Admission to AIM & First Day of Dealings

Summary by AI BETAClose X

Mendell Helium plc

("Mendell Helium" or the "Company")

Admission to Trading on AIM and First Day of Dealings

Mendell Helium, the helium production company with operations in Kansas, is pleased to announce that the admission of its ordinary shares of 1 pence each ("Ordinary Shares") to trading on the AIM Market ("AIM"), a market operated by the London Stock Exchange, will take place today ("Admission").

Dealings in the Ordinary Shares on AIM will commence at 8:00 a.m. today under the TIDM "MDH" and the ISIN GB00BLD3FF28.

Additionally, the Company's Ordinary Shares will be withdrawn from trading on the Access Segment of the Aquis Stock Exchange Growth Market with effect from 8.00 a.m. 30 June 2026, in accordance with AQSE Rule 5.3.

Mendell Helium is a helium producer in Kansas, USA where it operates in Fort Dodge, just to the east of Dodge City, and in the Hugoton gas field in South-Western Kansas, one of the largest natural gas fields in North America. It is Fort Dodge where the Company focuses its activities and where it plans up to four further wells. With a 5.1% helium composition, the Company's flagship well, Rost 1-26, has a recorded flow rate of 250 Mcf per day. This has become the blueprint for future expansion in the Fort Dodge region. The Company's Admission Document and information required pursuant to AIM Rule 26 is available on the Company's website at https://mendellhelium.com.

Part 1 of the Admission Document is set out in the Appendix below.

Nick Tulloch, CEO of Mendell Helium, said:

"We are delighted to begin trading on AIM today. As we advance our significant development programme in Fort Dodge, Kansas, this marks the right moment to join a globally recognised growth market that aligns with our long-term ambitions.

"We are supported by an exceptionally committed and talented team, and while there is considerable work ahead as we execute our plans, the foundations for growth are firmly in place. The success of the Rost 1-26 well has validated our strategy, and our extensive land position provides a strong platform from which to expand our operations.

"I would like to thank our shareholders and advisers for their continued support and confidence in Mendell Helium. As we enter this exciting new phase of growth, we look forward to keeping the market updated as our programme of new wells progresses over the coming months."

This announcement contains inside information for the purposes of the UK Market Abuse Regulation and the Directors of the Company are responsible for the release of this announcement.

ENDS

Engage with the Mendell Helium management team directly by asking questions, watching video summaries and seeing what other shareholders have to say. Navigate to our Interactive Investor website here: https://mendellhelium.com/link/PKa6Ve

Enquiries:

|

Investor questions on this announcement We encourage all investors to share questions on this announcement via our investor website

|

||

|

Mendell Helium plc Nick Tulloch, CEO

|

Via our website investors@mendellhelium.com |

|

|

Cairn Financial Advisers LLP (AQSE Corporate Adviser) Ludovico Lazzaretti / Liam Murray

|

Tel: +44 (0) 20 7213 0880 |

|

|

SI Capital Limited (Broker) Nick Emerson

|

Tel: +44 (0) 1483 413500 |

|

|

Fortified Securities Guy Wheatley

|

Tel: +44 (0) 203 4117773

|

|

|

Tel: +44 (0) 20 3973 3678 |

|

|

AlbR Capital Limited Gavin Burnell / Colin Rowbury / Jon Belliss

|

Tel: +44 (0) 207 4690930

|

|

|

Brand Communications (Public & Investor Relations) Alan Green |

Tel: +44 (0) 7976 431608

|

Overview of Mendell Helium

Mendell Helium is a helium producer in Kansas, USA where it operates through its wholly owned subsidiary M3 Helium.

M3 Helium's flagship well, Rost 1-26, is in Fort Dodge, just to the east of Dodge City, Kansas. It has been tested as containing 5.1% helium composition and a drill stem test yielded a maximum flow rate of approximately 2,900 Mcf per day. Water removed from Rost 1-26 is delivered to Brobee, a nearby disposal well that has been permitted at 10,000 barrels of water per day at 1,200 psi. Production at Rost 1-26 commenced in early November 2025 and the most recently recorded flow rate in December 2025 was 250 Mcf per day equating to approximately $1.4 million of helium per year (at $300/Mcf helium).

M3 Helium has subsequently drilled a second well, Rost 2-26, which is currently being completed. It also owns additional leases in the Fort Dodge area capable of supporting up to eight new production wells. It has also agreed a joint venture with Ritchie Exploration, Inc. to recomplete the Schneweis Ventures 13A, a well with a drill stem test of over 10,000 Mcf per day and a historic flow rate of 300 Mcf per day.

At the Rost wells in Fort Dodge, M3 Helium treats the raw gas on site to concentrate the helium and has leased two tube trailers which it uses for deliveries to its offtaker.

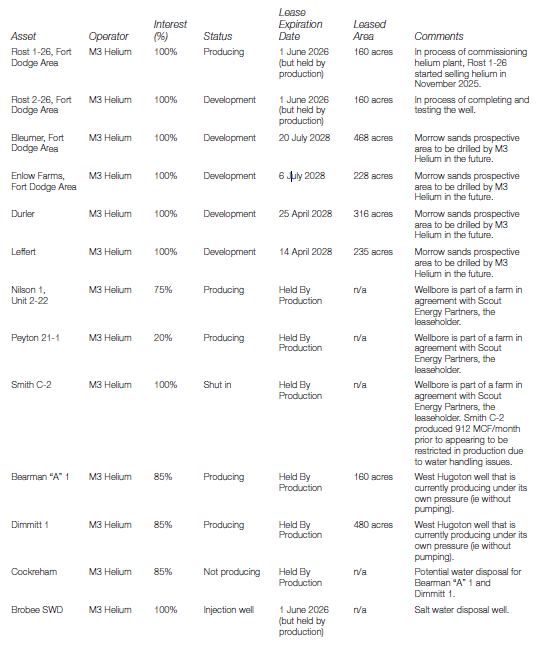

M3 Helium also has interests in five producing wells (Peyton, Smith, Nilson, Bearman and Dimmitt) within the Hugoton gas field in South-Western Kansas, one of the largest natural gas fields in North America. Significantly these wells are in the proximity of a gathering network and the Jayhawk gas processing plant meaning that producing wells are all tied into the infrastructure.

Appendix:

1. Introduction

Mendell Helium plc ("Mendell" or the "Company") (formerly Voyager Life plc) was incorporated as a private limited company on 12 November 2020 under the laws of Scotland with company number SC680788. The Company re-registered as a public limited company on 7 June 2021 and listed on the Access segment of AQSE on 30 June 2021.

On 18 May 2026, Mendell acquired the entire issued share capital of M3 Helium Corporation ("M3 Helium"), a helium producer and exploration company based in Kansas, USA. M3 Helium was incorporated to pursue helium production opportunities. It has interests in twelve wells, of which six (Rost 1-26, Peyton 21-1, Nilson 1 Unit 2-22, Smith, Bearman "A"1 and Dimitt 1) are in production. The Company issued 57,611,552 new Ordinary Shares to the Sellers in consideration for the transfer to the Company of the entire issued share capital of M3 Helium.

Helium (He) is an inert, non-renewable gas created by the natural decay of radioactive elements and primarily produced as a byproduct of natural gas production. Due to its unique physical properties, including low boiling point and non-reactivity, helium is a critical input across a range of advanced industries such as medical imaging, semiconductors, aerospace and fibre optics. Global helium demand was estimated at approximately 6 billion cubic feet (Bscf) in 2023 and is projected to grow to 8.7 Bscf by 2030.

Since entering into the M3 Helium Option in 2024, the Company has completed a number of fundraisings, and, in each case, has applied the net proceeds towards the continued development of M3 Helium's business by providing loans to M3 Helium. At the date of the Acquisition, the aggregate amount outstanding under these loans was US$2.35 million including accrued interest and, following completion of the Acquisition, they are treated as intra-group loans. The Directors considered this strategy to be of benefit to Shareholders given the significant change in M3 Helium's business since the M3 Helium Option was entered into, and specifically the success of the helium production operations at Fort Dodge. The acquisition of M3 Helium represented a significant strategic shift and is expected to provide the Company with access to the growing helium exploration and production sector.

The number of Ordinary Shares in issue as at the date of this Document is 340,761,938 and the number of outstanding options, warrants and CLNs to subscribe for new Ordinary Shares is 34,750,618, 109,658,799 and 9,333,333 respectively. The Directors believe that Admission to AIM will better position the Company to pursue growth opportunities within the helium sector, while providing greater access to capital and an enhanced profile among institutional investors.

It is expected that Admission will become effective and dealings in the Share Capital will commence on AIM on or around 16 June 2026. Following Admission to AIM, the Company will cancel the trading of its Ordinary Shares on AQSE. The last day of dealings on AQSE is expected to be 29 June 2026, with the AQSE Cancellation becoming effective at 8.00 a.m. on 30 June 2026.

You should read the whole of this Admission Document and not just rely upon the information contained in this Part I. In particular, you should carefully consider the Risk Factors set out in Part II of this Admission Document. Your attention is also drawn to the information set out in Parts III to VII of this Admission Document.

2. Investment Case

The Directors of Mendell believe that the Group's key strengths can be summarised as follows:

Innovative technique for accessing gas reservoirs

M3 Helium's primary operations are in Fort Dodge, Kansas where it employed an unconventional technique to significantly de-water a previously drilled but shut in gas well to bring it back to production. This well is Rost 1 where, during the course of 2025, M3 Helium employed an electric submersible pump and completed a nearby disposal well to move, initially, around 1,800 barrels of water per day. These operations were successful and commercial production of helium commenced in November 2025, albeit the well has not produced consistently since then, due to equipment maintenance and development of surface facilities. Rost 1 is an important milestone for M3 Helium as the well has been tested at a helium composition of 5.1 per cent. and a drill stem test indicating flow rates of up to 2,940 MSCF/D. In November 2025 flow rates were measured at 250 MSCF/D.

The Fort Dodge region has existing oil and gas operations with several wells showing the presence of helium. However, the Morrow Sands formation, which the Company believes is the optimum production zone, requires significant de-watering to generate production. This has deterred other operators but, through Rost 1, Mendell Helium has demonstrated that it has found a commercial solution to access what it believes is a reservoir rich in helium.

Rost 1 is connected to a nearby salt water disposal well, Brobee, where water that is pumped from Rost 1 is delivered. This is an essential part of the operations as trucking water from site would be uneconomic. The water disposal capacity available at Brobee is expected to be materially greater than that required under current production for Rost 1. As a result, Brobee may be further modified to accommodate water production from offset wells in the Fort Dodge area, including through access to deeper formations.

Furthermore, the Directors believe that this dewatering approach that has been employed at Rost 1 can be repeated across multiple other locations.

Low risk producing asset base

M3 Helium currently has six producing wells. Five of these producing wells are within the Hugoton gas field, one of the largest natural gas fields in North America - the fifth well, Smith C-2, is shut-in pending the drilling of a nearby disposal well. These wells benefit from proximity to established midstream infrastructure, including a gas gathering network and the Jayhawk gas processing plant, enabling production to be tied directly into that infrastructure. The Jayhawk gas processing plant is a major natural gas and helium processing facility located near Ulysses, Kansas, and is a key piece of midstream infrastructure in the Hugoton gas field using cryogenic processes and purification methods including pressure swing adsorption ("PSA"). The plant processes raw natural gas to extract methane, helium, nitrogen, and natural gas liquids, with some of its operations directly connected to the Federal Helium Pipeline.

Although the Company's focus in the near term will be on the development of the Fort Dodge region, its Hugoton operations provide a low maintenance and long term production base to its operations. In time these may be further developed through the addition of disposal wells to increase water removal and thereby gas production but there are no immediate plans in this regard.

Access to infrastructure

It is a fundamental part of the Company's strategy that its production wells have access to the market for helium. The helium market is immature and most sales are through bilateral agreements and not on the spot market. Furthermore, helium is challenging to contain and transport. Helium is often extracted as a minority part of a gas mixture and needs to be separated and purified.

All of M3 Helium's producing wells in the Hugoton are connected to the gathering system for the Jayhawk processing plant. In Fort Dodge, at present, helium production is being delivered by tube trailer under a tolling agreement. Over the medium term, the Directors consider that the success of Rost 1, and potentially other producing wells in the Fort Dodge area, may support the economic case for the construction of a pipeline connection to nearby gas gathering infrastructure.

Unprecedented short supply and increasing demand underpinning strong pricing

Helium is a vital element for a number of major technologies utilised on a daily basis, however the ability of existing and planned sources of helium supply to meet future demand is highly uncertain. A number of factors have come together to create a precarious situation, starting with the 1996 decision by the US government to sell off nearly its entire stockpile of helium, stored in a depleted natural gas field in Amarillo, Texas. This created an increase in supply and prices of helium have arguably been artificially depressed for much of the last decade. Until a few years ago, this facility was the only place in the world to store helium.

In addition to the depletion of the US government helium reserve, lower oil and gas prices have caused the cancellation or significant delay of a number of major energy projects. Helium has historically been produced as a by-product in a few large conventional oil & gas projects, which happened to have a high helium content. Many projects of this type with helium potential have been cancelled in the last few years, as they have been replaced by spending on oil & gas production from shale, which cannot generally trap or produce significant quantities of helium. As at the date of this Document, there are insufficient major projects under development in North America that could fully replace the loss of helium supply from US government stockpile sales. Recent shortages have made existing helium demand less elastic and quickly-maturing new sources of helium demand could increase the rate of demand growth. From new low-cost reusable rockets for space launches, to the advancement of nuclear fusion, to autonomous floating Internet infrastructure, to new therapies targeting cancer cells with ion beams, helium's unique physical properties make it increasingly vital to present and future technologies.

Five major fields/facilities supply around 80 per cent. of global upstream helium. A similar number of large players control the distribution, which is often executed on privately negotiated contracts. Data on current supply/demand/prices are therefore not widely disclosed and create uncertainty around precise estimates. Furthermore, existing helium supply is structurally fragile, as an outage of one of the (limited number of) suppliers could have disproportionate effects.

The helium market is also influenced by geopolitical factors. Qatar is one of the biggest suppliers globally and deliveries have been disrupted as a result of the 2026 Iran war in the Middle East at the date of this Document. Russia's significant helium reserves have been constrained by ongoing sanctions.

The Company expects a continued increase in demand underpinned by the lack of substitutes for helium in its main markets of MRIs and high-end science/engineering, including rapid growth in state-funded/private space exploration, pressure/purge applications and rising demand for semiconductors. A shortage in the early part of the last decade forced price spikes incentivising new supply (based on LNG plant start-ups), driving prices back to more normal levels. The Directors believe current supply constraints should continue to support pricing and may support marked increases.

Further detail on the global helium market can be found in paragraph 5 of Part I of this Document.

Support from local investors

On 9 December 2025, the Company announced that M3 Helium was approached by a group of US based investors (the "Investor Group") who expressed interest in supporting its expansion of Fort Dodge. Direct investments in oil & gas wells are common in the US and, if structured correctly, can attract certain tax benefits for US investors. For the Company, a direct investment at the asset level does not result in equity dilution for shareholders and provides a means of accelerating development plans, albeit with economic interests in individual wells shared with co-investors.

As announced on 16 April 2026, the Company entered into a series of binding agreements with Rixford in relation to the development of Rost Twin:

- Rixford is funding 35 per cent. of the expected cost of the Rost Twin and the upgrade of the Brobee salt water disposal well, being US$372,000 in aggregate.

- M3 Helium act as operator of the Rost Twin.

- Production from the Rost Twin will be processed at M3 Helium's facility at Rost 1, in return for which M3 Helium will earn a processing fee equal to 20 per cent. of gross production from the Rost Twin.

- Rixford has an option to acquire a 50 per cent. interest in the processing facility at development cost and, if it elects to do so the processing fee would cease.

- Rixford has been granted a right of first refusal to participate in up to five future wells drilled by M3 Helium or its affiliates in Kansas on substantially the same terms as the Rost Agreements.

- Pursuant to the Rost Agreements, Rixford has been granted a 35 per cent. working interest in the Rost Twin well.

M3 Helium has drilled the Rost Twin with a 7 inch casing (as opposed to the Rost 1 well which was drilled using a 5.5 inch casing). The larger casing will increase volume by approximately 62 per cent. enabling greater water removal. Evidence both from Rost 1 and also analogous wells in the same formation indicate a correlation between water removal and gas production. M3 Helium therefore believes this wider casing, coupled with an electric submersible pump, could enable the Rost Twin to be more productive than Rost 1.

Development of the Fort Dodge region

M3 Helium has been mapping out the formation to which the Rost 1 well has access. M3 Helium has leased further land (Bleumer and Enlow Farms) for possible future wells and it expects to continue to lease additional suitable locations as part of the Company's longer term strategy. As part of this strategy, M3 Helium has also been examining the location of gas pipelines. Although there is no gathering system directly proximate to Rost 1, there are nearby options that, should M3 Helium have several wells in production, may be economic to connect to in the future. Delivery of production via a pipeline negates the need for surface purification facilities and could enable sales of other components in the produced gases as well as helium.

Partnership with a Kansas-based oil & gas company

The Company announced on 25 March 2026 that M3 Helium has entered into a well workover agreement with Ritchie, a family-owned oil and gas operator headquartered in Wichita, Kansas, to re-complete the Schneweis well in the Fort Dodge region of Kansas, a well located around four miles south of Rost 1. M3 Helium believes that the Rost 1 de-watering technique could be employed elsewhere in the Fort Dodge region and, towards the end of 2025, it commenced discussions with Ritchie to recomplete Schneweis. A significant advantage of this method of expansion is that existing wells have evidenced prior flow rates and gas compositions. The parties have entered into a binding contract and work on Schneweis commenced in May 2026 following design and approval of the new disposal well that will be required for the project.

Schneweis has previously produced consistently over 300 MSCF/D before production was shut down due to significant water production. As with Rost 1 and the Rost Twin, the target formation is the Morrow Sands. With a sustained de-watering programme and noting that Schneweis' drill stem test in 2022 exceeded 10,000 MSCF/D, the Company believes there is potential to increase production at Schneweis from historic levels.

Helium composition has been measured at 1.39 per cent. but, unlike Rost 1, there is a higher methane content of 70.06 per cent. Significantly Schneweis is connected to a pipeline owned by Ritchie and it is envisaged that all produced gas from the well will be delivered to that pipeline with no requirement for prior treatment. Accordingly, the economics of the well will include the sale of hydrocarbons as well as helium.

The Company will fund the new disposal well and recompletion of Schneweis to earn an initial 85 per cent. net profit interest in Schneweis. Once Mendell Helium has recovered 110 per cent. of its investment, its net profit interest falls to 70 per cent. Ritchie is entitled to bring the arrangement between the parties to an equal (50 per cent.) net profit interest by reimbursing the Company for 50 per cent. of the Schneweis recompletion costs.

If the Schneweis project is successful, the Company believes that there may be further opportunities to collaborate with Ritchie and other local operators to recomplete existing oil and gas wells.

Experienced and Balanced Management Team

The Directors have considerable expertise in the helium sector, wider oil and gas industry and the UK public markets.

M3 Helium founder Paul Mendell has enjoyed a long and successful career developing natural resources projects in the US, and has developed a significant network within the helium space. Nick Tulloch previously served as adviser to, and then Finance Director and Chief Executive Officer of, UK-listed natural resources developer Highlands Natural Resources plc (now Chill Brands Group plc) where Mr Mendell was chairman. Eric Boyle was a co-founder of Highlands Natural Resources plc and retained a role with that company for around six years.

John Brown has more than 25 years of international experience in oil and gas and related industries, working for numerous UK listed companies including San Leon Energy plc, Gulf Marine Services plc, Bowleven plc and Pittencrieff Resources plc.

Through Mr Mendell's geological expertise, Mr Tulloch's legal qualification, Mr Brown formerly working as a Chartered Accountant and Mr Boyle's career in asset management, the Directors therefore believe that this mix of relevant technical, operational and financial experience means that Mendell Helium's Board is ideally suited to deliver value for shareholders. Furthermore, the Directors have assembled a senior management team with extensive experience of the oil & gas industry in Kansas, thereby providing local knowledge and connections.

3. Strategy

During 2025 M3 Helium re-completed Rost 1 in Fort Dodge, Kansas. With a recorded flow rate of 250 Mcf/day and a helium composition of 5.1 per cent. within the gas stream, the operation was successful and M3 Helium has more recently drilled a twin well 330 feet from Rost 1 - the Rost Twin. In both cases, a key factor in enabling the wells to produce is the ability to remove, and dispose of high volumes of water in the well - a technique that M3 Helium achieves with the use of a electric submersible pump ("ESP"), capable of lifting around 2,000 barrels of water per day, and injecting the displaced water into a nearby disposal well.

Current Project - Rost Twin

The Rost Twin was drilled with a larger 7-inch casing based on M3 Helium's theory, supported both by its experience with Rost 1 and also analogous wells in Oklahoma, that greater water removal enables higher gas production. Drilling of this larger well has been successful, with this part of the project being both on budget and on time, and accordingly M3 Helium expects 7 inch cased wells to be used in its forthcoming development of the Fort Dodge region.

During drilling of the Rost Twin, M3 Helium employed a mass spectrometer, coupled with gas detection equipment, to assess the prospective hydrocarbon gases, hydrogen and helium in the well. Encouragingly, the mass spectrometer recorded several shows of helium in different potential production zones within the well. The helium was detected with low hydrocarbon signatures supporting M3 Helium's theory that the helium-rich sands from which Rost 1 produces extend to the Rost Twin.

A completion rig is on site at the Rost Twin and it is intended that the well will be perforated to maximise benefit from these helium zones. Thereafter, the ESP previously used on Rost 1 will be installed in the Rost Twin to commence the de-watering process. When the same process was applied to Rost 1, there were gas shows at a very early stage and gas production increased steadily, in line with water production, until a mature flow rate was achieved within three months of commencement.

As part of the completion of the Rost Twin, the neighbouring Brobee salt water disposal well ("Brobee SWD") will be upgraded to take water from the two production wells. A permit has been applied for and work began in May 2026. M3 Helium has also entered into the Rost Agreements with Rixford in relation to the development of the Rost Twin well.

Next Project - Schneweis

The Schneweis Ventures 13 well ("Schneweis"), operated by Ritchie, has previously produced consistently over 300 Mcf/day before production was shut down due to significant water production. As with Rost 1 and Rost Twin, the target formation is the Morrow Sands. With a sustained de-watering programme and noting that Schneweis' drill stem test in 2022 exceeded 10,000 Mcf/day, Mendell Helium believes there is potential to increase production from historic levels.

Helium composition at Schneweis has been measured at 1.39 per cent. but, unlike Rost 1, there is a higher methane content of 70.06 per cent. Significantly, Schneweis is connected to a pipeline owned by Ritchie and it is envisaged that all produced gas from the well will be delivered to that pipeline with no requirement for prior treatment. Accordingly, the economics of the well will include the sale of hydrocarbons as well as helium.

The Company will fund the new disposal well and recompletion of Schneweis to earn an initial 85 per cent. net profit interest in the project. Once the Company has recovered 110 per cent. of its investment, its net profit interest falls to 70 per cent. Ritchie is entitled to bring the arrangement between the parties to an equal (50 per cent.) net profit interest by reimbursing M3 Helium for 50 per cent. of the project costs.

Next steps

Based on the success so far of Rost 1 and the Rost Twin, M3 Helium intends to roll out a development of helium production zones in the Fort Dodge region. The Fundraise and completion of the Acquisition enabled a significant acceleration of this development plan which has two aspects:

1. Drilling new 7 inch cased wells on land already leased by M3 Helium, specifically the Enlow and Bleumer leases; and

2. Re-completing existing third party wells that were shut in due to the presence of water, starting with Schneweis, in joint venture with Ritchie.

Alongside the above plans, M3 Helium intends to continue to lease additional land in Fort Dodge to continue to develop opportunities for further new production wells. The production zone that M3 Helium is targeting is known locally as the Morrow Sands, both a narrow and thin formation around 5,000 feet from surface. The management team has carried out considerable work in mapping out the Morrow Sands in Fort Dodge and both existing and future leases of land are typically small tranches designed to access this formation. Based on its experience at Rost 1 and supported by data from analogous wells in Oklahoma, the management team believes that the prospectivity of this region may represent a potentially significant opportunity for the Company. As set out above, the difficulty in accessing the formation coupled with the need for a high volume de-watering process, provides some protection from competing operators.

The Company raised gross proceeds of £5,000,000 from the Fundraise. Broker fees relating to the Fundraise are estimated to be £355,000, excluding VAT. The total costs and expenses of, and incidental to, Admission are estimated to be approximately £556,000, excluding VAT. The Company intends to use the net proceeds to expand its operations in the Fort Dodge area, by leasing additional land (of which it has already identified suitable locations), drilling and recompleting production and water disposal wells and developing further helium purification facilities and general working capital purposes.

Mendell Helium has estimated the following costs for the advancement of its operations at Fort Dodge:

|

Use of Proceeds |

Indicative cost |

|

Production well Includes drilling, completion and associated surface infrastructure |

£694,074 ($937,000) |

|

Disposal well Includes access to Arbuckle formation and triplex pump installation |

£315,555 ($426,000) |

|

Helium purification surface works Includes installation of condition unit, acquisition of membranes and PSA for helium concentration, set up of ground storage for helium and lease/purchase of Bauer compressor |

£1,102,963 ($1,489,000) |

It is important to note that each disposal well and helium purification plant are sized to accommodate up to four production wells.

Furthermore, the Company has identified material savings by carrying out these expansion opportunities simultaneously. These savings include no duplication of rig or team mobilisation costs as well as bulk purchase savings. The Fundraise therefore provides a significant advantage to Mendell Helium enabling it to accelerate its development plans and do so more cost effectively.

In line with the above, the Company intends to apply part of the net proceeds of the Fundraise towards the re-completion of Schneweis and the phased development of up to four further production wells, one disposal well and a new helium purification plant, subject in each case to operational progress and the Company maintaining sufficient working capital for its ongoing requirements.

4. Assets of M3 Helium/Details of M3 Helium's Tenements - Extracts from CPR

M3 Helium operates in two locations in Kansas - the Hugoton gas field in the south west of the state and Fort Dodge which is some 50 miles further to the east. Initially, M3 Helium concentrated on developing helium production wells in the Hugoton, and it currently has five wells that are either in production or have produced, but subsequently it moved its centre of operations to Fort Dodge. This move was driven by the success of its Rost 1-26 well which has been shown to have a helium composition of 5.1 per cent.

M3 Helium holds working interests in a portfolio of helium wells and associated acreage located primarily in the Fort Dodge area of Kansas and the West Hugoton field, as summarised in the table below. Certain interests are held under leases in which M3 Helium has a direct 100 per cent. working interest, while other interests arise through historical farm-in arrangements where the underlying leases are held by third parties, including Scout Energy Partners. Several of the Group's producing wells are currently held by production, while other leases remain within their primary term and are prospective for future drilling. M3 Helium's interests therefore comprise a combination of producing wells, development acreage and wells that are currently shut-in pending operational or commercial optimisation.

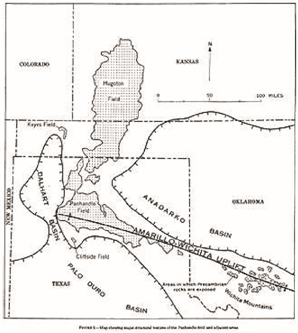

Five of M3 Helium's productive wells are located in the Hugoton Field in southwestern Kansas. This field, discovered in the 1920s, is the largest gas field in North America. It extends to the south through the Oklahoma panhandle and into Texas.

Figure 1: Hugoton Field Locator Map

0

0

The gas from the Hugoton Field contains varying concentrations of helium, ranging from 0.3 to 1.9 per cent., and represents the largest reserves of helium in the United States. This area of southwest Kansas is known as the Hugoton basin or Hugoton embayment, a northern shelf-like extension of the larger and deeper Anadarko basin in Oklahoma and Texas. The depositional environment was shallow seas that were transgressive and regressive, leaving interbedded deposits of carbonate (limestone and dolomite) and shale. The field is a stratigraphic-type trap overlying a monocline.

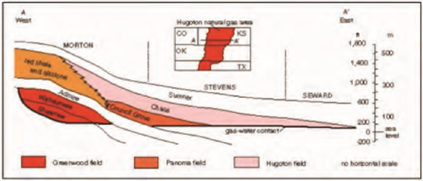

Most of the gas in the Hugoton Field is produced from the Permian Chase Group. The illustration below shows a schematic cross-section across the field. Rocks that are deeper and older also produce oil and gas in the Hugoton area, and have not been thoroughly tested.

Figure 2: Schematic Cross-Section, Hugoton Field

The Chase Group consists of interlayered carbonates, siliciclastics, and evaporites deposited in repeated sequences that are regionally continuous. The pore types within all carbonate layers are interconnected by a well-developed pore network that formed as a result of area-wide dolomitisation.

Fort Dodge

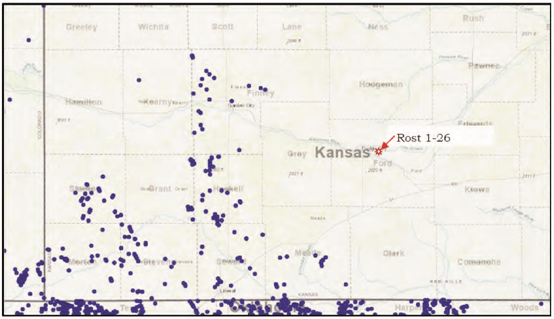

The bulk of M3 Helium's reserves are in the Fort Dodge area east of the Hugoton Field, in the Rost 1-26 well. While numerous wells produce from the Morrow in southeastern Kansas, the majority of these are located west/southwest of the Rost well in Hugoton Field, in defined fluvial meander belts. The Morrow sands in this area were generally deposited in erosional channels in the surface of the underlying Mississippian surface; thus, the reservoir can be difficult to track, follow, and exploit without 3D seismic data. Reservoir quality appears to be good where it is found, with porosity in the range of 10-15 per cent. and sufficient permeability to flow gas at rates of several million standard cubic feet per day (MMSCF/D). The Rost well in particular, as well as another Morrow well in Kansas and several others in the Oklahoma Panhandle (as described in the CPR in Part VI), exhibit unusual log and flow characteristics. All these wells exhibit good sand development on gamma ray logs, sonic log porosity as described, and some neutrondensity log crossover. However, the dual induction logs indicate low resistivity, and conventional log calculations such as the Archie equation for water saturation indicate that the reservoir is completely watersaturated. Despite these log results, these wells have all produced multiple billions of standard cubic feet (BSCF) of gas, along with high water rates. The typical production profile of these wells consists of initial low gas rates and high water rates, followed by increasing gas rates over the first 12 to 14 months and a gradual decline thereafter. M3 Helium's theory is that the gas is stored in the smaller pores in the reservoir, and that as the reservoir pressure declines with increasing cumulative water production, the gas expands and is able to flow.

Figure 3: Map showing Rost Well and Other Morrow Producers

Future development of Fort Dodge

M3 Helium holds two additional leases (Bleumer and Enlow Farms) in the Fort Dodge area, which reportedly either contain or are near wells drilled through the Morrow similar to the Rost 1-26. Therefore M3 Helium may have the potential to recomplete or twin such wells with minimal geological risk to develop additional reserves. M3 Helium believes that this additional leased area could support a further four production wells. This additional leased land is marked in green on the below map, with the location of Rost 1-26 shown in orange.

The Morrow formation is typically around observed 5,000 feet from surface but often with narrow boundaries. Unlike in the Hugoton, choice of location is paramount.

Reserves and Resources

The reserves estimates have been prepared by the Competent Person using standard petroleum engineering techniques in accordance with PRMS.

Reserves attributable to the Hugoton Field wells have been estimated using decline curve analysis of historical production data, supported by production performance from analogous wells where appropriate.

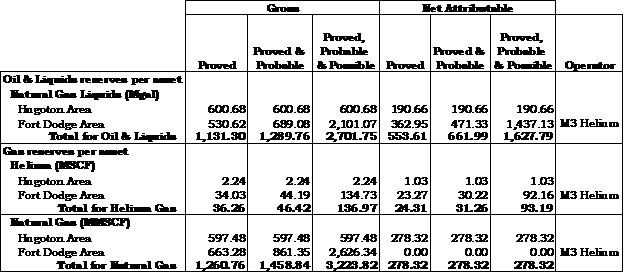

Table 1: Reserves Summary by Asset

Note: throughout this Document, MCF means thousands of standard cubic feet, MMCF means millions of standard cubic feet, Mgal means thousands of gallons, and M$ means thousands of US$.

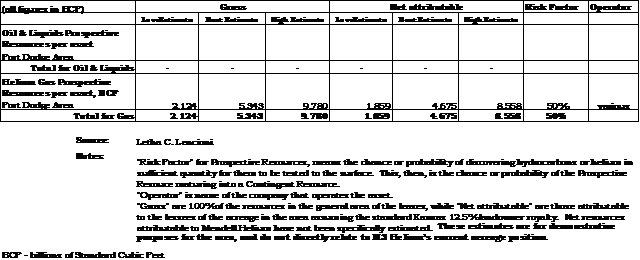

In addition to the above reserve estimates, the Competent Person has also estimated prospective helium resources in the Fort Dodge area. Prospective helium resources in the Fort Dodge area have been estimated using a probabilistic Monte Carlo simulation, incorporating a range of geological and reservoir parameters

Table 2: Summary of Prospective Resources Estimates, Fort Dodge Area

Prospective resource estimates are probabilistic in nature and relate to undiscovered accumulations. There is no certainty that any portion of the prospective resources will be discovered or commercially recoverable.

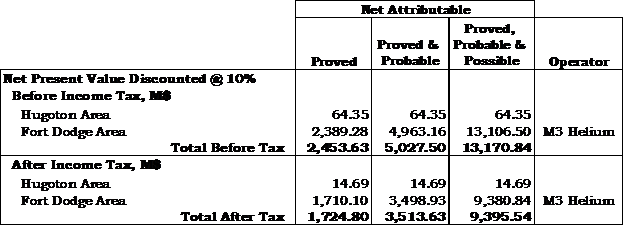

The CPR includes estimates of future net cash flows attributable to the Company's reserves. These have been calculated on both a before income tax and after income tax basis and discounted at 10 per cent. per annum (NPV10), as summarised in the table below. Based solely on M3 Helium's reserves across the Fort Dodge area and Hugoton area, the Competent Person has estimated an NPV10 after income tax of US$9.4 million.

Table 3: Value Summary by Asset

5. Helium Market

Background on Helium

Helium is an inert, non-renewable gas primarily produced through the natural decay of radioactive element and extracted primarily as a byproduct of natural gas production. Due to its unique physical properties, including low boiling point and non-reactivity, helium is a critical input across a range of advanced industries, including:

- Healthcare: MRI machines (cooling superconducting magnets)

- Semiconductors: Chip manufacturing and leak detection

- Aerospace: Pressurising and purging rocket fuel systems

- Welding & Industrial: Shielding gas in high-precision welding

- Cryogenics & Research: Essential for low-temperature experiments

Production of Helium

Whilst there is a large amount of helium in the atmosphere, it is prohibitively expensive to extract it from this source because its concentration is so low and, to do so, requires specialist equipment. It is estimated that distilling helium from the atmosphere would cost over US$1,500 per Mcf of helium. Helium has therefore historically been produced as a by-product of certain conventional natural gas projects, and those sources account for the bulk of the world's helium supply today. Commercial production generally occurs only when the concentration of helium in natural gas is economically viable - typically above 0.3 per cent.

The process of drilling for helium is identical to drilling for natural gas, allowing for the use of the same rigs, tools and personnel in these operations. However, exploration for helium is challenging and requires significant technical knowledge related to helium generation (from the underground decay of uranium and thorium), concentration and migration through formation fluids, exsolution and migration into gas phase traps and reservoir evolution through time. Specialised expertise and methods across multiple disciplines are required to effectively search for new helium fields.

Supply of helium globally is extremely geographically concentrated, with the US and Qatar currently accounting for approximately 75 per cent. of production. Other significant suppliers include Algeria, Russia, and Canada. In the US, the Federal Helium Reserve ("FHR") was established in Texas in 1925 to ensure consistent supply for critical applications. However, the FHR was wound down following a privatisation initiative in 1996 (the Helium Privatization Act), resulting in supply volatility and uncertainty, with numerous market shortages since 2006.

There are two notable projects, the LaBarge field in the US and the North Field in Qatar, which currently supply approximately 50 per cent. of world helium demand. However, existing production is estimated to be declining at 2-3 per cent. per annum due to natural reservoir depletion, compared to demand growth at a CAGR of 6 per cent.

Helium Separation and Purification

Once a commercially viable helium reserve has been discovered and development wells have been drilled, there are two stages in the production of helium: separation and purification. Because even 0.3 per cent. helium in a bulk-gas is considered a high-concentration, the first step is to separate the helium from the other components of the bulk gas stream. This can be accomplished through three principal technologies, which are often combined depending on the composition of the gas stream:

Membrane Separation

The helium content of a gas can be upgraded or purified by using high-pressure membranes which either concentrate or purify helium through selective diffusion of relatively smaller gas molecules through microscopic pores in the medium. This technology is relatively new for helium separation applications and may not be suitable for longer-lifetime projects.

PSA or TSA

Pressure-Swing Adsorption (PSA) or Temperature-Swing Adsorption (TSA). These technologies use temperature or pressure to cause selective adsorption of different sized gas molecules into a medium with a large surface area consisting of uniformly sized pore spaces. These technologies are time-tested, reliable, and can be deployed at small scale. The downside is that this process is less efficient than cryogenic separation, in terms of both energy use and product losses during the process.

Cryogenic Separation

Similar to the air separation units (ASUs) that are deployed worldwide in the industrial gas business, this technology uses low temperatures to cause different gases to condense off as a liquid in a fractionation tower. This process is ideally suited to helium, which has the lowest condensation point of any gas, but requires large scale for efficiency and has a higher initial capital cost.

Helium Liquefication

In order to ship helium economically around the globe, like LNG, purified helium gas is liquefied prior to shipping so that it will fill a smaller volume. Liquid helium product also addresses a wider market, including those end-users who require the low temperatures of liquid helium. In the larger global helium plants, the gas is liquefied and stored in specialised 40 foot long ISO intermodal shipping containers. Due to the high value of helium, it can also be economically shipped regionally as a gas in high-pressure tube trailers, although shipping costs for helium gas are higher than for liquid helium.

Key Market Participants

There are numerous players involved in the helium market but a handful of companies control the majority of supply and distribution. Qatargas, the US Government (historically through the FHR, although this has now been sold as noted previously), Sonatranch in Algeria, Gazprom and Exxon produce the majority of supply. Additionally, as of 2021, there were approximately 30 small helium exploration companies operating in the USA, Canada, Tanzania, Australia and South Africa.

Whilst the number of helium production and exploration companies continues to grow, the midstream helium purification stage is concentrated among mainly US based companies. The likes of Air Liquide, Linde, Air Products and Chemicals, and Matheson Tri-Gas play a critical role in refining, packaging, and distributing helium to end users globally.

Demand for Helium

As of 2025, global helium demand is estimated at approximately 6 billion standard cubic feet (Bscf) per annum, with China alone importing around 1 Bscf annually. This is expected to increase to approximately 8.5 Bscf per annum by 2030, reflecting a CAGR of approximately 7.2 per cent. By 2035 demand is projected to nearly double, reaching approximately 11.4 Bscf. This growth is driven primarily by the semiconductor industry's expanding needs, with the 2022 US CHIPS and Science Act aimed at increasing domestic semiconductor manufacturing being a key driver. Helium is used for cooling and maintaining controlled environments in semiconductor manufacturing processes.

Other expected areas of growth include semiconductor, flat panel display, and optical fibre manufacturing in Eastern and South East Asia. Emerging sectors such as commercial space or near-space travel, airships, quantum computing, nuclear fusion and small-scale fission are also expected to create new demand. In addition, growth in hydrogen demand is also expected to contribute to further demand for helium, which is used in leak testing.

Pricing of Helium

Helium pricing is not transparent due to the absence of a formal commodities exchange and a relatively immature market. Prices are typically set through long-term contracts, although spot pricing can vary widely during supply disruptions. Helium prices have seen significant volatility over the past decade due to: the depletion of the U.S. Federal Helium Reserve, supply interruptions (from maintenance at key assets or geopolitical events in key producing countries) and an overall tightening of the supply-demand balance due to limited new supply sources coming online. As with other commodities, retail pricing can be considerably higher than commercial prices and the costs of purifying the helium means that producers may receive a considerable discount to market prices.

Pricing for helium producers reflects a mix of contract vintages, with older agreements often locked in at lower prices and more recent contracts commanding significantly higher rates. Over the past decade, helium prices have increased at a CAGR of around 20 per cent. but more recently growth has slowed.

Imports from Qatar, the world's largest helium exporter, are priced on average between US$400 and US$500/mcf. After accounting for transportation costs, this suggests Qatar's export prices are in the range of US$350 to US$450/mcf. In North America, legacy supply contracts are similarly priced but agreements may vary considerably in price reflecting local demand and the costs of transport and purification.

Over a longer 20-year period, average helium prices have increased at a CAGR of approximately 8 per cent., reaching around US$375/mcf by late 2022. However, from 2017 to 2022, pricing accelerated, rising at an estimated 18 per cent. CAGR to reach the US$500/mcf level.

Looking forward, if helium prices were to grow at a conservative 5 per cent. CAGR from 2022 through 2030, contract pricing would rise to approximately US$550/mcf. At 10 per cent. CAGR, prices would approach US$750/mcf, while a 15 per cent. CAGR would result in prices of roughly US$1,150/mcf.

To put these projections in context, the U.S. Defence Logistics Agency bulk helium price - primarily for aerospace and defence-related use - peaked at US$1,080/mcf in October 2023. Meanwhile, during extreme global supply shortages in 2022, U.S. spot prices ranged from US$1,000 to US$2,500/mcf, underscoring both the volatility of the market and the premium end-users are willing to pay for reliable helium supply.

More recently, the March 2026 Iran-Gulf conflict has underlined the sensitivity of helium pricing to disruption in Qatar, one of the world's key helium suppliers. QatarEnergy's force majeure announcement following the suspension of LNG and associated products, together with industry estimates that Qatar's Helium 1 and Helium 2 facilities represent roughly 25 per cent. of global helium capacity, suggests that any sustained interruption to Qatari production or Gulf shipping routes could place upward pressure on helium prices.

6. Regulatory Framework in Kansas

Application of Kansas Laws to Helium

The Kansas statutory code does not provide an express definition of "helium". However, helium is generally treated as part of natural gas and falls under the regulatory framework governing natural gas exploration and development. Therefore, the permitting and operational framework for natural gas in the state of Kansas is addressed in this Document.

Permitting Process

Exploration Notification

In Kansas, seismic exploration does not require a separate state-issued permit. However, operators must comply with local county and land access requirements. Notice of intent to conduct exploration and obtain landowner permissions is typically required. No general state-level surety bond or centralised exploration permit is issued.

Drilling Permit

Before drilling a gas or test well, an operator must file an Application for Permit to Drill ("APD") with the Kansas Corporation Commission ("KCC") - Conservation Division. The application must be submitted with a certified well location and supporting documents, including casing design and blowout prevention details. Notification to affected landowners is required, and surface landowner permission must be obtained prior to entry.

Permit Approval Process

The KCC reviews applications for compliance with well construction standards, protection of groundwater, and public notice obligations. Requirements for surface casing, pit construction, and proposed completion techniques (including hydraulic fracturing) must be disclosed in the APD.

Spacing Requirements

Kansas spacing regulations for gas wells differ by field. Statewide spacing is generally one well per 640 acres for gas wells unless field-specific orders provide otherwise. The KCC may establish temporary or permanent spacing units, and notice must be provided to affected interest owners before a hearing on spacing applications.

Fees and Duration

As of current KCC regulations, fees for drilling permits are $300 for an intent-to-drill permit. Additional fees may apply for directional/horizontal wells.

Permit Expiration

Permits are generally valid for 12 months. If drilling does not commence within this period, a new application must be filed.

Transfer of Permit Location or Ownership

Permit transfers must be approved by the KCC. Operators acquiring a well must file a transfer form and provide updated bonding. No additional fee is required if depth and scope remain unchanged.

Hydraulic Fracturing

Kansas does not currently require full chemical disclosure under a centralised registry but encourages reporting via FracFocus. Operators must submit a post-fracturing treatment report to the KCC, detailing fluids used, proppants, and pressures applied. Trade secret protections apply to proprietary additives.

Leasing and Development

Mineral Estate Rights

Kansas follows the "ownership-in-place" doctrine, meaning the mineral estate owner retains full rights to lease, sell, or develop subsurface minerals. Unleased mineral interest owners are typically entitled to 1/8th royalty on production.

Oil and Gas Leases

Oil and gas leases in Kansas are real property interests governed by general contract principles. The lease terms dictate royalty obligations, payment schedules, and production thresholds. Operators must also comply with surface access and damage compensation rules under state common law or contractual agreements.

State-Owned Minerals

The Kansas State Land Office administers leasing of state-owned mineral rights. State leases typically include: a primary term (commonly 3-5 years), royalty rates of 12.5 per cent. to 16.67 per cent. and obligations to protect state property from drainage or pay compensatory royalties.

Drilling Notices & Reporting

Notice Requirements

Kansas law requires notice to surface owners before any surface-disturbing activity. Written notice must be given at least 15 days prior to surface entry for well site preparation.

Reporting Requirements

Operators must file: well completion reports within 90 days, production reports monthly, directional surveys for horizontal wells. The KCC maintains a public database for submitted well data.

Pooling and Unitisation

Pooling

Kansas allows voluntary pooling and compulsory integration under K.S.A. 55-1301 et seq. Compulsory pooling may occur if the operator shows a good faith effort to obtain voluntary agreements. Non-consenting interest owners may be subject to cost recovery penalties up to 200 per cent. of drilling and completion costs.

Unitisation

Unitisation (the coordinated development of a reservoir) requires consent of at least 75 per cent. of mineral interest owners and approval from the KCC. It is generally used for secondary or enhanced recovery operations.

Compensation and Royalties

Leasing Bonuses and Royalties

Bonus and royalty amounts are contractually determined. The standard landowner royalty in Kansas is 1/8 (12.5 per cent.), although leases may provide higher rates.

Royalty Payments and Records

Kansas requires timely payment of royalties and detailed remittance statements. Interest accrues on late payments after 60 days from first production, unless otherwise provided by contract.

Remedies for Nonpayment

A royalty owner may bring suit in district court and recover interest, attorney's fees, and court costs. Kansas does not require a division order to begin payments but allows their use to clarify payout splits.

Environmental Protection

Air Emissions

Operators must comply with Kansas Department of Health and Environment (KDHE) requirements. Facilities emitting volatile organic compounds (VOCs) may need air permits depending on throughput and control equipment.

Water Protection

Discharges of stormwater associated with oil and gas activity must comply with National Pollutant Discharge Elimination System (NPDES) standards as administered by KDHE. Discharges that do not contact pollutants are typically excluded from permitting.

Non-Significant Activities

Low-risk activities, including minor oil and gas operations without surface water impact, are excluded from water quality permitting under KDHE guidelines.

Surface Access

Kansas common law grants mineral owners the implied right to use as much of the surface as reasonably necessary for mineral development. However, Kansas statutes encourage surface use agreements and require notice and compensation for damages caused by drilling operations.

Surface Damage Agreements

While not mandated by statute, surface damage compensation is often addressed by private agreement. Operators are encouraged to negotiate surface use terms in advance.

Penalties for Noncompliance

Failure to give proper notice or to repair surface damages may result in liability under tort or contract law.

7. The Company's historical operations

On 14 October 2024, Mendell Helium announced the disposal of its Voyager-branded plant based health & wellness business to Orsus and, on 11 November 2024, the Company confirmed that completion had taken place.

The Company's historical operations comprised:

- Manufacturing facility in Perth, Scotland producing both products for own brand and third party customers (VoyagerCann)

- E-commerce and wholesale operations based in Perth, Scotland

- Three brands: Voyager, Ascend Skincare and Amphora

- Three retail stores in Scotland (St Andrews, Dundee and Edinburgh)

Prior to completion of the Disposal, agreements were reached to sublet the shops in St Andrews and Edinburgh. Owing to rising rents since the Company commenced trading from these premises, Mendell Helium makes a small profit from the subletting (after taking account of legal fees and agent commissions in the first year). The lease of the Dundee shop was assigned to, and is the responsibility of, Orsus.

In consideration for the Disposal, Orsus entered into a £25,000 loan agreement with Mendell Helium on 5 July 2025 (the "Loan"). The Loan is interest free for 12 months and thereafter accrues interest at the Bank of England base rate. The Loan is repayable by Orsus within five years but if Orsus completes any equity fundraising or equity-linked financing during the term of the loan, 3 per cent. of the gross proceeds received by the Orsus from such fundraising shall be applied towards repayment to Mendell Helium of the outstanding balance.

The share purchase agreement signed with Orsus contains warranties given by the Company relating to the Company's power and authority to enter into and perform its obligations under the Disposal. In addition, a number of business warranties were given by the Company to Orsus (for example in respect of employment, assets, trading, litigation and intellectual property). Orsus' recourse against the Company for breach of warranties, indemnifications and otherwise under the share purchase agreement is limited to certain agreed liability caps, with an overall maximum liability capped at £25,000.

On 23 July 2025, the Company announced that it had implemented a bitcoin treasury policy and its intention to potentially mine or purchase bitcoin as part of this strategy. As at the date of this Document, the Company has decided to terminate its bitcoin treasury policy and any potential bitcoin or crypto related mining activities. To date, the Company has neither mined nor purchased any crypto assets including bitcoin.

8. Reasons for Admission

The Company is seeking Admission in order to take advantage of AIM's profile, broad investor base, liquidity and access to institutional and other investors and to further support the achievement of its strategic objectives. The Company noted strong investor support for its fundraises completed during 2025 and earlier in 2026 and the positive sentiment towards seeking admission to AIM as an alternative to continued trading on AQSE, which reinforced the Board's decision to pursue Admission. The Board is also aware of one of the UK's largest retail broker's decision to cease activities in AQSE quoted companies in June 2026. Several of the Company's shareholders are customers of this broker and consequently have expressed concern to the Company about their ability to continue to hold Ordinary Shares should the Company remain quoted on AQSE.

The Company believes that Admission to AIM will provide access to a broader institutional investor base, enhanced liquidity, and greater profile within the public markets. The Board considers AIM to be a more suitable platform to support the Group's future growth strategy.

9. Directors

The Board consists of a professional team with experience in helium development and growing companies.

Eric James Boyle (aged 72) - Independent Non-Executive Chairman

Eric Boyle has over 30 years' experience in stockbroking, fund management and investment banking and was a partner of Smith & Williamson Investment Management LLP. During his career, Eric co-founded two London-listed companies, SR Pharma plc, where he was Chairman until 2004, and Highlands Natural Resources plc (now Chill Brands Group plc) in 2015. With the experience gained in studying a diversity of stock markets he has held directorships in three London-listed closed-end funds, including Atlantis Japan Growth Fund Limited where he was a director from 2000-2016. During his career he has raised new capital for several groups launching in both developed and emerging markets.

Nicholas ("Nick") George Selby Tulloch (aged 53) - Chief Executive Officer

Nick Tulloch advised companies on the UK capital markets for over 20 years, working for several well-known investment banks and stockbrokers, including Cazenove, Arbuthnot and Cenkos. In 2019, he became finance director and then subsequently CEO of Zoetic International plc (now Chill Brands Group plc and originally Highlands Natural Resources plc) overseeing its transformation from an oil & gas business to the first CBD company to be quoted on the London Stock Exchange. He went on to found the Company's original business, Voyager, becoming the first person to successfully list two CBD companies on UK stock exchanges. In 2024, he led Voyager's re-positioning as a helium producer in Kansas under its new name of Mendell Helium plc along with the disposal of its CBD operations. He is also chairman of ECR Minerals plc and Physiomics plc. Nick began his career as a solicitor with Gouldens (now part of US firm Jones Day) and holds a Master's Degree in law from Oxford University.

Paul Ethan Mendell (aged 60) - Executive Director

Paul is an oil and gas producer and co-founder of two UK listed companies - Iofina plc, an AIM listed iodine producer, and Highlands Natural Resources plc, later known as Zoetic International plc where he was chairman of that company, now known as Chill Brands Group plc. Paul has owned interests in over twohundred producing oil and gas wells in the US which were subsequently acquired by larger firms including Anadarko, EnCana, Noble, Oxy and others. He is a geologist and a well-respected developer of new concepts in exploration for oil, gas, iodine and other commodities. Paul also founded Mendell Energy; a Denver based independent oil and gas producer which sold for US$12 million in 2012.

John Davies Brown (aged 61) - Independent Non-Executive Director

John has more than 25 years of international experience in oil and gas and related industries, including eight years' experience with operations in North America. He is a Chartered Accountant (ICAS) and was Chief Financial Officer or Group Finance Director for numerous UK listed companies within the oil and gas sector including Gulf Marine Services plc, Bowleven plc and Pittencrieff Resources plc. He was also previously an independent non-executive director at the AIM-listed oil company San Leon Energy plc. He has extensive financial, commercial and strategic expertise and has had wide exposure to both listed capital markets and debt finance providers.

Further details of the terms on which the Directors are appointed are set out at paragraph 7 of Part VII of this Document.

10. Financial Information

Financial Information on the Group is included in Part III and Part IV of this Document.

11. Current trading, future prospects and significant trends

In terms of any known trends, uncertainties, demands, commitments or events that are reasonably likely to have a material effect on the Group's prospects for at least the current financial year, investors should refer to paragraph 5 of Part I above (in relation to commodities, products and markets) and Part II (in respect of risk factors).

12. Lock-ins and orderly market arrangements

The Directors who, on Admission, will hold in aggregate 41,096,411 Ordinary Shares (representing approximately 12.06 per cent. of the Share Capital) have undertaken not to (and to use their best endeavours to procure that their connected persons shall not), save in limited circumstances, dispose of any of their interests in Ordinary Shares (including any Ordinary Shares that they may acquire through the exercise of Options or otherwise) at any time prior to the first anniversary of Admission.

Further details of the lock-in and orderly-market arrangements are set out in paragraph 11 of Part VII of this Document.

13. Corporate Governance

Corporate Governance

The Board currently and historically has applied the ten principles of the Quoted Companies Corporate Governance Code (the "QCA Code") on a "comply-or-explain" basis. Following Admission and the AQSE Cancellation, the Group will continue to apply the QCA Code from the date of Admission.

The Board, which meets formally at least six times a year, is responsible for the management of the business of the Company, establishing the policies and setting the strategic direction of the Company. The Company also holds additional Board meetings as and when required. It is the Directors' responsibility to oversee the financial position of the Group and monitor the business and affairs of the Company on behalf of the Shareholders, to whom they are accountable. The primary duty of the Directors is to act in the best interests of the Company at all times. The Board also addresses issues relating to internal control and the Company's approach to risk management and has adopted an anti-corruption and bribery policy.

Mendell Helium has established an Audit and Risk Committee and a Remuneration and Nomination Committee with formally delegated duties and responsibilities.

Audit and Risk Committee

The Audit and Risk Committee assists the Board in, amongst other matters, discharging its responsibilities with regard to financial reporting, external and internal audits and controls, including reviewing the Company's annual financial statements, reviewing and monitoring the extent of non-audit work undertaken by external auditors, advising on the appointment, reappointment, removal and independence of external auditors, and reviewing the effectiveness of the Group's internal audit activities, internal controls and risk management systems. The ultimate responsibility for reviewing and approving the annual report and accounts and the half-yearly reports remains with the Board.

The Audit and Risk Committee is also responsible for (i) advising the Board on the Company's risk strategy, risk policies and current risk exposures, (ii) overseeing the implementation and maintenance of the overall risk management framework and systems, (iii) reviewing the Group's risk assessment processes and capability to identify and manage new risks and (iv) monitoring potential and actual changes to legislation, especially around the Company's products.

The Audit and Risk Committee will meet with appropriate employees of the Group at least once annually. The membership of the Audit and Risk Committee comprises John Brown (as its Chairperson) and Eric Boyle.

The Audit and Risk Committee will meet formally twice a year at appropriate intervals in the financial reporting and audit cycle and otherwise as required.

Remuneration and Nomination Committee

The Remuneration and Nomination Committee assists the Board in determining its responsibilities in relation to remuneration and nominations, including, amongst other matters, making recommendations to the Board on the Company's policy on executive remuneration, determining the individual remuneration and benefits package of each of the executive directors.

The membership of the Remuneration and Nomination Committee comprises John Brown (as its Chairperson) and Eric Boyle.

The Remuneration and Nomination Committee will meet formally twice a year and otherwise as required.

In addition, Mendell Helium's corporate governance is supported by the following:

Share Dealing Code

The Company has adopted a code for directors' and employees' dealings appropriate for a company whose shares are admitted to trading on AIM and will take all reasonable steps to ensure compliance by the Directors and all employees.

Anti-Bribery and Anti-Corruption Policy

The Company has adopted an anti-bribery and anti-corruption policy consistent with the UK Bribery Act 2010. The policy is designed to ensure that the Directors, executive officers, employees and agents understand the requirements of the UK Bribery Act 2010 and adhere to the Company's policy to comply with the UK Bribery Act 2010 and all anti-bribery legislation wherever the Company conducts its business. The Company has a zero tolerance for practices which would amount to bribery and/or corruption.

The policy specifically addresses facilitation payments or gifts and hospitality, dealings with public officials, political donations, lobbying and advocacy and charitable donations, and includes provisions dealing with notification, as well as provisions regarding disciplinary action in the event that any part of the anti-bribery and anti-corruption policy has been breached. New and existing staff are required under the policy to be trained and the Company's approach to anti-bribery and anti-corruption must be communicated to its business partners.

Environmental and climate-related compliance

The business of helium exploration and production involves operational, environmental and regulatory risks. In pursuing its business objectives, the Company seeks to operate in a responsible manner that takes account of environmental and climate-related considerations while delivering long-term value to shareholders and benefits to the communities in which it operates. The Company intends to conduct its activities in accordance with applicable environmental laws, regulations and permits in the jurisdictions in which it operates and to implement appropriate monitoring and operational procedures in support of these objectives.

Exploration, drilling and production activities are subject to a range of risks and hazards, including adverse weather conditions, industrial accidents, well control incidents, equipment failure, unexpected geological conditions, contamination or the release of hydrocarbons or other substances, and interruptions to infrastructure or operations. The Company intends to engage suitably qualified staff and experienced contractors and to adopt appropriate operational practices in order to manage these risks. Oversight of environmental matters, compliance and related governance will be undertaken by the Board.

14. Options and Warrants

Options

The Company has agreed to grant, immediately prior to and conditional on Admission taking place, options over 33,322,800 new Ordinary Shares, each exercisable at 4.5 pence per share, with certain vesting conditions, to certain directors of the Company and other members of staff. Options to be granted shall be effected pursuant to the Company's share option scheme. In addition, the Company will have authority to grant additional options pursuant to the share option scheme over up to 15 per cent. of the Company's issued share capital.

Further details of the Options are set out in paragraph 8 of Part VII of this Document.

Warrants

On Admission, the Company will have 109,658,799 Warrants in issue at exercise prices between 3 pence and 6 pence per Ordinary Share.

Further details of the Warrants are set out in paragraphs 4 of Part VII of this Document.

Convertible Loan Notes

The Company has £280,000 of CLNs in issue which are convertible into Ordinary Shares at a conversion price of 3 pence per share at any time up to 31 July 2026. Full conversion would result in the issue of 9,333,333 new Ordinary Shares.

Further details of the CLNs are set out in paragraphs 12 of Part VII of this Document

15. Dividend Policy

Mendell Helium has, to date, been loss-making but the potential of new production wells in Fort Dodge could be significant. It is the intention of the Board that, subject to (i) a sufficient number of new wells being drilled in 2026, (ii) the cashflow from those wells, and (iii) the Company having, as required by law, sufficient distributable reserves, Mendell Helium would seek to pay a dividend to Shareholders during 2027. However, there can be no certainty whatsoever as to whether or when any dividend or other distribution might be paid or made, or as to the amount of any dividend or other distribution which may be paid or made. Furthermore, the Company expects that it will first be necessary for it to undertake a Court-approved reduction of capital, in accordance with the Act, as part of seeking to generate sufficient distributable reserves for this purpose.

16. Taxation

Information regarding certain taxation considerations for corporate, individual and trustee Shareholders in the United Kingdom with regard to Admission is set out in paragraph 17 of Part VII (Additional Information) of this Document.

Enterprise Investment Scheme (EIS) and Venture Capital Trust (VCT)

The Company has applied for and obtained advance assurance from HMRC that the New Ordinary Shares will be eligible for EIS purposes, subject to the submission of the relevant claim form in due course.

The Company has applied for and obtained advance assurance from HMRC that the New Ordinary Shares should be eligible shares under VCT provisions.

The obtaining of such advance assurance and submission of such a claim by the Company does not guarantee EIS qualification for an individual, whose claim for relief will be conditional upon his or her own circumstances and is subject to holding the shares throughout the relevant three-year period.

The continuing status of the New Ordinary Shares as qualifying for EIS purposes will be conditional on qualifying conditions being satisfied throughout the relevant period of ownership. Neither the Company nor the Directors give any warranty, representation or undertaking that any investment in the Company by way of EIS Shares will remain a qualifying investment for EIS purposes.

17. Applicability of the Takeover Code

The Takeover Code applies to the Company. Under Rule 9 of the Takeover Code, any person who acquires an interest (as defined in the Takeover Code) in shares which, taken together with shares in which that person or any person acting in concert with that person is interested, carry 30 per cent. or more of the voting rights of a company which is subject to the Takeover Code, is normally required to make a general offer to all the remaining Shareholders to acquire their shares.

Similarly, when any person, together with persons acting in concert with that person, is interested in shares which, in the aggregate, carry not less than 30 per cent. of the voting rights of such company, but does not hold shares carrying more than 50 per cent. of the voting rights of the company, an offer will normally be required if such person or any person acting in concert with that person acquires a further interest in shares which increases the percentage of shares carrying voting rights in which that person is interested.

Further, under Rule 37.1 of the Code, when a company redeems or purchases its own shares, any resulting increase in the percentage of voting rights carried by the shares in which a person, or group of persons acting in concert, is interested will be treated as an acquisition of interests in shares carrying voting rights for the purpose of Rule 9.1 of the Code. An offer under Rule 9 of the Code must be made in cash at the highest price paid by the person required to make the offer, or any person acting in concert with such person, for any interest in shares of the company during the 12 months prior to the announcement of the offer.

An offer under Rule 9 must be in cash at the highest price paid by the person required to make the offer, or any person acting in concert with such person, for any interest in shares of the company during the 12 months prior to the announcement of the offer.

The Company has agreed with the Takeover Panel that the following individuals and entities are presumed to be acting in concert in relation to the Company by virtue of previous business relationships and their connected persons: (1) Nick Tulloch; (2) Sarah Tulloch; (3) Fetlar Capital Limited; (4) Eric Boyle; (5) Susan Boyle; (6) Laura Boyle (7) Marcus Boyle; (8) Paul Mendell and (9) Julie Mendell (together the "Concert Party").

On Admission, the Concert Party will be interested in 44,979,861 Ordinary Shares, representing approximately 13.20 per cent. of the Company's Share Capital.

Further information on the provisions of the Takeover Code and the holdings of the Concert Party is set out in paragraph 20 of Part VII of this Document.

18. AQSE Cancellation, Admission, Settlement and Dealings

Application will be made to the London Stock Exchange for the Share Capital to be admitted to trading on AIM. It is expected that Admission will become effective and dealings will commence in the Ordinary Shares at 8.00 a.m. on 16 June 2026. No application has or will be made for the Ordinary Shares to be admitted to trading or to be listed on any other stock exchange.

In connection with Admission, the Company will cancel the trading of its Ordinary Shares on AQSE. The last day of dealings on AQSE is expected to be 29 June 2026, with the AQSE Cancellation becoming effective at 8.00 a.m. on 30 June 2026.

The above-mentioned dates and times may be subject to change and will be notified accordingly.

No application has or will be made for the Options, Warrants or CLNs to be admitted to trading or to be listed on any other stock exchange and a register of holders of Warrants will be maintained by the Company. Upon exercise of an Option, Warrant or CLN, a holder will be issued new Ordinary Shares which the Company will procure to be admitted to trading on AIM. Further details of the Options, Warrants and CLNs are set out in paragraph 4, 8 and 12 respectively of Part VII of this Document.

The Ordinary Shares are in registered form and are capable of being held in either certificated or uncertificated form (i.e. in CREST).

Cairn has been appointed as the Company's nominated adviser in relation to the Admission and the Brokers have each been appointed as the Company's Broker in relation to the Admission.

19. CREST

CREST is a paperless settlement system enabling securities to be evidenced otherwise than by a certificate and transferred otherwise than by written instrument in accordance with the CREST Regulations.

The Ordinary Shares will be eligible for CREST settlement. Accordingly, following Admission, settlement of transactions in the Ordinary Shares may take place within the CREST system if a Shareholder so wishes. CREST is a voluntary system and Shareholders who wish to receive and retain share certificates are able to do so.

For more information concerning CREST, Shareholders should contact their stockbroker or Euroclear UK & International Limited at 33 Cannon Street, London EC4M 5SB or by telephone on +44 (0) 20 7849 0000.