ABC Project Scoping Study

Summary by AI BETAClose X

13 May 2026

Scoping Study Confirms Attractive Economics and Growth Potential at ABC Project, Côte d'Ivoire

Resolute Mining Limited ("Resolute" or "the Company") (ASX/LSE: RSG) is pleased to announce the results of a Scoping Study ("Study") for the ABC Project ("ABC" or the "Project") in Côte d'Ivoire based on the existing 2.16 Moz gold Mineral Resource Estimate ("MRE") published in 2021.

The Study confirms the ABC Project's strong economic potential and its pathway to become Resolute's second operating gold mine in Côte d'Ivoire, supporting the Company's strategy to build a diversified, multi-asset gold platform. It outlines a robust, long-life operation with attractive economics and meaningful potential upside from further resource growth and exploration success.

Resolute is accelerating step-out drilling at the Kona Central and Kona South deposits to unlock further resource growth and build on the Project's strong progress. To date, the Company has drilled over 25,000 m, with results expected to support an updated MRE in H2 2026.

Scoping Study Highlights

Scoping Study Highlights

Production - long-life, open pit gold operation

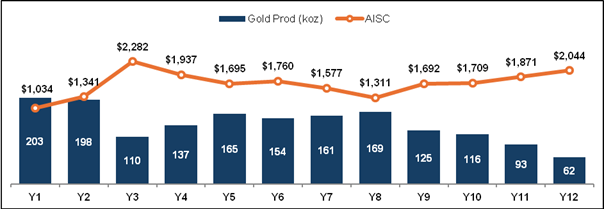

• Strong production profile averaging approximately 141 koz per annum over a 12-year mine life, delivering total gold production of 1.7 Moz at a competitive life-of-mine ("LoM") all-in sustaining cost ("AISC") of US$1,614/oz, supporting robust operating margins

• Large-scale open pit mining operation underpinned by total mill feed of 82.8 Mt at 0.76g/t Au containing 2.0 Moz of gold, with a low average life-of-mine strip ratio of 1.82

• Low-risk development pathway utilising a conventional 7.0 Mtpa carbon-in-leach ("CIL") processing plant with gold recoveries of 84% and further recovery optimisation potential during development

• Strong early cash flow generation with average annual gold production of 163 koz over the first five years at an attractive AISC of US$1,565/oz using a gold price assumption of US$3,500/oz,

Financial (post-tax, 100% basis) - attractive metrics and short payback period

• Net present value at 5% discount rate ("NPV5%") of US$1.2bn, Internal rate of return ("IRR") of 39%, 1.4-year payback at a gold price assumption of US$3,500/oz

• At US$4,750/oz gold price the NPV5% increases to US$2.3bn with an IRR of 63% and payback period of under 1 year

• Competitive capital cost estimate of US$648M

• Average annual free cash flow and EBITDA of US$262M and US$323M respectively in first five years of production at US$3,500/oz gold price

Potential upside via MRE growth

• Based on drilling activities in 2026 mineralisation remains open at depth and along strike; drilling at Kona South extended mineralisation to the North and South, highlighting the potential for resource expansion

• Updated Kona Central and Kona South MRE expected in H2 2026

Next Steps

• Accelerate drilling efforts with a focus on infilling resource as well as resource expansion

• Optimize metallurgical testwork to increase recovery rates of the deposits

• Initiate ESIA and other required technical study work

• Site investigations and permitting to target completion of a Definitive Feasibility Study ("DFS") in 2027

• Based on potential size of the resource further work will be done to optimize the size of the processing plant in order to increase the ounce profile above 200 koz per annum for at least 10 years of mine life

Note: Unless otherwise stated, all dollar figures are United States dollars ($).

The production target and forecast financial information in this announcement are conceptual in nature and are based entirely on Inferred Mineral Resources and there is no certainty that the outcomes will be realised.

The Scoping Study was undertaken by MineScope Services along with input from Orelogy, Knight Piésold and ECG Engineering.

The full Scoping Study can be found on the Resolute website on the Reports page.

Chris Eger, Managing Director and CEO commented:

"Resolute is very pleased to announce the results of the scoping study for ABC which demonstrates the significant economic potential of the ABC Project. Building on the strong results from the ongoing step-out drilling at the Kona South and Central deposit, we are confident the Project has potential to grow and become more commercially attractive.

Based on the study, the ABC Project will produce approximately 141 koz per annum over 12 years at a competitive average AISC of US$1,614/oz. At a conservative gold price of $3,500/oz this delivers a post-tax NPV5% of US$1.2bn and IRR of 39% and a payback of under 1.5 years.

While the initial results demonstrate the potential for a fourth mine for Resolute, we will continue to progress the Project with an updated MRE planned for H2 2026 as we are highly confident the resource will continue to expand and the project economics will only get more attractive with potential to increase the scale of the mine.

The scoping study now provides Resolute with the required technical platform to commence the DFS. Progress on exploration, metallurgical testwork, site investigations and permitting has been prioritised with the target of completing the required workstreams to finalise a DFS by the end of 2027."

Cautionary Statement

The Scoping Study referred to in this announcement has been undertaken for the purpose of ascertaining whether a business case can be made to proceed to feasibility studies on the technical and financial viability of a mining and processing operation at the Project and provide a preliminary evaluation of the development based on the Mineral Resource Estimate (report date: 31 July 2021). This Mineral Resource Estimate was reported as JORC-compliant in the Company's Ore Reserves and Mineral Resource Statement released on the ASX on 05 March 2026.

The Study is a preliminary technical and economic study of the potential viability of the Project. It is based on low level technical and economic assessments that are not sufficient to support the estimation of ore reserves under the definition of the JORC 2012 guidelines. The use of the word "ore" in the Study should not be interpreted as referring to an Ore Reserve but indicates material that has been selected as suitable for processing feed. Further exploration and evaluation work and appropriate studies are required before the Company will be in a position to estimate any Ore Reserves or to provide any assurance of an economic development case. The accuracy of the capital and operating cost estimates is ±30%.

The information in this announcement that relates to mining, processing, metallurgical recovery, infrastructure, capital and operating cost estimates is based on data and assumptions developed for the purposes of a Scoping Study and does not constitute Ore Reserves or JORC‑reportable estimates.

The Mineral Resources underpinning the production targets in this announcement have been prepared by a competent person in accordance with the requirements of the JORC Code. Inferred Resources comprise 100% of the production schedule over the modelled life of mine. The Company has concluded that it has reasonable grounds for disclosing a production target which includes an amount of Inferred Mineral Resources. However, there is a low level of geological confidence associated with Inferred Mineral Resources and there is no certainty that further exploration work will result in the determination of Measured and/or Indicated Mineral Resources or that the production target itself will be realised.

The Study is based on the material assumptions outlined below. While the Company considers all of the material assumptions to be based on reasonable grounds, there is no certainty that they will prove to be correct or that the range of outcomes indicated by the Scoping Study will be achieved. To achieve the range of outcomes indicated in the Study, funding of in the order of US$648 million will likely be required. Investors should note that there is no certainty that the Company will be able to raise that amount of funding when needed. It is also possible that such funding may only be available on terms that may be dilutive to or otherwise affect the value of the Company's existing shares. It is also possible that the Company could pursue other 'value realisation' strategies such as a sale, partial sale or joint venture of the Project. If it does, this could materially reduce the Company's proportionate ownership of the project. Given the uncertainties involved, investors should not make any investment decisions based solely on the results of the Scoping Study.

ABC Project Overview

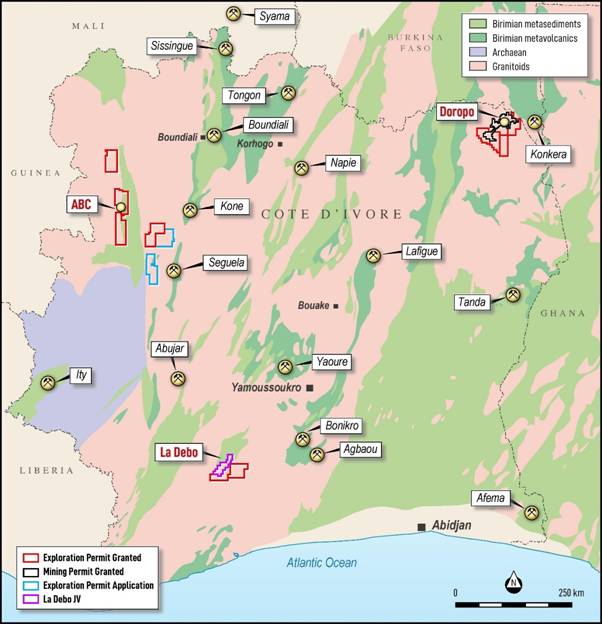

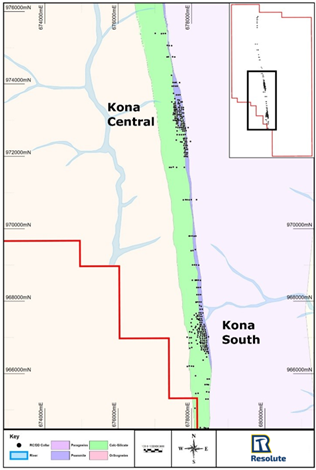

The ABC Project is located in northwest Côte d'Ivoire approximately 550km northwest of Abidjan and 460km west of the Doropo project. Resolute acquired the ABC Project from AngloGold Ashanti in 2025.

Figure 1: Resolute's Projects in Côte d'Ivoire

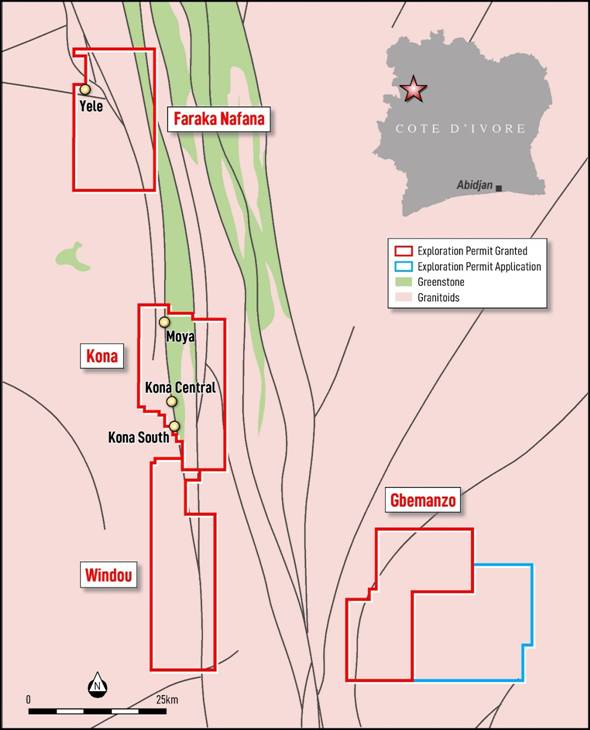

The ABC Project currently consists of four exploration permits - Faraka-Nafana, Kona, Windou and Gbemanzo - all of which are 100% owned by Resolute.

The Scoping Study is based on the existing inferred MRE prepared by Centamin Plc (July 2021)which is located on the Kona exploration permit. The MRE comprises two deposits, Kona Central and Kona South, totalling 72 Mt at 0.93 g/t for 2.16 Moz Au (at a 0.5g/t cut-off).

Figure 2: ABC Project permits

The inferred resource converts to an in situ production target of 82.8 Mt at 0.76 g/t Au containing 2.01 Moz.

The Project will encompass an open pit mine, CIL processing facility with a capacity of 7.0 Mtpa, water supply from known water supply schemes in the area, power from the Ivorian grid, tailings storage facility ("TSF") and related infrastructure. Gold production will average 163 koz per annum over the first five years of operations and 141 koz per annum over the 12-year life of mine.

The Study demonstrates that the Project has the capacity to deliver robust returns at a base case price assumption of US$3,500/oz. Project returns significantly improve at a price closer to spot of US$4,750/oz with the NPV5% increasing to US$2.3bn and IRR to 63%. Key project operational and financial highlights are outlined below:

|

Gold Price: US$3,500/oz |

Units |

Value |

|

Mine Life |

Years |

12 |

|

Total gold production |

koz |

1,693 |

|

Upfront capital cost |

US$M |

648 |

|

Life of Mine average: |

|

|

|

Gold production |

koz |

141 |

|

Revenue |

US$M |

494 |

|

EBITDA |

US$M |

276 |

|

Free Cash Flow (post-tax) |

US$M |

210 |

|

Cash cost |

US$/oz |

1,524 |

|

AISC |

US$/oz |

1,614 |

|

Project years 1 to 5: |

|

|

|

Gold production |

koz |

163 |

|

Revenue |

US$M |

569 |

|

EBITDA |

US$M |

323 |

|

Free Cash Flow (post-tax) |

US$M |

262 |

|

Cash cost |

US$/oz |

1,493 |

|

AISC |

US$/oz |

1,565 |

|

Pre-Tax Economics |

|

|

|

NPV 5% |

US$M |

1,624 |

|

IRR |

% |

46% |

|

Post-Tax Economics |

|

|

|

NPV 5% |

US$M |

1,178 |

|

IRR |

% |

39% |

|

Payback period (from first production) |

Years |

1.4 |

Table 1: Economic Summary

Figure 3: Gold Production Profile (koz) and AISC (US$/oz)

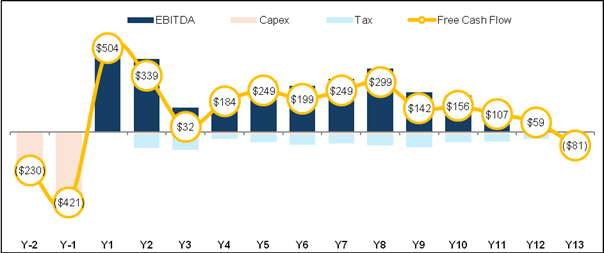

In the first five years average annual gold production is 163 koz at an AISC of US$1,565/oz. At the base case gold assumption of US$3,500/oz and on a 100% basis this generates average annual free cash flow of US$262M and a payback period of 1.4 years.

Figure 4: Free Cash Flow Profile (US$M)

The post-tax NPV sensitivity comparing varying discount rate percentages and gold price is presented in Table 2. The base case result for the Project is highlighted in bold.

|

|

3,000 |

3,500 |

4,000 |

4,500 |

5,000 |

|

5% |

749 |

1,178 |

1,607 |

2,036 |

2,465 |

|

7% |

619 |

999 |

1,380 |

1,761 |

2,142 |

|

10% |

460 |

782 |

1,103 |

1,425 |

1,747 |

Table 2: Sensitivity of post-tax NPV5% (US$M) to Discount Rate (%) and Gold Price (US$/oz)

Geology and Mineral Resources

The ABC Kona project is situated along the main Archean-Birimian Cratonic suture zone in western Côte d'Ivoire, specifically associated with the Sassandra Fault Zone.

The principal mineralised feature identified through mapping and sampling is the Lolosso structure, a north-south striking mineralised zone interpreted as a western splay off the major transcurrent Sassandra Fault. The geological setting includes a narrow keel of later Birimian volcano-sediments entrapped within earlier Archean thrusted granite and gneissic sheets, providing a complex structural and lithological host for mineralisation.

Figure 5: Kona Central lies 3.7 km to the north along strike from Kona South

At Kona South, gold is predominantly hosted in psammitic units (north-south striking) dipping approximately 70° west. This unit is sandwiched between a calc-silicate hanging wall to the west and a paragneiss footwall to the east. An additional mafic volcanic unit lies west of the calc-silicate layer, completing the local stratigraphy.

The style of mineralisation is structurally controlled and shows a strong spatial association with arsenopyrite. Arsenopyrite occurs as disseminations and aggregates aligned with the foliation of the psammitic host. Strong silicification is evident within mineralised zones, though quartz veining is rare and does not appear to play a significant role in gold control.

The MRE used in the study is reported in accordance with the JORC Code (2012). Table 3 presents the MRE at a 0.5 g/t cut-off. The figures in table 3 rounded to reflect the precision of the estimates and include apparent rounding errors.

|

Deposit |

Material Type |

Tonnes (Mt) |

Grade (g/t Au) |

Contained Gold (Moz) |

|

Kona South |

Transported |

0.1 |

1.20 |

0.00 |

|

Oxidised |

1 |

1.02 |

0.03 |

|

|

Transitional |

1 |

1.01 |

0.03 |

|

|

Fresh |

29 |

1.05 |

0.99 |

|

|

Kona Central |

Transported |

0.1 |

0.85 |

0.00 |

|

Oxidised |

0.4 |

0.86 |

0.01 |

|

|

Transitional |

0.9 |

0.81 |

0.02 |

|

|

Fresh |

40 |

0.84 |

1.08 |

|

|

Total |

Inferred |

72 |

0.93 |

2.16 |

Table 3: Summary of July 2021 MRE for Kona Central and Kona South deposits (all Resource are classified as Inferred)

Mining

Orelogy Consulting Pty Ltd was engaged to complete the mining aspects of the Study. The pit optimisations, production scheduling and associated costing are based on the MRE outlined above.

The preferred mining method at the Project is to utilise a conventional open pit truck/shovel approach as this is a proven mining method for near surface gold deposits, and the method is common practice in Côte d'Ivoire.

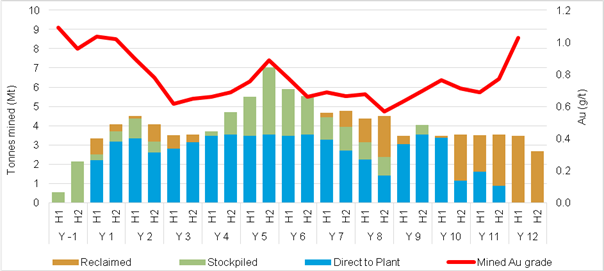

The Study envisages two open pits, Kona Central and Kona South, with mining commencing at the higher-grade Kona South deposit. The pits are relatively shallow at a final depth of 240 m and 210 m for Kona South and Central respectively.

The schedule uses interim stockpiles to manage run-of-mine material supply and improve plant feed grade. At a plant throughput rate of 7 Mtpa, the schedule is constrained by the ore that can be delivered within the overall mining rate and bench turnover limits. The lower grade in Year 3 is due to this constraint. By nature of the Study, the mine scheduling results are preliminary, and therefore, further optimisation is required in future studies to optimise the mine schedule and plant feed.

Figure 6: Mining schedule and mined gold grades

Processing

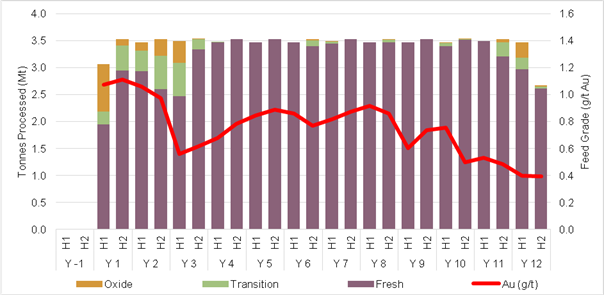

Orelogy completed the processing schedule with MineScope advising on plant design and flowsheet.

The process plant is designed as a conventional gold processing facility capable of treating 7 Mtpa of run-of-mine material. The selected flowsheet follows a typical gold processing flowsheet comprising of crushing, SAG and ball milling ("SABC") comminution circuit, gravity recovery, and CIL. This flowsheet represents a proven and widely applied approach for gold ore types.

The design incorporates a primary gyratory crusher and a SABC comminution circuit, reflecting the relatively competent material (mill feed consists of 93% fresh material) and the need for operational flexibility. The inclusion of a pebble crushing circuit is to mitigate SAG mill critical size buildup and maintain throughput.

Figure 7: Processing schedule and Au grades

Metallurgy

Metallurgical testwork completed to date is limited to a single historical composite sample (ALS, 2018), supplemented by bulk leach extractable gold testwork on 50 drill core samples. Accordingly, the metallurgical understanding is preliminary and indicative only, and further testwork will be required to support progression to Feasibility Study.

Gold occurs predominantly as native gold, with minor association to sulphide minerals, principally arsenopyrite. Comminution testing indicates the ore is very hard and competent, implying relatively high grinding energy requirements.

Two processing routes were assessed: gravity recovery followed by cyanidation (CIL), and flotation with concentrate regrind and cyanidation. Both flowsheets achieved comparable recoveries of approximately 87-89%, with the gravity plus CIL flowsheet achieving the highest recovery and materially lower reagent consumption. This flowsheet was therefore selected for the Scoping Study.

Capital Costs

A summary of the capital cost estimates is provided in table 4. It is reported with a base date of Q2 2026 and an accuracy of ±30% (Class 5 AusIMM level). The total capital cost of US$648M includes US$115M of contingency due to the preliminary nature of the Study. Totals may not compute due to rounding.

|

Cost Area |

Total |

|

Mining |

43.6 |

|

Process Plant |

139.1 |

|

Reagents & Plant Services |

38.9 |

|

Infrastructure |

131.5 |

|

Construction Indirects |

64.3 |

|

Project Indirects |

38.0 |

|

Owners Costs |

77.3 |

|

Sub-Total |

532.5 |

|

Contingency |

115.2 |

|

Total |

647.6 |

Table 4: Capital Cost Estimate (US$M)

Mining capital costs include all pre-production mining-related costs including site establishment and fleet mobilisation.

The proposed plant and infrastructure location was selected by limiting construction to occur within the current tenement boundary, along with avoiding interaction with nearby communities and protected forests. Consideration was also given to minimise ore haulage, waste rock haulage and cut-and-fill requirements.

Infrastructure capital costs include site earthworks, accommodation, TSF and power supply. ECG Engineering evaluated the HV power supply and connection to the Côte d'Ivoire power grid. A 48 km transmission line from the Laboa Substation to the Project site has been proposed.

Owners costs include approximately US$19M associated with land acquisition and compensation.

Raw water to the process plant will be supplied from the water storage dam ("WSD"), which is replenished from surface water run off collection points and the nearby Boa River.

Sustaining capital consists of TSF lifts as well as typical expenditure required for the consistent operation of the processing plant. From Y2 onward the average annual sustaining capital expenditure is estimated at US$13.5M.

A closure cost of US$76.0M has been estimated based on the Doropo DFS. The closure cost includes a contingency of US$17.5M and US$33.1M of costs associated with the closure of the TSF (provided by Knight Piésold).

Operating Costs

The operating cost estimate for the Scoping Study has been prepared by the contributing parties to an accuracy of ±30%, equivalent to a Class 5 AusIMM level.

Operating cost estimates have been developed based on preliminary engineering, benchmark data and assumptions derived from the Doropo DFS.

|

Deposit |

Unit |

Operating Cost (LoM average)

|

|

Mining |

US$/total tonnes mined |

4.3 |

|

Processing |

US$/t milled |

13.4 |

|

Site G&A* |

US$/t milled |

2.0 |

*Includes social development fund (0.5% of turnover) and Transport and Refining Charges (TCRC)

Table 5: Approximate LoM average operating costs

Q1 2026 Exploration Update

As outlined in the Q1 2026 Activities Report, exploration activity during Q1 focused on drilling programs planned to expand the Mineral Resources at the Kona deposits.

Drilling successfully advanced efforts to extend known mineralisation at both Kona South and Kona Central, along strike to the north and south of the deposits. A total of 64 RC holes for 11,000 m were completed during the March 2026 quarter with drilling at both areas reinforcing the scale and continuity of the mineralised system.

Drilling progressed strongly during Q1, where activity ramped up to five rigs toward period end to accelerate delineation and rapidly expand the mineralised footprint, positioning the project for continued resource growth.

Results from the first 40 holes demonstrate wide intervals of gold mineralisation across the majority of drilling completed in Q1, reinforcing the scale and continuity of the system. Key standout intersections that have been previously reported included:

• KNRC0499 - 73m @ 0.8g/t Au from 2m

• KNRC0500 - 80m @ 0.4g/t Au from 88m

• KNRC0501 - 23m @ 1g/t Au from 6m

• KNRC0506R - 35m @ 0.9 g/t Au and 21m @ 1.2g/t Au

• KNRC0508 - 10m @ 1.9g/t Au from 217m

• KNRC0512 - 31m @ 1g/t Au from 151m

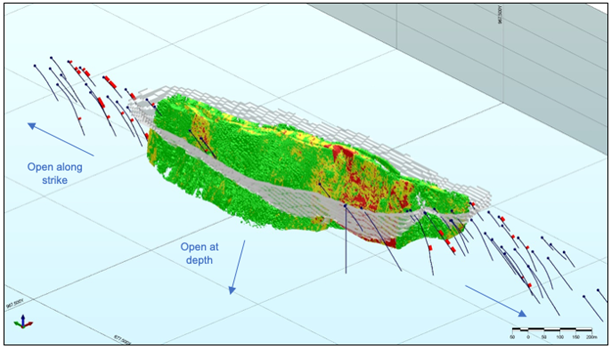

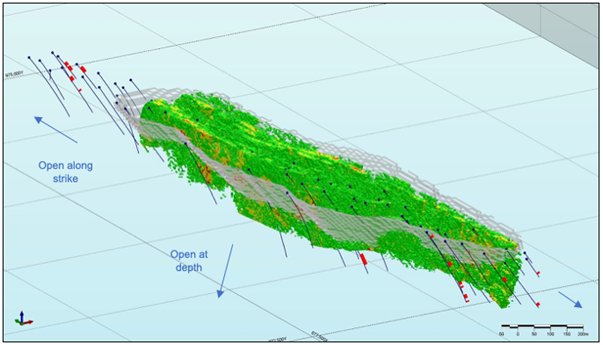

The majority of the results returned were from Kona South which is higher grade than Kona Central. The drill intersections clearly confirm the along strike extensions of the gold mineralisation to the north and south of Kona South, highlighting potential continued resource expansion.

All reported drill intersections are located outside the current Mineral Resource block models, highlighting clear potential for a meaningful increase in the existing resource base and underpinning a compelling growth opportunity.

Figure 8: Existing Kona South MRE with Resolute drill results

Figure 9: Existing Kona Central MRE with Resolute drill results

All previously reported drill intersections (in the Q1 2026 Activities Report) are located outside the current Mineral Resource block models, highlighting clear potential for a meaningful increase in the existing resource base and underpinning a compelling growth opportunity.

At both Kona South and Kona Central the mineralisation remains open at strike and at depth.

Next Steps

Resolute is currently drilling at Kona Central and Kona South to expand the current resources. This will continue throughout Q2 2026. An updated Mineral Resource Estimate is planned to be announced in H2 2026.

The Company plans to advance the Project through a staged work programme focused on progressing the Project toward a DFS in 2027. Key activities are expected to include targeted infill and step‑out drilling to further improve resource confidence and conversion, continued metallurgical and geotechnical testwork, optimisation of mine design and processing flowsheet assumptions, and advancement of environmental, permitting and infrastructure studies.

Contact

|

Resolute Matthias O'Toole-Howes motoolehowes@resolutemining.com +44 203 3017 620 |

Public Relations Jos Simson, Tavistock +44 207 920 3150

Corporate Brokers Jennifer Lee, Berenberg +44 20 3753 3040

Tom Rider, BMO Capital Markets +44 20 7236 1010 |

Authorised by Mr Chris Eger, Managing Director and Chief Executive Officer

Refer to the cautionary statement on page 1 for additional information.

Further detail on the Scoping Study, including all the material assumptions on which the production targets and forecast financial information are based, is included in the Scoping Study on the Company's website.

About Resolute

Resolute is an African-focused gold miner with more than 30 years of experience as an explorer, developer and operator. Throughout its history the Company has produced more than 9 million ounces of gold from ten gold mines. The Company is now entering a growth phase through the development of the Doropo project in Côte d'Ivoire which will supplement the existing production from the Syama mine in Mali and Mako mine in Senegal.

Competent Person Statement

The information in this announcement that relates to the Mineral Resource estimate has been based on information and supporting documents prepared by Mr Bruce Mowat, a Competent Person who is a member of The Australian Institute of Geoscientists. Mr Mowat is a full-time employee Resolute Mining Limited Group and has sufficient experience relevant to the style of mineralisation and type of deposit under consideration and to the activity which has been undertaken to qualify as a Competent Person. Mr Mowat confirms that the Mineral Resource estimate is based on information in the supporting documents and consents to the inclusion in the report of the Mineral Resource estimate and related content based on the information in the form and context in which it appears.

The information in this announcement that relates to mining, processing, metallurgical recovery, infrastructure, capital and operating cost estimates is based on technical studies and assumptions appropriate for a Scoping Study and does not constitute Ore Reserves or JORC‑reportable information.

Cautionary Statement about Forward-Looking Statements

This announcement contains certain "forward-looking statements" including statements regarding our intent, belief or current expectations with respect to Resolute's business and operations, market conditions, results of operations and financial condition, and risk management practices. The words "likely", "expect", "aim", "should", "could", "may", "anticipate", "predict", "believe", "plan", "forecast" and other similar expressions are intended to identify forward-looking statements. Indications of, and guidance on, future earnings, anticipated production, life of mine and financial position and performance are also forward-looking statements. These forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause Resolute's actual results, performance and achievements or industry results to differ materially from any future results, performance or achievements, or industry results, expressed or implied by these forward-looking statements. Relevant factors may include (but are not limited to) changes in commodity prices, foreign exchange fluctuations and general economic conditions, increased costs and demand for production inputs, the speculative nature of exploration and project development, including the risks of obtaining necessary licences and permits and diminishing quantities or grades of reserves, political and social risks, changes to the regulatory framework within which Resolute operates or may in the future operate, environmental conditions including extreme weather conditions, recruitment and retention of personnel, industrial relations issues and litigation. The production target in the Scoping Study contains 100% Inferred Mineral Resources. To the extent a production target is based on those Inferred Mineral Resources, there is a low level of geological confidence associated with Inferred Mineral Resources and there is no certainty that future exploration work will result in the determination of inferred mineral resources or that the production target itself will be realised

Forward-looking statements are based on Resolute's good faith assumptions as to the financial, market, regulatory and other relevant environments that will exist and affect Resolute's business and operations in the future. Resolute does not give any assurance that the assumptions will prove to be correct. There may be other factors that could cause actual results or events not to be as anticipated, and many events are beyond the reasonable control of Resolute. Readers are cautioned not to place undue reliance on forward-looking statements, particularly in the current economic climate with the significant volatility, uncertainty and disruption caused by geopolitical events. Forward-looking statements in this document speak only at the date of issue. Except as required by applicable laws or regulations, Resolute does not undertake any obligation to publicly update or revise any of the forward-looking statements or to advise of any change in assumptions on which any such statement is based. Except for statutory liability which cannot be excluded, each of Resolute, its officers, employees and advisors expressly disclaim any responsibility for the accuracy or completeness of the material contained in these forward-looking statements and excludes all liability whatsoever (including in negligence) for any loss or damage which may be suffered by any person as a consequence of any information in forward-looking statements or any error or omission.

ASX LISTING RULE 5.16 AND 5.17 REQUIREMENTS

The material assumptions on which the production target for the Project and the forecast financial information derived therefrom are based are detailed in the Scoping Study, which is available on the Company's website.

The production target is based on 100% inferred Mineral Resources that have been prepared by Competent Persons in accordance with the requirements of the JORC Code (2012) and can be found in the Ore Reserves and Mineral Resource Statement released on the ASX on 05 March 2026.

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.

Latest directors dealings

- 1 day ago Workspace Group

- 1 day ago Talon Resources Plc

- 1 day ago Vodafone Group

- 1 day ago Synthomer

- 1 day ago Ondo Insurtech