Final Results for the Year Ended 31 December 2025

Summary by AI BETAClose X

THIS ANNOUNCEMENT CONTAINS INSIDE INFORMATION FOR THE PURPOSES OF ARTICLE 7 OF REGULATION 2014/596/EU WHICH IS PART OF DOMESTIC UK LAW PURSUANT TO THE MARKET ABUSE (AMENDMENT) (EU EXIT) REGULATIONS (SI 2019/310) ("UK MAR"). UPON THE PUBLICATION OF THIS ANNOUNCEMENT, THIS INSIDE INFORMATION (AS DEFINED IN UK MAR) IS NOW CONSIDERED TO BE IN THE PUBLIC DOMAIN.

NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY IN OR INTO THE UNITED STATES, AUSTRALIA, CANADA, JAPAN, THE REPUBLIC OF SOUTH AFRICA OR ANY OTHER JURISDICTION WHERE TO DO SO WOULD CONSTITUTE A VIOLATION OF THE RELEVANT LAWS OF SUCH JURISDICTION.

30 April 2026

Cobra Resources plc

("Cobra" or the "Company")

Final Results for the Year Ended 31 December 2025

Cobra (LSE: COBR), a South Australian mineral exploration and development company, announces its final results for the year ended 31 December 2025.

Highlights

Boland Rare Earth Project

A bottom quartile cost opportunity

· A staged programme of resource drilling within the palaeochannel system confirmed increased continuity of rare earth mineralisation and provided valuable geological and hydrogeological data that exceeded expectations and confirmed favourable conditions for in situ recovery (ISR) development.

· Metallurgical studies also confirmed the suitability of the low-cost, low disturbance ISR extraction method.

· Successfully produced the first Mixed Rare Earth Carbonate, with a heavy rare earth content of 14.5% - subsequent optimisation studies increased heavy rare earth content to 42.94% and 38.9% magnet rare earths with less than 0.9% impurities - this industry standout breakthrough puts Boland on the path towards sustainable, marketable production.

· Large-scale ISR column testing delivered exceptional results, confirming strong recoveries of rare earths while maintaining low acid consumption.

· Advanced environmental and hydrogeological studies required to support ISR development:

o Field tests delivered exceptional results reaffirming that geological conditions are conducive to ISR

o Pump tests proved that the hydrological properties of the Boland aquifer are a world-first, supporting the commerciality of Cobra's future mining operations.

· Studies advanced the economic credibility of the Boland Project by:

o Minimising sulphuric acid requirements by promoting natural acid generation

o Optimising product quality by utilising unique metallurgical properties that enable the removal of low-value rare earths from solution before precipitation

o Successfully demonstrating hydrology and permeability metrics that support ISR mining

· Work completed by CSIRO highlighted the unique and cost-effective nature of Boland mineralisation where sequential leach tests demonstrated recoveries of up to 25% with tap water.

· Secured a package of tenements from Tri-Star Group in May 2025 and demonstrated shared characteristics with Boland - significantly increasing the scale of the ionic rare earth system. Cobra now holds an extensive land position covering over 3,200km2 of prospective geology.

· Post year-end - conducted further resource drilling at the Boland and Head rare earth prospects.

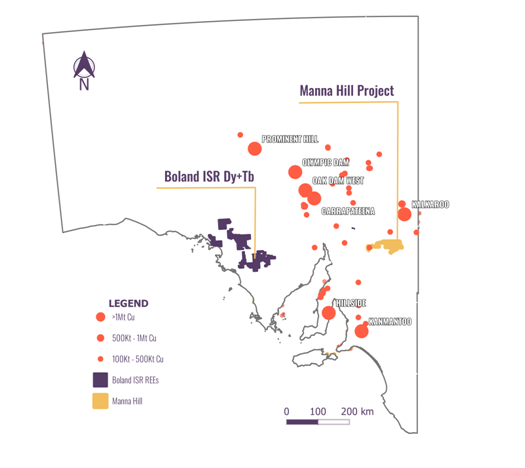

Manna Hill Copper Project

The making of a significant discovery

· Secured a 12-month option agreement to acquire the Manna Hill Copper Project in the Nackara Arc, South Australia, adding a substantial and underexplored 1,855 km² copper-gold opportunity to the portfolio.

· Post year-end - completed initial drill programme comprising 18 drillholes for 3,200m.

· Post year-end - reported results from the first 16 drillholes, with standout intersections including 74m at 1.02% copper and 62m at 1.0% copper.

o Results delivered from this initial programme have provided sufficient compelling evidence for economic scale. The Board proposes to exercise the Manna Hill Option and will seek shareholder approval to do so at the forthcoming AGM.

Corporate

· Completed the sale of the Wudinna Gold Assets for up to A$15 million, enabling the Company to increase its focus on advancing its rare earth and copper portfolio with retained upside exposure from a shareholding in the Barton Gold (BGD.AX), the purchaser.

· Post year-end - raised gross proceeds of £4.68 million through the issue of 116,999,995 ordinary shares to accelerate drilling at Manna Hill Copper Project while concurrently advancing the Boland Rare Earths Project through pre-feasibility.

· Appointed global mining industry leader Andrew Michelmore AO as Non-Executive Chairman.

Andrew Michelmore AO, Non-Executive Chairman, commented:

"2025 was a year that shaped Cobra for future value creation through a trifecta of portfolio developments in ISR rare earths, copper, and the divestment of non-core gold assets. On behalf of the Board, I commend Cobra's exploration team for delivering exceptionally successful drilling programmes during and after the period. These accomplishments not only validate the quality of Cobra's assets but also demonstrate the capability and commitment of its people on the ground. The Company's exploration programmes have the potential to establish it as a significant copper and rare earths developer in South Australia."

Enquiries:

|

Cobra Resources plc Rupert Verco (Australia) Dan Maling (UK)

|

via Vigo Consulting +44 (0)20 7390 0234

|

|

Hannam & Partners (Joint Broker) Leif Powis Andrew Chubb |

+44 (0)20 7907 8500

|

|

SI Capital Limited (Joint Broker) Nick Emerson Sam Lomanto |

+44 (0)1483 413 500

|

|

Vigo Consulting (Financial Public Relations) Ben Simons Seb Weller |

+44 (0)20 7390 0234 cobra@vigoconsulting.com |

The person who arranged for the release of this announcement was Rupert Verco, Managing Director of the Company.

About Cobra

Cobra Resources is a South Australian critical minerals developer, advancing assets at all stages of the pre-production pathway.

In 2023, Cobra identified the Boland ionic rare earth discovery at its Wudinna Project in the Gawler Craton - Australia's only rare earth project suitable for in situ recovery (ISR) mining. ISR is a low-cost, low-disturbance extraction method that eliminates the need for excavation, positioning Boland to achieve bottom-quartile recovery costs.

In 2025, Cobra further expanded its portfolio by optioning the Manna Hill Copper Project in the Nackara Arc, South Australia. The project contains multiple underexplored prospects with strong potential to deliver large-scale copper discoveries.

In 2025, Cobra sold its Wudinna Gold Assets to Barton Gold (ASX: BDG) for up to A$15 million in cash and shares.

Regional map showing Cobra's tenements in South Australia

Follow us on social media:

LinkedIn: https://www.linkedin.com/company/cobraresourcesplc

X: https://twitter.com/Cobra_Resources

Engage with us by asking questions, watching video summaries and seeing what other shareholders have to say. Navigate to our Interactive Investor hub here: https://investors.cobraplc.com/

Subscribe to our news alert service: https://investors.cobraplc.com/auth/signup

CHAIRMAN'S STATEMENT

I am pleased to present my first Chairman's Statement accompanying the Annual Report of Cobra since my appointment to the Board earlier this month.

2025 was a year that shaped Cobra for future value creation through a trifecta of portfolio developments. The Company advanced its plan to become the Western World's first controlled aquifer in situ recovery ("ISR") rare earth operation at Boland, demonstrating extraordinary metallurgy and scale potential; the Company also secured an option to acquire the highly prospective Manna Hill Cooper Project where Cobra has confirmed a discovery and is beginning to unlock a porphyry province; and Cobra capitalised on record gold prices to sell its non-core gold assets for up to A$15 million(£7.461M) with retained upside from a shareholding in the Barton Gold (BGD.AX), the purchaser.

Cobra's strategy now centres on three critical minerals for the energy transition: dysprosium, terbium and copper, with gold and molybdenum credits.

BOLAND PROJECT & ISR

Boland continued to deliver encouraging results during the year. A staged programme of aircore and sonic resource drilling was initiated within the palaeochannel system. Drilling confirmed increased continuity of rare earth mineralisation and provided valuable geological and hydrogeological data that exceeded expectations and confirmed favourable conditions for ISR development. Metallurgical studies also confirmed the suitability of the low-cost, low disturbance ISR extraction method at Boland.

Following the binding agreement to acquire a package of tenements from Tri-Star Group in May 2025, technical studies indicated the presence of a similar rare earth system on the Narlaby Palaeochannel which shares characteristics with Boland. Significantly increasing the scale of the ionic rare earth system, this discovery reflects an opportunity for further ISR-amenable rare earth mineralisation and emphasises the strength of Cobra's strategic acquisition of assets. Cobra now holds an extensive land position covering over 3,200km2 of prospective geology, following the completed acquisition of these exploration licences in January 2026.

The Company reported the production of an exceptionally high-grade maiden Mixed Rare Earth Carbonate ("MREC") product in January 2025. Comprised of 62.4% Total Rare Earth Oxides, this breakthrough was one of the highest grades produced from ionic REE projects globally. With a heavy rare earth content of 14.5%, the MREC was an industry standout that demonstrates the potential for high value return. Subsequent large-scale ISR column testing delivered exceptional results, confirming strong recoveries of rare earths while maintaining low acid consumption.

Important progress was also made in advancing the environmental and hydrogeological studies required to support ISR development. The Company received Environmental Protection and Rehabilitation approval from the Government of South Australia's Department for Energy and Mining to conduct in-field permeability studies at Boland. These field tests delivered exceptional results which aligned with the Company's expectations that geological conditions are conducive to ISR. Pump tests proved that the hydrological properties of the Boland aquifer are a world-first, supporting the commerciality of Cobra's future mining operations.

Through the work programme delivered in 2025, and continuing in 2026, the Company is defining a breakthrough approach to overcoming industry challenges associated with clay hosted rare earth mining and processing. The Company's strategy has been driven by the principle that to define a rare earth project of true value, the mineral occurrence requires advantageous properties that:

· Can be mined at a low-cost

· Can be cost-effectively processed, where mineralogy and lithology drive economic metallurgy

· Allow sustainable sourcing, through value-add or low impact extraction

Through studies completed in 2025, the Company has advanced the economic credibility of the Boland project by:

· Minimising sulphuric acid requirements by promoting natural acid generation

· Optimising product quality by utilising unique metallurgical properties that enable the removal of low-value rare earths from solution before precipitation

· Successfully demonstrating hydrology and permeability metrics that support in situ recovery mining

Work completed by CSIRO in 2025 highlighted the unique and cost-effective nature of Boland mineralisation where sequential leach tests demonstrated recoveries of up to 25% with tap water. The Company has focused on addressing technical risk, particularly metallurgy, hydrology and product quality. The work completed during 2025 places the Boland Project as a bottom quartile cost opportunity.

Key Boland developments post year end

Another milestone was the production of an industry leading MREC post year end. Further flowsheet optimisation work demonstrated the ability to improve the value of the final rare earth product by removing up to 100% of low-value cerium prior to precipitation. Not only can cerium carbonate be sold as a separate by-product, but the upgraded MREC product produced in March 2026 resulted in an industry leading heavy rare earth carbonate containing 42.94% heavy Rare earths and 38.9% magnet rare earths with less than 0.9% impurities.

Produced from ISR at a very low cost and via low disturbance mining methods, the high purity and quality of the MREC represents significant progress in process optimisation, successfully increasing the value and marketability of the project's saleable product. Compared to the first MREC production described above from early 2025, this development represented a ~170% increase in product value, based on its rare earth proportions. The breakthrough puts the Boland Project on the path towards sustainable, marketable production.

Having proven outstanding metallurgy, resource definition drilling was completed at the Boland and Head rare earth prospects in April 2026, with results expected over the coming months.

Manna Hill Copper Project

In August 2025, the Company entered into a 12-month option agreement to acquire the Manna Hill Copper Project in the Nackara Arc, South Australia, adding a substantial and underexplored 1,855 km² copper-gold opportunity to the portfolio and complementing the ionic rare earths discovery at Boland. The project focuses initially on the Blue Rose priority prospect, where the Program for Environment Protection and Rehabilitation approved up to 50 drillholes. The Company progressed an Induced Polarisation ("IP") survey to validate its interpretation of the scale of existing mineralisation, and to improve the targeting of the porphyry system. Such work aimed to demonstrate the potential of the Manna Hill asset ahead of looking to exercise the option to acquire the project, subject to shareholder approval, this year.

Key Manna Hill developments post year end

In January 2026, the initial drilling programme at Manna Hill, comprising 18 drillholes for 3,200m, was completed. By mid-April 2026, Cobra had reported results from the first 16 drillholes, with standout intersections including 74m at 1.02% copper and 62m at 1.0% copper. Results delivered from this initial programme have provided sufficient compelling evidence for economic scale. The Board proposes to exercise the Manna Hill Option and will seek shareholder approval to do so at the forthcoming AGM.

Portfolio Development

In addition to the acquisition of rare earth tenements from Tri-Star Group and the option to acquire Manna Hill, the Company optimises its asset portfolio during the year.

The Wudinna Gold Assets comprised a 279,000-ounce gold JORC Mineral Resource Estimate defined by Cobra in 2023, prior to the Boland discovery. In June 2025, the Company announced the completed sale of these assets to Barton Gold, and has to date received A$1 million(£497,300), comprising A$200,000(£99,460) in cash payments and A$800,000(£397,840) through the issue of 1,025,619 Barton Gold shares. Upon final settlement, which will occur at the completion of procedural approvals, Cobra will receive a further 5,384,615 shares and cash. Cobra will receive future payments of up to A$15 million(£7,459,500) in total deal consideration. The strategic transaction offers Cobra the opportunity to become a significant shareholder in a province-scale gold strategy, while minimising the capital expenditure required to optimise the value of small-to-mid size gold deposits of this kind. Granting the Company greater capacity to maximise value from Boland and Manna Hill, the deal still maintains Cobra's exposure to future upside through milestone payments and production-linked consideration.

Corporate developments post year end

Post year end, the Company established an Employee Benefit Trust ("EBT") to implement a proposed Performance Rights framework for executive directors and senior management. The EBT is designed to align employee and shareholder interests.

In March 2026, the company raised gross proceeds of £4.68 million through the issue of 116,999,995 ordinary shares to accelerate drilling at Manna Hill Copper Project while concurrently advancing the Boland Rare Earths project through pre-feasibility.

Conclusion

The metallurgical progress achieved during the year has significantly advanced the Boland project towards demonstrating the technical and economic viability of ISR extraction for rare earth elements.

Drilling programmes have confirmed the continuity of mineralisation across the palaeochannel system, while metallurgical and hydrogeological studies continue to demonstrate favourable conditions for ISR development. Resource definition drilling has recently completed at Boland and Head to demonstrate the scale and economic potential to underpin a multigenerational operation. Cobra looks forward to reporting on the results of this over the coming months.

With the exciting copper discovery at Blue Rose announced in March 2026, the requisite approvals have been received in respect of a planned further programme comprising 29 RC drillholes and three

diamond drillholes at Blue Rose. Cobra also intends to expand the initial focus beyond Blue Rose to test the greater porphyry system as well as the Netley Hill, Anabama and Golden Sophia targets.

Together, the Company's exploration programmes have the potential to establish Cobra as a significant copper and rare earths developer in South Australia.

I would also like to record the Board's sincere thanks to Greg Hancock, who stepped down from the Board during the period after eight years of service. Greg has made a significant contribution to the Company, providing valuable insight, leadership and guidance throughout his tenure, and the Board is grateful for his commitment and dedication to Cobra.

On behalf of the Board, I commend Cobra's exploration team for delivering exceptionally successful drilling programmes during and after the period. The team has evidently achieved outstanding results while maintaining tight cost control and operational safety. These accomplishments not only validate the quality of Cobra's assets but also demonstrate the capability and commitment of its people on the ground. The Board extends its congratulations to all involved for their professionalism and dedication.

Andrew Michelmore AO

Non-Executive Chairman

30 April 2026

CONSOLIDATED INCOME STATEMENT

FOR THE YEAR ENDED 31 DECEMBER 2025

|

|

Notes |

31 December |

31 December |

|

|

|

2025 |

2024 |

|

|

|

£ |

£ |

|

Gain on Financial Instruments at Fair Value through profit or loss |

16 |

1,441,413 |

- |

|

Other Income |

|

- |

91,267 |

|

Other Expenses |

2 |

(1,128,838) |

(565,298) |

|

Exploration Expenditure |

|

(140,503) |

- |

|

Loss on disposal |

|

(5,697) |

- |

|

Operating Profit/(Loss) |

|

166,375 |

(474,031) |

|

Net finance income |

3 |

13,514 |

7,169 |

|

|

|

179,889 |

(466,862) |

|

Change in estimate of contingent consideration |

14 |

- |

43,527 |

|

Profit/(Loss) before tax |

|

179,889 |

(423,336) |

|

Taxation |

6 |

- |

- |

|

Profit/(Loss) for the year attributable to equity holders |

|

179,889 |

(423,336) |

|

Earnings per Ordinary share |

|

|

|

|

Basic profit/(loss) per share attributable to owners of the Parent Company

|

7 |

£0.0002 |

(£0.0006) |

|

Diluted profit/(loss) per share attributable to owners of the Parent Company

|

|

£0.0002 |

(£0.0006) |

All operations are considered to be continuing.

The accompanying notes are an integral part of these financial statements.

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

FOR THE YEAR ENDED 31 DECEMBER 2025

|

|

|

31 December |

31 December |

|

|

|

|

2025 |

2024 |

|

|

|

|

£ |

£ |

|

|

Profit / (Loss) for the year |

|

179,889 |

(423,336) |

|

|

Other Comprehensive income Items that may subsequently be reclassified to profit or loss: |

|

|

|

|

|

- Exchange differences on translation of foreign operations |

|

13,305 |

(305,161) |

|

|

Items that will not be reclassified subsequently to profit or loss: |

|

|

|

|

|

- Fair value movement on equity instruments at FVOCI |

|

275,413 |

- |

|

|

|

|

|

|

|

|

Total comprehensive profit / (loss) attributable to equity holders of the Parent Company |

|

468,607 |

(728,497) |

|

|

|

|

|

|

|

|

The accompanying notes are an integral part of these financial statements.

|

|

|

|

|

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

31 DECEMBER 2025

|

|

Notes |

|

|

|

|

|

2025 |

2024 |

|

|

|

£ |

£ |

|

Non-current assets |

|

|

|

|

Intangible Fixed Assets |

9 |

2,329,659 |

4,318,175 |

|

Property, plant and equipment |

10 |

4,544 |

4,526 |

|

Other non-current assets |

11 |

35,308 |

35,088 |

|

Financial asset - Equity instruments (FVTPL) |

16 |

3,534,580 |

- |

|

Total non-current assets |

|

5,904,091 |

4,357,789 |

|

|

|

|

|

|

Current assets |

|

|

|

|

Trade and other receivables |

11 |

209,323 |

144,746 |

|

Cash and cash equivalents |

12 |

1,562,502 |

795,708 |

|

Financial asset - Equity instruments (FVOCI) |

16 |

673,254 |

- |

|

Total current assets |

|

2,445,079 |

940,454 |

|

|

|

|

|

|

Current liabilities |

|

|

|

|

Trade and other payables |

13 |

217,314 |

171,101 |

|

Contingent consideration |

14 |

119,698 |

119,698 |

|

Total current liabilities |

|

337,012 |

290,799 |

|

|

|

|

|

|

Net assets |

|

8,012,158 |

5,007,444 |

|

|

|

|

|

|

Capital and reserves |

|

|

|

|

Share capital |

15 |

9,358,860 |

7,988,713 |

|

Share premium account |

|

3,950,098 |

2,821,139 |

|

Share based payment reserve |

|

89,473 |

52,472 |

|

Retained losses |

|

(5,512,740) |

(5,692,629) |

|

Foreign currency reserve |

|

(148,946) |

(162,251) |

|

Equity Revaluation Reserve |

|

275,413 |

- |

|

Total equity |

|

8,012,158 |

5,007,444 |

The accompanying notes are an integral part of these financial statements.

These financial statements were approved and authorised for issue by the Board of Directors on 30 April 2026.

Signed on behalf of the Board of Directors

Rupert Verco, Managing Director, Company No. 11170056

PARENT COMPANY STATEMENT OF FINANCIAL POSITION

31 DECEMBER 2025

|

|

Notes |

|

|

|

|

|

2025 |

2024 |

|

|

|

£ |

£ |

|

Non-current assets |

|

|

|

|

Investment in subsidiary |

8 |

562,260 |

562,260 |

|

Property, plant and equipment |

10 |

1,428 |

1,428 |

|

Intangible Fixed Assets |

9 |

- |

- |

|

Total non-current assets |

|

563,688 |

563,688 |

|

|

|

|

|

|

Current assets |

|

|

|

|

Trade and other receivables |

11 |

6,453,865 |

5,019,440 |

|

Cash and cash equivalents |

12 |

1,183,365 |

690,633 |

|

Total current assets |

|

7,637,230 |

5,710,073 |

|

|

|

|

|

|

Current liabilities |

|

|

|

|

Trade and other payables |

13 |

83,005 |

67,168 |

|

Contingent consideration |

14 |

119,698 |

119,698 |

|

Total current liabilities |

|

202,703 |

186,866 |

|

|

|

|

|

|

Net assets |

|

7,998,215 |

6,086,895 |

|

|

|

|

|

|

Capital and reserves |

|

|

|

|

Share capital |

15 |

9,358,860 |

7,988,713 |

|

Share premium account |

|

3,950,098 |

2,821,139 |

|

Share based payment reserve |

|

89,473 |

52,472 |

|

Retained losses |

|

(5,400,216) |

(4,775,430) |

|

Equity shareholders' funds |

|

7,998,215 |

6,086,895 |

The Company has taken advantage of the exemption allowed under section 408 of the Companies Act 2006 and has not included its own income statement and statement of comprehensive income in these financial statements. The Parent Company's loss for the period amounted to £624,786 (2024: £302,847 loss).

The accompanying notes are an integral part of these financial statements.

These financial statements were approved and authorised for issue by the Board of Directors on 30 April 2026.

Signed on behalf of the Board of Directors

Rupert Verco, Managing Director, Company No. 11170056

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 31 DECEMBER 2025

|

|

Share capital |

Share premium |

Share based payment reserve |

Retained losses |

Equity revaluation reserve |

Foreign currency reserve |

Total |

|

|

|

|

|

|

|

|

|

|

|

£ |

£ |

£ |

£ |

£ |

£ |

£ |

|

|

|

|

|

|

|

|

|

|

As at 1 January 2024 |

5,923,794 |

2,785,366 |

21,476 |

(5,269,293) |

- |

142,906 |

3,604,249 |

|

Loss for the year |

- |

- |

- |

(423,336) |

- |

|

(423,336) |

|

Translation differences |

- |

- |

- |

- |

- |

(305,161) |

(305,161) |

|

Total Comprehensive loss for the year |

- |

- |

- |

(423,336) |

- |

(305,161) |

(728,497) |

|

Shares issued |

2,064,919 |

108,468 |

- |

- |

- |

|

2,173,386 |

|

Share issue cost |

- |

(72,695) |

- |

- |

- |

|

(72,695) |

|

Share options charge |

- |

- |

30,997 |

- |

- |

|

30,997 |

|

Total transactions with owners |

2,064,919 |

35,773 |

30,997 |

- |

- |

|

2,131,689 |

|

At 31 December 2024 |

7,988,713 |

2,821,139 |

52,473 |

(5,692,629) |

- |

(162,251) |

5,007,444 |

|

Profit/(Loss) for the year |

- |

- |

- |

179,889 |

- |

|

179,889 |

|

Fair value movements - financial assets at fair value through OCI |

- |

- |

- |

- |

275,413 |

- |

275,413 |

|

Translation differences |

- |

- |

- |

- |

- |

13,305 |

13,305 |

|

Total Comprehensive Income/(loss) for the year |

- |

- |

- |

179,889 |

275,413 |

13,305 |

468,607 |

|

Shares issued nett of costs |

1,370,147 |

1,128,959 |

- |

- |

- |

|

2,499,106 |

|

Share options charge |

- |

- |

37,000 |

- |

- |

- |

37,000 |

|

Total transactions with owners |

1,370,147 |

1,128,959 |

37,000 |

- |

- |

|

2,536,106 |

|

At 31 December 2025 |

9,358,860 |

3,950,098 |

89,473 |

(5,512,740) |

275,413 |

(148,946) |

8,012,158 |

The following describes the nature and purpose of each reserve within equity:

Share capital: Nominal value of shares issued

Share premium: Amount subscribed for share capital in excess of nominal value, less share issue costs

Share based payment reserve: Cumulative fair value of warrants and options granted

Retained losses: Cumulative net gains and losses, recognised in the statement of comprehensive income

Equity revaluation reserve: Equity instruments designated as financial assets at fair value through other comprehensive

income

Foreign currency reserve: Gains/losses arising on translation of foreign controlled entities into pounds sterling.

The accompanying notes are an integral part of these financial statements.

PARENT COMPANY STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 31 DECEMBER 2025

|

|

Share |

Share |

Share based |

Retained |

Total |

|

|

capital |

premium |

payment |

losses |

|

|

|

|

|

reserve |

|

|

|

|

|

|

|

|

|

|

|

£ |

£ |

£ |

£ |

£ |

|

As at 1 January 2024 |

5,923,794 |

2,785,366 |

21,476 |

(4,472,583) |

4,258,053 |

|

Loss for the year |

- |

- |

- |

(302,847) |

(302,847) |

|

Total Comprehensive loss for the year |

- |

- |

- |

(302,847) |

(302,847) |

|

Shares issued |

2,064,919 |

108,468 |

- |

- |

2,173,386 |

|

Share issue costs |

- |

(72,695) |

- |

- |

(72,695) |

|

Share option charge |

- |

- |

30,997 |

- |

30,997 |

|

Total transactions with owners |

2,064,919 |

35,773 |

30,997 |

- |

2,131,689 |

|

At 31 December 2024 |

7,988,713 |

2,821,139 |

52,473 |

(4,775,430) |

6,086,895 |

|

Loss for the year |

- |

- |

- |

(624,786) |

(624,786) |

|

Total Comprehensive loss for the year |

- |

- |

- |

(624,786) |

(624,786) |

|

Shares issued nett of costs |

1,370,147 |

1,128,959 |

- |

- |

2,499,106 |

|

Share option charge |

- |

- |

37,000 |

- |

37,000 |

|

Total transactions with owners |

1,370,147 |

1,128,959 |

37,000 |

- |

2,536,106 |

|

At 31 December 2025 |

9,358,860 |

3,950,098 |

89,473 |

(5,400,216) |

7,998,215 |

The following describes the nature and purpose of each reserve within equity:

Share capital: Nominal value of shares issued

Share premium: Amount subscribed for share capital in excess of nominal value, less share issue costs

Share based payment reserve: Cumulative fair value of warrants and options granted

Retained losses: Cumulative net gains and losses, recognised in the statement of comprehensive income

The accompanying notes are an integral part of these financial statements.

CONSOLIDATED CASH FLOW STATEMENT

FOR THE YEAR ENDED 31 DECEMBER 2025

|

|

Notes |

31 December |

31 December |

|

|

|

2025 |

2024 |

|

|

|

£ |

£ |

|

Cash flows from operating activities |

|

|

|

|

Profit/(Loss) before tax |

|

179,889 |

(423,336) |

|

Share-based payments |

|

37,000 |

30,997 |

|

Consulting fees settled in shares |

|

65,000 |

11,700 |

|

Loss/(Profit) on sale of investments |

|

5,697 |

- |

|

Gain on Financial Instruments at Fair Value through profit or loss |

|

(1,441,413) |

- |

|

Foreign exchange |

|

(7,653) |

(997) |

|

Interest income |

3 |

(13,606) |

(7,611) |

|

Other Income |

|

- |

(61,423) |

|

Fair value (gain)/loss on contingent consideration |

14 |

- |

(43,527) |

|

Decrease/(increase) in trade and other receivables |

11 |

84,423 |

(108,498) |

|

(Increase)/decrease in other non-current assets |

11 |

- |

(4,052) |

|

Increase / (decrease) in trade and other payables |

13 |

56,729 |

(27,583) |

|

Net cash used in operating activities |

|

(1,033,934) |

(634,330) |

|

|

|

|

|

|

Cash flows from investing activities |

|

|

|

|

Payments for exploration and evaluation activities |

9 |

(746,444) |

(767,063) |

|

Payments for property, plant and equipment |

10 |

- |

(2,875) |

|

Proceeds from the sale of intangible assets |

|

99,460 |

- |

|

Interest received |

3 |

13,606 |

7,611 |

|

Net cash used in investing activities |

|

(633,378) |

(762,327) |

|

|

|

|

|

|

Cash flows from financing activities |

|

|

|

|

Proceeds from the issue of shares |

15 |

2,444,620 |

1,626,586 |

|

Payment of share issuance costs |

|

(10,514) |

(72,695) |

|

Net cash generated from financing activities |

|

2,434,106 |

1,553,891 |

|

|

|

|

|

|

Net increase/(decrease) in cash and cash equivalents |

|

766,794 |

157,234 |

|

Cash and cash equivalents at beginning of year |

|

795,708 |

638,475 |

|

Cash and cash equivalents at end of year |

12 |

1,562,502 |

795,708 |

Major non- cash transactions

During the 2024 year the group acquired the remaining 25% of the Wudinna Project through issuing a further 52,010,000 shares at 1p each to Peninsula Resources Pty Ltd, and additional £25,000 in fees owing to suppliers were settled via the issue of 2,500,000 Ordinary shares at 1p each.

The accompanying notes are an integral part of these financial statements.

PARENT COMPANY CASH FLOW STATEMENT

FOR THE YEAR ENDED 31 DECEMBER 2025

|

|

Notes |

31 December |

31 December |

|

|

|

2025 |

2024 |

|

|

|

£ |

£ |

|

|

|

|

|

|

Cash flows from operating activities |

|

|

|

|

Loss before tax |

|

(624,786) |

(302,847) |

|

Share based payments |

|

37,000 |

30,977 |

|

Consulting fees settled in shares |

|

65,000 |

11,700 |

|

Fair value loss/(gain) on contingent consideration |

14 |

- |

(43,527) |

|

VAT reclaimable from prior period |

|

- |

(61,423) |

|

(Increase) in trade and other receivables |

11 |

(1,434,424) |

(596,661) |

|

Increase / (decrease) in trade and other payables |

13 |

15,837 |

(99,568) |

|

Net cash used in operating activities |

|

(1,941,374) |

(1,061,329) |

|

|

|

|

|

|

Cash flows from investing activities |

|

|

|

|

Loan to Subsidiary |

11 |

- |

(115,000) |

|

Net cash used in investing activities |

|

- |

(115,000) |

|

|

|

|

|

|

Cash flows from financing activities |

|

|

|

|

Nett proceeds from the issue of shares |

|

2,444,620 |

1,626,586 |

|

Payment of share issue costs |

|

(10,514) |

(72,695) |

|

Net cash generated from financing activities |

|

2,434,106 |

1,553,891 |

|

|

|

|

|

|

Net increase/(decrease) in cash and cash equivalents |

|

492,732 |

377,562 |

|

Cash and cash equivalents at beginning of year |

|

690,633 |

313,071 |

|

Cash and cash equivalents at end of year |

12 |

1,183,365 |

690,633 |

Major non-cash transactions

During the prior year the group acquired the remaining 25% of the Wudinna Project through issuing a further 52,010,000 shares at 1p each to Peninsula Resources Pty Ltd, and additional £25,000 in fees owing to suppliers were settled via the issue of 2,500,000 Ordinary shares at 1p each.

The accompanying notes are an integral part of these financial statements

NOTES TO THE FINANCIAL STATEMENTS

1. ACCOUNTING POLICIES AND BASIS OF PREPARATION

General information

The Company is a public company limited by shares which is incorporated in England. The registered office of the Company is 9th Floor, 107 Cheapside, London, EC2V 6DN, United Kingdom. The registered number of the Company is 11170056.

The principal activity of the Group is to objective is to explore, develop and mine precious and base metal projects.

Summary of significant accounting policies

The principal accounting policies applied in the preparation of these Financial Statements are set out below ('Accounting Policies' or 'Policies'). These Policies have been consistently applied to all the periods presented, unless otherwise stated.

Accounting policies

Basis of preparation of Financial Statements

These financial statements have been prepared in accordance with UK-adopted international accounting standards and with the requirements of the Companies Act 2006. The Group and Company Financial Statements have also been prepared under the historical cost convention, except as modified for assets and liabilities recognised at fair value on an asset acquisition.

The Financial Statements are presented in pounds sterling, which is the functional currency of the Parent Company. The functional currency of Lady Alice Mines Pty Ltd is Australian Dollars.

The preparation of the Financial Statements in conformity with IFRS requires the use of certain critical accounting estimates. It also requires the Board to exercise its judgement in the process of applying the Group's accounting policies. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the Financial Statements are disclosed in Note 1.

Changes in accounting policies

i) New and amended standards adopted by the Group and Company

The International Accounting Standards Board (IASB) issued various amendments and revisions to International Financial Reporting Standards and IFRIC interpretations. The amendments and revisions were applicable for the period ended 31 December 2025 but did not result in any material changes to the financial statements of the Group or Company.

Of the other IFRS and IFRIC amendments, none are expected to have a material effect on the future Group or Company Financial Statements.

ii) New standards, amendments and interpretations that are not yet effective and have not been early adopted are as follows:

· IFRS S1: General Requirements for Disclosure of Sustainability-related Financial Information (effective date TBC*);

· IFRS S2: Climate-related Disclosures (effective date TBC*);

· IFRS 18: Presentation and Disclosure in Financial Statements (effective date 1 January 2027);

· Amendments to IFRS 9: Financial Instruments and IRFS 7 Financial Instruments: Disclosures (effective date 1 January 2026); and

· Annual Improvements to IFRS standards - Volume 11 (effective date 1 January 2026).

*available for use but not yet endorsed in the UK.

None are expected to have a material effect on the Group or Company Financial Statements.

Going concern

The Financial Statements have been prepared on a going concern basis. In assessing whether the going concern assumption is appropriate, the Directors have taken into account all relevant available information about the current and future position of the Group and Company, including the current level of resources and the required level of spending on exploration and evaluation activities. As part of their assessment, the Directors have also taken into account the ability to raise additional funding whilst maintaining sufficient cash resources to meet all commitments. The Board regularly reviews market conditions, the Group's cash balance in alignment with the Company's forward commitments and shall where deemed necessary revise expenditure commitments, defer director payments and terminate short term contracts as a means of cash preservation. Post-period end, the Company raised a further £4,680,000 under the Company's head room with £3,000,000 coming from Australian major shareholders, directors and other subscribers.

The Group meets its working capital requirements from its cash and cash equivalents. The Company is pre-revenue, and to date the Company has raised finance for its activities through the issue of equity and debt.

The Group has £1,562,502 of cash and cash equivalents at 31 December 2025. The Group's and Company's ability to meet operational objectives and general overheads is reliant on the need to raise funds within the next 12 months to achieve its 12-month operational objectives

The Directors are confident that further funds can be raised and it is appropriate to prepare the financial statements on a going concern basis, however there can be no certainty that any fundraise will complete. These conditions indicate existence of a material uncertainty related to events or conditions that may cast significant doubt about the Group's and Company's ability to continue as a going concern, and, therefore, that it may be unable to realise its assets and discharge its liabilities in the normal course of business. These financial statements do not include the adjustments that would be required if the Group and Company could not continue as a going concern.

Basis of consolidation

The consolidated financial statements incorporate the financial statements of the Parent Company and companies controlled by the Parent Company, the Subsidiary Companies, drawn up to 31 December each year.

Control is recognised where the Company has the power to govern the financial and operating policies of an investee entity so as to obtain benefits from its activities, and is exposed to, or has rights to, variable returns from its involvement in the subsidiary. The results of subsidiaries acquired or disposed of during the year are included in the consolidated income statement from the effective date of acquisition or up to the effective date of disposal, where appropriate.

Where necessary, adjustments are made to the financial statements of subsidiaries to bring the accounting policies used into line with those used by the Group. All intra-group transactions, balances, income and expenses are eliminated on consolidation.

The Group applies the acquisition method of accounting to account for business combinations. The consideration transferred for the acquisition of a subsidiary is the fair values of the assets transferred, the liabilities incurred to the former owners of the acquiree and the equity interests issued by the Group. The consideration transferred includes the fair value of any asset or liability resulting from a contingent consideration arrangement. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values at the acquisition date.

Acquisition-related costs are expensed as incurred unless they result from the issuance of shares, in which case they are offset against the premium on those shares within equity.

Any contingent consideration to be transferred by the Group is recognised at fair value at the acquisition date. Subsequent changes to the fair value of the contingent consideration that is deemed to be an asset or liability is recognised either in profit or loss or as a change to other comprehensive income. Contingent consideration that is classified as equity is not re-measured, and its subsequent settlement is accounted for within equity.

Investments in subsidiaries are accounted for at cost less impairment.

Segmental reporting

Operating segments are reported in a manner consistent with the internal reporting provided to the chief operating decision-maker. The chief operating decision-maker, who is responsible for allocating resources and assessing performance of the operating segments, has been identified as the Board of Directors that makes strategic decisions.

The Group's operations are located Australia with the head office located in the United Kingdom. The main tangible assets of the Group, cash and cash equivalents, are held in the United Kingdom and Australia. The Board ensures that adequate amounts are transferred internally to allow all companies to carry out their operational on a timely basis.

The Directors are of the opinion that the Group is engaged in a single segment of business being the exploration of gold in Australia. The Group currently has two geographical reportable segments - United Kingdom and Australia.

Foreign currencies

For the purposes of the consolidated financial statements, the results and financial position of each Group entity are expressed in pounds sterling, which is the presentation currency for the consolidated financial statements.

In preparing the financial statements of the individual entities, transactions in currencies other than the entity's functional currency (foreign currencies) are recorded at the rates of exchange prevailing at the dates of the transactions. At each reporting date, monetary items denominated in foreign currencies are retranslated at the rates prevailing at the reporting date. Exchange differences arising are included in the profit or loss for the period.

For the purposes of preparing consolidated financial statements, the assets and liabilities of the Group's foreign operations are translated at exchange rates prevailing on the reporting date. Income and expense items are translated at the average exchange rates for the period. Gains and losses from exchange differences so arising are shown through the Consolidated Statement of Changes in Equity.

Property, plant and equipment

Property, plant and equipment is stated at cost less accumulated depreciation and any accumulated impairment losses. Depreciation is provided on all property, plant and equipment to write off the cost less estimated residual value of each asset over its expected useful economic life on a straight-line basis at the following annual rates: Office Equipment: 33.33% per annum

The assets' residual values and useful lives are reviewed, and adjusted if appropriate, at the end of each reporting period. An asset's carrying amount is written down immediately to its recoverable amount if the asset's carrying amount is greater than its estimated recoverable amount. Gains and losses on disposal are determined by comparing the proceeds with the carrying amount and are recognised within 'Other (losses)/gains' in the Statement of Comprehensive Income.

Impairment of tangible fixed assets

A review for indicators of impairment is carried out at each reporting date, with the recoverable amount being estimated where such indicators exist. Where the carrying value exceeds the recoverable amount, the asset is impaired accordingly. Prior impairments are also reviewed for possible reversal at each reporting date.

For the purposes of impairment testing, when it is not possible to estimate the recoverable amount of an individual asset, an estimate is made of the recoverable amount of the cash-generating unit to which the asset belongs. The cash-generating unit is the smallest identifiable group of assets that includes the asset and generates cash inflows that largely independent of the cash inflows from other assets or groups of assets.

Exploration and evaluation assets

Exploration and evaluation assets, held as intangible fixed assets on the statement of financial position comprises all costs which are directly attributable to the exploration of a project area. The Group recognises expenditure as exploration and evaluation assets when it determines that those assets will be successful in finding specific mineral resources. Expenditure capitalised as exploration and evaluation assets relates to the acquisition of rights to explore, topographical, geological, geochemical and geophysical studies, exploratory drilling, trenching, sampling and activities to evaluate the technical feasibility and commercial viability of extracting a mineral resource. Capitalisation of pre-production expenditure ceases when the mining property is capable of commercial production.

Treatment of options to acquire exploration assets and equity

The Group enters into different types of option arrangements, which are accounted for based on the nature of the rights obtained and the substance of the transaction, in accordance with IFRS 6 and relevant IFRS guidance.

Options to acquire exploration assets (including option agreements)

Where the Group acquires an option to earn an interest in an exploration licence or mineral project, and the option conveys substantive exploration rights that enable the Group to access the area and undertake exploration and evaluation activities, option costs are capitalised as exploration and evaluation assets. Subsequent exploration and evaluation expenditure incurred under such option agreements is also capitalised, provided it is directly attributable to exploration activities within the option area.

This treatment is considered appropriate under IFRS 6, as:

· the option cost represents consideration paid to obtain the right to explore for mineral resources; and

· the subsequent expenditure relates directly to exploration and evaluation activities aimed at identifying mineral resources.

IFRS 6 permits the capitalisation of expenditures incurred in obtaining the right to explore and costs incurred in the exploration for and evaluation of mineral resources prior to the demonstration of technical feasibility and commercial viability. Capitalised option-related costs are assessed for impairment in accordance with the Group's impairment policy for exploration and evaluation assets.

Options to purchase equity interests

Where the Group acquires an option to purchase equity instruments in another entity (for example, an option to acquire shares in a company holding exploration assets), and the option does not itself convey direct exploration rights or an interest in an exploration licence, the cost of the option and further expenditures in the option period prior to exercise, are expenses as incurredis expensed as incurred.

This is because:

· the option relates to a potential future investment in equity, rather than the acquisition of a right to explore for mineral resources; and

· the expenditure does not meet the definition of an exploration and evaluation asset under IFRS 6, as it is not directly attributable to exploration or evaluation activities.

Accordingly, such costs are recognised in profit or loss and are not capitalised as exploration and evaluation assets.

Exploration and evaluation assets recorded at fair-value on acquisition

Exploration assets which are acquired are recognised at fair value. When an acquisition of an entity whose only significant assets are its exploration asset and/or rights to explore, the Directors consider that the fair value of the exploration assets is equal to the consideration. Any excess of the consideration over the capitalised exploration asset is attributed to the fair value of the exploration asset.

Impairment of intangible assets

Intangible assets that have an indefinite useful life are not subject to amortisation and are tested annually for impairment, or more frequently if events or changes in circumstances indicate that they might be impaired. Other assets are tested for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised in profit or loss for the amount by which the asset's carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset's fair value less costs of disposal and value in use. For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash inflows which are largely independent of the cash inflows from other assets or groups of assets (cash-generating units). Early stage exploration projects are assessed for impairment using the methods specified in IFRS 6.

Financial Assets

Loans and Receivables

(a) Classified as receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an instrument level.

The Group's and Company's business model for managing financial assets refers to how it manages its financial assets in order to generate cash flows. The business model determines whether cash flows will result from collecting contractual cash flows, selling the financial assets, or both.

Subsequent measurement

For purposes of subsequent measurement, financial assets are classified in four categories:

• financial assets at amortised cost (debt instruments);

• financial assets at fair value through OCI with recycling of cumulative gains and losses through profit or loss (debt instruments);

• financial assets designated at fair value through OCI with no recycling of cumulative gains and losses upon derecognition through profit or loss (equity instruments); and

• financial assets at fair value through profit or loss.

Financial assets at amortised cost (debt instruments)

This category is the most relevant to the Group and Company. The Group and Company measure financial assets at amortised cost if both of the following conditions are met:

• the financial asset is held within a business model with the objective to hold financial assets in order to collect contractual cash flows; and

• the contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

Financial assets designated at fair value through OCI with no recycling of cumulative gains and losses upon derecognition through profit or loss (equity instruments)

· Upon initial recognition, the Group and the Company may make an irrevocable election to present subsequent changes in the fair value of certain equity instruments in other comprehensive income,provided that the equity instruments are not held for trading. The election is made separately for each relevant equity instrument and applies only to equity instruments within the scope of IFRS 9.

· Financial assets in this category are initially recognised at fair value plus transaction costs and are subsequently measured at fair value at each reporting date. Fair value gains and losses are recognised in other comprehensive income and are not reclassified to profit or loss upon derecognition. Instead,cumulative gains or losses are transferred directly to retained earnings.

· Dividends from such equity investments are recognised in profit or loss when the Group's or the Company's right to receive payment is established, provided the dividends represent a return on investment and not a recovery of part of the cost of the investment. Impairment losses and reversals of impairment are not recognised separately for equity instruments measured at fair value through OCI.

Financial assets at fair value through profit or loss

· Financial assets are classified at fair value through profit or loss ("FVTPL") if they do not meet the criteria for classification at amortised cost or at fair value through OCI, or if they are held for trading. Financial assets may also be designated at FVTPL upon initial recognition if doing so eliminates or significantly reduces an accounting mismatch.

· Financial assets at FVTPL are initially recognised at fair value, with transaction costs recognised immediately in profit or loss. Subsequently, these financial assets are measured at fair value at each reporting date, with all gains or losses arising from changes in fair value recognised in profit or loss. This includes interest income, dividend income, and fair value movements.

Financial assets at amortised cost are subsequently measured using the effective interest rate ("EIR") method and are subject to impairment. Interest received is recognised as part of finance income in the statement of profit or loss and other comprehensive income. Gains and losses are recognised in profit or loss when the asset is derecognised, modified or impaired. The Group's and Company's financial assets at amortised cost include trade and other receivables (not subject to provisional pricing) and cash and cash equivalents.

Derecognition

A financial asset is primarily derecognised when:

• the rights to receive cash flows from the asset have expired; or

• the Group and Company have transferred their rights to receive cash flows from the asset or has assumed an obligation to pay the received cash flows in full without material delay to a third party under a 'pass-through' arrangement; and either (a) the Group and Company have transferred substantially all the risks and rewards of the asset, or (b) the Group and Company have neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset.

Impairment of financial assets

The Group and Company recognise an allowance for expected credit losses ("ECLs") for all debt instruments not held at fair value through profit or loss. ECLs are based on the difference between the contractual cash flows due in accordance with the contract and all the cash flows that the Group and Company expect to receive, discounted at an approximation of the original EIR. The expected cash flows will include cash flows from the sale of collateral held or other credit enhancements that are integral to the contractual terms.

Financial liabilities

Financial liabilities are classified, at initial recognition, as financial liabilities at fair value through profit or loss, loans and borrowings, payables, or as derivatives designated as hedging instruments in an effective hedge, as appropriate. All financial liabilities are recognised initially at fair value and, in the case of loans and borrowings and payables, net of directly attributable transaction costs.

Subsequent measurement

After initial recognition, trade and other payables are subsequently measured at amortised cost using the EIR method. Gains and losses are recognised in the statement of profit or loss and other comprehensive income when the liabilities are derecognised, as well as through the EIR amortisation process. Financial liabilities at fair value through profit or loss include contingent liability. Gains or losses are recognised in the consolidated income statement.

Derecognition

A financial liability is derecognised when the associated obligation is discharged or cancelled or expires.

Cash and cash equivalents

The Company considers any cash on short-term deposits and other short-term investments to be cash and cash equivalents.

Share capital

The Company's Ordinary shares of nominal value £0.01 each ("Ordinary Shares") are recorded at such nominal value and proceeds received in excess of the nominal value of Ordinary Shares issued, if any, are accounted for as share premium. Both share capital and share premium are classified as equity. Costs incurred directly to the issue of Ordinary Shares are accounted for as a deduction from share premium, otherwise they are charged to the income statement.

Current and deferred income tax

Tax represents income tax and deferred tax. Income tax is based on profit or loss for the year. Taxable profit or loss differs from the loss for the year as reported in the Consolidated Statement of Comprehensive Income because it excludes items of income or expense that are taxable or deductible in other years and it further excludes items of income or expense that are never taxable or deductible. The liability for current tax is calculated using tax rates that have been enacted or substantively enacted by the Statement of Financial Position date.

Deferred tax is the tax expected to be payable or recoverable on differences between the carrying amounts of assets and liabilities in the Historical Financial Information and the corresponding tax bases used in the computation of taxable profit, and is accounted for using the liability method. Deferred tax liabilities are generally recognised for all taxable temporary differences and deferred tax assets are recognised to the extent that it is probable that taxable profits will be available against which deductible temporary differences can be utilised.

Deferred tax assets and liabilities are offset where there is a legally enforceable right to set off current tax assets against current tax liabilities and when they relate to income taxes levied by the same taxation authority and the intention is to settle current tax assets and liabilities on a net basis.

Share based payments

The fair value of services received in exchange for the grant of share warrants and options is recognised as an expense in share premium or profit or loss, in accordance with the nature of the service provided. A corresponding increase is recognised in equity.

The total expense to be apportioned over the vesting period of the benefit is determined by reference to the fair value (excluding the effect of non market-based vesting conditions) at the date of grant. Fair value is measured by the use of the Black-Scholes model. The expected life used in the model has been adjusted, based on management's best estimate, for the effects of the non- transferability, exercise restrictions and behavioural considerations. A cancellation of a share award by the Group is treated consistently, resulting in an acceleration of the remaining charge within the consolidated income statement in the year of cancellation.

Judgements and key sources of estimation uncertainty

The preparation of the Financial Statements in conformity with IFRS requires the directors to make judgements, estimates and assumptions that affect the amounts reported. These estimates and judgements are continually reviewed and are based on experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances.

Recoverability of exploration and evaluation assets

Exploration and evaluation costs have a carrying value at 31 December 2025 of £2,329,659(2024: £4,259,271). Such assets have an indefinite useful life as the Group has a right to renew exploration licences and the asset is only amortised once extraction of the resource commences. Management tests for impairment annually whether exploration projects have future economic value in accordance with the accounting policy stated in Note 2. Each exploration project is subject to an annual review to determine if the exploration results during the period warrant further exploration expenditure and have the potential to result in an economic discovery. This review takes into consideration long term prices, anticipated resource volumes and supply and demand outlook. In the event that a project does not represent an economic exploration target and results indicate there is no additional upside, a decision will be made to discontinue exploration; an impairment charge will then be recognised in the statement of comprehensive income.

On the 30 June 2025 Cobra entered into a binding agreement to sell the Wudinna Gold rights to Barton Gold Holdings Limited while retaining exposure to future upside through equity, milestone payments, production-linked cash payments, and retained mineral rights. The transaction converts a non-core gold asset into funding capacity and optionality, while allowing Cobra to continue focusing on rare earths.

The guaranteed fixed consideration payable under the transaction comprises up to $5.5 million(£2,735,150), consisting of $500,000(£248,650) in cash and $5.0 million(£2,486,500) in Barton Gold Holdings Limited shares. The cash component includes a $50,000(£24,865) non‑refundable deposit and $150,000(£74,595) post transfer of tenements both have been received, with the balance payable through to final settlement. The equity consideration will be issued progressively upon the grant of the relevant tenements and at final settlement, with the number of shares calculated using Barton's volume‑weighted average share price (VWAP) prior to each issue. The Barton shares issued under the transaction will be subject to escrow restrictions, with 40% escrowed for 12 months and the remaining 60% escrowed for 24 months from their respective issue dates.

Tranche 1 (received): A$50,000(£24,865) non-refundable deposit + A$150,000(£74,595) on Completion/transfer + A$800,000(£397,840)( in Barton Gold shares issued on Completion.

Tranche 2 (receivable): A$300,000(£149,190) cash + A$4.2 million(£2,088,660) iBarton Gold shares payable at Final Settlement

As a result of the exploration results received to date, budget for further exploration works and licences being in good standing, Management do not consider that the exploration and evaluation assets are impaired as at 31 December 2025 and 2024. .

Share-based payments valuations

Accounting estimates and assumptions are made concerning the future and, by their nature, may not accurately reflect the related actual outcome. Share options and warrants are measured at fair value at the date of grant. The fair value is calculated using the Black Scholes method for both options and warrants as the management views the Black Scholes method as providing the most reliable measure of valuation.

Contingent Consideration

Contingent consideration, resulting from business combinations, is valued at fair value at the acquisition date as part of the business combination. The determination of fair value is based on key assumptions involving estimation of the probability of meeting each performance target and the timing thereof which are judgement based decisions made by Management. As part of the acquisition of Lady Alice Mines Pty Ltd, contingent consideration with an estimated fair value of £296,536 was recognised at the acquisition date. See note 23 for further details. The Group is required to remeasure the contingent liability at fair value at each reporting date with changes in fair value recognised through profit or loss in accordance with IFRS 9.

Refer to note 14 for commentary on judgements made in relation to the 2025 balance.

Recoverable value of investment in subsidiary and intercompany debtors

As at 31 December 2025, the Company recognised an investment in subsidiary of £562,260 (2024: £562,260), and loans to the subsidiary of £6,400,144 (2024: £4,874,714). Significant judgement is applied in assessing the recoverability of these balances.

The investment in subsidiary is assessed for impairment in accordance with IAS 36. The key judgement relates to whether indicators of impairment exist, which depends primarily on the likelihood of successfully realising value from the subsidiary's exploration and evaluation assets.

The loans to the subsidiary are financial assets within the scope of IFRS 9, and management is required to assess expected credit losses. This assessment involves determining whether the loans are credit‑impaired or whether there has been a significant increase in credit risk. Due to the exploration‑stage nature of the subsidiary's activities, the amount and timing of future cash flows cannot be reliably estimated at this stage. Management therefore places reliance on the impairment assessment of the underlying exploration assets, the results of exploration activities to date, the planned programme of work, and the licences being in good standing.

Based on these factors, management has concluded that there are no indicators of impairment of the investment and that the loans are not credit‑impaired. Accordingly, no impairment charge or expected credit loss provision has been recognised. The directors expect both the investment and the loans to be recovered in full.

This judgement is subject to significant uncertainty. Changes in exploration outcomes, future funding requirements, commodity prices, or licence status could result in a material reassessment of recoverability in future periods.

2. INCOME & EXPENSES BY NATURE

|

|

|

31 December |

31 December |

|

|

|

2025 |

2024 |

|

|

|

£ |

£ |

|

VAT receivable |

|

- |

61,422 |

|

Option fee received |

|

- |

29,845 |

|

|

|

|

|

|

Other Income |

|

- |

91,267 |

|

Administrative expense |

|

390,073 |

113,489 |

|

Corporate expense and Finance |

|

392,357 |

258,837 |

|

Wages & Salaries expense |

|

346,408 |

192,972 |

|

Total Expenses |

|

1,128,838 |

565,298 |

Auditor's remuneration

|

|

31 December |

31 December |

|

|

2025 |

2024 |

|

|

£ |

£ |

|

|

|

|

|

Fees payable to the Group's auditor for the audit of the Group's annual accounts |

41,500 |

37,500 |

|

|

41,500 |

37,500 |

3. FINANCE INCOME

|

|

|

31 December |

31 December |

|

|

|

2025 |

2024 |

|

|

|

£ |

£ |

|

|

|

|

|

|

Interest income |

|

13,606 |

7,611 |

|

Finance costs |

|

(92) |

(442) |

|

Net finance income |

|

13,514 |

7,169 |

4. SEGMENT INFORMATION

The Group's prime business segment is mineral exploration.

The Group operates within two geographical segments, the United Kingdom and Australia. The UK sector consists of the parent company which provides administrative and management services to the subsidiary undertaking based in Australia.

The following tables present expenditure and certain asset information regarding the Group's geographical segments for the years ended 31 December 2025 and 2024:

|

Operational Results |

|

31 December 2025 £ |

|

31 December 2024 £ |

|

Profit/(Loss) after taxation |

|

|

|

|

|

- United Kingdom |

|

624,786 |

|

(302,847) |

|

- Australia |

|

(804,980) |

|

(120,489) |

|

Total |

|

179,889 |

|

(423,336) |

|

2025 |

|

Australia £ |

|

United Kingdom £ |

|

Total £ |

|

Non-current assets |

|

5,623,478 |

|

280,613 |

|

5,904,091 |

|

Current assets |

|

970,751 |

|

1,474,329 |

|

2,445,079 |

|

Total liabilities |

|

(134,309) |

|

(202,703) |

|

(337,012) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2024 |

|

Australia £ |

|

United Kingdom £ |

|

Total £ |

|

Non-current assets |

|

4,042,087 |

|

315,702 |

|

4,357,789 |

|

Current assets |

|

1,739 |

|

938,715 |

|

940,454 |

|

Total liabilities |

|

(103,932) |

|

(186,867) |

|

(290,799) |

|

|

|

|

|

|

|

|

5. DIRECTORS' EMOLUMENTS

There were no employees during the period apart from the directors, who are the key management personnel. No directors had benefits accruing under money purchase pension schemes.

|

Year ended 31 December 2025 |

Salaries £ |

Fees £ |

Other £ |

Share Based payment charge £ |

Total £ |

|

G Hancock* |

- |

34,000 |

- |

8,929 |

42,929 |

|

R Verco |

150,000 |

- |

80,000** |

11,000 |

241,000 |

|

D Maling |

- |

24,000 |

- |

8,142 |

32,142 |

|

D Clarke |

- |

50,000 |

- |

8,929 |

58,929 |

|

|

150,000 |

108,000 |

80,000 |

37,000 |

375,000 |

*Mr Hancock resigned as a director of the Company post reporting date on 13 April 2026

**Relates to historical KPI bonuses in line with Managing Director contract, approved in 2025.

· During the year £34,000 (2024: £33,650) was paid to Hancock Corporate Investments Pty Ltd, a company in which Greg Hancock is a Director, in respect of Directors fees and consultancy services.

· During the year £24,000 (2024: £24,000) was paid to Dan Maling, in respect of Directors fees.

· During the year £50,000 (2024: £50,000) was paid to The Springton Trust & Queens Road Mines, in which David Clarke is a Trustee, in respect of Directors fees and consultancy services.

Rupert Verco was the highest paid Director for the year who received remuneration of £230,000.

|

Year ended 31 December 2024 |

Salaries £ |

Fees £ |

Other £ |

Share Based payment charge £ |

Total £ |

|

G Hancock |

- |

33,650 |

- |

8,143 |

41,793 |

|

R Verco |

148,675 |

- |

- |

6,000 |

154,675 |

|

D Maling |

- |

24,000 |

- |

8,714 |

32,714 |

|

D Clarke |

- |

50,000 |

- |

8,143 |

58,143 |

|

|

148,675 |

107,650 |

- |

31,000 |

287,325 |

· During the year £33,650 (2023: £31,166) was paid to Hancock Corporate Investments Pty Ltd, a company in which Greg Hancock is a Director, in respect of Directors fees and consultancy services.

· During the year £24,000 (2023: £24,000) was paid to Dan Maling, in respect of Directors fees.

· During the year £50,000 (2023: £24,000) was paid to The Springton Trust & Queens Road Mines, in which David Clarke is a Trustee, in respect of Directors fees and consultancy services.

Rupert Verco was the highest paid Director for the year who received remuneration of £148,675.

6. INCOME TAXES

a) Analysis of tax in the period

|

|

31 December |

31 December |

|

|

|

2025 |

2024 |

|

|

|

£ |

£ |

|

|

Current tax |

- |

- |

|

|

Deferred taxation |

- |

- |

|

|

|

- |

- |

|

b) Factors affecting tax charge or credit for the period

The tax assessed on the loss on ordinary activities for the period differs from the standard rate of corporation tax in the UK of 25% (2024: 19%) and Australia of 25% (2024: 25%). The differences are explained below:

|

|

31 December |

31 December |

|

|

2025 |

2024 |

|

|

£ |

£ |

|

Profit/(Loss) on ordinary activities before tax |

179,889 |

(423,336) |

|

|

|

|

|