Quarterly NAV & Operational Update

Summary by AI BETAClose X

LEI: 213800ZPHCBDDSQH5447

3 June 2026

NextEnergy Solar Fund Limited

("NESF" or "the Company")

Unaudited Quarterly Net Asset Value & Operational Update

NextEnergy Solar Fund, a specialist investor in solar energy and energy storage, announces it has today published its unaudited Q4 Net Asset Value ("NAV") and Operational Update for the three-month period ended 31 March 2026.

Tony Quinlan, Chair of NextEnergy Solar Fund Limited, commented:

"This has been a very difficult period for the sector, NESF and for our shareholders. The wider renewables backdrop has been uncertain, and recent government consultations and announcements have not helped to provide the clarity the sector needs and therefore had a detrimental effect on the Company's Net Asset Value.

"We announced in March a strategic reset. To re-base the dividend policy at a sustainable but still healthy level, reduce gearing and reinvest a modest level of incremental capital into the existing portfolio, including complementary battery storage. We believe this will, over time, strengthen NESF and deliver long-term growth, unlocking opportunities within the asset base, over and above current cash flow forecasts.

Today's NAV is a technical measure, taken at a point in time, but certainly not reflecting the substantial upside optionality inherent in the portfolio."

Dividend update:

Total dividends declared of 8.43p per Ordinary Share for the twelve months ended 31 March 2026 (31 March 2025: 8.43p). Dividend cover for the twelve months ended 31 March 2026 was 1.2x (31 March 2025: 1.1x).

Following the completion of the target dividend of 8.43p for the financial year ended 31 March 2026, the Company has transitioned from a progressive dividend policy to a percentage-based dividend policy, targeting a 75% distribution of operating free cash flows, post debt servicing and portfolio and fund operating expenses.

The estimated dividend guidance range for the financial year ending 31 March 2027 is between 4.5p - 5.1p per Ordinary Share, subject to portfolio performance, which is above the estimated range previously presented during the strategic reset in March. This guidance is the equivalent to a dividend yield range of c.9% - c.11% as at 2 June 2026.

Quarterly NAV:

As of 31 March 2026, the Company's NAV was £437.5m (31 December 2025: £488.4m), representing a NAV per Ordinary Share of 76.1p (31 December 2025: 84.9p). The decline in NAV during the period was driven by several factors, including the inclusion of the ROC and FiT indexation change as previously announced. The Company's Gross Asset Value ("GAV") was £922m (31 December 2025: £997m).

|

Breakdown |

NAV per ordinary share |

NAV |

|

At 31 December 2025 |

84.9p |

£488.4m |

|

Capital movements (no net NAV impact) |

|

|

|

New assets at cost |

+0.1p |

+£0.8m |

|

Cash on hand to fund investment and RCF repayment |

-4.4p |

-£25.8m |

|

RCF reduction |

+4.3p |

+£25.0m |

|

Time value |

+0.6p |

+£3.3m |

|

Project actuals |

-0.9p |

-£4.9m |

|

Solar power price forecasts |

-0.6p |

-£3.7m |

|

BESS revenue forecasts |

0.0p |

+£0.2m |

|

Changes in short-term inflation |

+1.2p |

+£6.9m |

|

Revaluation of NextEnergy III LP investment and co-investments |

-0.5p |

-£2.7m |

|

Cash dividends paid |

-2.5p |

-£14.5m |

|

Fund operations and maintenance |

-0.3p |

-£1.5m |

|

Asset disposal |

-0.3p |

-£1.9m |

|

ROC & FiT indexation change |

-2.0p |

-£11.7m |

|

Discount rate change |

-1.6p |

-£9.2m |

|

Revaluation of development asset |

-1.3p |

-£7.7m |

|

Other movements in residual value |

-0.6p |

-£3.5m |

|

At 31 March 2026 |

76.1p |

£437.5m |

NAV movements:

Time value: The time value reflects the change in the valuation as a result of changing the valuation date, prior to adjusting for any outflows of the Company. The increase in value is attributable to the unwinding of the discount applied to cash flows for the period when calculating the discounted cash flow.

Project actuals: Q4 is typically a low-impact period for revenues due to the seasonal reduction in solar irradiation during the darker winter months. Project actuals reflect the portfolio's actual generation versus budget, with the shortfall during the Q4 period driven by lower than anticipated irradiance, which had an impact on generation over the quarter.

Solar power price forecasts: A net decrease in the UK power price forecasts provided by third-party forecasters and a decrease in REGO price forecasts. Third-party UK power price forecasts have increased in the near term due to the Middle East crisis, however, these are offset by decreasing solar capture rates from 2029 onwards due to increased forecast offshore wind and solar PV build-out as a result of the UK's 7th Allocation Round of the Contracts for Difference scheme.

BESS revenue forecasts: An increase in BESS revenue forecasts provided by a third-party consultant.

Inflation forecasts: An increase in short-term inflation assumptions up to 2030. The Company continues to take a consistent approach to its inflation assumptions, using external third-party, independent inflation data from HM Treasury Forecasts and long-term implied rates from the Bank of England for its UK assets. For international assets, IMF forecasts are used. Long-term assumptions are aligned with market consensus.

Revaluation of NextEnergy III LP and co-investments: Movements in the fair value of the holding in NextEnergy III LP and the two co-investments reflecting updates to power price and curtailment forecasts provided by third-party consultants.

Cash dividends paid: The dividends paid during the period, including both Ordinary Share and Preference Share dividend payments.

Asset disposal: As announced on 10 March 2026, NESF successfully disposed of a 100MW portfolio that raised £46.2m. The sale was comprised of two individual 50MW assets. The transaction represented a 1.1x multiple on invested capital. The disposal price was just below the assets' combined valuation.

ROC and FiT indexation change: As previously announced by the Company on 28 January 2026, the UK Government confirmed it has switched to CPI indexation from RPI effective from April 2026. This has a direct impact on the ROC buy-out prices and FiT prices that the Company receives as part of its subsidised revenue streams, impacting its future cash flows.

Discount rate change: An increase of 50bps used for UK unlevered projects to 8.00% (31 December 2025: 7.50%) driven by recent market volatility, increases in UK gilt yields and an increased cost of capital due to retroactive changes to the ROC and FiT schemes.

Revaluation of development asset: The revaluation reflects an adjustment to the open‑market valuation of a development asset. The Company has entered a phase of exclusive negotiations for the disposal of this asset with the objective of crystallising value from a non-yielding asset and recycling capital to repay debt.

Other residual value movements: Includes FX movements, incremental capex forecasts, planned outages, difference between forecast and actual tax payments plus changes to tax legislative rates and other immaterial changes.

Government policy changes:

Post period, the UK Government announced several initiatives that have affected the Company. Firstly, the removal of Carbon Price Support ("CPS") with effect from April 2028. As already indicated by the Company here, the removal of CPS in 2028 would have an impact on the electricity price assumptions used in NESF's NAV model. The updated assessment is that the removal of CPS will potentially reduce the Company's NAV as at 30 June 2026 by 0.0p - 0.8p per Ordinary Share, although the Company's Investment Adviser, NextEnergy Capital, expects this impact to be towards the lower end of that range.

Secondly, the UK Government announced changes to the Electricity Generator Levy, a tax on excess generation revenues. Although the Company falls within the scope of this levy, the current tax threshold is set at a level above that at which the Company has hedged power prices. This change is therefore not expected to affect the Company.

Thirdly, the UK Government announced a public consultation on Wholesale Contracts for Difference. These are a newly proposed voluntary long-term fixed-price contract that the UK Government plans to offer existing low-carbon electricity generators that are not already on a traditional Contract for Difference (notably, Renewables Obligation assets). This approach could help address a long-standing issue in how electricity prices are set, particularly as low-cost renewable generators make up a larger share of the UK's power supply. The proposed voluntary Wholesale Contracts for Difference would give renewable generators the option to exchange exposure to volatile wholesale prices for a long-term fixed price, potentially delivering lower and more stable energy costs for consumers alongside predictable, inflation-linked income for investors. Importantly, participation would be voluntary, not mandatory, and the Company would only take part where it believed that it was in the best interests of its shareholders.

Gearing:

As at 31 March 2026, total gearing1, including Preference Shares, was 51.2% (31 December 2025: 49.9%). While this is above the Company's 50% debt to GAV target, the increase was driven by the reduction in NAV relative to existing debt, rather than any additional debt drawdown.

Exceeding the 50% target does not impact the terms or covenants of the Company's debt facilities, it simply restricts the Company from drawing further debt, which it does not intend to do. As set out in the Company's recently published strategic reset and roadmap, NESF is targeting further asset sales to reduce gearing to a range of 40% - 45%.

The Company is already in the advanced stages of its first asset disposal under the extended Capital Recycling Programme, with proceeds expected to be used to make further repayments of the revolving credit facility ("RCF").

The enterprise value gearing ratio applied to the Preference Shares held by USS was 61.8% (31 December 2025: 60.1%). As outlined in the interim results, this does not impact the Company's current operations or the delivery of its strategic reset and roadmap. The Company continues to engage constructively with USS to identify a long-term solution to the current 50% limit and remains focused on closing the share price discount to NAV.

Since 1 April 2025, the Company has paid down approximately £12.9m of its long-term amortising debt (31 December 2025: £8.0m). The remaining outstanding long-term debt of £134.3m is on track to fully amortise in line with the remaining subsidy life of the portfolio's inflation-linked government subsidies.

In addition, the Company reduced the size of its RCF from £205m to £170m, supporting efficient treasury management.

|

Debt facilities as at 31 March 2026 |

Size (£m) |

Amount outstanding (£m) |

|

Long-term amortising debt |

£212.5m |

£134.3m |

|

Short-term RCF |

£170.0m |

£126.9m |

|

Total financial debt |

|

£261.2m |

|

Preference shares |

£200.0m |

£198.6m |

|

Total debt |

|

£459.8m2 |

Operational update:

The Company has 99 operating solar and energy storage assets3 (31 December 2025: 101) with a total installed capacity of 838MW4 (31 December 2025: 939MW). The assets have a remaining weighted life of 22.3 years (31 December 2025: 24.0 years).

During the period, generation performance for NESF's UK and Italian assets was -10.9% versus budget (31 December 2025: -12.9%). The shortfall was driven mainly by lower-than-expected solar irradiance of -9.0% (31 December 2025: -9.3%) and localised availability impacts during the period. As a reminder, this period is typically a low-impact quarter for the Company's revenues due to the seasonality of solar generation, with the darker winter months normally resulting in reduced irradiation and lower operational performance. The full year generation performance has been positive against budget due to the portfolio performance across the summer months in 2025.

The Company continues to run a proactive hedging strategy on its non-subsidised revenues to minimise risk and lock in future cash flows. The table below shows the hedged position using Power Purchase Agreements ("PPAs") of the 676MW UK NESF portfolio as at 31 March 2026.

|

|

FY25/26 |

FY26/27 |

FY27/28 |

|

Hedged (by capacity) % |

100.0% |

78.3% |

15.4% |

|

Weighted average hedged PPA Price £/MWh |

£79.72 |

£71.04 |

£70.00 |

The Company captured some near-term upsides from the wholesale market volatility in response to the conflict in the Middle East in the period and continues to lock in further power price hedges on a monthly basis as they become liquid.

Strategic Reset:

On 11 March 2026, the Company announced the outcome of the Board's comprehensive review and its strategic reset, which establishes a clear set of actions within the control of the Board and the Investment Adviser. The Company's strategic reset is focused on capturing the intrinsic value of its high-quality, cash-generative portfolio, with a clear objective of stabilising and growing NAV over the long term while strengthening the balance sheet.

The Board believes that the current share price discount does not reflect the underlying value and potential of NESF's diversified portfolio of long-life solar and energy storage assets, which continue to deliver resilient operational performance and stable cash flows. In response, the Company has taken decisive action to unlock value embedded within the portfolio which is not reflected in the current share price and NAV. This approach is designed to enhance total returns, support a sustainable dividend, and position the Company to benefit from a future market recovery and structural growth opportunities in solar and energy storage.

The key value creation levers underpinning this strategy are:

Crystallising and recycling embedded portfolio value:

- Targeted asset disposals under the expanded Capital Recycling Programme (up to 120MW) to realise value.

- Realisation of private fund investment and co-investments to generate additional capital for reinvestment.

- Track record of successful disposals demonstrating the ability to crystallise NAV and redeploy capital efficiently

.

Reinvesting capital into higher-return opportunities:

- Deployment of capital into higher-yielding assets, including energy storage and repowering projects.

- Reallocation of capital towards opportunities that enhance long-term NAV growth and total return potential.

- Increasing exposure to energy storage (target c.30% of GAV5) to diversify and strengthen portfolio returns.

Enhancing value from the existing portfolio:

- Repowering assets to increase generation efficiency, extend asset life and drive NAV uplift.

- Active asset management and cost optimisation initiatives to improve operational performance and cash flow generation.

- Leveraging existing grid connections and infrastructure to deliver capital-efficient growth.

Strengthening financial resilience and flexibility:

- Transition to a 75% dividend payout ratio to retain capital and support reinvestment.

- Targeting a reduction in gearing to 40% - 45% of GAV through disciplined capital allocation.

- Prioritisation of debt reduction to enhance balance sheet strength and reduce financing risk.

Delivering sustainable long-term returns:

- Targeting total returns of 9% - 11% through a combination of income and NAV growth.

- Creating a clear pathway to stabilise NAV and deliver long-term compounding value for shareholders.

- Positioning the Company to benefit from a recovery in market conditions and a narrowing of the discount to NAV over time.

Capital Recycling Programme:

The final phase of the initial Capital Recycling Programme was successfully completed in the period with two assets with an installed capacity of 100MW being sold to a third party. This concluded the initial Capital Recycling Programme where five solar assets totalling 245MW were recycled to raise c.£119m in total capital, which added a total NAV uplift of 2.44p per Ordinary Share.

As per the strategic reset announcement in March, the Company has identified an additional 120MW of assets for disposal over the next 36 months.

The Investment Adviser has identified the next assets for disposal and is progressing discussions with potential buyers.

ESG & Sustainability:

Sustainability remains a core component of the Company's strategy, values and culture. The Company continues to maintain its Article 9 Fund classification under the EU Sustainable Finance Disclosure Regulation ("SFDR") and the EU Taxonomy Regulation. The Company and its Investment Adviser continue to deliver initiatives under the Approach to Nature strategy, supporting biodiversity enhancements across NESF sites, and remain active in promoting supply-chain sustainability, including through ongoing participation in the Solar Stewardship Initiative.

Ross Grier, Chief Investment Officer of NextEnergy Capital said:

"Whilst NESF's share price discount has remained stubbornly wide, the underlying assets themselves continue to demonstrate the resilience and quality you would expect from a portfolio deployed by a specialist solar and energy storage investment manager with funds managed totalling over $4.8 billion and nearly two decades of renewables experience.

"It has been a difficult time for the sector, as UK Government consultations on subsidy reform created uncertainty and medium and long-term power price forecasts continue to soften. Against this backdrop, the NESF Board's Strategic Reset represents, in our assessment, the best available option to pursue: stabilising the balance sheet, putting the dividend on a sustainable footing, and critically, making the portfolio more attractive to the widest range of possible investors.

"We continue to believe firmly in the role of investment companies as the right structure for holding these long-dated, renewable infrastructure assets, and in the long-term investment case for UK solar and energy storage, where policy tailwinds around Clean Power 2030, CfD extensions, voluntary wholesale CfDs, and growing electricity demand are beginning to strengthen.

"In light of this ever-evolving landscape, the Board has set out a capital allocation framework within the strategic reset. The framework is designed to be dynamic and responsive based on market conditions. Currently, we are fully concentrated on NESF debt repayment as the near-term priority. Following the delivery of the strategic reset, having outlined strong indicative guidance and removed a level of uncertainty from the future of the platform, we are actively engaging with both existing NESF shareholders and prospective investors to drive renewed demand for the shares."

Key assumptions:

Inflation Rate (UK RPI) Assumptions

|

Calendar Year |

31 March 2026 |

31 December 2025 |

|

2026/27 |

4.60% |

3.10% |

|

2027/28 |

3.30% |

3.20% |

|

2028/29 |

3.10% |

3.20% |

|

2029/30 |

3.00% |

3.10% |

|

2030/31 |

2.80% |

2.25% |

|

Onwards |

Unchanged |

2.25% |

Inflation Rate (UK CPI) Assumptions

|

Calendar Year |

31 March 2026 |

31 December 2025 |

|

2026/27 |

3.60% |

2.20% |

|

2027/28 |

2.20% |

2.20% |

|

2028/29 |

2.20% |

2.20% |

|

2029/30 |

2.10% |

2.10% |

|

2030/31 |

2.00% |

2.25% |

|

Onwards |

Unchanged |

2.25% |

Discount Rate Assumptions

|

|

|

31 March 2026 |

31 December 2025 |

|

Solar |

UK unlevered |

8.00% |

7.50% |

|

UK levered |

8.70% - 9.00% |

8.20% - 8.50% |

|

|

Italy unlevered6 |

9.50% |

9.00% |

|

|

Subsidy-free (uncontracted)7 |

9.00% |

8.50% |

|

|

Life extensions8 |

9.00% - 10.00% |

8.50% - 9.50% |

|

|

Energy Storage |

Uncontracted |

Unchanged |

10.00% |

|

Contracted |

Unchanged |

7.00% |

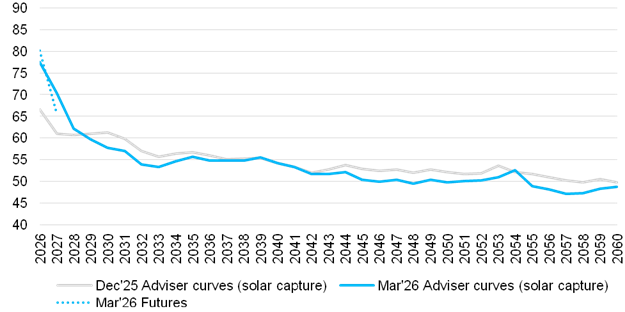

Power Curve Assumptions

31 March 2026: Blended Simple Average Power Curves (Capture Price)

Methodology: For the UK portfolio, the Company uses multiple sources for UK power price forecasts. Where power has been sold at a fixed price under a Power Purchase Agreement (or PPA) (a hedge), these known prices are used. For periods where no PPA hedge is in place, short-term market forward prices are used. After two years, the Company integrates an equal weighted average of leading independent energy market consultants' long-term central case projections. The blend of forecasts reduces volatility, presenting a fair and balanced outlook consistent with pricing methodologies used for successfully divested assets and power price assumptions across the broader peer group.

For the Italian portfolio, PPAs are used in the forecast where these have been secured. In the absence of hedges, a leading independent energy market consultant's long-term projections are used to derive the power curve adopted in the valuation.

Footnotes:

1. Total gearing is the aggregate of financial debt, and £200m of preference shares. The preference shares are equivalent to non-amortising debt with repayment in shares. Excludes total look-through debt of £24.3m since the Company does not have control over this debt for NAV based investments.

2. Excludes total look-through debt of £24.3m.

3. Excluding the $50m commitment into private vehicle NextEnergy III LP ("NEIII", formerly "NextPower III LP" or "NEIII").

4. Including share in private equity vehicle NEIII and co-investments (Agenor and Santarém). Inclusion of NESF's 6.21% share of NEIII on a look-through equivalent basis increases total capacity by 48MW (31 December 2025: 46MW). Inclusion of NESF's 24.5% share of Agenor increases total capacity by 12MW (31 December 2025: 12MW). Inclusion of NESF's 13.6% share of Santarém on a look-through equivalent basis increases total capacity by 29MW (31 December 2025: 29MW).

5. Subject to shareholder approval at the Company's upcoming AGM.

6. Unlevered discount rate for Italian operating assets implying 1.50% country risk premium to 8.0%.

7. Unlevered discount rate for subsidy-free uncontracted operating assets implying 1.0% risk premium to 8.0%.

8. 1.0% risk premium added to UK unlevered (8.00%) and UK levered assets (8.70% - 9.00%) for cash flows after 30 years where leases have been extended.

| End |

This announcement has been made by the Board of NextEnergy Solar Fund, the Investment Adviser, NextEnergy Capital Limited, and the Investment Manager, NextEnergy Capital IM Ltd, in good faith based on the information available to them at the time of this announcement.

This document is issued by NextEnergy Capital Limited ("NEC"), which is authorised and regulated by the UK Financial Conduct Authority ("FCA") with registered number 471192.

This document is not an offer to sell, or a solicitation of an offer to acquire, securities of the NextEnergy Solar Fund Limited (the "Fund") in the United Kingdom or in any other jurisdiction. Neither this document nor any part of it shall form the basis of or be relied on in connection with or act as an inducement to enter into any contract or commitment whatsoever.

The information contained in this document has been prepared in good faith but it is subject to updating, amendment, verification and completion. This document and any terms used herein are a broad outline of the Fund only.

The guidance is provided herein is for illustrative purposes only and does not constitute a forecast, prediction or guarantee of future performance. It should be treated with caution due to the inherent uncertainties and risks, including economic and business factors, that underpin forward-looking information, particularly from a retail investor perspective.

The Fund is incorporated in Guernsey, Channel Islands and is a registered closed-ended investment scheme under the Protection of Investors (Bailiwick of Guernsey) Law, 2020, and the Registered Collective Investment Scheme Rules 2021. The Fund is not an Authorised Person under the UK Financial Services and Markets Act 2000 ("FSMA") and, accordingly, will not be registered with the FCA. The Fund will therefore only be suitable for professional or experienced investors, or those who have taken financial advice.

|

For further information:

NextEnergy Capital

|

020 3746 0700

|

|

Michael Bonte-Friedheim |

|

|

Ross Grier |

|

|

Stephen Rosser |

|

|

Peter Hamid (Investor Relations) |

|

|

RBC Capital Markets |

020 7653 4000 |

|

Matthew Coakes |

|

|

Kathryn Deegan |

|

|

Cavendish |

020 7908 6000 |

|

Robert Peel |

|

|

H/Advisors Maitland |

020 7379 5151 |

|

Neil Bennett |

|

|

Finlay Donaldson |

|

|

|

|

|

Ocorian Administration (Guernsey) Limited |

01481 742642 |

|

Kevin Smith |

|

Notes to Editors 1:

About NextEnergy Solar Fund

NextEnergy Solar Fund is a specialist solar energy and energy storage investment company that is listed on the Main Market of the London Stock Exchange.

NextEnergy Solar Fund's investment objective is to provide Ordinary Shareholders with attractive risk-adjusted returns, principally in the form of regular dividends, by investing in a diversified portfolio of utility-scale solar energy and energy storage infrastructure assets. The majority of NESF's long-term cash flows are inflation-linked via UK government subsidies.

As at 31 March 2026, the Company had an unaudited gross asset value of £922m. For further information please visit www.nextenergysolarfund.com

Article 9 Fund

NextEnergy Solar Fund is classified under Article 9 of the EU Sustainable Finance Disclosure Regulation and EU Taxonomy Regulation. NextEnergy Solar Fund's sustainability-related disclosures in the financial services sector are in accordance with Regulation (EU) 2019/2088 and can be accessed on the ESG section of both the NextEnergy Solar Fund and NextEnergy Capital websites.

About NextEnergy Group

NextEnergy Solar Fund is managed by NextEnergy Capital, part of the NextEnergy Group. NextEnergy Group was founded in 2007 to become a leading market participant in the international solar sector which now employs over 400 professionals. Since its inception, NextEnergy Group has been active in the development, construction, and ownership of solar assets across multiple jurisdictions. NextEnergy Group operates via its three business units: NextEnergy Capital (Investment Management), WiseEnergy (Operating Asset Management), and Starlight (Asset Development).

- NextEnergy Capital: has over 19 years of specialist solar expertise having invested in over 530 individual solar plants across the world. NextEnergy Capital currently manages four institutional funds with a total capacity in excess of 4GW and has funds under management of c. $4.8bn. More information is available at www.nextenergycapital.com

- WiseEnergy¨: is a leading specialist operating asset manager in the solar sector. Since its founding, WiseEnergy has provided solar asset management, monitoring and technical due diligence services to over 1,600 utility-scale solar power plants with an installed capacity in excess of 3.5GW. More information is available at www.wise-energy.com

- Starlight: has developed over 100 utility-scale projects internationally and continues to progress a large pipeline of c.9GW of both green and brownfield project developments across global geographies. More information is available at www.starlight-energy.com

Notes:

1: All financial data is unaudited at 31 March 2026, being the latest date in respect of which NextEnergy Solar Fund has published financial information.

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.

Latest directors dealings

- 2 days ago TotalEnergies SE

- 2 days ago Bango

- 2 days ago Zigup

- 2 days ago PureTech Health

- 2 days ago Peel Hunt Limited NPV