Preliminary Results

Summary by AI BETAClose X

Fresnillo plc

Financial results for the year ended 31 December 2025

Fresnillo plc today announced its financial results for the full year ended 31 December 2025.

Octavio Alvídrez, CEO said:

"I am pleased to report a record financial performance in 2025, as Fresnillo continued to benefit from a high precious metals price environment, combined with our ongoing focus on operational consistency. These results demonstrate our ability to leverage our high-quality asset base while managing costs carefully to expand margins, resulting in significant cash generation and returns to our shareholders. I would like to thank our teams for their focus and execution throughout the period.

"We are today reporting a 27.6% increase in Adjusted Revenues to US$4.6 billion and an 80.7% rise in EBITDA to US$2.8 billion. In line with this robust performance, we are proposing a final ordinary dividend above the traditional policy of paying 50% of the adjusted profit, bringing total shareholder distributions for 2025 to US$950.0 million, or 128.92 US cents per share, our highest to date as a listed company.

"Operationally, silver production was in line with guidance and gold production exceeded expectations. We continued to implement structural improvements across our mines to support future production and effectively manage the cost base, while also laying the foundations for future growth by advancing our exploration projects and enhancing our pipeline through the announcement of the acquisition of Probe Gold.

"Looking ahead, we remain committed to responsible growth, with the safety of our people as our top priority. We will continue to monitor and manage costs, while advancing our exploration pipeline to support long-term value creation. Our financial position remains solid, with a net cash position of US$1,916.6 million, enabling us to invest in future growth while maintaining attractive returns to shareholders."

Financial Highlights - 12 months to 31 December 2025

|

$ million unless stated |

2025 |

2024 |

% change |

|

Silver Production1 (kOz) |

48,723 |

56,307 |

(13.5) |

|

Gold Production (Oz) |

600,287 |

631,573 |

(5.0) |

|

Total Revenue |

4,561.2 |

3,496.4 |

30.5 |

|

Adjusted Revenue2 |

4,645.3 |

3,639.9 |

27.6 |

|

Gross Profit |

2,664.1 |

1,246.3 |

113.8 |

|

EBITDA3 |

2,796.2 |

1,547.3 |

80.7 |

|

Profit Before Income Tax |

2,082.0 |

743.9 |

179.9 |

|

Profit for the year |

1,573.8 |

226.7 |

594.3 |

|

Basic and Diluted EPS excluding post-tax Silverstream effects (USD)4

|

2.058 |

0.364 |

465.4 |

|

|

|

|

|

1 Fresnillo attributable production, plus ounces registered in production through the Silverstream Contract.

2 Adjusted Revenue is revenue as disclosed in the income statement adjusted to exclude treatment and refining charges.

3 Earnings before interest, taxes, depreciation and amortisation (EBITDA) is calculated as gross profit plus depreciation less administrative, selling and exploration expenses. The reconciliation of EBITDA to amounts determined in accordance with IFRS can be found in the Financial Review.

4. The weighted average number of ordinary shares was 736,893,589 for 2025 and 2024 See note 18 in the consolidated financial statements.

2025 Highlights

Significantly increased profit margins and strong financial position underpinned by higher precious metal prices, operational discipline, and a continued focus on costs.

· Adjusted revenue of US$4,645.3 million, up 27.6% vs 2024 primarily due to the higher precious metals prices, mitigated by the lower volumes of all metals sold.

· Revenue of US$4,561.2 million, up 30.5% vs 2024 driven by the increase in adjusted revenue and lower treatment and refining charges.

· Adjusted production costs1 of US$1,406.7 million, down 11.1% vs 2024 primarily driven by the lower volumes processed at Herradura, Fresnillo, Ciénega and Saucito; the favourable effect of the devaluation of the average Mexican peso vs. US dollar exchange rate; the cessation of mining activities at San Julián DOB; and net efficiencies achieved, principally at Herradura.

· Gross profit of US$2,664.1 million, up 113.8%; EBITDA2 of US$2,796.2 million, up 80.7%.

· Exploration expenses of US$173.5 million, up 6.4%.

· Profit from continuing operations of US$2,292.5 million, up 142.4%. as a result of higher gross profit.

· Non-cash Silverstream loss, net of taxes, of US$132.4 million following the decision to end the Silverstream Contract in light of operational and financial difficulties impacting the long-term viability of the Sabinas mine.

· Income tax expense of US$315.0 million down 19.3% vs 2024, primarily as a result of the 11.4% revaluation of the spot Mexican peso vs. US dollar exchange rate on the tax value of assets and liabilities, the special mining rights deductible for corporate income tax.

· Mining rights of US$193.2 million, up 52.1% vs. 2024 due to the increase in the profit base used in the calculation along with the increase in the mining rights from 7.5% to 8.5% in 2025.

· Profit for the year attributable to equity shareholders of the Group of US$1,384.0 million vs US$140.9 million in 2024.

· US$2,756.5 million in cash and other liquid funds as of 31 December 2025. Net cash position of US$1,916.6 million as of 31 December 2025, compared with US$458.3 million as of 31 December 2024.

1 Adjusted production costs are calculated as cost of sales less depreciation, profit sharing, change in inventories and unproductive costs. The Company considers this a useful additional measure to help understand underlying factors driving production costs in terms of the different stages involved in the mining and plant processes, including efficiencies and inefficiencies as the case may be and other factors outside the Company's control such as cost inflation or changes in accounting criteria.

2 Earnings before interest, taxes, depreciation and amortisation (EBITDA) is calculated as profit for the year from continuing operations before income tax, less finance income, plus finance costs, less foreign exchange gain/(loss), less revaluation effects of the Silverstream contract and other operating income plus other operating expenses and depreciation.

Total 2025 dividend payment of US$950 million, or 128.92 US cents per share

· Total ordinary dividend for the year amounting to US$950.0 million, or 128.92 US cents per share, comprised of:

- The 2025 interim ordinary dividend of US$153.3 million, or 20.8 US cents per share, which was paid in September 2025, and

- The 2025 final ordinary dividend of 108.12 US cents per share, totalling US$796.7million.

· This is above the Group's traditional dividend policy to pay out 50% of the profit attributable to equity shareholders of the company after making certain customary adjustments to exclude extraordinary non-cash effects in the income statement, and was permitted by strong cash generation throughout the year, which resulted in a high cash balance at year end. The company continues to maintain a healthy cash balance to invest in growth focused projects, along with an additional buffer for any M&A opportunities that may present themselves in the future. The dividend policy remains unchanged.

Consistent operating performance with silver in line and gold ahead of guidance

· Full year attributable silver production of 48.7 moz in line with guidance (including Silverstream) decreased 13.5% vs. 2024, mainly due to the cessation of mining activities at San Julián DOB, the lower ore grade, decrease in volume of ore processed, and lower recovery rate at Ciénega, and the lower contribution from the Silverstream.

· Full year attributable gold production of 600.3 koz exceeded guidance, down 5.0% vs. 2024 primarily due to the lower ore grades and decreased volumes of ore processed at Saucito, Fresnillo and Herradura, and the lower contribution from Noche Buena.

· Full year attributable by-product lead and zinc production decreased vs. 2024, mainly due to: i) the lower ore grade and decreased volumes of ore processed at Fresnillo; ii) the cessation of mining activities at San Julián DOB; and iii) the discontinuation of zinc production at Ciénega from August 2025 onwards.

Continued focus on operational optimisation and efficiency-enhancing projects

· Significant efficiencies and cost reductions achieved at Herradura, and to a lesser extent at Ciénega, partly offset by an increase in cost at the Fresnillo district. The net operating efficiencies achieved in 2025 totalled US$13.8 million.

· Operational optimisation initiatives continued to progress at Fresnillo, including dilution control, improved mine planning and contractor rationalisation, with early benefits achieved. However, higher maintenance costs due to lower equipment availability, and increased consumption of explosives and milling balls more than offset the positive impact.

· Construction of supporting infrastructure and equipment placement at the Jarillas shaft in Saucito continued during the year. The shaft connection was deferred to 2026 to minimise disruption, it remains on track to be completed by 2027.

· Implementation of the San Julián optimisation plan, including cost-containment measures, continued.

· Efficient cost control, optimised drilling patterns, and improved mine cycles delivered a good performance at Herradura.

· Construction of the Carbon in Column facility continued with full operational capacity expected to be achieved in 2Q26, while the analysis for a new sulphide crushing circuit was completed, and detailed engineering for this facility and the Adsorption, Desorption and Recovery (ADR) plant is now underway.

Laying the foundations for future growth through our commitment to exploration and a disciplined approach to evaluate M&A opportunities

· Silver resources decreased 8.5% vs 2024 to 2.06bn oz, primarily driven by the implementation of the Reasonable Prospects for Eventual Economic Extraction (RPEEE) principle, in line with industry best practice, to classify mineral resources based on their expected future economic extraction.

· Gold resources increased 14.3% vs 2024 to 44.0 moz, primarily driven by the favourable impact of the higher price of gold at Herradura and the Lucerito exploration project.

· Proven reserves were reported at all mines.

· Silver reserves increased 9.4% to 362.6 million ounces, mainly due to higher metals prices and a lower cut-off grade together with the addition of ounces through the infill campaign, primarily at the Fresnillo district.

· Gold reserves increased 7.4% to 7.8 million ounces vs 2024, as a result of the higher gold price, principally at Herradura.

· Positive drilling results and higher gold prices increased mineral resources to 2.3 million ounces of gold at Rodeo. Ongoing drilling and metallurgical testwork continue to deliver a Preliminary Economic Assessment in 2H26.

· Several opportunities identified to optimise capex and operating costs at Orisyvo.

· An intensive core drilling programme was completed at Guanajuato, while land acquisition, and mine development and mineral processing evaluations continued. Total resources at our Guanajuato project amount to approximately three million ounces of gold, and 388 million ounces of silver.

· Acquisition of Probe Gold was successfully completed in 1Q26, providing immediate access to the prolific Val d'Or district in Quebec, with established infrastructure and a skilled workforce, and adding 10 million gold ounces to our resource base.

Safety remains our top priority as we further enhance the sustainability of our operations

· Improved TRIFR from 7.59 to 6.26 and decreased Fatality Frequency Rate to 0.046. However, the two fatalities recorded during the year underscore that further improvements are required.

· Consumed 77.8% of electricity from renewable sources (2024: 80.6%).

· Generated a positive economic impact[1] of US$2,173.8 million in 2025.

2026 outlook and longer term prospects

· Attributable silver production expected to be in the range of 42.0 to 46.5 moz.

· Attributable gold production expected to be in the range of 500 to 550 koz.

· Expressed in silver equivalent ounces2, production is expected to be 82-91 million ounces.

· Capex for 2026 is anticipated to be approximately US$765 million and will continue to be primarily focused on mining works, sustaining capex, optimisation projects at Herradura, the deepening of the Jarillas shaft at Saucito, a haulage conveyor at Juanicipio, and tailings dams.

· Exploration expenses are expected to be c.US$260 million, supporting intensified drilling at our operating mines, continued de-risking our advance exploration projects, and starting drilling at Probe Gold.

· Continue to monitor costs closely and capture further efficiencies where possible.

· Continue working towards reducing our TRIFR to the ICMM range and achieve zero fatal accidents.

Board Committee changes

Fresnillo plc announces that its Board of Directors, on the recommendation of the Nominations Committee has approved a change to the composition of the Health, Safety, Environment and Community Relations (HSECR) Committee effective as at 2 March 2026.

Ms Luz Adriana Ramírez has been appointed as an additional member of the HSECR Committee. She currently is an Independent Non-Executive Director.

Ms Ramírez has experience in health, safety, environment and community relations issues at an executive level as well as being a member of related committees in other relevant companies and the Board believes that she brings valuable insight to the work of the HSECR Committee.

Analyst Presentation

Fresnillo plc will be hosting a webcast presentation for analysts and investors today at 9:00am (GMT). A link to the webcast will be made available on Fresnillo's homepage: www.fresnilloplc.com or can be accessed directly here: https://brrmedia.news/FRESFY25

To dial in via a phone line, please use the below dial-in details:

|

Conference call dial-in numbers: |

UK-Wide: +44 (0) 33 0551 0200 UK Toll Free: 0808 109 0700 USA Local: +1 786 697 3501 USA Toll Free: 866 580 3963 Gabriela Mayor, Head of Investor |

|

Password (if prompted): |

Please quote 'Fresnillo FY25 Results' when prompted by the operator

|

For further information, please visit our website: www.fresnilloplc.com or contact:

|

Fresnillo plc |

|

|

London Office Gabriela Mayor, Head of Investor Relations Mark Mochalski

|

Tel: +44(0)20 7339 2470

|

|

Mexico City Office Ana Belém Zárate |

Tel: +52 55 52 79 3206

|

|

|

|

|

Sodali Peter Ogden |

Tel: +44(0)7793 858 211 |

About Fresnillo plc

Fresnillo plc is the world's largest primary silver producer and Mexico's largest gold producer, listed on the London and Mexican Stock Exchanges under the symbol FRES.

Fresnillo plc has eight operating mines, all of them in Mexico - Fresnillo, Saucito, Juanicipio, Ciénega, Herradura, Soledad-Dipolos1, Noche Buena and San Julián Veins and five advanced exploration projects - Orisyvo, Rodeo, Guanajuato, Tajitos, and Novador, as well as a number of other long term exploration prospects.

Fresnillo plc has mining concessions and exploration projects in Mexico, Peru and Chile.

Fresnillo plc's goal is to maintain the Group's position as the world's largest primary silver company and Mexico's largest gold producer.

1 Operations at Soledad-Dipolos are currently suspended

Chairman's statement

Alejandro Baillères

Capitalising on today's opportunities, focusing on the future

This was an exceptional year for Fresnillo. Our efforts to boost performance and reduce costs bore fruit and enabled us to achieve production and efficiency targets, while a positive price environment drove a significant increase in revenue.

When we first looked ahead to 2025, our initial thoughts were that it could be challenging to surpass the achievements of 2024. However, a number of key factors came together during the year to generate one of the most rewarding periods in Fresnillo's history.

Our teams worked hard to address factors within our control, improving performance, reducing costs and achieving production goals. Meanwhile, external factors led to significant increases in the prices of precious metals - and we have been able to capitalise on this positive tailwind.

However, there is no room for complacency. Towards the end of the year we announced an important acquisition which has expanded our presence into an exciting new territory and bolstered our already promising pipeline. In addition, our performance and cost reduction initiatives continue at pace - and these will help to underpin future performance regardless of external factors.

Strong operational performance

Production of silver and gold were again in line with guidance. In fact we exceeded our target for gold - with the team at Herradura continuing to execute our plans consistently and with great expertise. Silver production was towards the lower end of guidance, with performances above expectations at Juanicipio and San Julián Veins and the recovery that began at Saucito in 2024 beginning to show positive signs.

We achieved US$4,645.3 million in Adjusted revenue during the year. This represented an increase of 27.6%, primarily due to the increase in silver and gold prices. Gross profit increased 113.8% year-on-year to US$2,664.1 million, mainly driven by higher adjusted revenue and decreased costs, the latter primarily due to lower volumes processed at some of our operations, including at San Julián DOB following its closure, the devaluation of the average exchange rate between the Mexican peso and US dollar, and cost reduction initiatives and efficiencies.

These factors partially offset inflationary headwinds during the year. Cash and other liquid funds increased from US$1,297.8 million to US$2,756.5 million primarily driven by cash generated from our mining operations, which more than offset the use of funds in capital expenditure, dividend payments, taxes and mining rights.

Through the good times as well as those that prove more difficult our dividend policy has remained stable and well-respected. It is the basis for continued shareholder returns while also supporting the growth of the company. We aim to pay out 33-50% of profit after tax each year, while making certain adjustments to exclude non-cash effects in the income statement. Dividends are paid in the approximate ratio of one-third as an interim dividend and two-thirds as a final dividend. Before declaring a dividend, the Board carries out a detailed analysis of the profitability of the business, underlying earnings, capital requirements and cash flow. Our goal is to maintain enough flexibility to be able to react to movements in precious metals prices and seize attractive business opportunities. During 2025, for example, our strong balance sheet and healthy cash position facilitated the proposal to acquire Probe Gold Inc.

The Board also considers paying special dividends in cases where we build up a large cash balance, considering any extraordinary needs for cash, such as the aforementioned acquisition, along with the outlook for metals prices and expected cash generation in future periods.

For 2025, we declared an interim ordinary dividend of 20.8 US cents per share, with a final ordinary dividend of 108.12 US cents per share, bringing the total for the year to 128.92 US cents per share.

Making the most of today's opportunities…

In my statement last year, I reported that cost reduction and operational initiatives had already had a beneficial impact, and I am pleased to say that this continued through 2025, and we have again succeeded in managing our costs while improving productivity.

Our efforts were significantly strengthened by a very positive price environment, which was a major factor in the year's financial performance. The price of gold hit all-time highs, while that for silver more than doubled, following an increase of 21 per cent in 2024.

However, while we met our production objectives during the year, we failed to succeed on the one measure that is unquestionably our most important: safety. Despite achieving our lowest TRIFR (total recordable injury frequency rate) and LTIFR (lost time injury frequency rate) since 2018, it is with great sadness that I must report two fatalities in 2025, one unionised employee and one contractor. Everybody at Fresnillo recognises that we can - and indeed we must - do better.

…while focusing on the future

As expected, the political climate in Mexico has moved into more positive territory following the appointment of the government led by President Claudia Sheinbaum. Although clear direction is still required in some areas, such as permitting for mining activities, the new administration is proving to be broadly receptive to the business community. We are cautiously confident that this new mood will continue into 2026 and beyond, underpinning our continued commitment to the environment and supporting the development of the communities in which we operate.

Our future focus includes further cost reduction initiatives and operational efficiencies across the business, and these will be complemented by an exploration pipeline that is expected to yield at least one and possibly more projects that can move into our development portfolio within the next two to three years.

The pipeline was enhanced during 2025 by our move to acquire of Probe Gold Inc., a leading Canadian exploration company focused on the acquisition, exploration, and development of highly prospective gold properties. Following extensive due diligence to ensure it had the potential to add considerable long-term value for our shareholders, we concluded the deal in January 2026 for an all-cash consideration of CAD$3.65 per share. The total equity value of the transaction was approximately CAD$770 million, (approx. US$555 million) on a fully diluted basis.

The acquisition of Probe is consistent with the disciplined approach to M&As that we have consistently set out over time - including in my statement last year - and meets our strict criteria of having a sizeable resource base with upside optionality in a mining-friendly region with mining history, skilled personnel, and existing infrastructure. Exploration is in the DNA of both companies and we look forward to working closely together as we advance the exciting Novador project. The Fresnillo team has visited the Probe site on several occasions and has met directly with stakeholders including employees, First Nations representatives and local, provincial and federal authorities.

Board activities

Our regular Board meetings provide the opportunity for members to explore and discuss a wide range of issues that impact the business. These include operational matters and the prevailing political landscape at home and abroad, amongst others. Key decisions this year have included the special dividend, the decision to end the Silverstream Agreement, and the agreement to acquire Probe. There was also considerable focus on safety, culture, the ERP system, cyber security and cost reduction.

As in previous years, one of the highlights of 2025 was the three-day Working Meeting in Mexico, which was held in July and provided a significant opportunity for the Board to engage with longer-term strategic and stakeholder issues. The meeting included a visit to Herradura, where we were able to see for ourselves the tremendous improvements that the local team has been implementing.

Changes to the Board

There were no Board changes during the year. A number of significant developments for which the Audit Committee is responsible remain ongoing. The Nomination Committee has therefore proposed that at the 2026 AGM, Alberto Tiburcio (who was appointed to the Board in May 2016 and has chaired the Audit Committee since 2018) should again stand for re-election as an Independent Non-Executive Director for one further year.

In addition, the Board is recommending the re-election of Dame Judith Macgregor as an Independent Non-Executive Director at the 2026 AGM, notwithstanding that she will reach the ninth anniversary of her appointment to the Board soon after that AGM. In view of the other Board changes being made this year, we consider that it will be highly beneficial to the Company for her to serve one further year in her role as Senior Independent Director.

We will be consulting with shareholders concerning the proposed re-election of both Alberto and Dame Judith before publication of the notice of meeting for the 2026 AGM.

Outlook

Uncertainty will in all likelihood continue to be the watchword regarding global geopolitics, with ongoing conflicts such as the wars in Ukraine and the Middle East being exacerbated by heightened tensions between the US, China and Russia, along with developments in Venezuela that will have important implications for the whole region. We expect tariffs to remain a key issue for international trade, although these may evolve to become more negotiated and targeted.

The acquisition of Probe Gold Inc. has expanded our presence into Canada and the broader Western Hemisphere through our activities in Peru and Chile. However, Mexico remains central to our operations, and we will continue to engage proactively with the Government.

The new administration's more business-friendly approach has already had a positive impact on our industry, and we anticipate that this might further strengthen in the coming months.

In terms of our operations, our teams will again work hard to maintain and enhance the initiatives that have driven stable production and cost efficiencies in recent months. We will also focus on moving the most promising advanced exploration projects further along our pipeline.

We expect the high price environment for silver and gold to be maintained following the structural shift in prices seen in 2025. Advanced technologies, notably those around the energy transition, are underpinning sustained strength in silver prices. At the same time, ongoing global uncertainty is leading many investors to seek safe haven assets, offering further support to both gold and silver prices. Looking ahead, demand is forecasted to continue to exceed supply.

I am confident that we have the people, the strategy and the determination to capitalise on the many opportunities that will be presented in the months and years to come. Following a year when Fresnillo recorded a set of exceptional results, our ambitions to continue to deliver on our promises - to meet expectations and where possible go beyond them - burn as brightly as ever.

I would like to end by putting on record my gratitude to all our stakeholders - including those working in the supply chain and in government, as well as local communities, investors and, of course, our talented workforce - for their support over the past 12 months.

Alejandro Baillères

Chairman

Chief Executive's statement

Octavio Alvídrez

Exceptional performance in a positive price environment

I am delighted to report on what was an outstanding year for Fresnillo, as we continued to execute our long-term strategy. The tremendous efforts of our teams were complemented by sustained high prices for precious metals, with gold in particular reaching all-time highs.

2025 saw our Company deliver strong operating and financial results. Profitability increased on the back of our unrelenting focus on operational efficiencies supported by rigorous cost discipline and given added momentum by very favourable prices for precious metals. The outcome was the generation of substantial free cash flow and a robust balance sheet with ample liquidity.

Our people again demonstrated their deep-seated commitment to the Company's Purpose to contribute to the wellbeing of people through the sustainable mining of silver and gold. Their continuing dedication and expertise will be crucial in the years ahead, as a number of projects in our exciting pipeline move towards becoming operational mines.

At the same time, we must strengthen our safety performance. While most of our indicators continued to improve, two fatalities overshadowed that progress. These incidents are painful reminders that zero fatalities is the only acceptable outcome, and that our first and most important responsibility is to ensure the safety of our colleagues.

Production highlights and price review

Total gold production was 600.3 koz, above our guidance range and, as expected, down by 5.0% from 631.6 koz in the previous year. This was primarily due to the lower ore grade and decreased ore throughput at Saucito and Fresnillo, as well as at Herradura, where performance nevertheless exceeded original plans.

Total silver production of 48.7 moz was towards the lower end of the guidance range, down by 13.5% from 56.3 moz in 2024. While the ongoing turnaround at Saucito has started to deliver the anticipated outcomes, there remain significant opportunities for further

improvement. However, both production and ore grades were above plan at Juanicipio and San Julián Veins, helping to offset challenges elsewhere, including at Ciénega and Fresnillo.

Attributable by-product lead and zinc production decreased year-on-year, mainly due to the lower ore grade and volumes of ore processed at Fresnillo and the cessation of mining activities at San Julián DOB.

During 2025, silver and gold prices increased markedly for the third consecutive year. The average realised silver price was US$43.6 per ounce, up by 51.4%, while the price of gold hit record highs, rising by 44.0% to US$3,532.7 per ounce during the year. Average prices for zinc increased by 3.2% while those for lead decreased by 5.3%.

Demand for silver and gold is continuing to outstrip supply, with the key drivers of demand indicating good levels of support for prices in the medium term. The world's increasing reliance on advanced technologies, particularly those associated with the energy transition, is a major factor in demand for both silver and gold. Silver is essential to a wide range of applications from electric vehicle batteries and solar panels to 5G telecommunications, and also in the food, medical and electronics sectors. Towards the end of 2025, the importance of silver was underlined when the US and Chinese governments officially categorised it as one of the world's essential metals.

Gold is a key component in consumer electronics as well as in rapidly growing areas such as the automotive, aerospace and high-speed computing industries. In addition, demand for gold - and increasingly also for silver - as a safe haven has remained robust, among central banks as well as individual investors.

Executing our strategy

Our strategy has been well defined and consistently applied for many years. It is based on four strategic pillars that together enable us to maintain and, where possible, enhance our track record of seizing the opportunities of today while also preparing for the future.

Maximising the potential of existing operations

Improving the productivity and efficiency of our operational mines has been the subject of great focus over the last two to three years. While some of our operations are yet to fully achieve their targets, the trend is positive.

In last year's report, our Chief Operating Officers outlined a number of specific plans to deliver greater efficiency and cost control in their respective regions. In the Central Region, for example, a key task was to consolidate operations at Juanicipio, confirm the turnaround at Saucito and focus on greater control of the factors affecting ore grades at Fresnillo. Successful actions against the first and second of these priorities formed the basis for the region's silver production in 2025, with Juanicipio performing above plan. MAG Silver, our joint venture partner at Juanicipio, was acquired by Pan American during the year, and we have already started to work closely with them to ensure that Juanicipio continues to fulfil its outstanding potential.

At the Fresnillo mine, challenges are proving more complex to overcome. Although ore grades improved, we processed a lower volume of mineral during the year due to reduced contributions from deeper, narrower and more distant veins. However, the San Carlos shaft is now beginning to reduce haulage costs for the substantial amounts of ore we expect to mine from these areas in the coming years.

At our operations in the Northern Region of Mexico, several improvement initiatives have already paid dividends. Gold production at San Julián Veins increased due to a greater volume of ore processed, driven by the disciplined execution of plans to optimise plant operation . At Herradura, we have continued the transformation that began in 2024, controlling costs and focusing on planning and execution, including the recovery of gold content from the oxidised high-grade ore deposited at the leaching pads. Our plans to commence underground activities at Herradura have progressed well, with mining works expected to commence in 2026 and production set to follow early in 2027. We experienced challenges at Ciénega, where production decreased compared to 2024. Nevertheless, we remain confident in the mine's future, and expect cost control measures, operational efficiencies and a renewed exploration programme to successfully extend Ciénega's life beyond 2028.

Delivering growth through development projects

Although none of the projects discussed in the following section are yet quite ready to move out of the exploration phase and become standalone development projects, I look forward to reporting further progress in next year's Annual Report.

Extending the growth pipeline

We currently have six advanced exploration projects in our pipeline, an increase of two compared to this time last year.

A historic, world-class gold and silver epithermal vein field, our Guanajuato project stretches more than 40 kilometres along the central Mexican state from which it takes its name and is expected to make an important contribution to the Group's future silver production. During 2025, exploration concentrated on the southern part of the district where we drilled 107,759 metres. We continued to carry out scoping level studies as well as community engagement programmes which have already delivered access to key sections of land required for the project.

We remain moderately confident in the potential of our underground gold project at Orisyvo, despite the significant capital expenditure on infrastructure - including roads, tailings storage facilities, accommodation camps and land access - required to bring it to fruition. Following a review at the end of 2025 into the results of pre-feasibility studies, we are identifying possibilities to improve the project's cost-effectiveness and anticipate presenting next stage proposals to the Board for approval in the second half of 2026.

At Rodeo, an open pit, heap leaching gold project in central Durango state, we aim to finalise exploration activities in the first half of 2026. Over 5,000 metres have now been collared, proving good continuity of the ore bodies. Results of a preliminary economic assessment are expected in mid-2026, giving us greater visibility of considerations including development layout, water and energy supply as well as key technical issues.

Exploration continued progressing at the Tajitos gold project. In 2025 the Mexican government began to grant permits for open pit mining, and this has removed a degree of uncertainty for the project, paving the way for the new preliminary economic assessment that we expect to conclude early in 2026.

We also made encouraging progress with our project at Lucerito during 2025, and this has now joined Guanajuato, Orisyvo, Rodeo and Tajitos in the advanced exploration project pipeline. More than 9,100 metres of drilling were carried out at Lucerito over the last 12 months, and we have good grounds to believe that the ore body there includes extensive resources with a positive combination of gold, silver and zinc.

Our pipeline has been further enhanced by the acquisition, after the year end, of Probe Gold Inc. Probe's assets include the Novador Gold Project, as well as the early-stage Detour Gold project, both located in Quebec, Canada. In addition to providing us with strategic entry into a world class Tier 1 mining jurisdiction, Probe adds a large resource base of 10 million ounces of gold. Novador alone has the potential to produce over 200,000 ounces per annum over 10+ years, and we are confident that this project, together with our advanced exploration projects in Mexico, will underpin Fresnillo's long-term future, further positioning us as one of the leading precious metals companies in the world.

Exploration continued across the portfolio during the year, with positive results yielded by brownfield exploration around the Fresnillo and San Julián districts and by greenfield drilling at Candameña, in addition to activities at those projects already mentioned. We also continued to make progress at our mining concessions in South America. In Chile, we completed 1,654 metres of drilling at Capricornio, a joint-venture project with SQM, while in Peru we drilled 2,058 metres at the Chiclayo project, with modest results, and strengthened our community relations plan.

At the end of the year, silver in consolidated overall mineral resources decreased by 8.5% vs 2024 to 2.06bn oz. This was mainly due to

the application of a new approach, in line with industry best practice, to classify mineral resources based on their expected future economic extraction, which, although initially reduces the reported resource base, enhances transparency and strengthens long-term confidence in the estimates. Gold in consolidated overall mineral resources increased by 14.3% vs 2024 to 44.0 moz, primarily driven by the favourable impact of the higher price of gold at Herradura and the Lucerito exploration project.

Silver in consolidated overall ore reserves increased by 9.4% to 362.6 moz, mainly due to higher metals prices and a lower cut-off grade together with the addition of ounces through the infill campaign, primarily at the Fresnillo district. Gold in consolidated overall ore reserves increased by 7.4% to 7.8 moz as a result of the higher gold price, principally at Herradura.

Advancing and enhancing the sustainability of our operations

Thanks to the commitment of our teams, we have achieved steady progress in our safety journey since 2018, with a 69% decrease in TRIFR (total recordable injury frequency rate) and 51% in LTIFR (lost time injury frequency rate). The last year alone saw those indices decrease by 17.6% and 13.7%, respectively. However, such progress cannot outweigh the loss of life. The two fatal accidents we experienced during the year-one involving a unionised employee and one a contractor-completely eclipse the gains. Our thoughts are with their families, friends and colleagues. These tragedies underline the fact that our work is far from finished: we can never be complacent about safety.

We have examined both incidents thoroughly and have begun to implement the appropriate corrective actions to support our goal of zero fatalities. Although mining carries intrinsic risks, we have the systems, the training and the leadership to manage and mitigate them. Ultimately, however, safety requires every person to fully embrace their responsibility-taking ownership not only of their own wellbeing, but also that of their colleagues. This principle is the foundation of our 'I Care, We Care' strategy.

As I reported last year, the new government administration has shown a greater openness to dialogue with the mining industry. These exchanges have reinforced that sustainability-related issues, including those most critical to local communities, are central in advancing Mexico's environmental and social policy agenda-from implementing the National Agreement for Forests, Jungles and Mangroves to reducing GHG emissions by 35% by 2030 and safeguarding the fundamental right of access to water. On key sustainability matters such as these, Fresnillo has been - and will continue to be - a strategic partner.

On the decarbonisation front, we remain focused on sourcing 75% of our energy consumption from renewables. While we have consistently surpassed this target in recent years - including in 2025 - we recognise that it will become increasingly challenging as exploration projects transition into operation and demand more energy. We remain committed to ensuring that our environmental ambition keeps pace with our business growth and that our energy supply remains reliable, competitive and grounded in clean sources.

We have decided to pause the dual fuel project at Herradura, which introduced several LPG-diesel trucks into the haulage fleet. Shifts in price and performance dynamics mean that, unless conditions change significantly, we will retire these units at the end of their operational life and either revert to a diesel fleet or explore other technologies, such as electric trucks.

Mining operations not only require large quantities of water but are also frequently situated in arid locations where the population is already experiencing a high degree of water stress. Over the years we have advanced a range of initiatives to reduce our water footprint and support infrastructure and sanitation for local communities. For example, in 2025 the Proaño Potabilisation Water Plant was inaugurated in partnership with the municipal government of Fresnillo. This project diverts and treats mine water from the Fresnillo mine to supplement the local potable water system.

Having exceeded our 2025 targets for the representation of women in both our total workforce and managerial positions a year ahead of schedule, we have now begun defining the next stage of our ambition. Inclusion is a great source of strength and essential for attracting and developing the best talent at a time when we are preparing for a new phase of growth-both within Mexico and beyond.

Looking ahead

We have indicated that production of silver and gold from our current operations is expected to reduce in 2026, largely due to geological factors at our operating assets. The goal is to improve the quality of the ounces we produce by continuing to implement the wide range of initiatives introduced by Tomás Iturriaga and Daniel Diez, our Chief Operating Officers, to increase efficiency and reduce costs. At the same time, we will aim to move all five of the advanced exploration projects further along our pipeline. We believe that all of these projects show good potential - the goal now is to identify and promote those that are best suited to the current economic and operational situation, and I anticipate being able to provide a positive update in next year's Annual Report.

More generally, cost control will continue to be a focus in 2026, given cost pressures globally and the strength of the Mexican peso. On the other hand, we anticipate that our operational performance will be enhanced by the continuation of a high price environment for silver and gold, with global production failing to meet the steady increase in demand for both metals.

Our optimism is based on experience and an understanding of both known and unforeseen challenges, which we address through careful planning, precise execution, and risk mitigation.

Finally, I would like to pay tribute to the fine work of our teams, who worked with great skill and determination to execute our strategy over the last 12 months. I thank them unreservedly. The exceptional results we have posted this year would not have been possible without them.

Octavio Alvídrez

Chief Executive

FINANCIAL REVIEW

"The Group's financial performance in 2025 reflects the positive impact of higher precious metals prices together with a more stable operational performance."

The consolidated financial statements of Fresnillo plc are prepared in accordance with UK-adopted international accounting standards. This financial review intends to explain the main factors affecting performance as well as provide a detailed analysis of the financial results in order to enhance the understanding of the Group's financial statements. All comparisons refer to 2025 figures compared to 2024, unless otherwise noted. The financial information and year-on-year variations are presented in US dollars, except where otherwise indicated.

The following report presents how we have managed our financial resources.

Commentary on financial performance

The Group's financial performance in 2025 reflects the positive impact of higher precious metals prices coupled with a more stable operational performance, which was achieved despite a number of challenges.

Adjusted revenue1 increased 27.6% vs 2024 to US$4,645.3 million. This was primarily due to higher gold and silver prices. Revenue increased 30.5% year-on-year to US$4,561.2 million, principally due to the same factors as the increase in Adjusted revenue and lower treatment and refining charges.

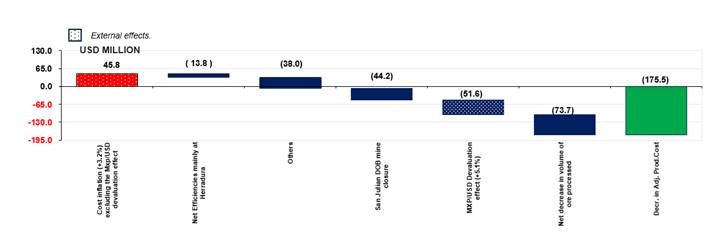

Adjusted production costs 2 decreased 11.1% vs 2024. This was mainly due to the cessation of mining activities at San Julián DOB; the lower volumes processed at Herradura, Fresnillo, Ciénega and Saucito; the favourable effect of the devaluation of the average Mexican peso vs. US dollar exchange rate; and net efficiencies achieved, principally at Herradura. These factors were partly offset by cost inflation of 3.2%, excluding the exchange rate devaluation.

As a result, gross profit more than doubled to US$2,664.1 million, while EBITDA3 increased by 80.7% to US$2,796.2 million in 2025.

We maintained our strong financial position, with US$2,756.5 million in cash and other liquid funds as of 31 December 2025, a net increase of US$1,458.7 million over the period, having paid dividends of US$654.3 million: US$346.3 million in accordance with our policy (adjusted for extraordinary, non-cash items, in particular the revaluation of the Silverstream contract and the effect of the exchange rate on deferred taxes), in addition to US$308.0 million in extraordinary dividends. We also invested US$400.1 million in capex, spent US$173.5 million on exploration expenses, and paid US$369.5 million in taxes, special mining rights, and profit sharing.

FINANCIAL REVIEW CONTINUED

Income statement highlights

|

|

2025 US$ million |

2024 US$ million |

Amount change US$ million |

Change % |

|

Adjusted revenue1 |

4,645.3 |

3,639.9 |

1,005.4 |

27.6 |

|

Total revenue |

4,561.2 |

3,496.4 |

1,064.8 |

30.5 |

|

Cost of sales |

(1,897.1) |

(2,250.1) |

353.0 |

(15.7) |

|

Gross profit |

2,664.1 |

1,246.3 |

1,417.8 |

113.8 |

|

Exploration expenses |

173.5 |

163.0 |

10.5 |

6.4 |

|

Operating profit |

2,292.5 |

945.8 |

1,346.7 |

142.4 |

|

EBITDA3 |

2,796.2 |

1,547.3 |

1,248.9 |

80.7 |

|

Special mining rights |

193.2 |

127.0 |

66.2 |

52.1 |

|

Income tax (Tax income) |

315.0 |

390.2 |

(75.2) |

(19.3) |

|

Profit for the period |

1,573.8 |

226.7 |

1,347.1 |

594.2 |

|

Profit for the period, excluding post-tax Silverstream effects |

1,706.3 |

354.3 |

1,352.0 |

381.6 |

|

Basic and diluted earnings per share (US$/share)4 |

1.878 |

0.191 |

1.687 |

883.2 |

|

Basic and diluted earnings per share, excluding post-tax Silverstream effects (US$/share) |

2.058 |

0.364 |

1.694 |

465.4 |

1 Adjusted revenue is revenue as disclosed in the income statement adjusted to exclude treatment and refining charges.

2 Adjusted production costs are calculated as cost of sales less depreciation, profit sharing, change in inventories and unproductive costs. The Company considers this a useful additional measure to help understand underlying factors driving production costs in terms of the different stages involved in the mining and plant processes, including efficiencies and inefficiencies, as the case may be, and other factors outside the Company's control such as cost inflation or changes in accounting criteria.

3 Earnings before interest, taxes, depreciation and amortisation (EBITDA) is calculated as profit for the year from continuing operations before income tax, less finance income, plus finance costs, less foreign exchange gain/(loss), less revaluation effects of the Silverstream contract and other operating income plus other operating expenses and depreciation.

4 The weighted average number of Ordinary Shares was 736,893,589 for 2025 and 2024. See Note 18 to the consolidated financial statements.

The Group's financial results are largely determined by the performance of our operations. However, other factors beyond our control, including a number of macroeconomic variables, also affect our financial results. These include:

Metals prices

The average realised silver price increased 51.4% from US$28.8 per ounce in 2024 to US$43.6 per ounce in 2025, while the average realised gold price rose 44.0% to US$3,532.7 per ounce. The average realised zinc by-product price increased 1.6% to US$1.30 per pound, with the lead by-product price decreasing 4.6% vs 2024 to US$0.88 per pound.

MX$/US$ exchange rate

|

Spot exchange rate at 31 December 2025 |

Spot exchange rate at 31 December 2024 |

Impact |

|

$18.00 per US dollar |

$20.27 per US dollar |

The 11.4% spot revaluation had a favourable effect on deferred taxes and special mining rights |

|

Average Mexican peso/US dollar exchange rate 2025 |

Average Mexican peso/US dollar exchange rate 2024 |

Impact |

|

$19.22 per US dollar |

$18.30 per US dollar |

The 5.1% devaluation had a positive effect of US$51.6 million on the Group's costs denominated in Mexican pesos (approximately 45% of total costs) when converted to US dollars. |

Cost inflation

The Mexican Consumer Price Index for 2025 calculated cost inflation at 3.9%. However, to evaluate the Group's cost inflation for the year, we calculate the unit price increase for each component of adjusted production costs and take into consideration their weighted average within the Group's basket. The resulting cost deflation estimate for 2025 was 0.2%, which included the favourable effect of the 5.1% average devaluation of the Mexican peso against the US dollar. Underlying cost inflation (cost inflation excluding the devaluation of the Mexican peso vs. US dollar) was 3.2%. We conduct the same exercise for each individual mine operation, whose basket components may carry different weightings.

The main components driving our cost inflation are listed below:

Labour

Unionised workers received on average a 7% increase in wages in Mexican pesos, while non-unionised employees received on average a 6% increase in wages in Mexican pesos; when converted to US dollars this resulted in a weighted average labour inflation of 1.5%.

Energy

Electricity

The weighted average cost of electricity in US dollars remained broadly stable at US$8.18 cents per kW in 2025.

Diesel

The weighted average cost of diesel decreased 4.0% in US dollars to 107.4 US cents per litre in 2025, compared to 111.9 US cents per litre in 2024.

Operating materials

|

|

Year-on-year change in unit price % |

|

Steel balls for milling |

4.3 |

|

Sodium cyanide |

4.1 |

|

Explosives |

3.3 |

|

Tyres |

1.7 |

|

Other reagents |

1.3 |

|

Steel for drilling |

(2.6) |

|

Lubricants |

(7.6) |

|

Weighted average of all operating materials |

2.2 |

The weighted average unit prices of all operating materials increased by 2.2% over the year as the unit prices of steel balls for milling, explosives and reagents, including sodium cyanide, continued to increase in US dollar terms, reflecting global inflationary pressures. This was partly offset by the decrease in the unit price of lubricants. There has been no significant impact on the unit cost of operating materials from the devaluation of the Mexican peso/US dollar exchange rate as the majority of these items are dollar-denominated.

Contractors

Agreements are signed with each individual contractor company and include specific terms and conditions that cover not only labour, but also operating materials, equipment and maintenance, among others. Contractor costs are mainly denominated in Mexican pesos and are an important component of our total production costs. In 2025, increases per unit (i.e. per metre developed/per tonne hauled) granted to contractors whose agreements were due for review during the period, resulted in a weighted average decrease of approximately 1.3% in US dollars, after considering the devaluation of the Mexican peso vs the US dollar.

The effects of the above external factors, combined with the Group's internal variables, are further described below through the main line items of the income statement.

Revenue

Consolidated revenue

|

|

2025 US$ million |

2024 US$ million |

Amount US$ million |

Change % |

|

Adjusted revenue1 |

4,645.3 |

3,639.9 |

1,005.40 |

27.6 |

|

Treatment and refining charges |

(84.1) |

(143.6) |

59.50 |

(41.4) |

|

Total revenue |

4,561.2 |

3,496.4 |

1,064.80 |

30.5 |

1 Adjusted revenue is revenue as disclosed in the income statement adjusted to exclude treatment and refining charges and metals prices hedging.

Adjusted revenue increased by US$1,005.4 million, driven by the higher gold and silver prices, partly offset by the lower volumes of all metals sold. Changes in the contribution by metal were the result of the relative changes in metals prices and volumes produced. The effect by metal, both in terms of volume and price, is shown in the table below.

Adjusted revenue1 by metal

|

|

2025 |

2024 |

||||||

|

|

US$ million |

% contribution |

US$ million |

% contribution |

Volume variance US$ million |

Price variance US$ million |

Total net changeUS$ million |

Change % |

|

Gold |

2,071.2 |

44.6 |

1,514.7 |

41.6 |

(93.0) |

649.4 |

556.5 |

36.7 |

|

Silver |

2,161.9 |

46.5 |

1,673.9 |

46.0 |

(309.9) |

797.9 |

488.0 |

29.2 |

|

Lead |

124.6 |

2.7 |

139.8 |

3.8 |

(9.0) |

(6.2) |

(15.2) |

(10.9) |

|

Zinc |

287.6 |

6.2 |

311.5 |

8.6 |

28.8 |

4.9 |

(23.9) |

(7.7) |

|

Total Adjusted revenue |

4,645.3 |

100.0 |

3,639.9 |

100.0 |

(440.8) |

1,446.1 |

1,005.4 |

27.6 |

1 Adjusted revenue is revenue as disclosed in the income statement adjusted to exclude treatment and refining charges and metals prices hedging.

Adjusted revenue by mine

The contribution by mine to Adjusted revenues is outlined in the table below. This is expected to change further in the future, as new projects are incorporated into the Group's operations and as precious metals prices fluctuate.

|

|

2025 |

2024 |

|||

|

|

(US$ million) |

% contribution |

(US$ million) |

% contribution |

Change % |

|

Herradura |

1,241.2 |

26.7 |

884.7 |

24.3 |

40.3 |

|

Saucito |

929.9 |

20.0 |

760.0 |

20.9 |

22.4 |

|

Juanicipio |

922.6 |

19.9 |

662.8 |

18.2 |

39.2 |

|

Fresnillo |

739.3 |

15.9 |

591.2 |

16.2 |

25.1 |

|

San Julián (Veins) |

527.9 |

11.4 |

354.5 |

9.7 |

48.9 |

|

Ciénega |

232.4 |

5.0 |

228.4 |

6.3 |

1.8 |

|

Noche Buena |

52.0 |

1.1 |

43.4 |

1.2 |

19.8 |

|

San Julián (DOB) |

0.0 |

0.0 |

115.1 |

3.2 |

(100.0) |

|

Total |

4,645.3 |

100 |

3,639.9 |

100 |

27.6 |

Treatment and refining charges

Treatment and refining charges1 are reviewed annually using international benchmarks. Treatment charges per tonne of lead and zinc concentrate and silver refining charges decreased substantially in dollar terms by 40.7%, 41.8% and 41.6%, respectively. These factors, combined with the lower volumes of lead and zinc concentrates shipped from our mines to Met-Mex, resulted in an 41.4% decrease in treatment and refining charges set out in the income statement in absolute terms when compared to 2024.

1 Treatment and refining charges include the cost of treatment and refining as well as the margin charged by the refiner.

Cost of sales

|

Concept |

2025 US$ million |

2024 US$ million |

Amount US$ million |

Change % |

|

Adjusted production costs2 |

1,406.7 |

1,582.2 |

(175.5) |

(11.1) |

|

Depreciation |

490.6 |

619.8 |

(129.2) |

(20.8) |

|

Profit sharing |

15.7 |

12.3 |

3.4 |

27.6 |

|

Change in work in progress |

(22.4) |

35.8 |

(58.2) |

N/A |

|

Unproductive costs including inventory reversal and unabsorbed production costs3 |

6.5 |

0.0 |

6.5 |

100.0 |

|

Cost of sales |

1,897.1 |

2,250.1 |

(353.0) |

(15.7) |

2 Adjusted production costs are calculated as cost of sales less depreciation, profit sharing, change in inventories and unproductive costs. The Company considers this a useful additional measure to help understand underlying factors driving production costs in terms of the different stages involved in the mining and plant processes, including efficiencies and inefficiencies, as the case may be, and other factors outside the Company's control such as cost inflation or changes in accounting criteria.

3 Unproductive costs primarily include unabsorbed production costs such as non-productive costs from the temporary suspension of activities at Herradura and non-productive fixed mine costs incurred at Noche Buena from the finalisation of mining activities.

Cost of sales decreased 15.7% to 1,897.1 million in 2025. The main factors driving the US$353.0 million decrease are listed below:

Adjusted production costs decreased by US$175.5 million as shown in the graph below:

Ongoing efforts to implement cost reduction initiatives have continued, generating positive results in 2025 and driving US$13.8 million net worth of operating efficiencies. These included efficiencies and cost reductions at Herradura (-US$39.6 million), and decreased contractor costs for development at Ciénega (-US$6.7 million). This achievement was offset by inefficiencies and cost increases at Fresnillo as a result of increased contractor costs for development, increased mechanical and electrical maintenance and higher consumption of explosives and milling balls at Fresnillo (+US$27.5 million), increased electrical and mechanical maintenance at Saucito (+US$3.4 million), and higher IT costs and increased mechanical maintenance at Juanicipio (+US$1.6 million).

Others reflect non-mining/core process costs converted from a commercial arrangement to a tolling agreement.

The decrease in depreciation (-US$129.2 million) was mainly due to lower depreciation of the asset base at San Julián as the DOB approached the end of its life, with its assets being fully depreciated in 2024, and, to a lesser extent, the reduced depletion factor at Ciénega and Saucito.

Gross profit

Gross profit is a key financial indicator of profitability at each business unit and the Fresnillo Group as a whole.

Total gross profit doubled from US$1,246.3 million in 2024 to US$2,664.1 million in 2025.

The main factors driving the US$1,417.8 million increase in gross profit are shown in the graphic below:

The contribution by mine to the Group's consolidated gross profit and the year-on-year variations are outlined in the table below:

Contribution by mine to consolidated gross profit

|

|

2025 |

2024 |

Change |

|||

|

|

US$ million |

% contribution |

US$ million |

% contribution |

US$ million |

% |

|

Herradura |

716.2 |

26.9 |

274.2 |

22.0 |

442.0 |

161.2 |

|

Juanicipio |

661.7 |

24.9 |

384.8 |

31.0 |

276.9 |

72.0 |

|

Saucito |

543.1 |

20.4 |

281.7 |

22.7 |

261.4 |

92.8 |

|

Fresnillo |

339.1 |

12.8 |

180.0 |

14.5 |

159.1 |

88.4 |

|

San Julián |

289.3 |

10.9 |

89.3 |

7.2 |

200.0 |

224.0 |

|

Ciénega |

77.7 |

2.9 |

29.6 |

2.4 |

48.1 |

162.5 |

|

Noche Buena |

31.1 |

1.2 |

3.2 |

0.2 |

27.9 |

871.9 |

|

Total for operating mines |

2,658.2 |

100.0 |

1,242.8 |

100.0 |

1,415.4 |

113.9 |

|

Metal hedging and other subsidiaries |

5.9 |

|

3.5 |

|

2.4 |

68.6 |

|

Total Fresnillo plc |

2,664.1 |

|

1,246.3 |

|

1,417.8 |

113.8 |

Administrative and corporate expenses

Administrative and corporate expenses increased 8.0% from US$109.5 million in 2024 to US$118.2 million in 2025, primarily due to an increase in personnel as well as performance bonuses linked to operating and financial results paid to administrative personnel, partly mitigated by the favourable effect of the devaluation of the Mexican peso vs the US dollar on administrative expenses denominated in pesos.

Exploration expenses

Exploration expenses increased 6.4% from US$163.0 million in 2024 to US$173.5 million in 2025. In line with our strategy, exploration continued to focus on the Fresnillo district and the Ciénega and San Julián mines, prioritising efforts to increase the resource base, convert resources into reserves and improve the confidence of the grade distribution in reserves. An additional US$2.6 million was capitalised, mainly relating to exploration expenses at the Guanajuato and Orisyvo projects. As a result, risk capital invested in exploration totalled US$176.1 million in 2025, compared to US$165.0 million in 2024 (of which US$2.0 million was capitalised). This represents a year-on-year increase of 6.7%.

EBITDA

EBITDA is a gauge of the Group's financial performance and a key indicator to measure debt capacity. It is calculated as profit for the year from continuing operations before income tax, less finance income, plus finance costs, less foreign exchange gain/(loss), less the net Silverstream effects and other operating income plus other operating expenses and depreciation.

|

|

2025 US$ million |

2024 US$ million |

Amount US$ million |

Change % |

|

Profit from continuing operations before income tax |

2,082.0 |

743.9 |

1,338.1 |

179.9 |

|

- Finance income |

(92.5) |

(46.9) |

(45.6) |

97.2 |

|

+ Finance costs |

68.5 |

73.6 |

(5.1) |

(6.9) |

|

- Revaluation effects of Silverstream contract |

189.2 |

182.3 |

6.9 |

3.8 |

|

- Foreign exchange loss/(gain), net |

45.2 |

(7.0) |

52.2 |

N/A |

|

- Other operating income |

(20.2) |

(39.6) |

19.4 |

(49.0) |

|

+ Other operating expense |

33.3 |

21.3 |

12.0 |

56.3 |

|

+ Depreciation |

490.6 |

619.8 |

(129.2) |

(20.8) |

|

EBITDA |

2,796.2 |

1,547.3 |

1,248.9 |

80.7 |

|

EBITDA margin |

61.3 |

44.3 |

- |

- |

In 2025, EBITDA increased 80.7% to US$2,796.2 million, primarily driven by the higher gross profit. EBITDA margin expressed as a percentage of revenue increased, from 44.3% in 2024 to 61.3% in 2025.

Other operating income and expense

In 2025, a net loss of US$13.1 million was recognised in the income statement primarily as a result of the assets derecognised in connection with new projects which, in accordance with the energy supply agreement with the state‑owned company (CFE), are required for grid connection and must be transferred to CFE. However, this compared negatively with the net gain of US$18.3 million recorded in 2024, mainly due to higher proceeds obtained from the sale of the non-core Guazapares mining concessions to Coeur Mining.

Silverstream effects

As reported in the 2025 Interim Report, following a thorough evaluation of strategic options, it was concluded that terminating the Silverstream contract via a buyback was in the best interests of Fresnillo and its shareholders. The decision to end the Agreement followed a comprehensive review by Fresnillo and its independent advisers SRK, of the ongoing operational and financial issues at the Sabinas mine. This resulted in a US$132.4 million net loss after taxes in the income statement, including the impacts of amortisation. Further information related to the Silverstream contract is provided in notes 14 and 30 to the consolidated financial statements.

Net finance income

Net finance income of US$24.0 million compared favourably to the US$26.6 million loss recorded in 2024. This was mainly driven by the increased interest on short term deposits and investments, net of the interest paid on the 4.250% Senior Notes due 2050.

Taxation

Income tax expense for the year was US$315.0 million, which compared favourably to the tax expense of US$390.2 million in 2024. The effective tax rate, excluding the special mining rights, was 15.1% (2024: 52.5%), compared to the 30% statutory tax rate. The reason for the variation in the effective tax rate is the difference between the tax and the accounting treatment related mainly to: i) the effect of the spot exchange rate on the tax value of assets and liabilities; ii) the special mining rights deductible for corporate income tax; iii) the effect of the Mexican inflation on the restatement of tax value of fixed assets; and iv) the benefit from the lower border tax, which applied to the Herradura and Noche Buena mines, as described in the table below:

|

|

2025 |

2024 |

|

Spot exchange rate (revaluation)/devaluation |

(11.4) |

20.0 |

|

Exchange rate effect on tax value of assets and liabilities |

(US$192.5 million) |

US$300.2 million |

|

Special mining right deductible for corporate income tax |

(US$58.4 million) |

(US$38.1 million) |

|

Inflationary uplift of the tax base of assets and liabilities |

(US$50.7 million) |

(US$55.2 million) |

|

Benefit from the lower border tax, which applied to Herradura and Noche Buena mines |

(US$24.0 million) |

- |

Mining rights in 2025 were US$193.2 million compared to mining rights of US$127.0 million charged in 2024, mainly as a result of the the increase in the profit base used in the calculation along with the increase from 7.5% to 8.5% in 2025.

Profit for the period

Profit for the year increased year-on-year by 594.2% as a result of the factors described above.

|

|

2025 US$ million |

2024 US$ million |

Amount change US$ million |

Change % |

|

Profit for the period |

1,573.8 |

226.7 |

1,347.1 |

594.2 |

|

Profit for the period, excluding post-tax Silverstream effects |

1,706.3 |

354.3 |

1,352.0 |

381.6 |

|

Profit due to non-controlling interests1 |

189.8 |

85.8 |

104.0 |

121.2 |

|

Profit attributable to equity shareholders of the Group |

1,384.0 |

140.9 |

1,243.1 |

882.3 |

|

Basic and diluted earnings per share (US$/share)2 |

1.878 |

0.191 |

1.687 |

883.2 |

|

Basic and diluted earnings per share, excluding post-tax Silverstream effects (US$/share) |

2.058 |

0.364 |

1.694 |

465.4 |

1 The increase reflects the higher profit generated at Juanicipio, where Pan American owns 44% of the outstanding shares.

2 The weighted average number of Ordinary Shares was 736,893,589 for 2025 and 2024. See Note 18 to the consolidated financial statements.

Cash flow

A summary of the key items from the cash flow statement:

|

|

2025 US$ million |

2024 US$ million |

Amount US$ million |

Change % |

|

Cash generated by operations before changes in working capital |

2,787.3 |

1,559.8 |

1,227.5 |

78.7 |

|

Increase in working capital |

(128.1) |

(162.9) |

34.8 |

(21.4) |

|

Taxes and employee profit sharing paid |

(369.5) |

(97.1) |

(272.4) |

280.5 |

|

Net cash from operating activities |

2,289.7 |

1,299.8 |

989.9 |

76.2 |

|

Disposal of equity instruments and dividends |

178.3 |

3.6 |

174.7 |

>100 |

|

Silverstream contract |

85.9 |

30.0 |

55.9 |

186.3 |

|

Financial gains/(expenses) and foreign exchange effects |

48.7 |

(9.8) |

58.5 |

N/A |

|

Proceeds from the sales of mining concessions (see Note 2 to the consolidated financial statements) |

16.1 |

10.0 |

6.1 |

61.0 |

|

Dividends paid to shareholders of the Company |

(654.3) |

(78.2) |

(576.1) |

736.7 |

|

Purchase of property, plant and equipment |

(400.1) |

(370.5) |

(29.6) |

8.0 |

|

Dividends paid to non-controlling interests and loans by minority shareholders |

(105.2) |

(118.8) |

13.6 |

(11.4) |

|

Net (decrease)/increase in cash during the period after foreign exchange differences |

1,458.7 |

763.2 |

695.5 |

91.1 |

|

Cash and other liquid funds at 31 December1 |

2,756.5 |

1,297.8 |

1,458.7 |

112.4 |

1 Cash and other liquid funds are disclosed in Note 17 to the consolidated financial statements.

Cash generated by operations before changes in working capital increased 78.7% to US$2,787.3 million, primarily due to higher precious metals prices. Working capital increased US$128.1 million, mainly due to: i) a US$208.3 million increase in trade receivables from related parties principally because of higher precious metals prices; ii) an increase in ore inventories of US$20.4 million; and iii) a US$20.1 million increase in prepayments. This was partly offset by a US$120.7 million increase in trade payables.

Taxes and employee profit sharing paid increased to US$369.5 million, mainly due to: i) the higher final income tax paid in 2025, net of provisional taxes paid, corresponding to the 2024 tax fiscal year; ii) an increase in provisional tax payments paid in 2025; iii) an increase in mining rights payments; and iv) higher profit sharing paid.

As a result of the above factors, net cash from operating activities increased 76.2% to US$2,289.7 million in 2025.

In addition, the Group benefited from additional sources of cash, primarily generated by:

i) Proceeds from the sale of Mag Silver shares and dividends received for US$178.3 million.

ii) Proceeds from the Silverstream contract of US$85.9 million.

iii) Financial gains and foreign exchange effects of US$48.7 million, which compared favourably to the financial expenses and foreign exchange effects of US$9.8 million in 2024. This was primarily driven by the increased interest on short term deposits and investments, net of interest paid on the 4.250% Senior Notes due 2050.

Main uses of funds were:

i) Dividends paid to shareholders of the Group in 2025 totalled US$654.3 million, compared with US$78.2 million in 2024. The 2025 payment comprised: i) the 2024 final ordinary dividend of 26.1 cents per share paid in May 2025, totalling US$192.3 million, in line with our dividend policy, which includes a consideration of profits generated in the year, adjusted for the extraordinary, non-cash items, in particular the revaluation of the Silverstream contract and the effect of the exchange rate on deferred taxes, ii) a one-off special dividend of 41.8 cents per share also paid in May 2025, totalling US$308.0 million, and iii) the 2025 interim ordinary dividend paid in September of US$153.3 million, equivalent to 20.8 cents per share.

ii) The purchase of property, plant and equipment for a total of US$400.1 million.

iii) Dividends and loans paid to non-controlling interest US$105.2 million decreased 11.4% vs 2024.

The sources and uses of funds described above resulted in an increase in net cash of US$1,458.7 million (net increase in cash and other liquid assets), which combined with the US$1,297.8 million balance at the beginning of the year resulted in cash and other liquid assets of US$2,756.5 million at the end of December 2025.

Balance sheet

Fresnillo plc continued to maintain a solid financial position during the period with cash and other liquid funds of US$2,756.5 million as of 31 December 2025. Taking this and the US$839.9 million outstanding Senior Notes, Fresnillo plc's net cash was US$1,916.6 million as of 31 December 2025. This compares positively to the net cash of US$458.3 million as of 31 December 2024.

Inventories increased 4.2% to US$502.6 million, mainly due to the increased inventories of lead and zinc concentrates at Fresnillo and Saucito.

Dividends

Based on the Group's 2025 performance, the Directors have recommended a final ordinary dividend of 108.12 US cents per Ordinary Share, which will be paid on 29 May 2026 to shareholders on the register on 24 April 2026. The dividend will be paid in UK pounds sterling unless shareholders elect to be paid in US dollars. This is in addition to the interim ordinary dividend of 20.8 US cents per share. This is above the Group's traditional dividend policy to pay out 33-50% of the profit attributable to equity shareholders of the company after making certain customary adjustments to exclude extraordinary non-cash effects in the income statement, and was permitted by strong cash generation throughout the year, which resulted in a high cash balance at year end. The company continues to maintain a healthy cash balance to invest in growth focused projects, along with an additional buffer for any M&A opportunities that may present themselves in the future. The dividend policy remains unchanged.

As disclosed in previous reports, the corporate income tax reform introduced in Mexico in 2014 created a withholding tax obligation of 10% relating to the payment of dividends, including to foreign nationals. The 2025 final ordinary dividend will be subject to this withholding obligation.

MANAGING OUR RISKS AND OPPORTUNITIES

Our approach to risk.

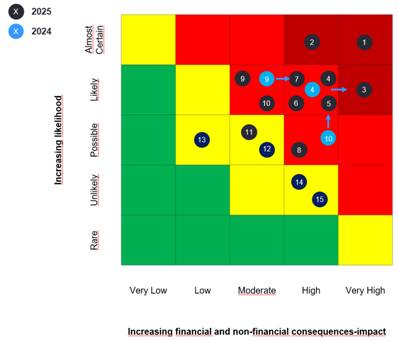

Effective risk management is an essential part of our culture and strategy. By understanding, prioritising and managing risk, Fresnillo plc safeguards our people, our assets, our values and reputation, and the environment, and identifies opportunities to best serve the long-term interests of all our stakeholders. We are focused on conducting our business responsibly, safely and legally, while making risk-informed decisions when responding to the opportunities or threats that are presented to us. Risk management is a key accountability and performance criterion for our leaders.

Our risk management process helps us to manage risks that have the potential to impact our business objectives, and timely risk monitoring is at the core of our management practices. All employees have responsibility for identifying and managing risks. Our risk management framework reflects the importance of risk awareness across Fresnillo plc. It enables us to identify, assess, prioritise and manage risks to deliver the value creation objectives defined in our business model.

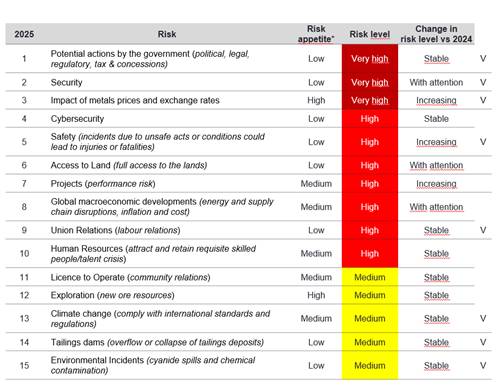

Risk appetite.

Defining risk appetite is key to embedding our risk management system into our organisational culture. The Company's risk appetite statement helps to align our strategy with the objectives of each business unit, clarifying which risk levels are, or are not, acceptable. It promotes consistent decision-making on risk, allied to the strategic focus and risk/reward balance approved by the Board.

We define risk appetite as 'the nature and extent of risk Fresnillo plc is willing to accept in relation to the pursuit of its objectives'. We look at risk appetite in the context of the severity of the consequences should the risk materialise, any relevant internal or external factors influencing the risk, and the status of management actions to mitigate or control the risk. A scale is used to help determine the limit of appetite for each risk, recognising that risk appetite will change over time.