in London.

Our pipeline prioritises acquiring sites subject to planning, ensuring that capital for land or building acquisition is deployed only when construction is imminent, which significantly shortens the investment cycle and accelerates payback timing. The pipeline reflects an average facility size of 55,000 sq ft and avoids the development of oversized stores, which we believe offer materially lower returns on capital due to lower rental rates (a stabilised rate c. 20% less than our portfolio average), higher construction costs and longer permitting timelines.

On completion of the existing pipeline the total investment since the start of FY 2023 will be £441 million funding 2.5 million sq ft of space and 50 new stores. In addition, we have invested a total of £44 million in joint ventures in Germany and Italy, which are generating management fees and provide us with the opportunity to access at scale two large European markets.

Our development hurdle rate is 10% yield-on-cost (defined as incremental EBITDA/initial investment) upon stabilisation, which is usually five to six years from opening with earnings break-even (after the cost of financing) achieved between 18 and 24 months. Consistent with our investment model, new stores typically follow a clear 'J-curve' trajectory: while year 1 reflects the impact of a fixed cost base whilst sales ramp up, stores typically achieve operational break-even towards the end of the first year, followed by rapid yield acceleration in years 2 to 5 as occupancy and rate move towards stabilisation.

Recent vintages of new stores, including those opened in FY 2022 and FY 2023, are tracking in line with these established historical benchmarks towards our hurdle rate, underpinning our confidence in the future revenue contribution from our development pipeline. We expect our non-LFL stores (stores <two years old / opened since FY 2024) together with the existing pipeline to deliver a total of £35-£40 million of incremental EBITDA to the Group upon stabilisation.

Beyond the existing pipeline, our strong cash flow and disciplined approach to capital allocation means that we have financial capacity for further moderate space expansion. We will take advantage of selective opportunities accordingly, including investment in joint ventures, while being mindful of the short term impact on earnings from new store costs and finance expenses.

New stores and extensions opening programme

We have a total pipeline of 20 developments opening in FY 2026 and beyond, which is expected to add a total of 1.1 million sq ft, representing 11.8% of the portfolio MLA as at 31 October 2025. All sites in our development pipeline are new freehold sites. This includes the two new stores below which had already opened in the first two months of the new financial year.

|

|

|

|

|

|

|

|

|

FY 2026 opened since year end |

FH/LH |

MLA |

Development type |

|

|

|

London - Wembley |

FH |

55.3 |

New Build |

|

|

|

Paris - Colombes |

FH |

65.2 |

New Build |

|

|

|

Total opened in 2026 |

|

120.5 |

|

|

|

|

|

|

|

|

|

In addition to the 120,500 sq ft of MLA added in November and December, there is a pipeline of six stores with 296,100 sq ft of MLA projected to be opening during the remainder of FY 2026. This brings a total additional MLA projected to be delivered in FY 2026 to 416,600 sq ft. Of the eight stores to open in FY 2026, five will be in the UK, two in Paris and one in Spain.

|

|

|

|

|

|

|

|

|

|

Remaining FY 2026 openings |

FH/LH |

MLA |

Development type |

Status* |

|

|

|

London - Woodford |

FH |

68.7 |

New Build |

C, UC |

|

|

|

London - Watford |

FH |

57.5 |

New Build |

C, UC |

|

|

|

Hemel Hempstead |

FH |

51.3 |

New Build |

C, UC |

|

|

|

Shoreham |

FH |

47.1 |

New Build |

C, UC |

|

|

|

Paris - West 4 (Orgeval) |

FH |

53.0 |

New Build |

C, UC |

|

|

|

Madrid - Perseo |

FH |

18.5 |

Conversion |

C, UC |

|

|

|

Total remaining openings in 2026 |

|

296.1 |

|

|

|

|

|

|

|

|

|

|

|

* C = completed, CE = contracts exchanged, STP = subject to planning, PG = planning granted, UC = under construction

Our ongoing pipeline of new store developments beyond FY 2026 comprises twelve projects identified which will deliver an additional 678,300 sq ft of new space. Of the twelve developments nine will be in the UK, two in Paris and one in Spain.

|

|

|

|

|

|

|

|

|

|

FY 2027 and beyond openings |

FH/LH |

MLA |

Development type |

Status* |

|

|

|

London - Old Kent Road |

FH |

75.6 |

New Build |

C, STP |

|

|

|

London - Belvedere |

FH |

53.6 |

New Build |

C, STP |

|

|

|

London - Bermondsey |

FH |

50.0 |

New Build |

C, STP |

|

|

|

London - Kingston |

FH |

55.0 |

New Build |

C, PG |

|

|

|

Nottingham - Abbeyfield Road |

FH |

55.0 |

Conversion |

CE, PG |

|

|

|

Woking |

FH |

55.0 |

New Build |

CE, STP |

|

|

|

Norwich |

FH |

52.7 |

New Build |

C, STP |

|

|

|

Swindon |

FH |

52.0 |

New Build |

CE, PG |

|

|

|

Welwyn Garden City |

FH |

51.0 |

New Build |

CE, PG |

|

|

|

Paris - Bry-sur-Marne |

FH |

58.1 |

New Build |

C, UC |

|

|

|

Paris - West 1 (Conflans) |

FH |

56.0 |

New Build |

C, PG |

|

|

|

Barcelona - Hospitalet |

FH |

64.3 |

New Build |

CE, STP |

|

|

|

Total FY 2027 and beyond openings |

|

678.3 |

|

|

|

|

|

|

|

|

|

|

|

CHIEF FINANCIAL OFFICER'S REVIEW

Underlying income statement

The table below sets out the Group's underlying results of operations for the twelve months ended 31 October 2025 ("FY 2025") and the twelve months ended 31 October 2024 ("FY 2024"). To calculate the underlying performance metrics, adjustments are made for the impact of exceptional items, share-based payments, corporate transaction costs, change in fair value of derivatives, gain or loss on investment properties and the associate tax impacts, as well as exceptional tax items and deferred tax. Although not superseding IFRS, management considers this presentation of earnings to be representative of the underlying performance of the business, as it removes the income statement impact of items not fully controllable by management, such as the revaluation of derivatives and investment properties, and the impact of exceptional credits, costs and finance charges.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2025 |

2024 |

Mvmt |

|

|

|

|

|

|

|

|

£'m |

£'m |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue |

|

|

|

|

234.3 |

223.4 |

4.9% |

|

|

|

Underlying cost of sales |

|

|

|

(78.4) |

(72.2) |

8.6% |

|

|

|

|

Underlying store EBITDAR |

|

|

155.9 |

151.2 |

3.1% |

|

||

|

|

Underlying administrative costs |

|

|

|

(18.9) |

(15.8) |

19.6% |

|

|

|

|

Underlying EBITDAR |

|

|

|

137.0 |

135.4 |

1.2% |

|

|

|

|

Leasehold costs |

|

|

|

(16.1) |

(15.5) |

3.9% |

|

|

|

|

Underlying EBITDA after leasehold costs |

|

120.9 |

119.9 |

0.8% |

|

|||

|

|

Depreciation |

|

|

|

(1.5) |

(1.5) |

0.0% |

|

|

|

|

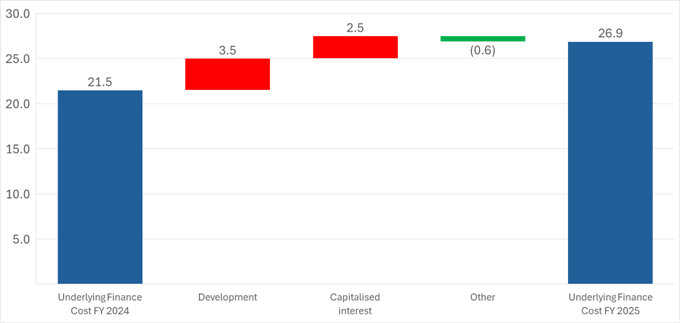

Net underlying finance charges |

|

|

|

(26.4) |

(21.4) |

23.4% |

|

|

|

|

Net profit from joint ventures and associates |

|

(0.1) |

(0.0) |

100.0% |

|

|||

|

|

Underlying profit before tax |

|

|

92.9 |

97.0 |

(4.2%) |

|

||

|

|

Current tax |

|

|

|

|

(4.4) |

(4.3) |

2.3% |

|

|

|

Adjusted EPRA earnings |

|

|

88.5 |

92.7 |

(4.5%) |

|

||

|

|

|

|

|

|

|

|

|

||

|

|

Diluted shares (for ADE EPS) (m) |

|

|

219.7 |

219.3 |

0.2% |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted diluted EPRA EPS (p) |

|

40.3 |

42.3 |

(4.7%) |

|

|||

|

|

|

|

|

|

|

|

|

|

|

The table below reconciles statutory profit before tax in the income statement to underlying profit before tax in the table above.

|

|

|

|

|

|

|

|

|

|

|

2025 |

2024 |

|

|

|

|

|

£'m |

£'m |

|

|

|

Statutory profit before tax |

127.1 |

398.6 |

|

|

|

|

Adjusted for: |

|

|

|

|

|

|

|

- gain on investment properties and investment properties under construction |

(33.4) |

(301.9) |

|

|

|

|

- share of associates non-underlying income |

(2.6) |

- |

|

|

|

|

- share-based payments |

1.1 |

0.3 |

|

|

|

|

- exceptional items |

0.7 |

- |

|

|

|

Underlying profit before tax |

92.9 |

97.0 |

|

|

|

|

|

|

|

|

|

Revenue and underlying profit by region

|

|

|

|

||||||

|

|

2025 |

2024 |

||||||

|

|

UK |

Paris |

Exp Mkt |

Total |

UK |

Paris |

Exp Mkt |

Total |

|

Total Revenue local currency 'm |

167.5 |

52.6 |

26.2 |

- |

162.2 |

51.3 |

20.6 |

- |

|

Average exchange rate |

- |

1.173 |

1.173 |

- |

- |

1.173 |

1.173 |

- |

|

Total revenue (CER) £'m |

167.5 |

44.8 |

22.3 |

234.6 |

162.2 |

43.7 |

17.5 |

223.4 |

|

Underlying EBITDAR (CER) £'m |

96.9 |

29.9 |

10.3 |

137.1 |

99.3 |

28.7 |

7.4 |

135.4 |

|

Foreign exchange |

- |

(0.1) |

- |

(0.1) |

- |

- |

- |

- |

|

Underlying EBITDAR £'m |

96.9 |

29.8 |

10.3 |

137.0 |

99.3 |

28.7 |

7.4 |

135.4 |

Analysis of cost base

Cost of sales

|

|

|

|

|

|

|

|

2025 |

2024 |

Change |

|

|

|

£'m |

£'m |

£'m |

% |

|

Volume related costs including bad debt |

5.7 |

5.7 |

- |

- |

|

Store employees |

24.8 |

23.8 |

1.0 |

4.2% |

|

Marketing |

9.6 |

9.1 |

0.5 |

5.5% |

|

Business rates |

18.3 |

16.9 |

1.4 |

8.3% |

|

Facilities and premises insurance |

15.7 |

15.5 |

0.2 |

1.3% |

|

Underlying LFL cost of sales (CER) |

74.1 |

71.0 |

3.1 |

4.4% |

|

Non-LFL and developments |

4.5 |

1.2 |

3.3 |

275.0% |

|

Foreign exchange |

(0.2) |

- |

(0.2) |

- |

|

Underlying cost of sales |

78.4 |

72.2 |

6.2 |

8.6% |

|

Depreciation |

1.5 |

1.5 |

- |

- |

|

Total cost of sales |

79.9 |

73.7 |

6.2 |

8.4% |

|

|

|

|

|

|

Cost of sales in the financial year continued to be impacted by elevated levels of inflationary cost pressures, particularly in the UK. This led to a 4.4% increase year on year in the underlying LFL cost of sales. The key drivers of this were:

· Volume related costs including bad debt: flat year on year with a normalisation of bad debt provisions in Paris;

· Store employees: a 4.2% increase year on year, driven by higher payroll costs in the UK from National Living Wage increases and rising employer National Insurance costs. This increase was partially offset by savings in the UK where we have integrated call centre activities into stores and lower costs in Paris as a result of dynamic staff management and lower variable pay;

· Marketing: remained stable at 4.1% of sales (FY 2024: 4.1%) reflecting our centrally controlled securing of customer enquiries in a cost-effective manner;

· Business rates: increased 8.3% because of higher charges in the UK from reduced taper relief and inflationary uplifts; and

· Facilities and insurance: increased by only 1.3% in the year due to risk/reward sharing with insurers of the benefit of incident prevention work largely offsetting inflationary increases in energy costs in the UK.

New stores classified as non-LFL incurred costs of £4.5 million in the year resulting in an overall increase in cost of sales of 8.4% to £79.9 million (FY 2024: £73.7 million).

Administrative Expenses

|

|

|

|

|

|

|

|

|

|

|

2025 |

2024 |

Change |

|

|

|

|

|

£'m |

£'m |

£'m |

% |

|

|

|

Underlying administrative expenses (CER) |

18.9 |

15.8 |

3.1 |

19.6% |

|

|

|

Exceptional costs |

0.7 |

- |

0.7 |

- |

|

|

|

Share-based payments |

1.1 |

0.3 |

0.8 |

266.7% |

|

|

|

Foreign exchange |

- |

- |

- |

- |

|

|

|

Total administrative expenses |

20.7 |

16.1 |

4.6 |

28.6% |

|

|

|

|

|

|

|

|

|

Administrative expenses comprise the Head Office costs of the Group. These costs include employee costs, listed company costs, professional fees and IT costs. The key centralised operations of the Group include marketing, price-setting and IT carried out by specialist teams for all markets.

In FY 2025 underlying administrative costs grew £3.1 million, up 19.6%. The key drivers were an increase in spend to enhance our capabilities in AI and data management and finance, together with a return to a more normalised level of variable pay following FY 2024 when performance targets were not met.

Underlying administrative costs exclude exceptional items of £0.7 million comprising investment in a new SAAS-based finance computer system. The implementation of this system is expected to be completed in FY 2026 with further cost in that year. These costs have been excluded from underlying performance due to their scale and irregular nature.

Investment Properties

Cushman & Wakefield Debenham Tie Leung Limited LLP ("C&W") valued the Group's property portfolio as at 31 October 2025. The total value of the Group's investment property portfolio of open stores ("IP") was £3,245.9 million, an increase of £193.1 million over the financial year (31 October 2024: £3,052.8 million).

In addition, investment property under construction ("IPUC") had a value at the balance sheet date of £122.8 million and comprises ongoing developments.

52 of our stores are leaseholds with the lease liabilities included separately on the balance sheet with a corresponding asset included in investment property.

|

|

|

|

|

|

|

|

UK |

Paris |

Exp Mkt |

Total IP |

|

|

£'m |

£'m |

£'m |

£'m |

|

Value of IP as at 1 November 2024 |

2,144.5 |

627.2 |

281.1 |

3,052.8 |

|

Developments and acquisitions* |

49.7 |

36.0 |

44.0 |

129.7 |

|

Disposals |

- |

(5.2) |

(0.8) |

(6.0) |

|

Revaluation |

(8.2) |

4.9 |

26.6 |

23.3 |

|

Foreign exchange |

- |

30.5 |

15.6 |

46.1 |

|

Value of IP as at 31 October 2025 |

2,186.0 |

693.4 |

366.5 |

3,245.9 |

|

|

|

|

|

|

|

IP under construction |

85.1 |

32.8 |

4.9 |

122.8 |

|

IP and IPUC, before lease liabilities |

2,271.1 |

726.2 |

371.4 |

3,368.7 |

|

|

|

|

|

|

|

IP lease liabilities |

79.4 |

21.9 |

10.1 |

111.4 |

|

Total as at 31 October 2025 |

2,350.5 |

748.1 |

381.5 |

3,480.1 |

|

|

|

|

|

|

* includes transfers from Investment Property Under Construction

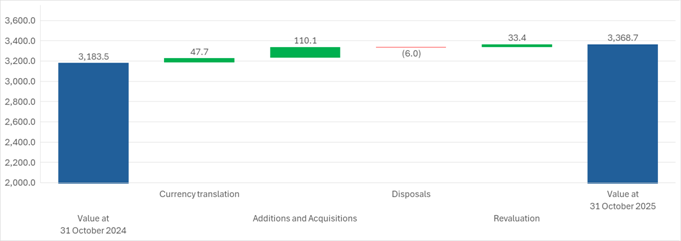

Property valuation: IP and IPUC, before lease liabilities £'m

The Group's property portfolio valuation, including investment properties under construction, increased by £185.2 million, including a gain on revaluation of £33.4 million, £110.1 million relating to additions and store refurbishments and a favourable £47.7 million increase in the value of our investment properties due to foreign currency movements.

The revaluation gain was driven by increases from both new and maturing stores reflecting the value created through their development and subsequent stabilisation. The LFL portfolio valuation was stable year on year and there was a small movement in yields, which increased 13bps to 5.32% (FY 2024: 5.19%) and discount rates for future cash flows, which increased 36bps to 9.02% in the year (FY 2024: 8.66%).

Disposals in the year totalled £6.0 million from the sale of excess land and buildings.

In the year, the freehold of an existing store was acquired for £3.5 million (FY 2024: two stores for £13.5 million).

The exchange rate at 31 October 2025 was €1.1375 : £1 compared to €1.1905 : £1 at 31 October 2024.

Gain on revaluation of properties

A full, independent external valuation of the store portfolio is undertaken by the Group on an annual basis for year-end reporting.

As a result of this exercise, the net gain on investment properties during the year was as follows.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2025 |

2024 |

|

|

|

|

|

|

|

|

£'m |

£'m |

|

|

|

|

|

|

|

|

|

|

|

|

|

Revaluation of investment properties |

|

23.3 |

310.7 |

|

|||

|

|

Revaluation of investment properties under construction |

10.1 |

(8.8) |

|

||||

|

|

Fair value re-measurement of lease liabilities |

|

(10.3) |

(9.7) |

|

|||

|

|

Gain on revaluation of investment properties and investment properties under construction |

23.1 |

292.2 |

|

||||

|

|

|

|

|

|

|

|

|

|

The revaluation of investment properties reflects the increased value of the Group's store portfolio primarily as the new stores begin to trade and deliver in line with our plans. The fair value re-measurement of lease liabilities reflects the reduction in investment property lease liabilities as rent payments are made.

Joint Ventures and Associates

|

|

|

|

|

|

|

|

|

|

Year ended 31 October 2025 |

Italy |

Germany |

Paris |

Total |

|

|

|

|

£'m |

£'m |

£'m |

£'m |

|

|

|

Underlying share of joint venture and associate profit / (loss) |

0.5 |

(0.6) |

- |

(0.1) |

|

|

|

Fair value re-measurement of investment property lease liabilities |

- |

0.2 |

- |

0.2 |

|

|

|

Gain on revaluation of investment property |

2.4 |

- |

- |

2.4 |

|

|

|

Share of profit / (loss) from joint ventures and associates |

2.9 |

(0.4) |

- |

2.5 |

|

|

|

|

|

|

|

|

|

The underlying share of joint venture and associate profit reflects the income for the first nine months of trading (following its acquisition in FY 2025) from our Italian joint venture and the share of loss from our German associate. The result for the German associate includes the impact of one-off professional fees related to the establishment of the business and normalisation of leases. In addition, the result for Italy includes a £2.4 million gain (at share) on the revaluation of the investment property of the joint venture, taking the total share of profit from joint ventures and associates to £2.5 million (FY 2024: £nil).

Operating profit

Reported operating profit was £159.3 million for FY 2025, down £266.5 million, primarily due to a decrease in the investment property revaluation gain.

A bridge from Underlying EBITDAR to operating profit can be found below:

|

|

|

|

|

|

|

|

|

|

|

2025 |

2024 |

|

|

|

|

|

£'m |

£'m |

|

|

|

Underlying EBITDAR |

|

137.0 |

135.4 |

|

|

|

|

|

|

|

|

|

|

Adjusted for |

|

|

|

|

|

|

Gain on revaluation of investment properties |

|