Annual Financial Report

Summary by AI BETAClose X

|

Geiger Counter Limited Plc

(the "Company")

24 December 2025

RELEASE OF REPORT AND FINANCIAL STATEMENTS

The Directors announce the release of the Annual Report and Financial Statements for the year ended 30 September 2025, which are included as an attachment to this announcement.

http://www.rns-pdf.londonstockexchange.com/rns/8691M_1-2025-12-24.pdf

CHAIRMAN'S STATEMENT - FOR THE YEAR ENDED 30 SEPTEMBER 2025

When I last wrote to Shareholders in the interim report earlier this year uranium markets were recovering from a period of underperformance. The net asset value ("NAV") per ordinary share of the Company as at 31 March 2025 was 33.71p compared to 53.93p as at 30 September 2024. Since then, I am pleased to report that the momentum in uranium equities has returned, represented by an improvement in the Company's NAV per ordinary share as at 30 September 2025 to 71.66p, representing an increase of 32.89% for the full year under review. The Company's share price return has also recovered with the full year share price appreciation to 30 September 2025 coming in at 32.88%. The discount to NAV per ordinary share closed at 17.39%.

In my opinion the principal reasons for the strong recovery in our NAV per ordinary share is two fold - first, the world is embracing and recognising the resurgence in demand for electrical energy, generated by nuclear power stations, which in turn are fuelled by enriched uranium; second, our highly experienced and knowledgeable fund managers, have identified the optimal investment opportunities to benefit from resultant demand growth for uranium.

Essentially, the market is unbalanced, in that the fuel supply chain does not currently have the capacity to meet future demand. We have seen various attempts to alleviate this supply shortfall with the most notable being the US Government announcing executive orders in May 2025 to accelerate the deployment of new nuclear capacity as well as increase funding for the development of enriching and conversion facilities.

The private sector has also invested in nuclear reactor life extensions and restarts as the power source of choice to power their new AI data centres. These initiatives along with many others have driven price increases in the portfolio companies in which we invest. The investment manager's report on pages 13 to 19 sets out the investment position in more detail.

Share Buybacks and Corporate Activity

On 11 December 2024, the Company's ordinary shares were admitted to listing in the closed-ended investment funds category of the Official List of the FCA and to trading on the Main Market of the London Stock Exchange. The previous listing on The International Stock Exchange was subsequently cancelled. The Board anticipates that the Main Market listing will continue to bring the Company to the attention of a wider group of potential shareholders and improve liquidity in the Company's shares.

The Company has continued to engage in a program of stock buybacks to provide liquidity, increase the NAV per ordinary share and ideally narrow the discount. During the period under review the Board has utilised its share buyback powers to repurchase 28,210,360 ordinary shares at a cost of £12.3m.

It is disappointing to note that although the Company continues to provide investors with excellent capital growth over one year (+32.88%), three years (+49.57%) and five years (+332.02%) to 30 September 2025, the discount has remained stubbornly wide at times over the last 12 months. This is not uncommon in the wider investment company sector and your Board has engaged with several advisers to try to increase the appeal of the Company's shares and widen the shareholder base.

Since the end of September, the Company has continued to utilise the share buyback authority and has repurchased a further 8,144,747 shares at a cost of £4.7m.

Subscription Rights

The Annual Subscription Right enables Shareholders to subscribe for 1 new Ordinary Share for every 5 Ordinary Shares held on 30 April in each year at a price equal to the undiluted NAV per ordinary share on 1 May one year prior.

The Company announced on 1 May 2025 that the fifth Subscription Rights price would be 37.20 pence per share and that the exercise date would be 30 April 2026. Shareholders will be sent details of how to subscribe a few weeks prior to that date.

In anticipation of this five year term expiring in April 2026, the Board has resolved to propose an ordinary resolution for the continuation of the Subscription Right mechanism on an annual basis thereafter. If such resolution is not passed, the Directors will formulate proposals to be put to Shareholders to amend the Articles in order to remove the Subscription Right.

Outlook

The recently released, World Nuclear Outlook Report Preview 2025, has highlighted that Global nuclear capacity could reach 1428 GWe by 2050, exceeding the 1200 GWe target set in the December 2023. For this and an abundance of other well telegraphed drivers behind the positive sentiment, your investment managers and Board of Directors believe that the fundamental structural support for uranium equities remains as strong as ever, and that with growing global nuclear power demand coupled with a highly constrained and fragile supply landscape, our portfolio is well-positioned to benefit.

On behalf of the Board, I would like to thank shareholders for their continued support in the Company.

Ian Reeves CBE

Chairman

December 2025

INVESTMENT ADVISER'S REPORT - FOR THE YEAR ENDED 30 SEPTEMBER 2025

Summary

The year 2025 marked a material Nuclear Renaissance over and above what was already a positive supply/demand dynamic for Uranium miners. According to the International Energy Agency ("IEA"), global nuclear power capacity is set to increase by at least one-third to 2035 with over 40 countries having plans in place to expand the use of this source of power.

US energy policy has seen strong support for nuclear, with funding and backing across the nuclear fuel supply chain, whilst the miners who have the longest lead times in adjusting supply have been left behind and, in our view, will increasingly become the bottleneck to fuel supply growth. This should be very bullish for U3O8 pricing and the companies in which this fund invests.

Nuclear power, with its zero-carbon base load power is viewed as an integral part of the solution for growing Artificial Intelligence (AI) data centre demand in the future. This has been seen via announcements (see below) on life extensions and restarts of existing reactors, with further commitments for a larger build of America's nuclear fleet. Energy security is paramount for both the US and China given trade hostilities, as is the development of AI due to security and technological implications. Cheap reliable energy is the key to unlocking this geopolitical advantage, which is well understood and adds a further positive fundamental driver for the Uranium mining sector.

China has been way ahead of the west on energy policy and is still building 10 reactors per year, as they have for the last decade, which puts into perspective the recently announced $80bn investment by the US to construct 10 Westinghouse reactors in the US over multiple years.

Nuclear also forms part of the electricity generation plans for high growth economies such as India where the country has a goal to reach 100 GW of nuclear power capacity by 2047 (currently 8 GW) as part of its plans to reach net-zero emissions by 2070.

Physical uranium funds returned to substantial purchases, with Sprott Physical Uranium Trust and latterly Yellow Cake, injecting further momentum and the U3O8 spot price increased from its April low of $52/lb to $82/lb by end-September. As a result, sentiment swung decisively positive in the second half of the year, as illustrated by the Fund's NAV performance which rebounded 148% from its early April low to deliver a 33% gain for the year as a whole. This was comparable with the sterling return from the North Shore Uranium Miners Index that focuses on companies that devote 50% of assets to mining, developing or exploring for uranium.

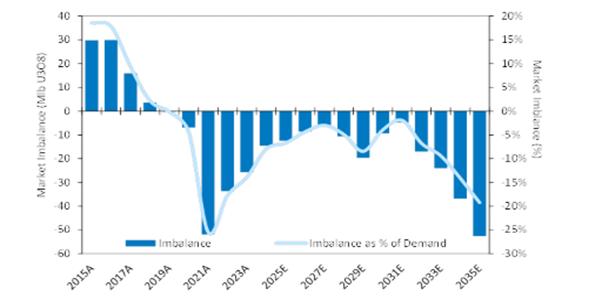

Uranium Supply Demand balance

The uranium market is in deficit today and this is set to widen over the next decade. This was illustrated by this years World Nuclear Association's ("WNA") Bi-annual supply demand assumption below.

New market balance - Sept 2025

It should also be noted that this industry-produced supply demand balance is an optimistic supply case, which we believe is unrealistic.

Firstly the cut off date for the supply assumption was June 2025, and did not capture production guidance downgrades that occurred after from;

· Kazatomprom, which warned ongoing acid shortage will likely lead to a miss on their subsoil approved allowance;

· Cameco's McArthur River mine in Canada, reducing guidance from 18Mlbspa to 14-15Mlbspa; or

· Paladin, which reduced guidance for FY26 to 4-4.4Mlbs following operational issues in ramp up.

This also assumes a number of unpermitted mines will come online, that are unlikely to meet that timeline. Already, we know Cameco will need to buy spot material in the market simply to cover their production shortfall and deliver into their existing supply contracts.

Small Modular Reactors ("SMR") advancements and the recent US reactor approvals were given minimal weighting from a demand perspective, which whilst they may be some years out, supply will need to be contracted years ahead of ultimate usage given western producers such as Cameco are fully contracted for the next five years.

Big tech and AI adding demand growth

Data centres currently account for 2-3% of US power demand but are set to grow rapidly given the hundreds of billions committed to new AI data centres. Nuclear, as a zero-carbon base load power, is perfect for the 24/7 operations whilst maintaining environmental credibility.

Incoming nuclear power can be split into two groups: near term reactor life extension/ restart, and future expansion. Both are positive, but in the near term it is the restarts and extensions that are most impactful on uranium spot price.

Some examples include;

• Meta (Facebook): 20 year power deal with US utility Constellation;

• Microsoft: 20 year deal with Constellation to restart Three Mile Island;

• Google: 7 SMR build with Kairos;

• Amazon: $350m deal with Talen Energy & SMR partnership with Dominion Energy; and

• Equinix / Oracle: investing in SMR's.

Geopolitics removing access to nuclear fuel for western reactors

Fears of a US-Russian thawing of tensions and possible easing of the nuclear fuel supply chain weighed heavily on sentiment during the first quarter of 2025. Current waivers allow Russian material to remain in circulation until the end of 2027, but western utilities remain focused on finding other sources of supply. Relations with Russia have since soured, with Putin refusing Trumps request for a ceasefire, leading to further US sanctions against state-owned Russian oil producers Lukoil and Rosneft. Russian material will increasingly head to China; given geopolitics and energy security requirements, China will likely buy and store all available material they can, effectively removing it from availability for western reactors.

The geopolitical strategic relevance is highlighted by the Russia/China influence dominated supply chain, versus the western weighted global reactor fleet. It is notable that the majority of Kazakhstan's uranium heads to China or Russia, given both the major land borders and China/Russia controlling approximately 70% of global conversion and enrichment.

Outlook - Utilities must increase purchases or risk reactor shutdowns

According to the IEA more than 40 countries now include nuclear energy in their strategies and are taking steps to develop new projects. There are estimated to be more than 70 GW of new capacity under construction currently, one of the highest levels in 30 years.

With the uranium supply deficit expected to widen, western utilities also currently have exceptionally low inventories and limited sources of available supply, and thus face possible fuel shortages over the next decade. This compounds the risks faced by nuclear power generators. This is especially the case in the US, where they currently stand precariously low with just 14 months of reactor needs, according to the latest information from the Energy Information Administration ("EIA").

Western government energy policy reforms, driven by both Net Zero concerns and ambitions of supply chain resilience, continue to have a marked impact on the nuclear power sector. As the largest nuclear power market currently, nowhere is reform more evident than in the US. In 2024 the US relied on imports for the supply of 90% of reactor needs, with Russia supplying approximately 20% of enriched fuel used in US reactors. In this context, western exploration, development and production of uranium for nuclear power is highly incentivised.

Accompanying supportive shifts in nuclear energy policies around the world, considerable funding is being directed at the sector to alleviate supply chain challenges. While this includes bottlenecked conversion and enrichment stages of the fuel manufacturing process, the relative absence of upstream financing for uranium miners which have endured decades of underinvestment, leaves U3O8 supply increasingly looking like a bottleneck over coming years.

In this regard Canada is prominent in its promotion of strategic energy projects, of which NexGen's Arrow project is a prime example. Coinciding with affirmative US action to develop regional new nuclear generating capacity, the combination of constrained supply, pick-up in global reactor roll-outs and favourable nuclear policy reforms continues to highlight the positive secular growth outlook.

US policy increasingly supportive of nuclear

US/China trade tensions have supported proactive policies towards nuclear power and critical minerals more widely, boosting investor interest in the uranium mining sector. Nuclear power is a key component of the US AI strategy and broader reindustrialisation policies of the US.

Specific to the nuclear power industry, Executive Orders were announced in Q2 to accelerate deployment of new nuclear capacity to help meet the ambitious plans to quadruple national generating capacity to 400GW by 2050. Since, the US government has also streamlined the regulatory approvals process, provided financing for the development of enrichment and conversion facilities along with some funding to help development of new reactor technologies. Simultaneously, the Trump administration has removed many incentives previously available to variable wind and solar generation, underscoring prioritisation of nuclear for Net Zero.

Elsewhere, the US government's direct investment into rare earth metals developer MP Minerals, accompanied by an agreement to guarantee premium prices for its products, spurred sentiment directly into rare earth related sectors. Often geologically associated with uranium, this also fed through to boost interest in the uranium mining sector. Notable beneficiaries of this sentiment included fund holding Energy Fuels which is seeking to develop some rare earth production capability at its White Mesa Mill alongside its prospective uranium activities.

While there has been considerable focus on US nuclear power policies it is also helpful that Japan's new prime minister is pushing to accelerate the revival of nuclear power in the region to help lower the inflationary pressures resulting from the importation of costly fuel imports, which in 2024 represented 10% of its total import spending with imported LNG and coal behind 60-70% of Japan's electricity generation.

Performance

The largest contributions to performance were from US in-situ miner Ur-Energy, Athabasca developer Nexgen and US uranium and rare earth developer Energy Fuels, whose share prices increased 148%, 55% and 294% respectively over the period. The Company has since divested its holding of UEC, following its strong performance and given the relatively opaque plans for its proposed development of conversion capacity, which make it difficult to value. For Energy Fuels, expectations that the US government could possibly copy its approach to investment in rare earth developer MP Minerals, whose share price has risen around 150% over the same period, drove the rerating. Such investment could allow the group to scale-up operations from its pilot plant which has produced small quantities of heavy rare earth metals.

Positioning

The Company remains weighted to developers relative to the uranium mining sector, with Nexgen as the largest component. This is to give full participation into future uranium price gains; where the likes of Cameco are largely contracted out for the next 5 years with a degree of fixed pricing, they will not see the full benefit of a stronger priced uranium market. The Company is underweight Cameco relative to the sector primarily for this reason, but also because Cameco are trading at a material premium at around 2x P/NPV, versus Nexgen at a closer to 1x at spot.

Positioning is thus focused on names that will benefit from stronger uranium pricing, and the anticipated upcoming increase in western reactor contracting. We believe these names offer the greatest return through the cycle as they are strategically the most significant for gaining both political and regulatory support. The focus on value over liquidity, we believe, presents the most attractive risk reward position.

Top 5 Holdings

Nexgen

· Key catalyst: Federal Permit hearing in February 26 - full permit should support a rerate.

· Largest high-grade deposit globally in tier 1 Canadian Athabasca basin.

· Already has provincial permit and first nations support.

· Uncontracted so has full participation in uranium price upside.

· Tier 1 jurisdiction - Canada Athabasca Basin.

· Parallel system discovered and depth extension not in market valuation assumptions.

Ur-Energy

· Largest US producer.

· Attractive valuation versus better marketed US peers.

· High spot uranium participation.

· Future beneficiary of supportive regulatory backdrop in the US as they need more uranium.

Paladin Energy

· Mostly spot price exposed - well placed for western reactor contracting.

· Producer in Namibia with development project adjacent to Nexgen in Canada's Athabasca basin.

· Attractive valuation.

Cameco

· The Company is underweight Cameco.

· Whilst richer in valuation, Cameco remains the go to big liquid name in the sector.

· Owns 49% of Westinghouse, with its leading AP-1000 reactor design is well placed to benefit from nuclear construction renaissance.

· Benefitting from strong uranium conversion pricing via exposure in Westinghouse.

Energy Fuels

· US producer of ~2M lbspa, with White Mesa Mill in Utah.

· Further expansion projects in the pipeline.

· Rare Earth and Vanadium resources as well make strategically important to US.

· US government funding for domestic rare earth supply with MP Materials may provide route for Energy Fuels support.

Robert Crayfourd and Keith Watson

CQS (UK) LLP

December 2025

Enquiries

|

Manulife | CQS |

Craig Cleland |

T: +44 (0) 20 7201 5368

|

|

Cavendish Capital Markets Limited |

Tunga Chigovanyika (Corporate Finance)

|

T: +44 (0) 20 7220 0557

|

|

|

Daniel Balabanoff / Pauline Tribe (Sales)

|

T: +44 (0) 20 7220 0500 |

|

Summit Fund Services Jersey Limited |

Christopher Foulds |

T :+44 (0) 1534 825 219 |

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.

Latest directors dealings

- 30 minutes ago Croda International

- 42 minutes ago IMI

- 43 minutes ago QinetiQ Group

- 1 hour ago Rotork

- 1 hour ago Schroders