Final Results for the year ended 31 December 2025

Summary by AI BETAClose X

26 May 2026

EARNZ plc

("EARNZ", the "Company", or the "Group")

Final Results for the year ended 31 December 2025 and Notice of AGM

Pivotal stage in the Group's evolution reached, with positive adjusted EBITDA in FY25

EARNZ plc ("EARNZ" or the "Company") (AIM: EARN), an energy services company whose objective is to capitalise on the drive for global decarbonisation, is pleased to announce its audited results for the year ended 31 December 2025 (the "Full Year").

Financial Highlights

· Revenue increased to £11.8m (FY25: £2.6m)

o Full year impact from the acquisitions of Cosgrove & Drew Ltd ("C&D") and South West Heating Services ("SWH") in September 2024

· EBITDA[1] of £0.1m (FY25: (£1.0m loss))

o Achieved despite significant increase in central support costs to support business growth.

· Loss before tax of £1.7m (FY24: £3.6m)

· Net debt of £1.2m (net cash FY24: £0.3m), excluding IFRS16 lease liabilities net debt was £0.7m (net cash FY24: £0.6m)

Operational Highlights

· The Group is benefitting from significant opportunities for growth, following the first phase of the buy and build strategy.

· In July 2025 the Group acquired A&D Carbon Solutions Limited ("A&D"), which has been integrated into the Group and has provided the platform for two new startup businesses, Warm Low Living ("WLL") and National Retrofit Solutions Limited ("NRS").

· Significant contract wins with Equans announced in FY25, and post year end further contract wins with Fortem, working on behalf of Sanctuary Housing announced in February and May 2026.

· During the year the Board was strengthened with the appointment of Peter Smith as CEO.

· Post year end, the business acquired Zero Carbon Group Limited ("ZCG"), which enhances the Group's scale and activities in the North of England.

The Group has had a successful first full year at the start of its journey to build a significant group in the energy services sector focussing on delivering for the key objectives of energy efficiency, reducing fuel poverty and building energy security across the UK through decarbonisation. The strengthened central support teams are in place for significant future growth.

We continue to develop our active list of potential acquisition targets across the decarbonisation agenda. Due to the difficulties of the capital restrictions to date, our acquisition strategy has been highly selective as we work within our financial constraints. As we have established a profitable platform for growth, the Board is looking at more significant opportunities for acquired growth which will enhance service offerings and provide a more stable base.

Outlook

· Momentum has continued with further contract wins announced in Q1 2026

· Strong pipeline of opportunities in all the businesses within the Group

· Further opportunities for growth through acquisition in line with our buy and build strategy.

· The Board remains confident in the outlook for FY26.

Peter Smith, CEO of EARNZ, said: "I am delighted with the progress to date. I would like to thank the whole EARNZ team across the Group for their hard work during the year. The business is well placed to benefit from the opportunities that lie ahead."

The Report & Accounts for the Full Year, the contents of which are set out below, together with the Notice of Annual General Meeting ("AGM"), will be posted to shareholders and will be made available later today on the Company's website at www.earnzplc.com. The AGM will be held at 10.30am on 23 June 2026 at EARNZ's office, Blackwell House, Guildhall Yard, London EC2V 5AE.

Engage with the Earnz PLC management team directly by asking questions, watching video summaries and seeing what other shareholders have to say. Navigate to our interactive investor hub here: https://investors.earnzplc.com/link/PnJ98P

For further information, please contact: https://investors.earnzplc.com/link/PnJ98P

|

Investor questions on this announcement We encourage all investors to share questions on this announcement via our investor hub

|

https://investors.earnzplc.com/link/PnJ98P |

|

Earnz Plc Peter Smith/ Elizabeth Lake

|

Via our investor hub |

|

Nominated Adviser and Broker Zeus Investment Banking Antonio Bossi / Andrew de Andrade / Oscar Stack Corporate Broking Dominic King / Alex Bartram

|

+44 (0) 203 829 5000 |

CHAIR'S REVIEW

I am pleased to announce another satisfactory year for the Group during a period of uncertainty in the energy services sector. We have continued to invest in both organic and inorganic growth with the acquisition of A&D Carbon Solutions Limited and toward the end of the year the formation of two start-up businesses, Warm Low Living Limited and National Retrofit Solutions Limited. These two start up opportunities became possible as a result of vendors from competitors wanting to join the Group at the start of our journey. We aspire to be a partner of choice to major property landlords in both the public and private sector.

Post year end we announced the acquisition of Zero Carbon Group Limited, for a total consideration of £9.5 million. The management team headed by Peter Jones bring an exciting range of skills which we believe add significant value to the business - welcome!

I have managed businesses in this sector for over 30 years and believe the opportunity to be just as big as it was when I floated Mears Group PLC which built a market leading position of revenues in excess of £1 billion; and Sureserve plc which became very successful under my Chairmanship and subsequently was acquired by private equity. I'm particularly proud to confirm that both businesses have continued their earlier successes under subsequent ownership.

The primary market we operate in is believed to be worth more than £10 billion.

We continue to seek out potential acquisition targets across the energy services. In the immediate short term we look to build partnerships with landlords across the full range of decarbonisation and general maintenance services. These budgets are vast and our determination to provide value for money services in periods of tight fiscal times will provide excellent long-term rewards.

As the business grows, we are seen as an attractive home for vendors and competitors' management teams, and our organic growth will be substantial in the short medium and long term.

I must congratulate all employees who have to work harder in a small company to demonstrate the skills they possess and why we should be the beneficiary of significant contract awards.

The primary responsibility of the Board is to ensure that our capital application is sound capital, as we continue to work within our financial constraints.

We have established the profitable platform for growth that was our priority.

We are looking at more significant opportunities for acquired growth. Our shareholders and other stakeholders have been great support to date for which I am very grateful.

I look forward to bringing news of further growth in earnings in the coming months.

Bob Holt OBE,

Chair

22 May 2026

CEO REPORT

2025 marked an important milestone in the progress of the Group. Our two original businesses, Cosgrove & Drew (C&D) and South West Heating Services (SWHS) were joined by the newly acquired A&D Carbon Solutions (A&D) in July and then the formation of two new businesses, Warm Low Living (WLL) and National Retrofit Solutions (NRS) in October.

These five businesses have allowed us to broaden our service offering considerably across the energy services sector. A&D gives us both a presence in Wales and opportunities around decarbonisation schemes and commercial solar, whilst WLL and NRS have a focus on the Social Housing sector, whether operating via Tier One contractors, or directly with Local Authorities and Housing Associations. With C&D continuing dual focus on mechanical engineering projects and facilities management, and SWHS focused on boiler servicing, repairs and maintenance, we are well positioned for growth on multiple levels.

It is worth adding that with businesses based in Plymouth, Bristol, Swansea, Stafford and Leeds, our geographical reach has increased substantially.

We were particularly pleased to be awarded a multi-year contract with Equans for Bradford City Council, not least because the opportunity came about through the accreditations held by A&D and delivered by WLL. Strength of the Group approach already evident and I am delighted to report that in 2026 we have already been awarded further multi-year contracts via Equans for Leeds Federated Housing Association (WLL) and via Fortem for Sanctuary Housing in Stoke-on-Trent and Chester (NRS). Alongside the existing pipeline of work for C&D, in particular, our Order Book is strong.

The post Year End acquisition of Zero Carbon Group (ZCG) continues the growth theme, increasing our reach in Social Housing and the Midlands and North West, in particular.

With these strong foundations in place, we welcomed the publication of the Government's Warmer Homes Plan in early 2026, which sets out plans for the next five years, with £15bn of funding set aside, £5bn of it for those on low incomes. Whilst we await further details, we are confident that this will only provide increased opportunities for the Group.

With growth comes the need to ensure functional support is appropriate. We have a strong Board in place and have strengthened our PLC team with the recruitment of an experienced People Director and Head of Health & Safety. We have taken space in a small managed office in London for the team. We will continue to review the support we give to the operators in the field, on whom we are so dependent.

I would like to thank all employees for their contributions over the past year and look forward to continuing our growth story.

Peter Smith,

CEO

22 May 2026

STRATEGIC REPORT

The Directors present their strategic report on the Group for the year ended 31 December 2025.

EARNZ plc disposed of its interests in its Solar Business on 29 February 2024. The Company's principal business is targeting acquisitions in the energy services sector. Going forward the Company will build a leading business in the energy services sector focusing on decarbonisation of public and private sector building fabric, leveraging UK Government investment in Net Zero transition and UK clean energy industries.

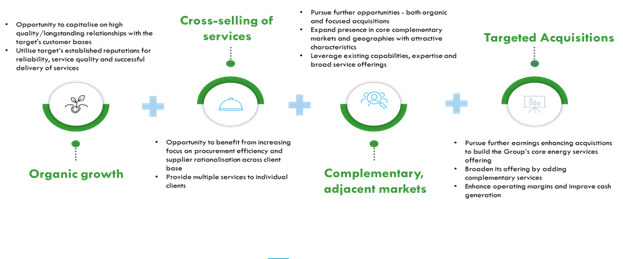

The sector is hugely fragmented, providing significant growth opportunities, by acquisition and organically.

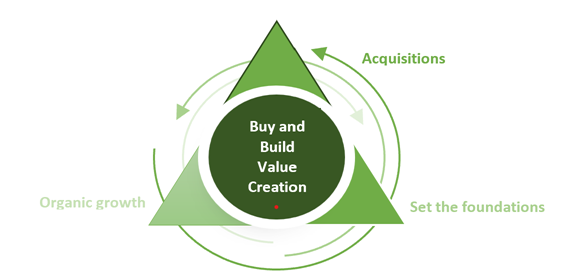

The Group's buy and build strategy is designed to create shareholder value through bringing together businesses in the energy services sector, providing consolidation in a fragmented sector, and extensive industry experience gained over many years. This creates improved service experience for customers and a virtuous circle of value creation. The foundations have been set through the addition of three businesses to the Group and the opportunity for organic growth and further acquisitions set.

For a review of the business during the year, please refer to the Chair's Review on page 1 of this report. For an analysis of financial performance indicators, please refer to the Financial Review set out on page 5.

Principal risks and uncertainties facing the business

A full review of principal risks and uncertainties facing the business during the year and going forward is given on pages 8 to 9 of this report .

S172 Statement

As required by Section 172 of the Companies Act, a director of a company must act in the way he or she considers, in good faith, would likely promote the success of the company for the benefit of the shareholders. In doing so, the director must have regard, amongst other matters, to the following issues:

• the likely consequences of any decisions in the long term (see Corporate Governance Report, pages 12 to 15);

• the interests of the company's employees (see Corporate Social Responsibility report on page 19)

• the need to foster the company's business relationships with suppliers/customers and others (see Corporate Governance Report, pages 12 to 15);

• the impact of the company's operations on the community and environment (see Corporate Social Responsibility report on page 19);

• the company's reputation for high standards of business conduct (see Corporate Governance Report, pages 12 to 15); and

• the need to act fairly between members of the company (see Corporate Governance Report, pages 12to 15).

On behalf of the Board

Peter Smith

CEO

22 May 2026

FINANCIAL REVIEW

The Financial Review covers aspects of the consolidated statements of comprehensive income, financial position and cash flows.

Group revenue increased from £2.6m in 2024 to £11.8m in 2025. This performance was driven by the full year impact of the acquisitions made in August 2024 plus contribution from the acquisition of A&D Carbon Solutions Limited on 1 July 2025.

The Group posted break even adj. EBITDA for the first time since it started trading 15 months ago in August 2024. Group adj. EBITDA was £0.0m in 2025 against a loss of £1.0m in 2024. This represents a milestone for the Group, with the first full year of the initial acquisitions (Cosgrove & Drew, and South West Heating Services) covering the Group PLC operating costs.

Adjusted Profits

The Group uses a number of Alternative Performance Measures ("APMs") in addition to those measures reported in accordance with IFRS. Such APMs are not defined terms under IFRS and are not intended to be a substitute for any IFRS measure. The Directors believe that APMs are important when assessing the underlying financial and operating performance of the Group.

The exceptional items identified as non-recurring in nature are set out below and were considered in calculating the adjusted profits.

|

Adjusted EBITDA from continuing operations £'000 |

Year ended 31 December 2025 |

Restated Year ended 31 December 2024 |

|

Operating Loss |

(1,349) |

(3,486) |

|

Depreciation & amortization |

310 |

73 |

|

Share based payment |

71 |

23 |

|

Exceptional items: |

|

|

|

Transaction costs |

304 |

1,622 |

|

Impairment Restructuring costs |

71 29 |

704 - |

|

Pre-trading start up costs |

642 |

- |

|

Non-recurring audit fee |

16 |

68 |

|

Total items added back |

1,443 |

2,490 |

|

Adjusted EBITDA |

94 |

(996) |

The performance of the two businesses that were in the Group for the full 12 months of FY25, C&D and SWH generated sufficient EBITDA to cover the costs of running the PLC.

Gross Profit

Gross profit for the year was £3.1m, 26%, a significant improvement on 2024 as can be seen in the table below.

|

Continuing Operations £'000 |

Year ended 31 December 2025 |

Year ended 31 December 2024 |

|

Revenue |

11,785 |

2,637 |

|

Cost of sales |

(8,734) |

(2,289) |

|

Gross profit |

3,051 |

348 |

|

Gross Profit % |

25.9% |

13.1% |

The key driver for this performance has come from C&D, which delivered £2.8m of margin at 29.3% v's £214k of margin at 9% in 2024. This improvement has been achieved through control of the cost base and the introduction of financial rigor in forecasting and controlling costs on projects and facilities management.

The margin in SWHS was lower year on year at 27% v's 33% in 2024, as expected, due to seasonality, with FY 2024 only containing 4 peak activity winter months, September to December.

For the six months that A&D has been in the Group, the margin they have achieved has been lower than the Group's overall margin and has had a diluting effect. We have been improving financial rigor and reporting and balancing the business portfolio with solar in A&D and going forward into 2026 we will see the benefits of this work.

Finance Costs

Net finance costs were £0.4m (2024: £0.1m). The increase year on year is attributable to the annualised costs for C&D and SWHS, together with costs within A&D brought into the Group from 1 July 2025. Just over half the total balance relates to loan interest with the remainder arising from the unwinding of contingent consideration discount and lease interest.

Taxation

Loss after tax from continuing operations was £1,747k (2024: £3,363k)

Loss per share

The basic and diluted loss per share was 0.015p (2024: 0.057p).

Financial Position

As at 31 December 2025, the Group's net assets were £3,752k (2024: 3,297k).

Non-current assets

Goodwill of £3,839k is the principal item in our balance sheet. This has arisen on the acquisitions of C&D, SWH and A&D and has been recognised at cost, representing the excess of the consideration paid over the fair value of the net assets acquired. The details relating to the acquisitions are set out in Note 12. As required by IAS 36, an impairment review has been carried out and concluded an impairment was necessary in SWH for the prior year, see Note 14.

The intangible assets are the value of the customer relationships acquired, and these are amortised each year.

Current assets excluding cash

Current assets excluding cash have increased from £1,733k in 2024 to £2,599k at the end of 2025. The main drivers of the movement comprise accrued revenue in C&D, A&D and NRS, reflecting revenue growth. See Note 16 for further details.

Liabilities excluding borrowings

The largest balance is trade and other payables at £1,836k (2024: £1,947k) which is consistent with the prior year.

Also included is the contingent deferred consideration arising from the acquisitions of C&D, SWH & A&D. The total balance of contingent consideration is £1,141k of which £348k is due within 12 months of the FY25 year end.

Lease liabilities amount to £394k (2024: £245k).

See Note 16 for further details.

Liquidity

The Group cash balance as at 31 December 2025 was £1,076k (2024: £1,965k).

Details of borrowings are shown in Note 16(vii)

Cashflow

|

£'000 |

Year ended 31 December 2025 |

Year ended 31 December 2024 |

|

Net cash (used in) operating activities |

(2,307) |

(3,083) |

|

Payment for acquisitions net of cash acquired |

(306) |

(747) |

|

Other |

(76) |

(28) |

|

Cash flows from investing activities |

(382) |

(775) |

|

Net proceeds from issues of shares |

1,942 |

5,663 |

|

Net proceeds/(repayment) of borrowings |

98 |

(89) |

|

Repayment of lease liabilities |

(179) |

(73) |

|

Other |

(61) |

431 |

|

Cash generated from financing activities |

1,800 |

5,932 |

|

Net cash outflow from discontinued operations |

- |

(162) |

|

Net increase/(decrease) in cash and cash equivalents |

(889) |

1,912 |

Net cash used in operations includes £642k of exceptional costs supporting the start-ups NRS and WLL and £304k for transaction costs for the acquisition of A&D

Issue of New Shares

New shares have been issued during the period to raise funds for the acquisition of A&D and for additional working capital to support the Group continuing with its buy and build strategy.

Dividends

No dividend is recommended (2024: £nil).

Events after the reporting period

On 11 March 2026, the Group signed a sale and purchase agreement to acquire all the share capital of Zero Carbon Group Limited at a cost of £9.5m with initial consideration of up to £5m, £1.5m in cash and £1.5m in new ordinary shares of EARNZ plc, to be adjusted for net debt and normalised working capital and a further £2m of which is contingent on meeting certain targets. When EBITDA of £0.5m has been achieved following completion, £1m becomes payable, 50% in cash and 50% in Consideration Shares at the Placing Price. The final £1.0m of the initial consideration is payable when EBITDA of £1.0m is achieved post completion, payable 50% cash and 50% in new ordinary shares in EARNZ plc.

The remaining consideration in the sale and purchase agreement is deferred and contingent upon reaching EBITDA targets for up to 3 years post completion and is payable 60% in cash and 40% in new ordinary shares in EARNZ plc.

On 12 March 2026 the Company raised £3.5m through a share placing, to fund the acquisition and provide additional working capital for the Group. The purchase completed on 31 March 2026 following shareholders' approval at a general meeting to authorise the directors to issue the consideration shares.

Events after the reporting period are described in Note 25 to the financial statements.

Elizabeth Lake

Chief Financial Officer

22 May 2026

RISK REPORT

Risk Management Framework

The Group has a risk register which includes all principal risks critical to the business.

The Board retains responsibility and accountability for the effectiveness of the risk management framework and internal control systems. As the business grows the risks will continue to evolve and grow in complexity and so will the risk management processes. This will ensure continuous improvement in the organisation's risk maturity.

Approach to Risk Management

The Audit Committee, under delegated authority from the Board, is accountable for overseeing the effectiveness of the risk management process, including identification of the principal and emerging risks facing the Group. The Audit Committee has particular focus on those risks that affect accounting in general and safeguarding the Group's assets.

Principal Risks and Uncertainties

The current Board has identified the Group risks.

|

DETAIL OF RISK |

MITIGATION and MANAGEMENT |

ASSESSMENT |

|

Continued Global political and economic uncertainty diverts resources away from the decarbonization agenda and increases costs |

The Group has diversified its operations to move away from government funded schemes and to increase work directly with landlords. In addition, the solar offering for both commercial and residential has been expanded. The Group is moving towards centralising procurement to achieve economies of scale to mitigate any cost increases of key materials. |

High risk |

|

Insufficient working capital to fund growth opportunities in delivery of the Group's buy and build strategy. |

The Board has reviewed medium-to-long-term cashflow forecasts (including sales forecast) and aims to ensure sufficient funding is in place to meet requirements. The Board is continually engaged with its investors and potential investors. With the Group now moving into positive EBITDA there will be an opportunity for facilities with our banking partner |

Medium risk |

|

Underperformance of target businesses |

Focusing on building relationships with key partners in the social housing sector. Build in contingencies in budgets and forecasts. Strong management teams are in place within the target businesses. |

Medium risk |

|

HSE violations in Group operating companies. |

The Group is directly responsible for installing and auditing an HSE culture. Documented operating procedures are in place in the operating businesses. Health & Safety is reviewed at each Board meeting and a Group Head of Health & Safety has been appointed. |

Medium risk |

|

Failure of business systems or loss of data, potentially causing issues such as delay in sales, reduced financial performance, reputational damage. |

The Group uses external IT support to carry out regular penetration testing and auditing security and processes. Robust insurance policy in place in case the event of ransom, including obtaining cyber essentials and training. |

Medium risk |

|

Attracting and retaining key employees. There is a general shortage of labour across the construction industry. Each operating company has a key management team, including the founders. The loss of any of these staff would have a detrimental impact on the growth of the business. |

Founders are incentivised with earn outs and bonuses. Executives have an LTIP in place, and senior management have bonus schemes. The Group is committed to improving working conditions, work life balance, progression, and training.

|

Medium risk |

|

Failure to meet AIM corporate governance requirements. |

The executive benchmarked its corporate governance, policies and procedures against published QCA guidelines to ensure compliance. The Company has regular discussions with its nominated adviser and external counsel. |

Low risk

|

GOVERNANCE

BOARD OF DIRECTORS

The Directors of EARNZ plc as at the date of signing the report and accounts comprised:

Bob Holt OBE (Chair) - appointed 29 February 2024 as Executive Chair, became Non-Executive Chair on 1 July 2025

Bob Holt is a highly accomplished executive with over 35 years' experience in senior leadership roles across various sectors, most recently serving as CEO of Revolution Beauty Plc after joining its board as interim COO. Prior to that, he successfully led Sureserve Group Plc as Chair, overseeing its successful turnaround that resulted in over a fivefold increase in the company's share price. He is perhaps most widely known for his role in the rise of Mears Group PLC. Since being appointed as Chair in 1996, he guided the company through its successful IPO on AIM and played a pivotal role in building its order book value to £3 billion, establishing Mears as a market leader in its sector. Bob has been awarded the OBE for his services to philanthropic causes.

Peter Smith (Chief Executive Officer) - appointed 1 July 2025

Peter was the former CEO of Sureserve Group PLC, (an AIM listed company) where he was responsible for growth strategy which delivered significant results and then oversaw its sale to PE in July 2023. Peter also has previous considerable experience as CFO/FD with widespread success in delivering results. Peter has worked in and specialises in highly regulated industries and has experience of extensive stakeholder engagement.

Peter is a qualified finance professional with a Henley Business School MBA

Elizabeth Lake FCA (Chief Financial Officer) - appointed 3 June 2024

(appointed non-executive director from 13 March 2024 - 3 June 2024)

Elizabeth is an accomplished executive with more than 25 years' finance and commercial experience. Previously, Elizabeth joined the board of Revolution Beauty Group as CFO in May 2022 and was instrumental in turning around the business following the suspension of its shares from trading on AIM. Prior to Revolution Beauty, she was CFO of AIM quoted, Everyman Media Group. During her time at Everyman, Elizabeth successfully led the company through the challenges presented by the Covid 19 pandemic, demonstrating her ability to navigate uncertainty with strong financial and operational acumen. Prior to Everyman, Elizabeth was Chief Financial Officer at AIM quoted, Science in Sport, and before that finance director at Hugo Boss UK and Ireland. She brings extensive UK plc experience to EARNZ having also worked in finance roles at Marks & Spencer, Pearson and Thomson Reuters. Elizabeth is ACA qualified, having trained at Coopers and Lybrand (now PwC).

Linda Main (Senior Independent Director) - appointed 1 May 2024

Linda is a chartered accountant who retired from KPMG LLP in September 2023 after a long career leading its Capital Markets Advisory Group. Linda has advised on well over 100 IPOs and significant transactions by listed companies of all sizes ranging from start-ups to members of the FTSE 100. She was also a member of the UK board of KPMG where she chaired the Risk Committee and sat on the Audit Committee. Until December 2023, Linda was a member of the London Stock Exchange's AIM Advisory Group and earlier in her career sat on a number of the Quoted Companies Alliance ("QCA")'s technical committees. She also sits on the QCA board. Linda is a non-executive director at MHA PLC and Princes Group Plc and is a Trustee at United Response. Linda chairs the Company's Audit and Remuneration committees.

Sandra Skeete (Independent Non-Executive Director) - appointed 3 June 2024

Sandra has over 25 years' experience working in social housing, holding senior roles in organisations such as the Peabody Trust and Refugee Housing Association Limited, and was previously a director of One Housing Group and the Duke of Lancaster Housing Trust. She was the Chief Executive of Octavia Housing Association Group, a not-for-profit organisation offering social housing and care services for vulnerable members of the community in central and west London. She was previously a non-executive board associate of Principality Building Society. Sandra sits on the Company's Audit and Remuneration committees.

Directors in post during the year included:

John Charlton (Director) - resigned 1 July 2025

The Board and responsibilities

The Board holds bi-monthly meetings to review, formulate and approve the Group's strategy, budgets, corporate actions and oversee the Group's progress towards its goals. There is an Audit Committee and a Remuneration Committee in place with formally delegated duties and responsibilities and with specific terms of reference. From time-to-time separate committees may be set up by the Board to consider specific issues when the need arises. Due to the size of the Group, the Directors have decided that issues concerning the nomination of directors will be dealt with by the Board rather than by a committee but will regularly reconsider whether a nominations committee is required.

Details of board meetings held in the reporting period, and attendance of Board directors is shown below:

|

Board Members |

Eligible to attend |

Attended |

|

|

|

|

|

Executive Directors |

|

|

|

Bob Holt OBE (appointed 29 February 2024) |

15 |

15 |

|

Elizabeth Lake FCA (appointed Non-Executive Director 13 March 2024 and as Chief Financial Director 3 June 2024) |

15 |

15 |

|

John Charlton (appointed 29 February 2024, resigned 1 July 2025) Peter Smith (appointed CEO 1 July 2025) |

9 |

9 |

|

|

6 |

6 |

|

Non-Executive Directors |

|

|

|

Linda Main (appointed 3 June 2024) |

15 |

15 |

|

Sandra Skeete (appointed 1 May 2024) |

15 |

15 |

The Audit Committee

The Audit Committee comprises Linda Main (appointed 1 May 2024) as Chair and Sandra Skeete (appointed 3 June 2024).

The Audit Committee determines the terms of engagement of the Group's auditors and will determine, in consultation with the auditors, the scope of the audit. The Audit Committee receives, and reviews reports from management and the Group's auditors relating to the interim and annual accounts and the accounting and internal control systems in use throughout the Group. The Audit Committee has unrestricted access to the Group's auditors. The Audit Committee Report is presented on page 16.

The Remuneration Committee

The Remuneration Committee comprises Linda Main (appointed 1 May 2024) as Chair and Sandra Skeete (appointed 3 June 2024).

The Remuneration Committee reviews the scale and structure of the executive Directors' and senior employees' remuneration and the terms of their service or employment contracts, including share option schemes and other bonus arrangements. The remuneration and terms and conditions of the non-executive Directors are set by the entire Board. The Directors' Remuneration Report is presented on pages 17-18.

Investor relations

The Annual General Meeting is the principal forum for dialogue with shareholders. Updates on the progress of the business are regularly published on the Group's website.

On behalf of the Board

Bob Holt OBE

Chair

22 May 2026

CORPORATE GOVERNANCE REPORT

The Chair has overall responsibility for corporate governance and good corporate governance is central to the Group's approach to creating sustainable growth and enhancing long-term shareholder value. The Directors are expected to always act ethically and responsibly, reflecting the Group's core values.

The Directors recognise that good corporate governance is a key foundation for the long-term success of the Group. As the Company is listed on the AIM market of the London Stock Exchange it is subject to the continuing obligation of the AIM Rules. The Board has therefore adopted the principles set out in the Corporate Governance Code for small and midsized companies published by the Quoted Companies Alliance (the "QCA Code").

|

QCA Code Principle |

What we do and why |

|

1. Establish a strategy and business model which promotes long-term value for shareholders |

The Company's strategy is explained fully within the Chair's Review section of the Report and Accounts for the year ended 31 December 2025.

Our strategy is identifying potential acquisitions in the energy services sector, to create a consolidated Group with scale and breadth of offering in the energy services sector, growing revenues and profitability.

The key challenges to the business and how these are mitigated are detailed on pages 8 to 9 of the Report and Accounts for the year ended 31 December 2024. |

|

2. Promote a corporate culture that is based on ethical values and behaviours |

The Corporate and Social Responsibility section on page 19 of the Report & Accounts for the year ended 31 December 2025 details the ethical values of the Company.

The Board continues to review policies and will amend as required. These policies and procedures are made available to staff and consultants and anti-bribery and anti-corruption training, and data protection training is mandatory.

Staff and consultants are encouraged to ask questions and seek clarifications from senior members of the team on these policies and procedures. |

|

3. Seek to understand and meet shareholder expectations

|

Whilst the Company is early stage, the Board is committed to returning value to shareholders through execution of our strategy.

The Board recognises the AGM as an important opportunity to meet shareholders. All the Directors are available to listen to the views of shareholders informally immediately after the AGM The people responsible for shareholder liaison are: The Chair The Executive Directors NOMAD (Zeus) The Company's website maintains a channel to provide information and receive feedback from all stakeholders. The Company has also invested in a subscription to Investor Hub to enhance the opportunities for communication with shareholders In addition the Company will present results directly to Investors and provide opportunities for questions at the AGM.

|

|

4. Take into account wider stakeholder interests, including social and environmental responsibilities, and their implications for long term success. |

The executive maintained communications with trade and interest groups working in the markets where its products are sold and applied. A number of mechanisms are in place to solicit feedback from shareholders including the Company's website and face to face meetings as well as the AGM and Investor Hub. |

|

Going forward, much of the Group's business will be involved in decarbonisation of public, commercial and private buildings, leading to greater fuel efficiency and energy security.

The Company has a whistleblowing policy in place which is given to all new employees. This provides a confidential mechanism for employees to raise concerns. The business model is focussed on decarbonisation of buildings in the public, commercial and private sector, together with energy efficiency. The culture of the business reinforces social and environmental responsibility. |

|

|

5. Embed effective risk management, internal controls and assurance activities, considering both opportunities and threats, throughout the organisation. |

Risk management on pages 8 to 9of our Annual Report and Accounts details the risks to the business and how these are mitigated. The Board considers risks to the business at its monthly meetings and reviews the principal risks to the business and the risk register quarterly. Risks are reviewed in the business monthly and quarterly by the Board. The enterprise-wide controls are continually reviewed and the FPPP (Financial Position and Prospects Procedures) manual updated if required. All Board members are entitled to engage external experts as part of their roles where they see fit. The Company's auditor HaysMac is independent of management. |

|

6. Establish and maintain the Board as a well-functioning, balanced team, led by the Chair. |

All members of the Board are experts in their fields with no one individual dominating. All Directors are seasoned Board members and understand the responsibilities of being a company Director. The shareholders have the opportunity annually at the AGM to vote for the (re-)election of all the Directors The new Board comprises 2 executive Directors, the Chair and 2 non-executive Directors. The 2 non-executive Directors are independent. Both the audit and remuneration committees comprise non-executive Directors only, with Linda Main being the Senior Independent Director. The Board is relatively newly constituted. Any related parties are excluded from Board discussions concerning their interests to maintain independence. Directors' remuneration is set by the Remuneration Committee which comprises the independent non-executive Directors. |

|

7. Maintain appropriate governance structures and ensure that individually and collectively the Directors have the necessary up-to-date experience, skills and capabilities. |

The Corporate Governance report on pages 10 to 11 details the Company's governance structures and why they are appropriate and suitable for the Company. The Board has a formal schedule of matters reserved for the Board and is supported by the Audit and Remuneration committees. Due to the size of the Company, the Board has decided that issues concerning the nomination of Directors will be dealt with directly by the Board but will reconsider on a regular basis whether a Nominations committee is needed. The Audit and Remuneration committees have specific terms of reference under which they operate. The Directors have a proven track record of previously serving on Boards. Where an expert view is needed the Board will seek input from external advisers Further information about the Board's skillset, including each Director's biography is set out on the Company website and additional information is set out on page 8 in this report. Each director attends industry events and seminars to continually update their skills and knowledge. Through the FPPP process a new Board pack has been developed and this will continue to evolve as the business grows. |

|

8. Evaluate board performance based on clear and relevant objectives, seeking continuous improvement. |

The Board is relatively new, a performance evaluation process will be developed. The annual review process will be implemented following the appointment of the CEO, together with succession planning.

|

|

9. Establish a remuneration policy which is supportive of long-term value creation and the Company's purpose and culture |

The Remuneration Committee has been established comprising 2 independent non-executive Directors. The Committee are reviewing the remuneration strategy on a regular basis. The remuneration policy includes long term incentive schemes to promote long term growth of shareholder value. The remuneration policy includes share options and plans to include a Save-As-You-Earn scheme for wider participation in shareholding across the Group. The Remuneration Committee will consult with the Audit Committee and the Board, as appropriate, when developing the remuneration policy. The Chair of the Remuneration Committee will consult with major shareholders on the design of incentives. Whilst this will not be binding, it will give shareholders the opportunity for input. |

|

10. Communicate how the company is governed and is performing by maintaining a dialogue with shareholders and other relevant stakeholders. |

The Company encourages two-way communication with its investors and responds quickly to all queries received.

The Board recognises the AGM as an important opportunity to meet private shareholders. The Directors are available to listen to the views of shareholders informally immediately following the AGM.

The Chair is responsible for ensuring appropriate communication and reporting to shareholders.

A range of corporate information (including Company announcements, historical annual reports and other governance related material) is also available on the Company's website. The Company will disclose outcomes of all votes at shareholder meetings in a clear and transparent manner by releasing a market announcement and by including it on the Company website. |

AUDIT COMMITTEE REPORT

The Audit Committee helps the Board discharge its responsibilities regarding financial reporting, external and internal audits and controls as well as reviewing the Group's annual and half-year financial statements, other financial information and internal Group reporting.

This includes:

• considering whether the Company has followed appropriate accounting standards and, where necessary, made appropriate estimates and judgments taking into account the views of the external auditors;

• reviewing the clarity of disclosures in the financial statements and considering whether the disclosures made are set properly in context;

• where the audit committee is not satisfied with any aspect of the proposed financial reporting of the Company, reporting its view to the Board of Directors;

• reviewing material information presented with the financial statements and corporate governance statements relating to the audit and to risk management; and

• reviewing the adequacy and effectiveness of the Company's internal financial controls and, review the Company's internal control and risk management systems and, except where dealt with by the Board, review and approve the statements included in the annual report in relation to internal control and the management of risk.

The Audit Committee assists by reviewing and monitoring the extent of non-audit work undertaken by external auditors, advising on the appointment of external auditors and reviewing the effectiveness of the Group's internal audit activities, internal controls and risk management systems. The ultimate responsibility for reviewing and approving the Annual Report and financial statements and the half-yearly reports remains with the Board.

For the year under review, there were no non-audit services rendered to the Group and the Company. Fees paid for audit services are provided in Note 5a.

Significant reporting issues considered during the year included the following:

· Revenue recognition under IFRS 15 and the application within the Group.

· Application of IFRS 3 and calculations to allocate the purchase price of acquisitions made in the period.

· Impairment reviews of acquired subsidiaries.

Going concern

The Committee considered the Going Concern basis on which the accounts have been prepared and can refer shareholders to the Group's accounting policy set out in Note 2.2. The directors are satisfied that the going concern basis is appropriate for the preparation of the financial statements

Linda Main

Audit Committee Chair

22 May 2026

DIRECTORS' REMUNERATION REPORT

This report sets out the remuneration policy operated by the Company in respect of the Chair, Executive and Non-Executive Directors. The remuneration policy is the responsibility of the Remuneration Committee, a sub-committee of the Board. No Director is involved in discussions relating to their own remuneration.

Remuneration policy

The objective of the remuneration policy is to attract, retain and motivate high calibre executives to deliver outstanding shareholder returns and at the same time maintain an appropriate compensation balance with the other employees of the Group. There is no formal requirement for Directors to own shares in the Group.

The Remuneration Committee comprises independent Non-Executive Directors, and is appointed by the Board. The Remuneration Committee has terms of reference approved by the Board, which sets out a framework for determining the remuneration of the Company's Chair and Executive Directors including pension rights and compensation payments. The remuneration of Non-Executive Directors is a matter reserved for the Board. No Director or senior manager shall be involved in any decisions as to their own remuneration. The Remuneration Committee recommends and monitors the level and structure of remuneration for senior management.

The Remuneration Committee has regard to the following factors when determining remuneration:

· The pay and employment conditions across the Company and/or the Group when setting remuneration policy for Directors, especially when determining salary increases.

· The Company's appetite for risk and long-term strategic goals.

· Remuneration in other companies of comparable scale

The Remuneration Committee sets appropriate Directors' compensation to reward long-term success:

· A significant proportion of Executive Directors' remuneration should be structured to link rewards to corporate and individual performance and be designed to promote the long-term success of the Company. The Remuneration Committee approves the design of, and determines targets for, any performance-related pay schemes operated by the Company and approves any payments made under such schemes.

The Remuneration Committee has regard to the following factors when reviewing remuneration:

· The Remuneration Committee reviews the performance of share incentive plans and discretionary bonus schemes. Each year the Remuneration Committee determines whether awards will be made, and if so, the overall amount of such awards, the individual awards to Executive Directors and other senior management and the performance targets to be used.

· The Remuneration Committee periodically reviews the ongoing appropriateness and relevance of the remuneration policy.

Directors' remuneration

The normal remuneration arrangements for Executive Directors consist of base salary, performance bonuses and other benefits as determined by the Board. The Company currently has two Executive Directors, who have service agreements that can be terminated at any time by either party giving to the other six months' written notice.

The remuneration package for an Executive Director is detailed below:

Base Salary:

Annual review of the base salary of the Executive Director considering the Executive Director's role, responsibilities and contribution to the Group performance.

Performance Bonus:

No bonuses were paid in relation to the reporting period. Going forward the remuneration committee will be establishing a performance bonus scheme with relevant targets.

Benefits:

Benefits include Company pension contributions of 5%. On 1 November 2025 the Group established a Private Healthcare Scheme which all employees of the Group are eligible to join. Post the year end the Group has also established death-in-service benefits scheme which all employees are enrolled in.

Longer term incentives:

To incentivise the Directors, and align their interests with shareholders, the Company granted share options in the period. The share options will vest at a future date as described in Note 19 in the financial statements. The vesting conditions are exclusively share price related.

Non-Executive Directors are currently remunerated solely in the form of Directors' fees and pension contributions.

Re-election of Directors

All Directors stand for re-election on an annual basis and all Directors are aware of the need to maintain their independence and to demonstrate their continued commitment to the role. Succession planning is limited due to the current size of the Board.

|

The emoluments of the Directors were as follows (Audited): |

||||||

|

|

Year ended 31 December 2025 |

Year ended 31 December 2024 |

||||

|

|

Salary & Directors' fees |

Pension contributions |

Share-based payments |

Other Benefits |

Total |

Total |

|

|

£ |

£ |

£ |

£ |

£ |

£ |

|

Executive Directors |

|

|

|

|

|

|

|

Bob Holt OBE (appointed 1 March 2024) |

50,000 |

2,500 |

34,663 |

834 |

87,997 |

57,122 |

|

Peter Smith (appointed 1 July 2025) |

56,667 |

4,583 |

1,642 |

353 |

63,245 |

- |

|

Elizabeth Lake (appointed 13 March 2024) |

125,000 |

6,249 |

13,196 |

424 |

144,869 |

86,690 |

|

John Charlton (resigned 1 July 2025) |

25,000 |

1,250 |

11,554 |

- |

37,804 |

37,340 |

|

Robert Richards (resigned 1 March 2024) |

- |

- |

- |

- |

- |

28,272 |

|

Non-Executive Directors |

|

|

|

|

|

|

|

Linda Main (appointed 1 May 2024) |

31,917 |

2,208 |

- |

- |

34,125 |

17,500 |

|

Sandra Skeete (appointed 3 June 2024) |

29,288 |

4,837 |

- |

- |

34,125 |

15,750 |

|

George Katzaros (resigned 29 February 2024) |

- |

- |

- |

- |

- |

- |

|

Gavin Mayhew (resigned 2 January 2024) |

- |

- |

- |

- |

- |

- |

|

Total |

317,872 |

21,627 |

61,055 |

1,611 |

402,165 |

242,674 |

The remuneration of the Directors in EARNZ plc who held office during the years to 31 December 2025 and 2024 were as follows:

Linda Main

Chair - Remuneration Committee

22 May 2026

CORPORATE AND SOCIAL RESPONSIBILITY

The Company understands that its impact reaches beyond that of its core business and into the environment and society in which it operates. With integrity at the heart of our corporate social goals our aim is to make a lasting positive contribution to all our stakeholders.

In view of the limited number of stakeholders, the Company has not adopted a specific policy on Corporate Social Responsibility. However, it does seek to protect the interests of stakeholders in the Company through its policies, combined with ethical and transparent business operations.

Environment

EARNZ Plc is sensitive to the environment in which it operates. Previously the Group established well defined operating guidelines with some of the manufacturing partners where it sought their compliance with ISO14001 (a recognized standard for Environmental Management Systems) when relevant, to ensure certain environmental standards are complied with. Going forward the Company will be operating in the energy services sector, and as such will be instrumental in assisting with the delivery of de-carbonisation across the public and private sector.

Human Rights

EARNZ plc is committed to socially and morally responsible business practices for the benefit of all stakeholders. The activities of the Company are in line with applicable laws on human rights.

Employees

Employees are key to achieving the business objectives of the Company. The Board's priority is to provide a working environment in which our employees can develop to achieve their full potential and have opportunities for both professional and personal development. We aim to invest time and resource in supporting, engaging and motivating our employees to feel valued, to be able to develop rewarding careers and want to stay with us. The Company embraces employee participation in issue raising and resolution through regular meetings with managers and values contributions from all levels regardless of their position in the business.

Shareholders

The Board of Directors actively encourages communication, and they seek to protect the interest of shareholders at all times. The Company updates shareholders regularly through regulatory news, financial reports and research notes. The Company also engages directly with investors at our General Meetings or investor events.

Health and Safety

Company and Group activities are carried out in accordance with its health and safety policies which adhere to all applicable laws.

DIRECTORS' REPORT

The Directors present their report and the audited financial statements for EARNZ plc ("EARNZ" or the "Company") for the year ended 31 December 2025.

The preparation of financial statements is in compliance with UK adopted International Accounting Standards and the Companies Act 2006. The Group financial statements comprise of the financial information of the parent Company and its subsidiaries (together the "Group"). The parent Company's financial statements present information about the Company as a separate entity and not about its Group.

Principal activities

EARNZ plc is a holding company based in UK. The principal activity of the Group is to build a leading business in the energy services sector focusing on decarbonisation of public and private sector building fabric, leveraging UK Government investment in Net Zero transition and UK clean energy industries.

A detailed review of the business activities of the Group is contained in the Strategic Report.

Business review and future developments

The review of the business' operations, future developments and key risks is contained in the Strategic Report. The Directors do not recommend the payment of a final dividend for the year (2024: £nil).

Directors and directors' interests

The directors who held office during the year or subsequently were as follows:

|

Bob Holt |

Appointed 29 February 2024 |

|

Peter Smith |

Appointed 1 July 2025 |

|

Elizabeth Lake |

Appointed 13 March 2024 |

|

Linda Main |

Appointed 1 May 2024 |

|

Sandra Skeete |

Appointed 3 June 2024 |

|

John Charlton |

Appointed 29 February 2024, resigned 1 July 2025 |

Regarding the appointment and replacement of Directors, the Company is governed by its articles of association, the Companies Act and related legislation. The articles themselves may be amended by special resolutions of the shareholders.

Directors' interests

The Directors held the following beneficial interests in the shares of EARNZ plc at 31st December 2025:

|

|

Ordinary shares |

Issued share capital % |

|

of £0.04 each |

||

|

Bob Holt OBE |

12,400,000 |

9.3% |

|

Peter Smith |

1,013,888 |

0.8% |

|

Elizabeth Lake |

3,819,443 |

2.9% |

|

John Charlton |

1,339,083 |

1.0% |

|

Linda Main |

255,555 |

0.2% |

|

Sandra Skeete |

27,221 |

0.0% |

The Directors held the following beneficial interests in the shares of EARNZ plc at 31st December 2024:

|

|

Ordinary shares |

Issued share capital % |

|

of £0.04 each |

||

|

Bob Holt OBE |

11,300,000 |

11.06% |

|

Peter Smith |

- |

- |

|

Elizabeth Lake |

1,666,666 |

1.63% |

|

John Charlton |

1,100,000 |

1.08% |

|

Linda Main |

200,000 |

0.20% |

|

Sandra Skeete |

13,333 |

0.01% |

|

|

|

|

|

|

|

|

|

Directors' indemnities

The Company has taken out Directors' and Officers' indemnity insurance for the benefit of its Directors.

Events after the reporting date

See Note 25 of the accounts.

Financial Risk management

Details of financial risk management are provided in [Note 21] to the accounts.

Political and charitable contributions

The Group made no charitable or political contributions during the year.

Going Concern

The Director' considered the Going Concern basis on which the accounts have been prepared and can refer shareholders to the Group's accounting policy set out in Note 2.2. The directors are satisfied that the going concern basis is appropriate for the preparation of the financial statements

Substantial shareholdings:

The Company has been advised of the following interests in more than 3% of its ordinary share capital as at 31 December 2025:

|

Shareholder |

|

No. of Shares (nominal value £0.04) |

% |

|

Gresham House Asset Management |

|

35,436,474 |

26.5% |

|

Bob Holt |

|

12,400,000 |

9.3% |

|

Pentwater Capital Management |

|

6,944,444 |

5.2% |

|

UBS Group AG |

|

5,802,146 |

4.3% |

|

Bank of America Securities |

|

5,555,555 |

4.2% |

|

Hargreaves Lansdown PLC |

|

5,024,244 |

3.8% |

|

Andrew Custer |

|

4,666,666 |

3.5% |

|

Philip J Milton & Co |

|

4,396,597 |

3.3% |

|

Aberdeen PLC |

|

4,026,579 |

3.0% |

At the signing date the Company had been advised of the following interests in more than 3% of its ordinary share capital:

|

Shareholder |

|

No. of Shares (nominal value £0.004) |

% |

|

Gresham House Asset Management |

|

63,936,474 |

27.20% |

|

Pentwater Capital Management |

|

46,749,998 |

19.89% |

|

Bob Holt |

|

13,480,000 |

5.76% |

|

Peter Jones |

|

9,000,000 |

3.83% |

|

Debra Jones |

|

9,000,000 |

3.83% |

|

Elizabeth Lake |

|

8,219,443 |

3.35% |

Statement of Disclosure to the Auditors

The Directors at the date of approval of this report confirm that:

· As far as each director is aware, there is no relevant audit information of which the Company's and the Group's auditor is unaware; and

· Each Director has taken all reasonable steps that they ought to have taken as a Director to make themselves aware of any relevant information and to establish that the Company's and the Group's auditor is aware of that information.

Auditors appointment

HaysMac LLP were re-appointed as auditors to the Company during the year. In accordance with section 485 of the Companies Act 2006, a resolution proposing that they be re-appointed will be put to the vote at the AGM.

By order of the Board

John Charlton

Company Secretary

22 May 2026

STATEMENT OF DIRECTORS' RESPONSIBILITIES

The Directors are responsible for preparing the Annual Report and the financial statements in accordance with applicable law and regulations.

Company law requires the Directors to prepare Group and Company financial statements for each financial year. Under that law the Directors have elected to prepare the Group consolidated financial statements in accordance with UK adopted International Accounting Standards (UK IAS) and elected to prepare the parent company financial statements under United Kingdom Generally Accepted Accounting Practice (United Kingdom Accounting Standards and applicable laws including FRS 101 Reduced Disclosure Framework).

Under company law the Directors must not approve the financial statements unless they are satisfied that they give a true and fair view of the state of affairs of the Group and the Company and of the profit or loss of the Group for that period.

In preparing each of the Group and Company financial statements, the Directors are required to:

• Select suitable accounting policies and then apply them consistently;

• Make judgments and estimates that are reasonable and prudent;

• State whether they have been prepared in accordance with UK-adopted International Accounting Standards (IASs) and International Financial Reporting Standards (IFRSs) have been followed, subject to any material departures disclosed and explained;

• Prepare the Strategic Report and Directors' report which comply with the requirements of the Companies Act 2006; and

• Prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Group and the Company will continue in business.

The Directors are responsible for keeping adequate accounting records that are sufficient to show and explain the Group and the Company's transactions and disclose with reasonable accuracy at any time the financial position of the Group and the Company and enable them to ensure that the financial statements comply with the Companies Act 2006. They are also generally responsible for taking such steps as are reasonably open to them to safeguard the assets of the group and to prevent and detect fraud and other irregularities.

The Directors are responsible for the maintenance and integrity of the corporate and financial information included on the Company's website. Information published on the website is accessible in many countries and legislation in the United Kingdom governing the preparation and dissemination of financial statements may differ from legislation in other jurisdictions.

The Directors consider that the annual report and accounts, taken as a whole, is fair, balanced and understandable and provides the information necessary for shareholders to assess the Group's position and performance, business model and strategy. Each of the directors confirms that, to the best of their knowledge:

The Group financial statements, which have been prepared in accordance with UK IAS and Companies Act 2006, give a true and fair view of the assets, liabilities, financial position and profit of the Group; and the Annual Report includes a fair review of the development and performance of the business and the position of the Group, together with a description of the principal risks and uncertainties that it faces.

Independent auditors' report

to the members of Earnz Plc

Opinion

We have audited the financial statements of Earnz Plc (the 'company') and its subsidiaries (the 'group') for the year ended 31 December 2025 which comprise:

|

Group |

Company |

|

the Consolidated Statement of Comprehensive Income; |

the Company Balance Sheet; |

|

the Consolidated Balance Sheet; the Consolidated Statement of Changes in Equity; the Consolidated Statement of Cash flows; and related notes to the financial statements

|

the Company Statement of Changes in Equity;

and related notes to the financial statements

|

The financial reporting framework that has been applied in their preparation is applicable law and United Kingdom adopted International Financial Reporting Standards (IFRSs).

In our opinion:

the financial statements give a true and fair view of the state of the group's and of the company's affairs as at 31 December 2025 and of the group's loss for the year then ended;

the group financial statements have been properly prepared in accordance with UK adopted International Financial Reporting Standards (IFRS).

the company financial statements have been properly prepared in accordance with United Kingdom Generally Accepted Accounting Practice; and

the financial statements have been prepared in accordance with the requirements of the Companies Act 2006.

Basis for opinion

We conducted our audit in accordance with International Standards on Auditing (UK) (ISAs (UK)) and applicable law. Our responsibilities under those standards are further described in the auditor's responsibilities for the audit of the financial statements section of our report.

We are independent of the group and the company in accordance with the ethical requirements that are relevant to our audit of the financial statements in the UK, including the Financial Reporting Council's (the FRC's) Ethical Standard as applied to listed public interest/listed entities, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

An overview of the scope of our audit

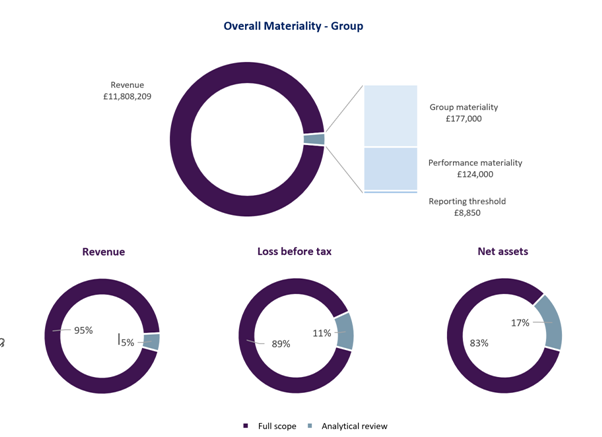

The group comprises a parent holding company, an additional holding company, two existing subsidiaries (acquired in the prior year), a newly acquired subsidiary, and two newly formed entities. The material components of the group for which we performed full scope audit procedures following an assessment at the audit planning phase were Earnz Plc, Southwest Heating Services Limited ("SWH") and Cosgrove & Drew Limited ("C&D") with analytical review or specific scope procedures as well as verification of bank balances to third party confirmation completed on other group entities that were determined to be less significant to the group based on our assessment of materiality.

The scope of the audit and our audit strategy was developed by using our audit planning process to obtain and update our understanding of the group and its environment, including the group's system of internal control, and assessing the risks of material misstatement at the group level.

We communicated with both the Directors and the Audit Committee our planned audit work via our audit planning report and relevant discussion. We communicated audit progress with the Audit Committee through interim audit progress.

Conclusions relating to going concern

In auditing the financial statements, we have concluded that the directors' use of the going concern basis of accounting in the preparation of the financial statements is appropriate.

Our evaluation of the Directors' assessment of the group's ability to continue to adopt the going concern basis of accounting included consideration of the inherent risks to the group's business model and analysed how those risks might affect the group's financial resources or ability to continue operations over the period 12 months from the date of the signing of the financial statements.

The risks that we considered most likely to affect the group's financial resources or ability to continue operations over this period were adverse circumstances impacting the underlying profitability of the trading subsidiaries and being able to fund potential contingent consideration relating to historic acquisitions, as well as the acquisition that was undertaken of Zero Carbon Group post year end.

We considered these risks through a review of the application of reasonably foreseeable downside scenarios that could arise with reference to the level of available financial resources indicated by the group's financial forecasts and management's assessment of these risks, including potential mitigations available.

Our audit procedures to evaluate the Director's assessment of the group and the company's ability to continue to adopt the going concern basis of accounting included:

- Undertaking an initial assessment at the planning stage of the audit to identify events or conditions that may cast significant doubt on the group and the company's ability to continue as a going concern;

- Evaluating the methodology used by the Directors to assess the group and the company's ability to continue as a going concern;

- Reviewing the Directors' going concern assessment and evaluating the key assumptions used and judgements applied;

- Reviewing the sensitivities performed by management to understand the going concern implications;

- Performing our own review of the liquidity headroom and applying sensitivities to the base trading and cashflow forecast assessments of the Directors to ensure there was sufficient headroom to adopt the going concern basis of accounting;

- Reviewing the availability of the group's existing cash balances for use in the day to day running of the business;

- Considered the reasonableness of management's reasonable worst case scenarios which included significant reductions in gross margin generated by newly acquired entities as well as entities which have been set up in the year, these included reductions in gross profit of 50%, consideration of the mitigating levers at managements disposal such as cutting of overhead costs and the timeliness in which these could be enacted should adverse scenarios occur;

- We evaluated management's ability to meet future contingent consideration obligations under a range of adverse scenarios to ensure there were no 'cliff edge' outcomes within the assessment prepared by management;

- We considered how reasonable the potential mitigants presented by management were, that would be required in adverse scenarios modelled as part of their going concern assessment, as well as in a range of further sensitivities prepared by ourselves;

- For newly acquired entities (both in year and post year end acquisitions, as well as entities set up in the year (being A&D Carbon Solutions Ltd, NRS Ltd, WLL Ltd, and Zero Carbon Energy Ltd), we reviewed management's pipeline forecasts to assess whether it was reasonable to expect revenues and profits to be generated by these entities - our further sensitivities assessed, considered delays in revenue generation and slower revenue generation than was included in management's base case forecast;

- We reviewed post year end cash balances to ensure the appropriate starting position was used in both the base case scenario, and all sensitised scenarios prepared by management;

- A review of post year end actuals compared to forecasts prepared by the Directors to note whether there was any adverse trading or change in underlying performance of the trading subsidiaries within the group that would impact the going concern assessment. Where adverse variances were noted, we obtained appropriate justification for these variances to determine whether there were fundamental issues with the forecasted revenues and profits of the entities included within the cashflow forecast;

- We ensured that management's forecasts included covenant testing review in both the base case and sensitised cases to determine whether any covenants relating to the bank loans held by the group would be in breach and, if so, whether there were suitable mitigants to enable the group to remain a going concern;

- For the acquisition of Zero Carbon Group made post year end, we completed a review of the revenue pipeline alongside supporting documentation to determine whether forecast overhead costs were included on a reasonable basis. We also reviewed the SPA to ensure that we understood the structure of future consideration payable, and ensured that this was factored into the cashflow forecast;

- Reviewing and assessing the appropriateness of the Directors' disclosures regarding going concern in the financial statements.

Based on the work we have performed, we have not identified any material uncertainties relating to events or conditions that, individually or collectively, may cast significant doubt on the group and the company's ability to continue as a going concern for a period of at least twelve months from when the financial statements are authorised for issue;

Our responsibilities and the responsibilities of the Directors with respect to going concern are described in the relevant sections of this report.

Key audit matters

Key audit matters are those matters that, in our professional judgement, were of most significance in our audit of the financial statements of the current period and include the most significant assessed risks of material misstatement (whether or not due to fraud) that we identified, including those which had the greatest effect on:

· the overall audit strategy,

· the allocation of resources in the audit; and

· directing the efforts of the engagement team.

These matters were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

In determining the key audit matters we considered the:

· Areas of higher risks of material misstatement or significant risks identified in accordance with ISA (UK) 315

· Significant audit judgements on financial statement line items that involved significant management judgement such as accounting estimates, and

· The impact of significant events and transactions during the period covered by the audit.

The following table summarises the key audit matters we have identified and rationale for their identification together we how we responded to each in our audit. The table also shows how our judgement of the magnitude of each risk has changed since the previous audit.

Risk magnitude key

|

|

|

|

|

|

||

|

Key audit matter |

How we addressed the key audit matter in the audit |

|||||

|

|

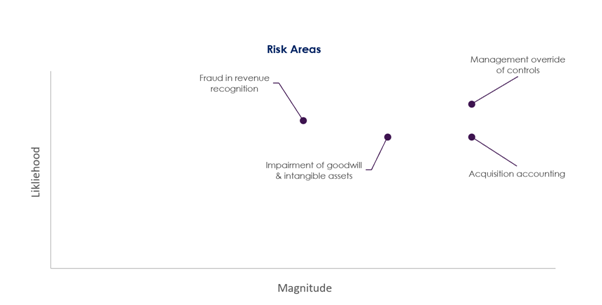

Fraud in revenue recognition The risk of incorrect or inappropriate treatment and recognition of revenue under IFRS 15. We consider there to be a significant risk of misstatement in the financial statements arising as a result of incorrect application of IFRS 15 and recording revenue when the performance obligations have not been met, thus resulting in a material misstatement of revenue.

The Group recognised revenue at a point in time and had revenue recognised over time. There is a risk that revenue is materially overstated if revenue has been recorded prior to the relevant performance obligations being satisfied.

Specifically, there is a risk in relation to the cut-off of revenue around the year-end and occurrence of revenue. Specific testing was planned to ensure this risk had been appropriately tested for.

|

We performed specific tests to consider whether revenue has been recorded in the correct period and is free from misstatement. These included: · We assessed the group's accounting policy for each material revenue stream and performed walkthrough procedures to assess the design and implementation of controls. · We performed substantive tests of detail for a sample of revenue items recorded during the year to assess whether revenue recognition was in accordance with the standard, including consideration of identification of performance obligations such that revenue had not been materially misstated. · We performed specific targeted cut-off testing around the year-end, with sales in December 2025 and January 2026 selected for testing to supporting documentation to ensure that revenue had been included within the correct period. · We utilised data analytics to identify unusual or unexpected revenue journal entries, including those posted outside normal business processes, and investigated any items identified. · We obtained and critically evaluated management's revenue recognition policy and whether the application of IFRS 15 was reasonable and appropriate. · For revenue recorded over time, we performed relevant testing on accrued and deferred income to ensure that revenue was being appropriately recognised during the year ended 31 December 2025. |

||||

|

|

Acquisition accounting and valuation of intangible assets

There is a risk that the acquisition accounting in relation to the acquisition of two trading subsidiaries during the year have been accounted for incorrectly with reference to IFRS 3 'Business Combinations'.

The risks we identified were as follows: · The accounting entries of the newly acquired entities in the group accounts · Over/misstatement of the fair value of the net assets acquired and the resulting goodwill being recorded · Identification and accounting of separately identifiable intangible assets arising on acquisition in accordance with IFRS 3 · Cut-off of the income and expenses from the point of acquisition to be recognised in the consolidated accounts · Completeness and cut-off of balance sheet of the entities being acquired at the date of acquisition. · Appropriateness of the disclosures in the financial statements relating to the acquisition of the new businesses. · Any impairment of the intangible assets including goodwill recognised as part of the acquisition may be materially overstated.

|

To address the risks associated with acquisition accounting and the valuation of intangible assets, our audit procedures consisted of but were not limited to: