Strategic Review, Reset & Roadmap

Summary by AI BETAClose X

LEI: 213800ZPHCBDDSQH5447

11 March 2026

This announcement contains information that is inside information for the purposes of Article 7 of the UK version of Regulation (EU) No. 596/2014 which is part of UK law by virtue of the European Union (Withdrawal) Act 2018, as amended (the Market Abuse Regulation).

NextEnergy Solar Fund Limited

("NESF" or "the Company")

Strategic Review, Reset & Roadmap

NextEnergy Solar Fund, a leading specialist investor in solar energy and energy storage, is pleased to announce the outcome of the Board's comprehensive strategic review, alongside a strategic reset that establishes a clear roadmap to deliver increased shareholder returns.

The Company will present its strategic reset and roadmap in detail this morning at 10:30am GMT. Further details on how to register for the presentation can be found at the bottom of this announcement.

Key Highlights

After reviewing a broad range of options during the Board's strategic review and assessing sentiment from investors, the Board has decided that a strategic reset is currently the best option available to the Company and pursuing it is in the best interest of its shareholders.

The Strategic Reset:

· A shift in focus to total returns: The Company will in future aim to deliver a balanced total return profile that provides ordinary shareholders with both attractive income and capital growth, targeting total long‑term returns of between 9% to 11%.

· Long‑term income distribution: Following the payment of this year's ordinary share target dividend of 8.43p, the Company will transition from a progressive dividend policy to a percentage‑based dividend policy, targeting a 75% distribution of operating free cashflows, post debt servicing and portfolio and fund operating expenses. The new dividend policy is expected to free up approximately £40m of operational free cash flows over the next five years, unlocking capital for the Company to strengthen its balance sheet through additional debt repayments while also supporting future Net Asset Value growth opportunities. Following the sale of the final phase of the capital recycling programme, during which 100MW of operational assets were successfully sold, and also reflecting the impact of lower power prices, the estimated dividend range for FY26/27 would be 4.0p to 4.6p per Ordinary Share, which is the equivalent to a c.7% to c.8% dividend yield as at 10 March 2026.

· A reduction in debt: The Company will reduce and maintain its total gearing in a range between 40% to 45% of Gross Asset Value ("GAV"), comfortably below the Company's investment policy limit of 50%.

· Initiate more frequent capital recycling events for reinvestment: The Company will expand its Capital Recycling Programme through additional asset sales of up to 120MW. The Company will also benefit from the realisations of its private solar fund investment and two co-investments from 2027 onwards, representing the equivalent of 116MW.

· Restart NAV growth: The Company will target renewed NAV growth through repowering existing solar assets with the latest technology to increase power output alongside the addition of co-located energy storage, which would enable the Company to ensure long-term asset health and performance, whilst adding revenue diversification.

· Increase energy storage exposure: The Company will look to increase its allocation to energy storage up to 30% of GAV. This will enhance the Company's existing stable revenues generated by its operational solar assets and support future revenues post the end of the Company's subsidised asset period.

This roadmap is a clear and deliverable route for the Company to accelerate NAV growth while reducing the Company's total debt. It will enable the Company to free up capital to access a range of investment opportunities that align with long-term structural trends in the sector, with the aim of providing shareholders with long-term visibility and enhancing long-term returns.

Foreword from the Chair - Tony Quinlan, Chair of NextEnergy Solar Fund Limited:

"NESF is a leading participant in the UK's energy transition, owning a high‑quality portfolio of attractive solar and energy storage assets primarily across the country. The solar sector has undergone substantial technological and economic progress over the past decade and now plays a critical role in meeting Britain's future energy needs.

The strategic reset represents a pivotal moment for the Company, positioning NESF to fully capitalise on developments within the sector. Following a comprehensive strategic review, the Board has concluded that recalibrating the Company's strategy is essential to ensure NESF adapts to the evolving equity and power markets and is positioned for sustainable growth. A central element of this plan is addressing the current share discount through a realignment of the dividend policy to a 75% payout ratio, releasing capital to strengthen the balance sheet, improve asset health, repower sites, and invest in higher‑return opportunities such as energy storage, driving long‑term NAV growth.

This reset is designed to maximise long‑term shareholder value and seize the significant opportunities emerging in the UK market. It enables NESF to maintain a stable income profile while transitioning towards a total‑return‑focused strategy. With a clear roadmap, a resilient asset base, and the strong expertise of our Investment Adviser, we are confident that this strategic shift will restore growth and unlock the substantial potential presented by the UK's clean energy transition."

The Big Picture

Informed by both the ongoing engagement with shareholders and its own assessment of market conditions, the Board considers that the persistent discount to NAV across the listed renewable infrastructure sector is neither sustainable nor acceptable and reflects investor views that more fundamental strategic change is required for companies to adapt to the current market environment.

Although UK interest rates have been reduced, the Company's ability to access additional capital from equity markets, whether for reinvestment, asset expansion, or deployment into new opportunities, is constrained. The traditional model for listed investment companies such as NESF, which has supported growth and shareholder returns to date, is not capable of raising additional investment capital in the current environment.

Despite this disconnect, the UK's evolving renewables landscape provides a strong and supportive long‑term foundation for disciplined investment across both solar generation and energy storage. The Government has committed to achieving net‑zero greenhouse gas emissions by 2050, and its 'Clean Power 2030 Action Plan' outlines ambitious interim goals, including delivering up to 50GW of operational solar capacity and 27GW of energy storage by 2030. These targets represent a significant step up from the approximately 21GW of solar and 7GW of energy storage in place at the end of 2025.

Key drivers:

· The future role of solar and energy storage in investment companies ("ICs") is pivotal in delivering net zero targets and energy security:

o Solar and energy storage are essential in all future energy scenarios and there is an expectation of significant power demand growth driven by AI and Datacentre demand.

o Policy tailwinds are providing positive momentum through support for domestic renewables resilience alongside national targets being set (e.g. Clean Power 2030 "CP30" / Net Zero).

o Solar and energy storage are scalable now, with solar being classed as a core infrastructure asset and energy storage no longer being an emerging technology.

o The need for energy security continues to rise in an increasingly unstable geo-political landscape, where secure, domestic energy systems are now essential.

o ICs are the right investment structure for these types of physical assets that provide liquid access to a diversified long‑life renewable portfolio for all investors.

· Positive market drivers provide a robust foundation for NESF's strategic reset:

o Macroeconomics:

- Headwind: Elevated interest rate cycles have driven significant negative impacts across the sector over the last couple of years.

- Tailwind: UK interest rates have been steadily decreasing since 2024 with further softening expected in 2026, despite recent events in the Middle East.

o Policy & Regulatory Environment:

- Headwind: Government consultations on ROC and FiT created significant uncertainty.

- Tailwind: Clean Power 2030 mandates a tripling of solar capacity to 50GW and a four-fold increase in energy storage to 27GW.

o Market Environment:

- Headwind: Future long-term power price forecasts have been falling and the current discount to NAV constrains new capital raises meaning renewable ICs cannot scale.

- Tailwind: Electricity demand is still rising and the need for energy security is higher than ever.

o Capital Flows & Sentiment:

- Headwind: Capital outflows created an oversupply of shares relative to demand therefore the current discount to NAV remains dislocated to the potential opportunity in the market.

- Tailwind: The UK's clean power transition requires sustained, large-scale generation investment and NESF's portfolio remains robust.

· NESF's portfolio fundamentals remain strong:

o Portfolio size: NESF has grown its portfolio to 99 operating solar & energy storage assets, alongside a $50m investment into a private solar infrastructure fund, NextEnergy III LP ("NEIII"), as at 10 March 2026.

o Portfolio performance: NESF's portfolio continues to perform well. As at 31 December 2025, the portfolio generation was +1.5% above forecast for FY25/26 year-to-date.

o Dividend track record: NESF has an 11-year track record of delivering a cash covered dividend, with £431m of dividends (82.6p/share) declared to ordinary shareholders as at 31 December 2025.

o Diversification: Since IPO, NESF has successfully expanded its portfolio internationally and into energy storage assets.

o ESG & Sustainability: NESF has built a portfolio that is making a genuine impact, generating enough electricity to power c.254,000 homes each year.

o Experienced independent Board: NESF benefits from a strong governance structure, with an independent Board of Directors.

The Opportunity

Against this backdrop, NESF is well positioned to contribute meaningfully to the UK's energy transition, and energy security, through the continued expansion and optimisation of its solar and storage portfolio. To protect value and ensure NESF is positioned for stability and future growth, the Board, alongside the Company's Investment Manager and Investment Adviser, concluded that a strategic reset is required. As part of this reset, the Company has set out a number of long‑term strategic goals designed to strengthen NESF's foundations, achieve growth, and improve its ability to generate sustainable total returns. In summary, these are:

· Provide shareholders with a total return of 9% to 11%.

· Restart NAV growth.

· Reduce debt to a range between 40% to 45% of GAV.

· Provide a long‑term dividend that is covered through a 75% payout ratio.

· Initiate regular capital recycling for reinvestment.

· Repower existing assets.

· Increase energy storage assets to 30% of portfolio GAV.

The Board believes these goals set a credible path to unlock value, restore market confidence, and create a clear route for long‑term shareholder return.

NESF has a high‑quality portfolio of operational assets, that the market continues to undervalue, with NESF's intrinsic value not reflected in the ordinary share price. There is an opportunity for the Company to initiate regular asset sales to raise proceeds for NAV accretive reinvestment by increasing the number of assets for sale in the Company's Capital Recycling Programme, alongside using the proceeds from the realisations of the Company's $50m private solar fund investment into NEIII and its affiliated co-investments, in line with the previously announced timing expectation from 2027 onwards.

The Investment Adviser has completed a full review of the Company's assets and identified assets that offer additional value creation opportunities. These assets will sit at the heart of the Company's portfolio to support the long-term dividend. Assets identified outside of this will be selectively used to extend the Capital Recycling Programme and be sold to create new opportunities to extract long-term value for shareholders.

Graph 1: Treemap showing NESF's entire portfolio of operating and development assets

· This treemap diagram displays NESF's portfolio as a set of nested rectangles, where the size of each box represents an individual asset as a proportion of the whole portfolio.

· Assets were scored against different criteria to identify the best fit value creation opportunities for NESF.

A key opportunity, alongside repaying debt, is to recycle this capital into energy storage projects, helping diversify the portfolio whilst adding higher‑yielding assets to NESF's predominantly solar generation profile. NESF has access to a material value opportunity via repowering its existing solar sites alongside the introduction of co‑located energy storage systems. When co‑located with solar, energy storage can optimise generation to align with demand, unlock additional revenue streams, and materially strengthen project economics by maximising the value of existing grid connections, which remain a critical constraint in the current market.

By creating access to capital, the Board believes NESF's platform, pipeline access, and operational expertise position the Company well to deploy recycled capital into repowering assets and energy storage opportunities that align to the UK's Clean Power 2030 Action Plan.

Results of the Board's strategic review

During the strategic review, the Board evaluated a broad set of options, including maintaining the status quo, a strategic reset, a managed wind‑down, a structural transformation, a public‑to‑private transaction, sector consolidation (NAV‑for‑NAV), and use of third‑party private capital.

Against each of these options, the Board reached the following conclusions:

· Maintaining the status quo: NESF's shareholders require proactive measures to provide long-term total returns and narrow the share price discount to NAV. Therefore, the Board concluded that doing nothing is not an option.

· Managed wind-down: Given the current opportunity for growth and the additional value that can be realised from continued proactive management of the Company's existing assets, the Board does not believe a wind‑down is in shareholders' best interests. Recent market experience shows that wind‑downs have been value‑destructive, with companies becoming forced sellers of assets at discounted prices, eroding rather than preserving long‑term value.

· Structural transformation: A strategic transformation of NESF from an Investment Company to an alternate operating model, e.g. Op-Co. This was discounted at an early stage as it was not cost-effective or value-creating.

· Sector consolidation: The Board concurs with consistent advice from third-party advisers that the strategic value case for sector consolidation or bi-lateral mergers is difficult to make in current market conditions. The pervasive nature of deep discounts across the renewable investment company sector demonstrates that a combination creating a larger vehicle would not, on its own, be a path to narrowing the discount or increased stock liquidity for NESF shareholders. Whilst some limited potential to unlock synergies may exist on a case-by-case basis, these are generally not of sufficient scale to justify incurring the cost, complexity and risk inherent in pursuing NAV-for-NAV or all-equity mergers.

· Public-to-private: The Board has an unrelenting focus to maximise value for shareholders, therefore it has not excluded such a transaction where there is an opportunity to crystallise shareholder value.

· Third-party capital: The Board and the Investment Adviser are exploring the opportunities to use third‑party private capital alongside the Company's existing development pipeline to inject new capital, capture growth, and extract value. The Company will continue to explore this option alongside the strategic reset to unlock potential additional value for shareholders.

· Strategic reset: A strategic reset, as set out and confirmed in this announcement, will enable the Company to utilise the levers fully within its control, including changing the dividend policy to free up capital and, through additional asset sales, to regularly recycle capital. This will free the resources required for the Company to pursue debt repayment, make NAV accretive investment such as through asset repowering, strengthening asset health, and extending asset lifetimes, actions that support long‑term performance and sustained NAV growth. It will also enable the Company to pursue value‑accretive opportunities that diversify the portfolio and its revenue streams, ensuring it is well positioned to capture additional income sources in a post‑subsidy environment.

After reviewing all options and assessing sentiment from investors, the Board have decided that a strategic reset is currently the best option available to the Company and that pursuing it is in the best interest of its shareholders.

The Reset

The Company is taking proactive action as part of this strategic roadmap to unlock capital by changing its dividend policy and extending its capital recycling programme to raise proceeds for reinvestment.

Dividend Policy Change:

· Following the completion of this year's target dividend of 8.43p, the Company will transition from a progressive dividend policy to a percentage‑based dividend policy, targeting a 75% distribution of operating free cashflows, post debt servicing and portfolio and fund operating expenses. The new dividend policy is expected to free up approximately £40m of operational free cash flows over the next five years, unlocking capital for the Company to strengthen its balance sheet through additional debt repayments while also supporting future Net Asset Value growth opportunities. Following the sale of the final phase, the current capital recycling programme, during which 100MW of operational assets were successfully sold, and also reflecting the impact of lower power prices, the estimated dividend range for FY26/27 would be 4.0p to 4.6p per Ordinary Share, which is the equivalent to a c.7% to c.8% dividend yield as at 10 March 2026.

· Cashflows that are not distributed to shareholders will be used to accelerate debt reduction and redeploy capital into higher‑yielding opportunities such as repowering and co‑located energy storage to support long-term growth.

· The Company is on track to meet its current full-year target dividend of 8.43p per Ordinary Share for the financial year ending 31 March 2026.

· As part of the Company's ongoing approach to transparency, please see below the indicative long-term ordinary share dividend guidance.

Graph 2: Indicative long-term ordinary share dividend guidance 1

· Post the ROC/FiT subsidy end, NESF has future long-term optionality to reinvest to provide dividend upside in the future, as shown below. The dotted continuous reinvestment line shows what happens to the indicative dividend if NESF continues re-investing 25% of operational cashflows back into the portfolio post subsidy end. This scenario is conservative and has not included any further opportunities for upside such as additional asset recycling, equity raises, utilising third party capital, or any other action currently outside of the Company's control.

Graph 3: Possible long-term ordinary share dividend path post ROC / FiT subsidy end 1

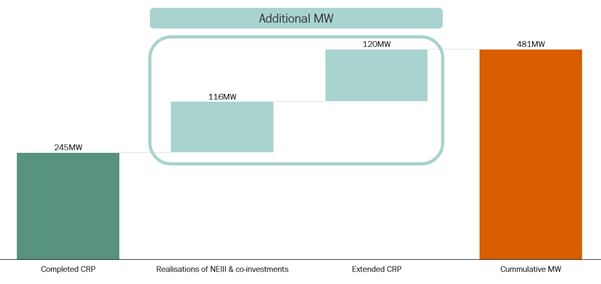

Targeting additional capital recycling for reinvestment:

· The Company will extend its Capital Recycling Programme ("CRP") by up to 120MW by selling assets in the portfolio identified for potential disposal as shown in the treemap earlier. These assets have been selected based on their limited near-term value enhancement potential. The Company expects the additional disposals to be executed in phases over multiple years.

· The Company will also use proceeds from the realisations of the Company's $50m private solar fund investment into NEIII and NESF's two co-investments, that represent 116MW of capacity owned by NESF as an investor. Realisations of the Company's NEIII and co investment interests are expected from 2027 onward, consistent with normal fund life cycles, each creating a significant cash-flow event to drive the Company's strategic roadmap plan.

Graph 4: Additional capital recycling, and NEIII & Co-investments planned realisations (MW)

By combining both the dividend policy change and additional capital recycling the Company will unlock significant capital going forward to help deliver the goals of the strategic roadmap. The graph below provides indicative long-term cash flow guidance, with the green area (operational free cashflow) created from the actions taken in the strategic reset. The graph also accounts for fund expenses (light blue), preference share dividends (orange) and the payment of the new ordinary share dividend (light orange).

Graph 5: Indicative guidance: Long-term cash flows 1

The Delivery

Capital generated through the strategic reset will be prioritised in line with the Company's capital allocation framework that is focused on improving financial resilience and supporting long‑term value creation. Full details of the capital allocation framework will be explained in today's presentation. The framework creates a hierarchy of the different possible uses for capital that is in the best interests of the Company and its shareholders, whilst providing ongoing flexibility to change the hierarchy order to react to different market conditions.

· Debt Repayment: The Company will repay a proportion of its Short-Term Revolving Credit Facility in addition to the ongoing amortisation of the Company's £143.7m long-term debt, which is on track to fully amortise in line with the remaining life of the portfolios subsidised assets. The Company will target its gearing limit between 40% to 45% of the Company's GAV.

· Investment into Asset Health & Performance Optimisation: The Company will reinvest into the long-term health of the Company's core operational portfolio to help sustain the Company's NAV and drive long-term asset performance.

· Repowering Solar Assets to Unlock Hybridisation Opportunities: The Company will actively pursue NAV accretive repowering opportunities across its current operational core solar portfolio which will also unlock the opportunity to develop higher yielding co-located energy storage assets. This approach offers significant cost savings by utilising the same grid connection for both assets whilst overcoming grid connection issues currently associated by retrofitting co-located energy storage.

· Energy Storage Expansion: To realise the significant opportunities anticipated over the next decade, the Company will seek an amendment to its investment policy to increase its energy storage allocation to 30% of its GAV, aligning this with the roadmap commitment of delivering growth and higher total returns. Two-hour duration energy storage projects are expected to generate 10% to 13% IRRs, which are at the upper end of the Company's target range. The Company intends to seek shareholder approval at the AGM to increase the formal investment policy limit for energy storage from 10% to 30% of GAV.

· Share Buybacks: To date the Company has purchased 15,621,142 Ordinary Shares for a total consideration of £11.5m. Although this programme has temporarily paused primarily due to debt limits, share buybacks remain a powerful tool available to the Company and will continue to form part of the Company's ongoing capital allocation framework.

The Goal

As the Company delivers against the roadmap established through the strategic reset, the Board and the Investment Adviser strongly believe that total shareholder returns will strengthen over time. The three graphs below illustrate the indicative shape of the Company's targeted long‑term returns and highlight the benefits of actioning the strategic reset now. This reset enables NESF to prioritise long‑term NAV growth, supporting long-term and more sustainable dividends, whilst maintaining near‑term distribution certainty. By reinvesting capital where appropriate, the strategy ensures the dividend policy remains robust and creates meaningful upside potential for shareholders in the future.

Graph 6: Indicative components that build total target return of 9 - 11% 1,2

· The Company is targeting long-term total returns of 9% to 11%.

· The dividend income distributed to ordinary shareholders through the 75% dividend policy is anticipated to steadily increase over time in line with new assets coming online, including higher-yielding energy storage assets.

· NAV growth is driven by recycling of capital into reinvestment through repowering, co-located energy storage and construction/development assets, reflecting an uplift when assets are energised.

· The strategy also captures the narrowing of the discount, which is a key goal, as pro-active actions drives value alongside the market backdrop recovering.

Graph 7: Indicative guidance: Long-term cumulative NAV return 1

· This graph highlights the long-term total NAV return out to 2040, representing a total NAV return of +3.2% compound annual growth rate ("CAGR").

Graph 8: Indicative guidance: Long-term NAV value created (Roadmap vs no action) 3

· This graph highlights the long-term benefits of the strategic reset and delivery versus no action, where there is a short-term opportunity cost, through the change in the dividend policy, which is heavily outweighed by the benefit of enhanced total NAV return in the long run.

The Board believes this roadmap presents a credible path to unlock value, restore market confidence, and create a clear route for long‑term shareholder return. Combining the reset and delivery with the right ingredients, NESF can deliver the goals of the roadmap.

Strategic Roadmap Presentation:

The Company will present its strategic roadmap in more detail this morning followed by a Q&A session. To view via webcast please use the registration link below.

· Registration and Webcast link: [Click Here]

· Time: 10:30 GMT

· Date: Wednesday 11 March 2026

· Duration: Approximately 2 hours

· Presenters:

o Tony Quinlan: Chair, NextEnergy Solar Fund

o Ross Grier: Chief Investment Officer, NextEnergy Capital

o Stephen Rosser: Investment Director, NextEnergy Capital

· A recording of the presentation will be made available on the London Stock Exchange and Company's website shortly after the event.

Footnotes:

(1) Assumptions: 75% of earnings distributed for dividend; NAV as at 31 December 2025; includes ROC / FiT consultation effect; RCF and Preference shares are maintained in the structure indefinitely.

(2) Assumes that the ordinary share price discount remains at 39.9%. Targeting share price discount reduction to 10.0% to 0.0%.

(3) Assumptions for base case: Same assumptions as (1) but no assets are sold and recycled into new investments, NEIII & co-investments proceeds are used to pay down RCF.

- End -

This announcement has been made by the Board of NextEnergy Solar Fund, the Investment Adviser [NextEnergy Capital Limited], and the Investment Manager [NextEnergy Capital IM Ltd] in good faith based on the information available to them at the time of this announcement.

This document is issued by NextEnergy Capital Limited ("NEC"), which is authorised and regulated by the UK Financial Conduct Authority ("FCA") with registered number 471192.

This document is not an offer to sell, or a solicitation of an offer to acquire, securities of the NextEnergy Solar Fund Limited (the "Fund") in the United Kingdom or in any other jurisdiction. Neither this document nor any part of it shall form the basis of or be relied on in connection with or act as an inducement to enter into any contract or commitment whatsoever.

The information contained in this document has been prepared in good faith but it is subject to updating, amendment, verification and completion. This document and any terms used herein are a broad outline of the Fund only.

The guidance is provided herein is for illustrative purposes only and does not constitute a forecast, prediction or guarantee of future performance. It should be treated with caution due to the inherent uncertainties and risks, including economic and business factors, that underpin forward looking information, particularly from a retail investor perspective.

The Fund is incorporated in Guernsey, Channel Islands and is a registered closed-ended investment scheme under the Protection of Investors (Bailiwick of Guernsey) Law, 2020, and the Registered Collective Investment Scheme Rules 2021. The Fund is not an Authorised Person under the UK Financial Services and Markets Act 2000 ("FSMA") and, accordingly, will not be registered with the FCA. The Fund will therefore only be suitable for professional or experienced investors, or those who have taken financial advice.

|

For further information:

NextEnergy Capital

|

020 3746 0700

|

|

Michael Bonte-Friedheim |

|

|

Ross Grier |

|

|

Stephen Rosser |

|

|

Peter Hamid (Investor Relations) |

|

|

RBC Capital Markets |

020 7653 4000 |

|

Matthew Coakes |

|

|

Kathryn Deegan |

|

|

Cavendish |

020 7908 6000 |

|

Robert Peel |

|

|

H/Advisors Maitland |

020 7379 5151 |

|

Neil Bennett |

|

|

Finlay Donaldson |

|

|

|

|

|

Ocorian Administration (Guernsey) Limited |

01481 742642 |

|

Kevin Smith |

|

Notes to Editors 1:

About NextEnergy Solar Fund

NextEnergy Solar Fund is a specialist solar energy and energy storage investment company that is listed on the Main Market of the London Stock Exchange.

NextEnergy Solar Fund's investment objective is to provide Ordinary Shareholders with attractive risk-adjusted returns, principally in the form of regular dividends, by investing in a diversified portfolio of utility-scale solar energy and energy storage infrastructure assets. The majority of NESF's long-term cash flows are inflation-linked via UK government subsidies.

As at 31 December 2025, the Company had an unaudited gross asset value of £997m. For further information please visit www.nextenergysolarfund.com

Article 9 Fund

NextEnergy Solar Fund is classified under Article 9 of the EU Sustainable Finance Disclosure Regulation and EU Taxonomy Regulation. NextEnergy Solar Fund's sustainability-related disclosures in the financial services sector are in accordance with Regulation (EU) 2019/2088 and can be accessed on the ESG section of both the NextEnergy Solar Fund and NextEnergy Capital websites.

About NextEnergy Group

NextEnergy Solar Fund is managed by NextEnergy Capital, part of the NextEnergy Group. NextEnergy Group was founded in 2007 to become a leading market participant in the international solar sector which now employs over 400 professionals. Since its inception, NextEnergy Group has been active in the development, construction, and ownership of solar assets across multiple jurisdictions. NextEnergy Group operates via its three business units: NextEnergy Capital (Investment Management), WiseEnergy (Operating Asset Management), and Starlight (Asset Development).

· NextEnergy Capital: has over 18 years of specialist solar expertise having invested in over 530 individual solar plants across the world. NextEnergy Capital currently manages four institutional funds with a total capacity in excess of 4GW and has funds under management of c.$4.8bn. More information is available at www.nextenergycapital.com

· WiseEnergy®: is a leading specialist operating asset manager in the solar sector. Since its founding, WiseEnergy has provided solar asset management, monitoring and technical due diligence services to over 1,600 utility-scale solar power plants with an installed capacity in excess of 3.5GW. More information is available at www.wise-energy.com

· Starlight: has developed over 100 utility-scale projects internationally and continues to progress a large pipeline of c.12GW of both green and brownfield project developments across global geographies. More information is available at www.starlight-energy.com

Notes:

1: All financial data is unaudited at 31 December 2025, being the latest date in respect of which NextEnergy Solar Fund has published financial information.

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.

Latest directors dealings

- 1 day ago Workspace Group

- 1 day ago Talon Resources Plc

- 1 day ago Vodafone Group

- 1 day ago Synthomer

- 1 day ago Ondo Insurtech