Final Results & Notice of AGM

Summary by AI BETAClose X

Prospex Energy PLC / Index: AIM / Epic: PXEN / Sector: Oil and Gas

28 May 2026

Prospex Energy PLC

('Prospex' or the 'Company')

Final Results for Year ended 31 December 2025

and

Notice of Annual General Meeting

Prospex Energy plc, an AIM quoted investment company, is pleased to announce its audited Final Results for the year ended 31 December 2025 (the "year-end") and Notice of the Annual General Meeting ("AGM") on 23 June 2026.

Corporate Highlights

· Acquired 100% ownership of Tarba Energía S.L., including the El Romeral gas-to-power project and Tesorillo permit

· Selva Malvezzi signs new 12- month gas sales agreement with Hera Group S.r.l.

· Successfully completed a c. £1.2 million placing and subscription to support operational and development activities

· Invested c. £3.8 million into our assets in the first three quarters of 2025, with c. £2.6 million (70%) funded from internal resources

· Appointment of Hannam & Partners ('H&P') as Joint Broker

· Appointment of Richard Jameson, as Chief Operating Officer

Post-period Corporate Highlights

· The Company strengthened the board with the appointment of Tom Reynolds as Chief Executive Officer and Simon Ashby-Rudd as Non-Executive Director

· The board undertook a strategic review of the Company's asset portfolio and corporate objectives to refocus on shareholder value creation

· Total of £2 million raised via Convertible Loan Note ("CLN"), 25% above the original £1.6 million target. Funds used to support the Company's ongoing activities and anticipated 2026 cash call needs, ensuring the company retains its current ownership stake in all its investments.

· Enhanced shareholder communications and engagement activities to increase shareholder understanding and strengthen market confidence

· Advanced its strategy to expand into a third European country - Poland, with the award of the San and Dunajec exploration licences

Financial Highlights

· The Company recorded a loss for the year of £2,795,169 (2024: loss - £46,759). The current year's loss includes an unrealised loss on revaluation of investments of £2,541,311 (2024: unrealised gain £713,583) primarily related to depletion of reserves through production from the Selva Field in 2025 and lower gas prices used for valuation at 31 December 2025.

· The Company is reporting a decrease in shareholder equity (net asset value) at 31 December 2025 of £1,650,233, to £22,939,921 (2024: £24,590,154).

· Total Assets decreased by £1,248,677 to £24,509,190 (2024: £25,757,867). The decrease is primarily attributable to a decline in the valuation of the Company's investment in PXOG Marshall Limited, the investment vehicle that directly and indirectly holds 37% of the Selva Malvezzi production concession in Italy, primarily related to depletion of reserves through production from the field and lower gas prices at year end.

· At 31 December 2025, the Company held cash and cash equivalents of £38,935 (2024: £1,185,386). Post period the Company extended the CLN offer raising an additional £653,950 which, together with higher than budgeted cashflow from gas sales, saw the company ending Q1 2026 with a cash balance of £907,000 (unaudited). This is expected to cover general working capital requirements as well as anticipated capex costs for the balance of 2026.

Operational Overview

Selva Field - Northern Italy

· Consistent gas production throughout 2025 from the Podere Maiar-1 well.

· The share of production for the year attributable to the Company's investment was 10.4 MMscm, and the share of gross revenue earned from gas sales was €4.1 million.

· Signed a new 12-month gas sales agreement with Hera Trading to supply approximately 27.96 MMscm at prices linked to the Italian Gas Index (IG Index GME), which typically trades at a premium to TTF.

· Secured INTESA approval and final MASE authorisation for a 3D seismic acquisition campaign

· In December 2025, the operator completed the acquisition of approximately 140 km² of 3D seismic data, on time and within budget.

· Continued technical and permitting work in support of the planned four-well development programme.

Post-Period Selva Field Highlights

· In Q1 2026, stable production continued with gross production of 7.26 MMscm (net to Prospex 2.69 MMscm), which was sold at an average realised price of €0.43/scm, generating €1.155 million net revenue.

· Gross cumulative production exceeded 72.9 MMscm, passing the milestone certified P1 reserve level.

· Progress made on Environmental Impact Assessment (EIA) updates and development planning for the Casale Guida-1d, Ronchi-1d, Bagnarola-1d, and Selva Malvezzi-1d wells, incorporating feedback from the Ministry.

· Data from the 3D geophysical survey is undergoing processing by Schlumberger Italy

Tarba Energía, El Romeral licences and Tesorillo/Ruedalabolia Permits - Southern Spain

· In April 2025, the Company announced the acquisition of outstanding shares of Tarba Energía, resulting in full ownership of the El Romeral gas-to-power project and the suspended Tesorillo and Ruedalabola permits.

· Generated 3,752 MWh of electricity during H1 2025, delivering revenue of €365,152; however, the plant was offline from 1 July 2025 due to transformer availability issues. A new transformer was ordered in November 2025.

· Progressed permitting for five new development wells, with the EIA consultation process completed without objections from statutory consultees or the public.

· EIA statutory consultation for five new wells was publicly gazetted in February 2025 following the submission of the permit application in May 2024.

Post-Period Tarba Energia Highlights

· Production restart at El Romeral following the installation of a replacement rental transformer.

· Continued to engage with Spanish regulators regarding the delivery of permits to drill five wells at El Romeral and connect to the Spanish gas grid, supporting direct gas export.

· Engaged with potential third-party investors who have appetite and financial capability to support development of the El Romerol assets.

Viura Field - Northern Spain

· Gross production from start-up in December 2024 to end-Q1 2025 totalled 30.2 MMscm (1.1 Bcf) gross, or approximately 4.4 MMscm (154 MMscf) net to Prospex.

· Undertook a workover programme on the Viura-1B well following the detection of a tubing leak at the beginning of April 2025, which resulted in the well being shut down.

· Resolved wireline equipment issues encountered during testing operations in August 2025.

· The Viura-1B well was brought back online on 17 October 2025 with gas production increased in stages.

· Achieved average production rates of approximately 190,000 scm/d during November 2025.

Post-Period Viura Field Highlights

· During Q1 2026, operator HEI conducted a series of production trials to support the construction and calibration of a dynamic reservoir model, which will be used to inform future development drilling decisions.

· Average production rates during Q1 2026 were 107,800 scm/d gas and 163 scm/d water, although these are not indicative of steady state production.

· Modelling work is ongoing with a steady-state regime expected after the calibration trials

· 2026 focus is on the preparation of an independent reserves report with the potential to underpin a debt facility at HEI, minimising shareholder dilution and planning for future drilling and tie-in activities.

San and Dunajec Licences - Poland

· Applied for two exploration licences in the Carpathian Foreland Basin.

· San and Dunajec licences awarded post year-end with Prospex holding 100% ownership.

· Expanded the Company's European portfolio into a new operating jurisdiction with established oil and gas infrastructure.

· Began compilation and review of historical geological and production data across both licence areas.

· Continued technical assessment of the Mniszów undeveloped oil discovery within the Dunajec licence area to understand potential for near term drilling and development.

Commenting on the results, Tom Reynolds, Prospex's CEO, said:

"First of all I would like to thank Andrew Hay for his support since I joined Prospex and also for his service on the audit committee in preparing these accounts.

"Since my appointment in February, I have undertaken a comprehensive review of the Company's asset base and believe Prospex is well positioned with an enviable portfolio that combines existing cash flow, development upside and longer-term exploration potential. Selva Malvezzi continues to demonstrate its importance as the Company's foundation asset, delivering stable production and revenue while supporting the technical work required for the planned multi-well development programme. At the same time, El Romeral has returned to production, Viura offers significant potential to deliver future shareholder value through increased production and planned development activity, and our newly awarded licences in Poland provide additional longer-term upside exposure.

"I was also grateful to our shareholders for their continued support, which was evident during our extended CLN offering, which took place post period. Their support, and the additional circ. £654,000 raised, means that we are fully funded for our anticipated capex commitments this year.

"Meanwhile, European energy security and domestic supply remain high on the political agenda, and natural gas prices continue to reflect broader geopolitical pressures. We believe Prospex offers investors rare exposure to these macro tailwinds as well as attractive opportunities to add value at the asset level across its portfolio."

Notice of Annual General Meeting

The Company also gives notice that its AGM will be held at Huckletree Bishopsgate, 8 Bishopsgate, London EC2N 4BQ, at 10.00 a.m. on 23 June 2026.

The Financial Results for the year ended 31 December 2025 together with the Notice of AGM will be available to download from the Company's website: https://prospex.energy/ and will also be posted to shareholders on or around 29 May 2026.

This announcement contains inside information for the purposes of Article 7 of the Market Abuse Regulation (EU) 596/2014 as it forms part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018 ("MAR") and is disclosed in accordance with the Company's obligations under Article 17 of MAR.

* * ENDS * *

For further information visit www.prospex.energy or contact the following:

|

Tom Reynolds |

Prospex Energy PLC |

Tel: +44 (0) 20 7236 1177 |

|

Ritchie Balmer |

Strand Hanson Limited |

Tel: +44 (0) 20 7409 3494 |

|

Andrew Monk (Corporate Broking) |

VSA Capital Limited |

Tel: +44 (0) 20 3005 5000 |

|

Neil Passmore / Leif Powis |

Hannam & Partners |

Tel: +44 (0) 20 7907 8500 |

|

Ana Ribeiro / Charlotte Page |

St Brides Partners Limited |

Tel: +44 (0) 20 7236 1177 |

Prospex Energy Plc

Chairman's Report

for the year ended 31 December 2025

Prospex Energy is an AIM quoted investment company with a portfolio of producing natural gas interests in Spain and Italy, a connected electrical plant in Spain and exploration and potential development licences in Poland. The Company's core investment thesis is that European natural gas is a key strategic asset for energy security, energy supply and lower emissions.

2025 saw progress in some areas but was an operationally challenging year for the Company. Late in the year, the Board of Directors refocused the Company's strategic objectives and Tom Reynolds, a highly experienced oil and gas company Director with a successful track record in the sector, was appointed as CEO and Director effective 1 February 2026.

Increasing shareholder value, as reflected in the share price, involves growing the production and asset base by accessing alternative sources of capital and accretive financing, limiting share offerings and, where appropriate, making portfolio adjustments through acquisition or divestment. This is enabled by a strong technical and operating team, motivated to increase share price and liquidity while being sensitive to the Company's financial capacity and risk tolerance. Post year-end, Simon Ashby-Rudd joined the Board as a Non-Executive Director, bringing decades of corporate finance experience to support this goal.

The Company's main producing assets are the Viura gas field in Northern Spain, operated by HEYCO Energy Iberia ("HEI"), and the Selva Malvezzi concession in Italy, operated by Po Valley Operations Pty Limited("PVO"), a wholly owned subsidiary of Po Valley Energy Limited ("Po Valley Energy"). El Romeral in southern Spain is operated by the Company's wholly owned subsidiary, Tarba Energía S.L. ("Tarba"), while the two licences in Poland (awarded post year end) are operated by the Company's wholly owned subsidiary, PXEN Tatra SP Z. o. o. Further operational details are included in the CEO's Report.

There were several significant achievements in 2025 including the acquisition of our former partner's shares in Tarba on the exercise of a Right of First Refusal in April 2025; completion of a seismic acquisition programme at Selva Malvezzi in December; filing of the final documentation needed for the application for permits to drill five wells at El Romeral also in December; and filing applications for two licence areas in Poland, which were awarded after year end.

However, the Company faced several operational challenges during the year, including the unexpected but necessary workover at Viura which halted production and required the Company to raise funds to maintain its stake in the asset and reinstate production at the Viura-1B well. Production at El Romeral was also stopped from July 2025 to January 2026 due to an equipment issue. While natural gas prices realised at Selva Malvezzi and Viura were reasonable for most of 2025, electricity prices at El Romeral fluctuated due to Spain's solar and wind capacity and hydroelectric generation, resulting in low and sometimes negative electricity prices. Funds generated at Viura are retained in HEI to fund future capital needs pursuant to the shareholder agreement. Net operating income from Selva Malvezzi was sufficient to fund the Company's day-to-day expenses, but not to fund growth capital.

The Company undertook a placing and subscription share offering in June 2025 which was partially successful but failed to achieve all stated objectives. The Company was therefore initially unable to meet the full cash call for the Viura workover. The operator helpfully agreed to accept subsequent payment in Convertible Loan Notes as part of the December 2025 offering. The seismic acquisition campaign at Selva Malvezzi, and the capital expenditures in El Romeral required additional investment capital. The offering of unsecured Convertible Loan Notes referred to above was initiated in December 2025 and ultimately oversubscribed at completion in March 2026, raising over £1.90 million of new capital for the Company.

Facing significant challenges in accessing the capital required to protect and enhance the asset base, and the apparent lack of market support, the Board determined a need to reestablish market confidence, access alternative sources of capital and reemphasise the growth and monetisation of investments, while maintaining operating and technical excellence. Several significant changes took place including the appointment of Tom Reynolds as Chief Executive Officer in February 2026, a deep review of the Company's holdings, the appointment of Simon Ashby-Rudd as Non-Executive Director in May 2026, enhanced shareholder communications, and engagement with partners and investors.

Management and Staff

The Company benefits from an exceptional team with a broad range of skills and experience including geoscience, engineering, and finance. The team has operating experience and knowledge in Italy, Spain and Poland and engages constructively with the Company's partners. In a year marked by many technical and operational challenges, the team brought creativity and insight across all areas of activity.

I would like to thank Mark Routh for his significant contribution to bringing the Company's asset portfolio to its current stage and wish him the best in the future. Andrew Hay is not standing for re-election at the AGM. His insight and experience have been very much appreciated.

Outlook

The changes to strategic focus and leadership are solid steps toward enabling the Company to deliver on its commitment to create shareholder value. The Company has strong investments to grow upon and a team capable of delivering results. Communication and interaction with shareholders help to inform progress towards the shared goals.

Your Board of Directors appreciate the trust and confidence placed in us. On behalf of the entire team, I thank all investors, both long-term and those who have recently joined, for their support.

William Smith

Non-Executive Chairman

27 May 2026

Prospex Energy Plc

Chief Executive Officer's Report

for the year ended 31 December 2025

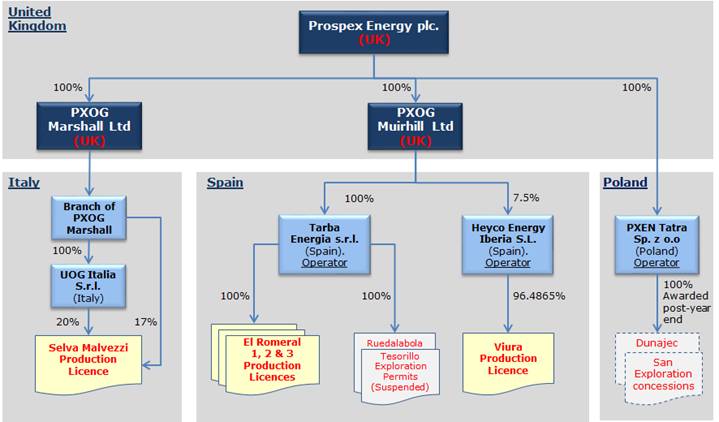

Corporate Structure and Investments

The chart below shows the ownership structure of the Prospex group of companies (the "Group").

The table below summarises the Company's investments in, and loans to, Group companies as at 31 December 2025.

|

|

Group Company: |

|

PXOG Marshall Ltd |

PXOG Muirhill Ltd |

PXEN Tatra |

||

|

|

Country of focus: |

|

Italy |

Spain |

Poland |

||

|

|

Related to: |

|

Selva Malvezzi |

Romeral & Tesorillo |

Viura |

Shares/ |

San and Dunajec |

|

|

£000's |

|

£000's |

£000's |

£000's |

£000's |

£000's |

|

Prospex Energy Plc. Balance sheet: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investments in Group Undertakings at Fair Value |

13,719 |

|

13,717 |

|

|

|

2 |

|

Included in Investments (Note 11) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans to Group Undertakings |

10,673 |

|

1,895 |

1,743 |

6,235 |

741 |

59 |

|

Included in Trade and Other Receivables (Note 12) |

|

|

|

|

|

|

|

|

Owed by PXOG Muirhill Ltd. |

8,719 |

|

|

1,743 |

6,235 |

741 |

|

|

Owed by PXOG Marshall Ltd. |

1,656 |

|

1,656 |

|

|

|

|

|

Owed by UOG Italia S.r.l. |

239 |

|

239 |

|

|

|

|

|

Owed by PXEN Tatra Sp z.o.o. |

59 |

|

|

|

|

|

59 |

|

|

|

|

|

|

|

|

|

|

Total included in Assets |

24,392 |

|

15,612 |

1,743 |

6,235 |

741 |

61 |

Preparation of Consolidated Financial Statements

Prospex Energy Plc is an investment entity as defined by IFRS 10, and as such, the results of its subsidiaries are not consolidated up to the parent company.

These financial statements therefore present the financial position of the Company on a standalone basis, and the Company's investments in its subsidiaries, joint ventures and underlying assets are recognised at fair value through profit and loss.

Asset Report

Since being appointed CEO in February 2026 the priority has been to reassess priorities and re-evaluate our investment portfolio to ensure the Group is positioned for long-term growth. Prospex has an attractive portfolio of assets that is well positioned to deliver growth through increased reserves and production. I summarise the portfolio below and for each asset include a review of 2025 activity. Guidance on the pathway to value growth and an indication of the timeline is also set out for each asset.

As of the date of writing this report, the Company has cash on hand following the extension of the Convertible Loan Note financing in Q1 2026. Continuing strength in European gas markets supports robust cashflow, adding to cash reserves.

Tarba Energía, El Romeral licences and Tesorillo/Ruedalabola permits

Asset Description

Tarba Energía S.L. ("Tarba") is owned 100% by PXOG Muirhill Limited, a wholly owned subsidiary of Prospex Energy plc. Tarba owns 100% of the El Romeral gas to power project, which includes three exploitation licences covering 310 km2, and the connected El Romeral gas to power plant located near Seville in the Andalucía region of southern Spain. Tarba also owns 100% of the suspended Tesorillo and Ruedalabola exploration permits covering 380 km2 in the Cadiz province of Spain. El Romeral delivered first gas and power in 2002. The originally developed reservoirs are largely depleted and Tarba is focused on obtaining new drilling permits to increase production and reserves.

2025 Period

2025 saw Prospex consolidating its ownership in Tarba with full ownership secured at modest cost, the permitting process for five new wells significantly advanced without material challenge and H1 production delivered modest cash flow before an extended transformer-related outage.

At the beginning of 2025 Prospex held a 49.9% working interest in Tarba. In April 2025, the Company announced the completion of the acquisition of Warrego Energy's remaining shareholding in Tarba for a total consideration of €665,725, including a deferred payment of €100,000 payable upon approval of drilling permits for three of the five wells which were then in the regulatory process. This took Prospex to 100% ownership of both El Romeral and the suspended Tesorillo permit, adding significant prospective resources at low cost.

Production performance in H1 2025 saw the El Romeral plant generate 3,752 MWh of electricity and €365,152 in sales revenue. However, the electrical plant was offline from 1 July 2025 due to a transformer availability issue. A planned two-week shutdown to replace the main transformer was extended because delivery of a more suitably sized, lower-cost unit was delayed. The Company ordered a replacement transformer in November 2025, with delivery expected in Q3 2026.

In February 2025 the EIA statutory consultation for five new wells was publicly gazetted following the submission of the May 2024 application. No adverse comments or objections were received from 29 statutory consultees or the public; the process advanced through the sub-delegation in Seville toward final Ministry review in Madrid. The applications were delivered to the Minister's office on 5 December with a target for review completion of 90-180 days.

Events after period end and asset outlook

A replacement rental transformer was installed in February 2026. This reinstated Tarba's ability to generate and export electricity. Generation is intermittent, limited by low production rates from El Romeral's depleted gas reservoirs and by volatile pricing in the Spanish electricity market, which at certain times of the day does not support economic generation. As a result Tarba is supported financially by Prospex through an interest-bearing loan to cover operating costs while permits are progressed toward approval. Generation activity contributes to Tarba income and reduces the level of support required from Prospex.

Looking ahead, the Company's focus is to continue to engage with Spanish regulatory authorities to deliver the permits which will allow the drilling of five additional wells and the construction of a direct gas export route through connection to the gas grid. This will position Tarba for significant reserve and production growth and mitigate the limitations placed on economic export by the electricity market through the ability to export gas directly to the grid. The Company has identified 11 low risk prospects with up to 2,469 MMscm (90 Bcf - Best Estimate Prospective Resource based on the Reserves and Resources Report by NSAI, 2019). This represents a significant opportunity to convert prospective resources to producing reserves and the Company expects to engage with third parties with an appetite and capability to invest alongside Prospex to support any future drilling and development capex.

Selva Malvezzi

Asset description

The Selva Malvezzi production concession is located in the Po Valley in northern Italy, covering an area of 81 km2. Prospex holds an aggregate 37% working interest through two entities. PXOG Marshall Limited, 100% owned subsidiary of Prospex, owns 17%. UOG Italia SRL, a 100% owned subsidiary of PXOG Marshall Limited, holds 20%. The concession is operated by Po Valley Operations Pty Ltd, a subsidiary of ASX listed Po Valley Energy Ltd (ASX: PVE) which holds 63%. The concession delivers natural gas production from the Podere Maiar-1 well (PM-1), which has cumulatively produced 65.6 MMscm (gross) since first gas on 4 July 2023 to 31 December 2025. The joint venture is progressing other drilling targets with the objective of increasing production and reserves.

2025 Period

The asset delivered consistent production throughout the year from the PM-1 well. The share of production for the year attributable to the Company's investment was 10.4 MMscm, and the share of gross revenue earned from gas sales was €4.1 million.. Rates remained stable at c. 80,000 scm/d (gross) for the balance of the year underpinned by strong reservoir performance and a supportive Italian regulatory environment focused on domestic gas supply security.

Permitting linked to future development planning for the broader concession advanced materially in the period. In early April 2025 the operator secured INTESA from the Emilia-Romagna Region and final MASE authorisation for a low-cost 3D geophysical survey. Field acquisition (covering c.140 km²) was originally targeted for early October 2025 to avoid harvest disruption. During May 2025 the MASE EIA technical commission requested additional flood-risk studies linked to field development (following 2023-2024 regional events), while Budrio Municipality sought relocation of the Casale Guida (North Selva) and Ronchi (South Selva) well pads on visual/noise grounds; the East Selva site was also reviewed for flood mitigation. The operator prepared an updated EIA incorporating these inputs.

In August 2025 the joint venture signed a new 12-month Gas Sales Agreement with Hera Trading (effective 1 October 2025), replacing the expiring BP contract and committing to supply approximately 27.96 MMscm at prices linked to the Italian Gas Index (IG Index GME), which typically trades at a premium to TTF.

In December 2025 the 3D seismic acquisition campaign was successfully completed on budget and on schedule, providing high-quality data to refine subsurface targets ahead of drilling expected in 2027.

Events after period end and Outlook

During Q1 2026 stable production continued with gross production of 7.26 MMscm (net to Prospex 2.69 MMscm) which was sold at an average realised price of €0.43/scm, generating €1.155 million net revenue. Cumulative gross production exceeded 72.9 MMscm, passing the milestone certified P1 reserve level. The 3D seismic data is being processed by Schlumberger Italy to create a high-resolution subsurface model supporting future development plans. Development costs of £300k primarily related to seismic processing were funded from the proceeds of the extended CLN raise.

Stable production during 2025 confirms Selva Malvezzi as a foundation asset delivering consistent cash flow while the operator progressed the necessary technical and regulatory groundwork for a four-well development programme targeting substantial additional gross contingent resources of approximately 400MMscm (14.6 Bcf), and further gross prospective resources of 2,083MMscm (75.9 Bcf).

Looking ahead during the balance of 2026 the seismic data will be processed, forming the basis for an updated Competent Persons Report ("CPR") on the asset with the potential for resource upgrades. In H2 2026 the operator plans to advance the necessary technical and regulatory work for the development programme. The CPR will also support engagement with potential investors including debt providers for the development programme planned for 2027.

Viura, HEYCO Energy Iberia

Asset description

The Viura gas field is located in Northern Spain and is Operated by HEYCO Energy Iberia ("HEI") which owns a 96.4865% interest. Prospex's wholly owned subsidiary PXOG Muirhill Limited holds a 7.5% shareholding in HEI following acquisition of 'B' shares in 2024. Prospex therefore benefits from an indirect, equivalent working interest of 7.24% in the field. Prospex does not hold a direct participating interest in the Viura concession. Prospex does not receive cashflow related to Viura production. Under the terms of the acquisition, net cashflow from Viura arising from HEI's c. 96.5% interest is retained within HEI for general corporate requirements and future capex.

Prospex rights to invest and receive cashflow from Viura are expected to change over the life of the investment:

• Investment Phase - the current phase where further investment in development drilling is expected. Prospex has the right to invest at a 15% participation level. Any net cashflow accruing within HEI can be used to offset capex.

• B share distribution -After development drilling is complete and steady state operation established - expected in 2027 - initial distribution will be to B shareholders until they recover their cumulative investment plus a premium of 10% (the "B Share Payback"). Prospex cumulative investment to 31 December 2025 is c. £6.2 million.

• General distribution - Following the B Share Payback, dividend distributions will be made to all HEI shareholders (both A and B shareholders) and Prospex share of dividend distributions will reduce to 7.5%.

The operator's best estimate of gross remaining recoverable gross reserves stands at 2.5 Bcm (90 Bcf) with Prospex net implied share of 0.18 Bcm (6.5 Bcf).

2025 Period

Production at Viura from startup in December 2024 through end-Q1 2025 totalled 30.2 MMscm (1.1 Bcf) gross, or approximately 4.4 MMscm (154 MMscf) net to Prospex. Beginning in April 2025 production was significantly disrupted due to a series of operational difficulties. In April 2025 the Viura-1B well was shut in due to a detected leak in the completion tubing. The operator HEI mobilised a workover rig to reinstate production in June 2025. The tubing repair was completed in July. The costs associated with Prospex's net share of the drilling workover costs were funded via a combined placing and WRAP retail offer, together with the issue of unsecured Convertible Loan Notes.

Testing in August 2025 using wireline downhole pressure and flow-rate monitoring encountered a pressure-control equipment failure. This required the safe cutting of the wireline cable inside the well, leaving a logging tool and cable in the tubing. Retrieval operations using equipment mobilised from Aberdeen commenced in September 2025, with production unable to resume safely until the obstruction was cleared and secured below the safety valve.

The well was brought back online on 17 October 2025 and gas production increased in stages, reaching 120,000 scm/d with 7 scm/d water by 20 October 2025. Plateau rates of 186,333 scm/d were achieved by 24 October 2025. By November 2025 the well was delivering steady natural gas production averaging around 190,000 scm/d. Water production had fallen to an average of less than 10 scm/d.

Events after period end and asset outlook

During Q1 2026 operator HEI conducted a series of production trials to support the construction and calibration of a dynamic reservoir model which will be used to inform future development drilling decisions. Average production rates during Q1 2026 were 107,800 scm/d gas and 163 scm/d water. Because the operating regimes were deliberately selected to calibrate the dynamic model these production rates are not indicative of steady state operation. The modelling work, originally scheduled for completion by end-April 2026, continued at the time of annual report preparation.

The operator anticipates establishing a steady-state regime following the calibration trials. The balance of 2026 will focus on the preparation of an independent reserves report (with the potential to underpin a debt facility at HEI) and preparatory work to support drilling and tie-in works in 2027. Participation in Viura offers Prospex the opportunity to benefit from significantly increased gas production and valuation uplift during 2027 following the planned drilling programme. Once new well production is online and HEI dividend distributions commence, Prospex will receive cashflow capable of supporting further investment in the wider portfolio.

San & Dunajec licences, Poland (awarded after period end)

Asset description

The Company applied for two licences in the Carpathian Foreland Basin in southern Poland in 2024 following an extensive work programme reviewing unlicenced potential. Prospex believes that Poland offers an attractive regime to explore for and develop hydrocarbon resources:

· The political and regulatory regimes are pragmatic and supportive of the oil & gas industry

· Poland benefits from an established oil field services sector with the equipment, capabilities and experience available locally to support asset development

· Established infrastructure. As an operating production territory, Poland has a network of infrastructure ensuring efficient and cost-efficient transportation and delivery of product to market

· Historical database. Oil and gas production has been active in Poland for over 100 years and as a result there is a broad database of seismic, well and production data available.

Two licences were awarded after period end with Prospex holding 100% ownership in both.

San is an exploration licence covering 818km2 in south-east Poland. Prospex believes the block contains attractive shallow, Miocene-age exploration potential which fit well with the Company's established strategy and technical expertise. The licence is a drill or drop permit. The Company will need to elect to drill a well before the third anniversary of award to retain the licence. The licence also places a firm obligation on Prospex to carry out an AirGravMag survey over the block within the initial three-year term.

Dunajec is an exploration licence covering 1,182km2 in southern Poland. It contains similar Miocene age, shallow gas prospectivity as well as deeper Jurassic age potential. Dunajec also contains the undeveloped Mniszów oil discovery which is described in more detail below. The Dunajec licence is also a drill or drop permit. The Company will need to elect to drill a well before the third anniversary of award to retain the licence. The licence also places a firm obligation on Prospex to carry out an AirGravMag survey over the block within the initial three-year term.

Both licences have seen very limited activity since the early 2000s and as a result the Company believes that the application of modern technology, methods and equipment developed over the last 20+ years can add value to the licences.

Mniszów discovery, Dunajec licence

Multiple discovery wells drilled in 1966 identified a 13m oil pay within fractured carbonate at approximately 600m depth, with a historically mapped oil-water contact indicating around 2 mmbbl of OOIP. The Mniszów-3 well confirmed a 13m oil-saturated interval and flowed at 45 bbl/d following a cased hole acidised test, but the field remained undeveloped due to its relatively small size and thinner reservoir compared to the nearby Grobla (1962) and Pławowice (1963) fields.

Asset outlook

Prospex intends to use modern imaging, evaluation and development techniques to support resource discovery and development on its Polish licences. The Company is currently gathering historical data across both licences to inform and prioritise its work programmes. The Mniszów shallow undeveloped oil discovery has near-term commercial potential, and the Company is assessing the opportunity for early development given the potential to deliver near-term cashflow for re-investment. Once a work programme is finalised, the 100% ownership in both licences provides Prospex with the option of farming-out to partners at the asset level to fund activity.

Financial Review

The Company recorded a loss for the year of £2,795,169 (2024: loss - £46,759).

The current year's loss includes an unrealised loss on revaluation of investments of £2,541,311 (2024: unrealised gain £713,583).

Administrative expenses decreased by £83,962 (6.6%) to £1,179,490 (2024: £1,263,452).

Net finance income increased by £292,393 to £906,826 (2024: £614,433).

The Company is reporting a decrease in shareholder equity (net asset value) at 31 December 2025 of £1,650,233, to £22,939,921 (2024: £24,590,154).

Total Assets decreased by £1,248,677 to £24,509,190 (2024: £25,757,867).

The decrease is primarily attributable to a decrease in the valuation of the Company's investment in PXOG Marshall Limited, the investment vehicle which directly and indirectly holds 37% of Selva Malvezzi production concession in Italy. A decreased valuation within PXOG Marshall Limited of its interest in the production concession arose from the utilisation during the year of the reserves at the Podere Maiar-1 production well ("PM-1"), and a decrease in European forward gas prices applied to remaining reserves of PM-1, and to contingent resources on the concession.

Total Liabilities increased by £401,556 to £1,569,269 (2024: £1,167,713).

This is comprised primarily of a provision for deferred tax and the unsecured Convertible Loan Notes in issue at the year end.

The revaluation of investments at fair value resulted in a decrease of 15.5% to £13,768,886 (2024: £16,310,197) and the unrealised loss of £2,541,311 (2024: unrealised gain - £713,583).

This unrealised loss comprises the change in the fair value of the Company's wholly owned investment vehicle, PXOG Marshall Limited. The change takes into account the reduction in the valuation of the Selva Malvezzi production concession, interest payable by the Company on its loans, and deferred taxes, offset by a reduction in the liability of PXOG Marshall to the Company through loan repayments made during 2025 and interest receivable by the Company on its loans to its subsidiary undertakings.

The Italian asset has been re-valued on a methodology consistent with that used in prior years audited financial statements, updated to reflect underlying future gas pricing based on the benchmark Title Transfer Facility ("TTF") European forward contract gas prices applicable at 31 December 2025.

At 31 December 2025, the Company held cash and cash equivalents of £38,935 (2024: £1,185,386).

Amounts owed to the Company by its investment vehicles earn interest and are repaid out of surplus funds arising from after-tax net earnings in the underlying undertakings. Where appropriate, surplus funds within the investment entities are reinvested, at the direction of the Company, to develop and diversify the underlying assets.

Business Development and outlook

In 2025, the Company's technical team conducted in-depth evaluations of a number of potential opportunities; however, no investments were made in new properties other than the acceptance of the two licences in Poland which were awarded post year end. The Company's resources were focused on protecting and growing the value of existing assets: the acquisition of additional shares in Tarba, funding well intervention work at Viura and seismic acquisition at Selva Malvezzi.

The Company has an enviable inventory of investment opportunities. Looking ahead to the balance of 2026 and beyond, Prospex will continue to prioritise the application of resources to its existing assets to increase reserves, grow production and increase cashflow. The Company will also continue to seek opportunities to add to the portfolio, particularly where production can be acquired at a favourable valuation. Due to the depth of opportunity within the existing portfolio, any additional cashflow can be quickly re-invested creating a flywheel effect that accelerates growth.

The new licences in Poland offer attractive prospectivity and potential development opportunities. This will be a key area of focus for the team in the near term, given the attractive return profile and ability to farm-down from 100% ownership to fund activities.

A significant amount of shareholder value is tied up in Prospex assets. The Company has a portfolio of investments in three European countries with very significant production potential which it is taking active steps to realise. A number of attractive investment opportunities are expected to be finalised over the next 12-18 months. It is the responsibility of the Prospex Board and management team to test whether value can be crystallised for existing assets at attractive valuations and this is supported by the current strong European gas market. If the opportunity presents itself to sell part, or all, of an existing asset to fund an investment or acquisition that offers significant future growth, this allows the Company to compound shareholder value over time whilst avoiding the need to issue shares to fund activity.

A key objective for the next 12 months is to demonstrate to shareholders and the broader market that increasing production and cashflow can be delivered by leveraging additional sources of funding and minimising the call on shareholders through equity issuance.

Tom Reynolds

Chief Executive Officer

27 May 2026

Glossary:

Bcf Billion standard cubic feet

Bcm Billion standard cubic metres

Boe Barrels of Oil Equivalent (where 1 MMBoe = 5.8 Bcf)

MMBoe Million Barrels of Oil Equivalent

mcf Thousand standard cubic feet

MMscf Million standard cubic feet

MMscfd Million standard cubic feet per day

MMscm Million standard cubic metres

MMscm/d Million standard cubic metres per day

MWh Mega Watt hour

OOIP Oil Originally in Place

scm Standard cubic metres

scm/d Standard cubic metres per day

TTF The 'Title Transfer Facility' - a virtual trading point for natural gas in the Netherlands.

Prospex Energy Plc

Statement of Profit or Loss and Other Comprehensive Income

for the year ended 31 December 2025

|

|

|

2025 |

|

2024 |

|

|

Notes |

£ |

|

£ |

|

|

|

|

|

|

|

Administrative expenses |

|

(1,179,490) |

|

(1,263,452) |

|

Share-based payment charges |

|

- |

|

(96,388) |

|

OPERATING LOSS |

|

(1,179,490) |

|

(1,359,840) |

|

(Loss)/gain on revaluation of assets |

12 |

(2,541,311) |

|

713,583 |

|

|

|

(3,720,801) |

|

(646,257) |

|

Finance income |

6 |

915,384 |

|

621,486 |

|

Finance costs |

6 |

(8,558) |

|

(7,053) |

|

LOSS BEFORE INCOME TAX |

7 |

(2,813,975) |

|

(31,824) |

|

Income tax |

8 |

18,806 |

|

(14,935) |

|

LOSS FOR THE YEAR |

|

(2,795,169) |

|

(46,759) |

|

|

|

|

|

|

|

LOSS PER SHARE |

9 |

|

|

|

|

Basic loss pence per share |

|

(0.67)p |

|

(0.01)p |

|

Diluted loss pence per share |

|

(0.67)p |

|

(0.01)p |

Prospex Energy Plc (Registered number: 03896382)

Statement of Financial Position

31 December 2025

|

|

|

2025 |

|

2024 |

|

|

Notes |

£ |

|

£ |

|

ASSETS |

|

|

|

|

|

NON-CURRENT ASSETS |

|

|

|

|

|

Investments |

11 |

13,768,886 |

|

16,310,197 |

|

|

|

13,768,886 |

|

16,310,197 |

|

|

|

|

|

|

|

CURRENT ASSETS |

|

|

|

|

|

Trade and other receivables |

12 |

10,701,269 |

|

8,262,184 |

|

Investments |

13 |

100 |

|

100 |

|

Cash and cash equivalents |

14 |

38,935 |

|

1,185,386 |

|

|

|

10,740,304 |

|

9,447,670 |

|

|

|

|

|

|

|

TOTAL ASSETS |

|

24,509,190 |

|

25,757,867 |

|

|

|

|

|

|

|

EQUITY |

|

|

|

|

|

SHAREHOLDERS' EQUITY |

|

|

|

|

|

Called up share capital |

15 |

7,375,755 |

|

7,349,585 |

|

Share premium |

|

22,124,548 |

|

21,052,369 |

|

Merger reserve |

|

2,416,667 |

|

2,416,667 |

|

Capital redemption reserve |

|

43,333 |

|

43,333 |

|

Fair value reserve |

|

12,007,734 |

|

15,315,822 |

|

Other equity reserve |

|

46,587 |

|

- |

|

Retained earnings |

|

(21,074,703) |

|

(21,587,622) |

|

TOTAL EQUITY |

|

22,939,921 |

|

24,590,154 |

|

|

|

|

|

|

|

LIABILITIES |

|

|

|

|

|

NON-CURRENT LIABILITIES |

|

|

|

|

|

Financial liabilities - borrowings |

|

|

|

|

|

- Interest bearing loans and borrowings |

17 |

536,971 |

|

- |

|

Deferred taxation |

18 |

923,787 |

|

942,593 |

|

|

|

1,460,758 |

|

942,593 |

|

|

|

|

|

|

|

|

|

|

|

|

|

CURRENT LIABILITIES |

|

|

|

|

|

Trade and other payables |

16 |

108,511 |

|

225,120 |

|

|

|

108,511 |

|

225,120 |

|

|

|

|

|

|

|

TOTAL LIABILITIES |

|

1,569,269 |

|

1,167,713 |

|

|

|

|

|

|

|

TOTAL EQUITY AND LIABILITIES |

|

24,509,190 |

|

25,757,867 |

The financial statements were approved by the Board of Directors and authorised for issue on 27 May 2026 and were signed on its behalf by:

T. H. Reynolds

Director

Prospex Energy Plc

Statement of Changes in Equity

for the year ended 31 December 2025

|

|

Share capital |

Share premium |

Merger reserve |

Capital redemption reserve |

Fair value reserve |

Other equity reserve |

Retained earnings |

Total |

|

|

£ |

£ |

£ |

£ |

£ |

|

£ |

£ |

|

Balance at 1 January 2024 |

7,279,630 |

17,158,847 |

2,416,667 |

43,333 |

14,617,174 |

- |

(20,938,603) |

20,577,048 |

|

Changes in equity |

|

|

|

|

|

|

|

|

|

Loss for the year |

- |

- |

- |

- |

- |

- |

(46,759) |

(46,759) |

|

Issue of shares |

69,955 |

4,127,368 |

- |

- |

- |

- |

- |

4,197,323 |

|

Costs of shares issued |

- |

(233,846) |

- |

- |

- |

- |

- |

(233,846) |

|

Equity-settled share-based payments |

- |

- |

- |

- |

- |

- |

96,388 |

96,388 |

|

Transfer to fair value reserve |

- |

- |

- |

- |

698,648 |

- |

(698,648) |

- |

|

Balance at 31 December 2024 |

7,349,585 |

21,052,369 |

2,416,667 |

43,333 |

15,315,822 |

- |

(21,587,622) |

24,590,154 |

|

Changes in equity |

|

|

|

|

|

|

|

|

|

Loss for the year |

- |

- |

- |

- |

- |

- |

(2,795,169) |

(2,795,169) |

|

Issue of shares |

26,170 |

1,151,488 |

- |

- |

- |

- |

- |

1,177,658 |

|

Costs of shares issued |

- |

(79,309) |

- |

- |

- |

- |

- |

(79,309) |

|

Equity component of convertible loan notes |

- |

- |

- |

- |

- |

46,587 |

- |

46,587 |

|

Transfer to fair value reserve |

- |

- |

- |

- |

(3,308,088) |

- |

3,308,088 |

- |

|

Balance at 31 December 2025 |

7,375,755 |

22,124,548 |

2,416,667 |

43,333 |

12,007,734 |

46,587 |

(21,074,703) |

22,939,921 |

Share capital - The nominal value of the issued share capital

Share premium account - Amounts received in excess of the nominal value of the issued share capital less costs associated with the issue of shares

Merger reserve - The difference between the nominal value of the share capital issued by the Company and the fair value of the subsidiary at the date of acquisition

Capital redemption reserve - The amounts transferred following the redemption or purchase of the Company's own shares

Fair value reserve - the cumulative fair value changes of the company's fixed asset investment, net of deferred tax

Other equity reserve - The equity component of the convertible loan notes assessed under IAS 32

Retained earnings - Accumulated comprehensive income for the year and prior periods

Prospex Energy Plc

Statement of Cash Flows

for the year ended 31 December 2025

|

|

|

2025 |

|

2024 |

|

|

Notes |

£ |

|

£ |

|

Cash outflow from operations |

1 |

(2,820,480) |

|

(2,606,456) |

|

|

|

|

|

|

|

Cash flows from investing activities |

|

|

|

|

|

Purchase of fixed asset investments |

|

- |

|

(1,683) |

|

Interest received |

|

680 |

|

2,402 |

|

Interest paid |

|

- |

|

(7,053) |

|

Net cash inflow/(outflow) from investing activities |

|

680 |

|

(6,334) |

|

|

|

|

|

|

|

Cash flows from financing activities |

|

|

|

|

|

New loan notes |

|

575,000 |

|

- |

|

Loan repayments |

|

- |

|

(168,487) |

|

Share issue |

|

1,177,658 |

|

4,197,323 |

|

Costs of shares issued |

|

(79,309) |

|

(233,846) |

|

Net cash inflow from financing activities |

|

1,673,349 |

|

3,794,990 |

|

|

|

|

|

|

|

(Decrease)/increase in cash and cash equivalents |

|

(1,146,451) |

|

1,182,200 |

|

|

|

|

|

|

|

Cash and cash equivalents at beginning of year |

2 |

1,185,386 |

|

3,186 |

|

|

|

|

|

|

|

Cash and cash equivalents at end of year |

2 |

38,935 |

|

1,185,386 |

Prospex Energy Plc

Notes to the Statement of Cash Flows

for the year ended 31 December 2025

1. RECONCILIATION OF LOSS BEFORE INCOME TAX TO CASH GENERATED FROM OPERATIONS

|

|

|

2025 |

|

2024 |

|

|

|

£ |

|

£ |

|

Cash flows from operations |

|

|

|

|

|

Loss before income tax |

|

(2,813,975) |

|

(31,824) |

|

Loss/(gain) on revaluation of fixed asset investments |

|

2,541,311 |

|

(713,583) |

|

Finance income |

|

(915,384) |

|

(621,486) |

|

Finance costs |

|

8,558 |

|

7,053 |

|

Operating loss |

|

(1,179,490) |

|

(1,359,840) |

|

Increase in trade and other receivables |

|

(1,524,381) |

|

(1,442,007) |

|

(Decrease)/increase in trade and other payables |

|

(116,609) |

|

99,003 |

|

Equity settled share-based payments |

|

- |

|

96,388 |

|

Net cash outflow from operations |

|

(2,820,480) |

|

(2,606,456) |

2. CASH AND CASH EQUIVALENTS

The amounts disclosed on the Statement of Cash Flows in respect of cash and cash equivalents are in respect of these Statement of Financial Position amounts:

|

Year ended 31 December 2025 |

|

31.12.25 |

|

01.01.25 |

|

|

|

£ |

|

£ |

|

Cash and cash equivalents |

|

38,935 |

|

1,185,386 |

|

|

|

|

|

|

|

Year ended 31 December 2024 |

|

31.12.24 |

|

01.01.24 |

|

|

|

£ |

|

£ |

|

Cash and cash equivalents |

|

1,185,386 |

|

3,186 |

Prospex Energy Plc

Notes to the Financial Statements

for the year ended 31 December 2025

1. STATUTORY INFORMATION

Prospex Energy Plc is a public limited company, is registered in England and Wales and is quoted on the AIM Market of the London Stock Exchange Plc. The Company's registered number and registered office address can be found on the Company Information page.

The presentation currency of the financial statements is the Pound Sterling (£), rounded to the nearest £1.

2. ACCOUNTING POLICIES

Basis of preparation

The Company's financial statements have been prepared in accordance with International Accounting Standards in conformity with the requirements of the Companies Act 2006 as they apply to the financial statements of the Company for the year ended 31 December 2025 and as applied in accordance with the provisions of the Companies Act 2006.

The Company financial statements have been prepared under the historical cost convention or fair value where appropriate.

Preparation of consolidated financial statements

The Company is an investment entity and, as such, does not consolidate the investment entities it controls. The Company's interests in subsidiaries are recognised at fair value through profit and loss.

Going concern

The Company has reported an operating loss for the 2025 year of £1,179,490 and as at 31 December 2025 had cash at bank and in hand of £38,935 and net assets of £22,939,921.

In 2026 it is expected that the Company will have continuing receipts resulting from ongoing gas sales from its investment in Italy which are either reinvested or used to repay loans to the Company. These receipts are initially being received as loan repayments together with interest charged, reimbursing the Company for capital advances made in prior years which were applied to acquisition, exploration and development costs. As a result, it is expected that the Company will again record an operating loss during 2026, but also again, an increase in cash inflows and balance sheet strength.

In Spain, gas sales from the Viura gas-field net of operating costs are applied by the Operator, HEYCO Energy Iberia ("HEI") against the Companies 15% share of costs of the continuing drilling programme, expected to complete in 2027. Once the drilling programme is complete, the Company's total investment cost (which is already net of the reinvested operating income to that point) and a 10% additional preferred return will be repaid by HEI at a rate of 15% of net after-tax income as a dividend until both the capital invested and the 10% preferred return are fully repaid. The Company will then continue to earn dividends from HEI as a 7.5% shareholder.

The Directors have prepared detailed financial forecasts and cash flows looking beyond 12 months from the date of the approval of these financial statements. In developing these forecasts, the Directors have made assumptions based upon their view of the current and future economic conditions that are expected to prevail over the forecast period.

In Q1 2026, the Company received subscriptions to £1.435m of Convertible Loan Notes. The Board expects to raise additional funding only as and when required to cover any shortfall between the Group's own cash resources and its development and expansion of activities. In the absence of sufficient funds being available to the Company from producing assets, farm-out activity, debt and equity finance, the Company has the ability to alter its planned investment activities to concentrate on key areas in order to ensure sufficient cash is available for at least 12 months from the date of approval of these financial statements.

Should regulatory approval be received which allows for an expansion of current operations, or appropriate new investment opportunities arise which meet the Company's objectives and criteria, then the Directors will explore all potential sources of funding available to meet such shortfall. Based on the Company's track-record, assets and prospects, the Directors have a reasonable expectation that they will be able to secure such further funding should the need arise.

The Directors have therefore prepared the financial statements on a going concern basis.

Property, plant and equipment

Depreciation is provided at the following annual rates in order to write off the cost less estimated residual value of each asset over its estimated useful life.

|

|

Computer equipment |

- |

25% per annum on reducing balance |

Financial instruments

Financial assets and financial liabilities are recognised on the statement of financial position when the Company becomes a party to the contractual provisions of the instrument.

2. ACCOUNTING POLICIES - continued

Loans and receivables

These assets are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. The principal financial assets of the Company are loans and receivables, which arise principally through the provision loans to subsidiary undertakings but also incorporate other types of contractual monetary asset. They are included in current assets, except for maturities greater than 12 months after the statement of financial position date. These are classified as non-current assets.

The Company's loans and receivables are recognised and carried at the lower of their original amount less an allowance for any doubtful amounts. An allowance is made when collection of the full amount is no longer considered possible.

The Company's loans and receivables comprise other receivables and cash and cash equivalents in the consolidated statement of financial position.

Financial liabilities and equity

Financial liabilities and equity instruments are classified according to the substance of the contractual arrangements entered into. An equity instrument is any contract that evidences a residual interest in the assets of the entity after deducting all of its financial liabilities.

Where the contractual obligations of financial instruments (including share capital) are equivalent to a similar debt instrument, those financial instruments are classed as financial liabilities. Financial liabilities are presented as such in the statement of financial position. Finance costs and gains or losses relating to financial liabilities are included in the profit and loss account. Finance costs are calculated so as to produce a constant rate of return on the outstanding liability.

Where the contractual terms of share capital do not have any terms meeting the definition of a financial liability then this is classed as an equity instrument. Dividends and distributions relating to equity instruments are debited direct to equity.

Equity comprises the following:

- Share capital represents the nominal value of equity shares;

- Share premium represents the excess over nominal value of the fair value of consideration received for equity shares, net of expenses of the share issue;

- Profit and loss reserve represents retained deficit;

- The capital redemption reserve arises on redemption of shares in previous years and own share reserve;

- Merger reserve represents the difference between the nominal value of the share capital issued by the Company and the fair value of the subsidiary at the date of acquisition;

- Fair value reserve represents the cumulative fair value changes of the company's fixed asset investment, net of deferred tax.

Leases

Leases are recognised as finance leases. The lease liability is initially recognised at the present value of the lease payments which have not yet been made and subsequently measured under the amortised cost method. The initial cost of the right-of-use asset comprises the amount of the initial measurement of the lease liability, lease payments made prior to the lease commencement date, initial direct costs and the estimated costs of removing or dismantling the underlying asset per the conditions of the contract.

Where ownership of the right-of-use asset transfers to the lessee at the end of the lease term, the right-of-use asset is depreciated over the asset's remaining useful life. If ownership of the right-of-use asset does not transfer to the lessee at the end of the lease term, depreciation is charged over the shorter of the useful life of the right-of-use asset and the lease term.

Taxation

Current taxes are based on the results shown in the financial statements and are calculated according to local tax rules, using tax rates enacted or substantially enacted by the statement of financial position date.

Deferred tax is provided in full, using the liability method, on temporary differences arising between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes. Deferred tax is determined using tax rates that have been enacted or substantially enacted at the balance sheet date and are expected to apply when the related deferred income tax asset is realised, or the deferred tax liability is settled. Deferred tax is charged or credited in the income statement, except when it relates to items charged or credited to equity, in which case the deferred tax is also dealt with in equity. Deferred tax assets are only recognised to the extent that it is probable that future taxable profit will be available against which the asset can be utilised.

Cash and cash equivalents

Cash and cash equivalents include cash at bank and in hand and short-term deposits with an original maturity of three months or less.

Trade and other payables

Trade and other payables are initially measured at fair value and subsequently measured at amortised cost using the effective interest rate method.

Foreign currency translation

Items included in the Financial Statements are measured using the currency of the primary economic environment in which the Company operates (the functional currency) which is UK sterling (£). The Financial Statements are accordingly presented in UK Sterling

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the transactions or at an average rate for a period if the rates do not fluctuate significantly. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognised in the Statement of Profit or Loss. Non-monetary items that are measured in terms of historical cost in a foreign currency are not retranslated.

Finance income and finance costs

Finance income is recognised when it is probable that the economic benefits will flow to the Company and the amount of income can be measured reliably. It is accrued on a time basis by reference to the principal outstanding and at the effective interest rate applicable.

Borrowing costs are recognised as an expense in the period in which they are incurred.

Equity-settled share-based payment

The Company makes equity-settled share-based payments. The fair value of options granted is recognised as an expense, with a corresponding increase in equity. The fair value is measured at grant date and spread over the vesting period, which is the period over which all of the specified vesting conditions are to be satisfied. The fair value of the options granted is measured based on the Black-Scholes framework, taking into account the terms and conditions upon which the instruments were granted. At each statement of financial position date, the Company revises its estimate of the number of options that are expected to become exercisable. It recognises the impact of the revision to original estimates, if any, in the income statement, with a corresponding adjustment to equity.

New standards, interpretations and amendments adopted from 1 January 2025

The following amendments are effective for the period beginning 1 January 2025:

• Lack of Exchangeability (Amendments to IAS 21).

• Amendments to the SASB standards to enhance their international applicability (

These amendments had no effect on the financial statements of the Company. In the current year the Company has applied a number of new and amended IFRS Accounting Standards issued by the International accounting Standards Board ("IASB") and adopted by the UK, that are effective for the first time for the financial year beginning 1 January 2025 Their adoption has not had any material impact on the disclosure or on the amounts reported in these financial statements.

New standards, interpretations and amendments effective from 1 January 2026 onwards

There are a number of standards, amendments to standards, and interpretations which have been issued by the IASB that are effective in future accounting periods that the Group has decided not to adopt early.

|

|

|

Effective date (period beginning on or after) |

|

IFRS 9 and IFRS 7 |

Financial instruments Amendment regarding the classification and measurement of financial instruments |

01/01/2026 |

|

IFRS 1 |

First-time Adoption Amendment - Hedge accounting for first-time adopter |

01/01/2026 |

|

IFRS 7 |

Financial instruments; Disclosures Amendment - Gain or loss on derecognition |

01/01/2026 |

|

IFRS 7 |

Financial instruments: Disclosures Amendment - deferred difference between fair value and transaction price |

01/01/2026 |

|

IFRS 7 |

Financial instruments: Disclosures Amendment - Introduction and credit risk disclosures |

01/01/2026 |

|

IFRS 9 |

Financial instruments: Amendment - Lessee derecognition of lease liabilities |

01/01/2026 |

|

IFRS 9 |

Financial instruments: Amendment - Transaction price |

01/01/2026 |

|

IFRS 10 |

Consolidated financial statements: Amendment - Determination of a 'de facto agent' |

01/01/2026 |

|

IAS 7 |

Statement of Cash Flows: Amendment - Cost method |

01/01/2026 |

|

IFRS 9 and IFRS 7 |

Financial instruments: Amendment - Contracts referencing nature-dependent electricity |

01/01/2026 |

|

IFRS 18 |

Presentation and disclosures in financial statements Original issue |

01/01/2027 |

|

IFRS 19 |

Subsidiaries without public accountability: Disclosures Original issue |

01/01/2027 |

|

IFRS 19 |

IFRS for SMEs - third edition |

01/01/2027 |

|

IFRS S2 |

Greenhouse Gas Emissions Disclosures: Amendment - simplification of disclosures |

01/01/2027 |

|

IAS 21 |

The Effects of Changes in Foreign Exchange Rates: Amendment - Translation to a Hyperinflationary presentation currency |

01/01/2027 |

IFRS 18 Presentation and Disclosures in Financial Statements

IFRS 18 replaces IAS 1, carrying forward many of the requirements in IAS 1 unchanged and complementing them with new requirements.

IFRS 18 introduces new requirements to:

• present specified categories and defined subtotals in the statement of profit or loss

• provide disclosures on management-defined performance measures (MPMs) in the notes to the financial statements

• improve aggregation and disaggregation.

The Company is currently assessing the effect of these new accounting standards and amendments, but does not expect that they will have a material impact on the Company's financial statements in future periods.

The Company does not expect to be eligible to apply IFRS 19.

Revenue recognition

Revenue is measured at the fair value of consideration receivable, net of any discounts and VAT. It is recognised to the extent that the transfer of promised services to a customer has been satisfied, and the revenue can be reliably measured.

Revenue from the rendering of services to the customer is considered to have been satisfied when the service has been undertaken.

Revenue which is not related to the principal activity of the Company is recognised in the Statement of Profit or Loss as other operating income. Such income includes consultancy fees and rent receivable.

3. CRITICAL ACCOUNTING JUDGEMENTS AND KEY SOURCES OF ESTIMATION UNCERTAINTY

The preparation of the financial information in conformity with IFRS requires the use of certain critical accounting estimates that affect the reported amounts of assets and liabilities at the date of the financial information and the reported amounts of revenue and expenses during the reporting period. Although these estimates are based on management's best knowledge of the amounts, events or actions, actual results ultimately may differ from these estimates. The estimates and underlying assumptions are as follows:

Investment entities

The judgements, assumptions and estimates involved in the Company's accounting policies that are considered by the Board to be the most important to the portrayal of its financial condition are the fair valuation of the investment and the assessment regarding investment entities. The investment portfolio is held at fair value. The Directors review the valuations policies, process and application to individual investments.

Entities that meet the definition of an investment entity within IFRS 10 are required to account for most investments in controlled entities, as well as investments in associates and joint ventures, at fair value through profit and loss. The Board has concluded that the Company continues to meet the definition of an investment entity as its strategic objective of investing in portfolio investments for the purpose of generating returns in the form of investment income and capital appreciation remains unchanged.

Fair value is the underlying principle and is defined as "the price that would be received to sell an asset in an orderly transaction between market participants at the measurement date". Fair value is therefore an estimate and, as such, determining fair value requires the use of judgement. The quoted assets in our portfolio are valued at their closing bid price at the statement of financial position date. The largest investment in the portfolio, however, is represented by an unquoted investment.

Impairment of assets

The Company's principal investments are in wholly owned unquoted subsidiaries which each have a minority interest in overseas entities with energy assets.

The Company is required to test, on an annual basis, whether its non-current assets have suffered any impairment. Determining whether these assets are impaired requires an estimation of the value in use of the cash-generating units to which the assets have been allocated. The value in use calculation requires the Directors to estimate the future cash flows expected to arise from the cash-generating unit and a suitable discount rate to calculate the present value. Subsequent changes to the cash generating unit allocation or to the timing of cash flows could impact on the carrying value of the respective assets.

The calculation of value-in-use for energy assets under development or in production is most sensitive to the following assumptions:

- Commercial reserves

- production volumes;

- commodity prices;

- fixed and variable operating costs;

- capital expenditure; and

- discount rates.

A potential change in any of the above assumptions may cause the estimated recoverable value to be lower than the carrying value, resulting in an impairment loss. The assumptions which would have the greatest impact on the recoverable amounts of the fields are production volumes and commodity prices.

Share based payments

The estimates of share-based payments requires that management selects an appropriate valuation model and make decisions on various inputs into the model including the volatility of its own share price, the probable life of the options before exercise and behavioural consideration of employees.

Deferred tax assets

Deferred taxation is provided for using the liability method. Deferred tax assets are recognised in respect of tax losses where the Directors believe that it is probable that future profits will be relieved by the benefit of tax losses brought forward. The Board considers the likely utilisation of such losses by reviewing budgets and medium-term plans for the Company. The Directors have decided that no deferred tax asset should be recognised at 31 December 2025. If the actual profits earned by the Company differs from the budgets and forecasts used then the value of such deferred tax assets may differ from that shown in these financial statements.

4. REVENUE

Segmental reporting

The Company operates a single reportable segment, being an Investing Company. All of the Company's activities are conducted from the UK. Segmental information is therefore not presented, as the Directors consider that the financial statements provide sufficient information.

5. EMPLOYEES AND DIRECTORS

|

|

2025 |

|

2024 |

|

|

£ |

|

£ |

|

Wages and salaries |

355,042 |

|

517,939 |

|

Social security costs |

39,823 |

|

49,640 |

|

Other pension costs |

15,555 |

|

6,073 |

|

Share-based payments |

- |

|

96,388 |

|

|

410,420 |

|

670,040 |

The average number of employees during the year was as follows:

|

|

2025 |

|

2024 |

|

|

Number |

|

Number |

|

Directors |

4 |

|

4 |

|

Staff |

1 |

|

1 |

|

|

5 |

|

5 |

Under the Pensions Act 2008, every employer must put certain staff into a pension scheme and contribute to it. The Company auto-enrolled its eligible employees in a defined contribution scheme. The charge to the Statement of Profit or Loss represents the amounts paid to the scheme. At the year end, the amount due to the pension scheme was £nil (2024: £nil).

Details of Directors' remuneration can be found in note 23.

6. NET FINANCE COSTS

|

|

2025 |

|

2024 |

|

|

£ |

|

£ |

|

Finance income |

|

|

|

|

Interest receivable on group loans |

914,704 |

|

619,084 |

|

Bank interest receivable |

680 |

|

2,402 |

|

|

915,384 |

|

621,486 |

|

Finance costs |

|

|

|

|

Loan interest payable |

8,558 |

|

6,753 |

|

Interest on overdue tax |

- |

|

300 |

|

|

8,558 |

|

7,053 |

|

|

|

|

|

|

Net finance income |

906,826 |

|

614,433 |

7. LOSS BEFORE INCOME TAX

The loss before income tax is stated after charging:

|

|

2025 |

|

2024 |

|

|

£ |

|

£ |

|

Auditors remuneration |

45,000 |

|

30,000 |

|

Foreign exchange differences |

(46,898) |

|

1,289 |

8. INCOME TAX

|

|

2025 |

|