MCB DFS confirms stronger economics

Summary by AI BETAClose X

ASX/AIM RELEASE

23 January 2026

MCB Definitive Feasibility Study confirms stronger economics

HIGHLIGHTS:

· The Definitive Feasibility Study (DFS) confirms a technically and economically robust Maalinao-Caigutan-Biyog (MCB Project).

· Pre-tax NPV(8%) of US$1.3 billion (~A$1.98 billion) at an IRR of 31% and Post-tax NPV (8%) of US$ 771 million (≈ AU$1.15 billion) at an IRR of 24% - based on long range conservative copper and gold prices of $4.30/lb Cu and US$3,000/oz Au for first nine years then $7.0 USD/lb Cu and $4,500 USD/oz Au for the succeeding years.

· At current spot price of US$6.00/lb Cu and US$4500/oz Au, the Pre-tax NPV(8%) increases to US$1.9 billion (~AU$2.9 billion) - IRR 42% Post-tax NPV(8%) US$1.2 billion (≈ AU$1.8 billion) - IRR 34%.

· Large-scale, high-quality resource base, with a JORC (2012) compliant Mineral Resource of 343 Mt and a Maiden Ore Reserve of 130.2 Mt, underpinning a 35-year mine life.

· Early high-grade production profile, with mining of a high-grade core during the first 10 years and an average C1 cash cost (net of by-product credits) of US$0.41/lb Cu driving strong early cash flow and EBITDA of ~US$230 million per annum in Years 1-10.

· Established and scalable mining strategy, utilising sublevel open stoping ("SLOS") with paste backfill, decline access transitioning to a shaft and hoisting system, supporting efficient long-term operations and the company's strong ESG Goals.

· Identified growth optionality, including potential throughput expansion to approx.3.0 Mt/y, staged surface material recovery, and resource upside at depth, which is not yet included in the base-case valuation.

___________________________________________________________________________

Celsius Resources Limited ("Celsius" or the" Company") (ASX, AIM: CLA) is pleased to announce the results of the Definitive Feasibility Study ("DFS") for the Maalinao-Caigutan-Biyog Copper-Gold Project ("Project" or "MCB") which is held under its Philippine affiliate Company, Makilala Mining Company., Inc. ("MMCI"). The MCB Project is owned and operated by MMCI and Celsius has 40% working interest in MCB as Celsius conditionally agreed to transfer a 60% working interest in the MCB Project to Sodor, Inc, subject to certain conditions, which remain outstanding, as announced on 20 March 2023.

Celsius has reported, in accordance with the JORC Code (2012), a JORC-compliant Mineral Resource totaling 343 Mt at 0.46% Cu and 0.12 g/t Au, containing approximately 1.6 Mt of copper and 1.4 Moz of gold, and a Maiden Ore Reserve of 130.2 Mt at 0.66% Cu and 0.21 g/t Au, containing approximately 856 kt of copper and 891 koz of gold. The Ore Reserve comprises 22.1 Mt of Proven Reserves and 108.2 Mt of Probable Reserves and underpins the long-term development plan for the Project[1].

The DFS follows a scoping study announced in December 2021 and has been prepared with a focus on optimising the underground mine plan, advancing the process plant design, refining surface and underground infrastructure layouts, and developing tender-ready early work packages. The selected mining method is sub-level open stoping, reflecting the geometry and continuity of the mineralisation and prevailing geotechnical conditions. Ore will be processed through a conventional crushing, grinding and flotation concentrator, producing a high-quality copper-gold concentrate.

The DFS also sought to identify cost efficiencies across mining, processing, tailings management, power supply and associated infrastructure. In parallel, additional geotechnical and hydrogeological investigations were undertaken to refine design inputs, reduce technical uncertainty, and support the Project's development pathway in compliance with the JORC Code (2012).

This announcement reflects the work undertaken by Ausenco[2] (Lead Engineer, Process plant and surface infrastructure capital and operating costs), DMT Consulting Limited[3] (Mining), MMCI, and their respective contractors and consultants, as described and referenced throughout this release. It has been prepared for the information of stakeholders and the broader investment community, both domestic and international, and to support ongoing engagement with existing and prospective investors.

An executive summary of the detailed DFS has been made available online, and is accessible at: https://celsiusresources.com/announcements .

Celsius Executive Director, Neil Grimes said:

"The MCB Definitive Feasibility Study marks a significant milestone, positioning the MCB Project as a leading near-term copper-gold development opportunity in the Philippines. The Study demonstrates a technically robust and economically enhanced project, with competitive capital intensity and operating costs. The Company is progressing funding and offtake discussions to advance the Project toward a Final Investment Decision and construction."

The table below summarises the key physical and financial outcomes of the DFS, which has been completed to a Class 3 level of estimate accuracy (typically up to ±15%), consistent with industry standards and suitable for project financing and execution planning. The outcomes are derived from engineering and cost estimates developed predominantly on a first-principles basis, supported by defined mine plans, process plant design, infrastructure layouts, execution methodology and contractor benchmark inputs.

The table also highlights the economic significance of mining the high-grade core zone during the initial 10 years of operation, which underpins the Project's early cash flow profile and overall economic robustness. Key technical and economic highlights are summarised as follows:

· Pre-tax NPV(8%) of US$1.3 billion (~A$1.98 billion) and an IRR of 31% and Post-tax NPV (8%) of US$ 771 Million (≈ A$1.15 billion) and an IRR of 24%, assuming copper and gold prices of US$4.30/lb Cu and US$3000/oz Au for first nine years then US$7.0 /lb Cu and US$4500/oz Au for the succeeding years.

· At current spot price of US$6.00/lb Cu and US$4500/oz Au, the Pre-tax NPV(8%) increases to US$1.9 billion (~AU$2.9 billion) - IRR 42% Post-tax NPV(8%) US$1.2 billion (≈ A$1.8 billion) - IRR 34%.

· C1 Cash Cost during the first 10 years average US$0.41/lb Cu and LOM average of US$1.73/lb Cu, net of credits.

· CAPEX of US$276 Million which includes US$ 26.5 Million in contingency and US$15.1 Million in growth. This assumes a payback period of 4.7 years from start of production.

Table 1. Summary of Key Technical and Financial Outcomes

|

ITEM |

PREFERRED CASE FIRST 10 YEARS |

PREFERRED CASE LIFE OF MINE |

|

Ore Mined |

24.5 MT |

89.7 MT |

|

Copper Grade |

1.08% |

0.69% |

|

Gold Grade |

0.51 g/t |

0.24 g/t |

|

Copper Recovery |

92.5% |

89.7% |

|

Gold Recovery |

79.7% |

72.6% |

|

Mine Life |

10 Years |

35.3 Years |

|

Process Plant Throughput |

2.64 MTPA |

2.64 MTPA |

|

Average Annual Cu concentrate production (dry) |

102.5 kt |

66.0 kt |

|

Total Copper Recovered |

542 Mlbs |

1234 Mlbs |

|

Total Gold Recovered |

319 koz |

507 koz |

|

Copper Price for first 9 Years (assumed) |

US$4.3/lb |

US$4.3/lb |

|

Copper Price for remaining years |

US$7.0 /lb |

US$7.0 /lb |

|

Gold Price For First 9 Years (assumed) |

US$3,000 /oz |

US$3,000 /oz |

|

Gold Price for remaining years |

US$4,500 /oz |

US$4,500 /oz |

|

Initial Capital |

US$276 M |

US$276 M |

|

NPV (Post tax;8%) |

US$444 M |

US$771 M |

|

NPV (Pre Tax;8%) |

US$771M |

US$1.3 B |

|

IRR (Pre-Tax) |

28.5% |

30.50% |

|

IRR (Post Tax) |

22.1% |

24.10% |

|

Payback from start of production |

4.7 Years |

4.7 Years |

|

LOM C1 Cost |

US$0.41 /lb Cu |

US$1.73 /lb Cu |

MMCI Chief Operations Officer Patrique Jane Duran said:

"The completion of the DFS represents a major milestone and value inflection point for the MCB Copper-Gold Project, confirming it as a long-life, technically robust and finance-ready underground operation with strong economics and a clear development plan. The DFS validates more than a decade of technical work and provides a solid foundation for funding execution, and long-term value creation.

Importantly, the DFS demonstrates a competitive cost structure, strong margins, and early cash flow, from the substantial Ore Reserve and a disciplined, risk-managed development strategy. Project optimisation prioritises operational efficiency and delivery certainty in the early years, while reducing the overall environmental footprint and preserving flexibility as infrastructure is established and the operation matures, thereby supporting both cost performance and environmental outcomes.

With the DFS now complete, the Company is focused on advancing funding discussions, finalising execution planning and progressing toward a Final Investment Decision. Management believes the MCB Project is well positioned to deliver sustainable shareholder returns and to become a significant new copper-gold producer in the Philippines, aligned with responsible mining and ESG principles."

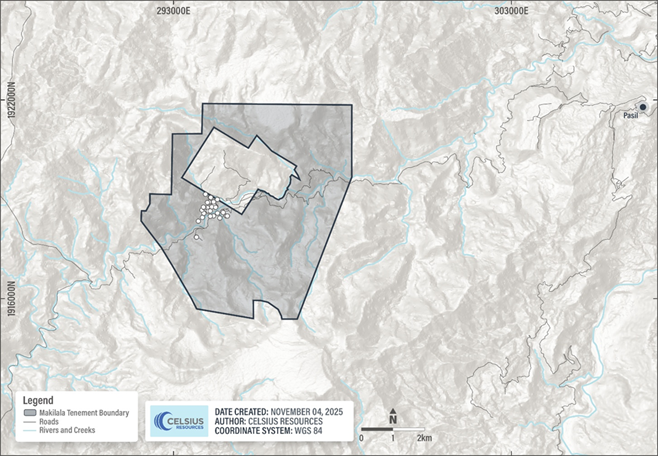

MCB Copper-Gold Project Location

The MCB Project covers an area of 2500 Ha in the Cordillera Administrative Region in the Philippines, approximately 320km north of Manila. The MCB Project is located in Barangay Balatoc, Municipality of Pasil, Province of Kalinga. The Project area settlements are generally small, compact and occupy a limited area within the main Barangay of Balatoc. The closest major centre is the city of Tabuk which is approximately a 3-hour drive from the Project location. (Figure 1).

The Mines and Geosciences Bureau ("MGB") issued the Mineral Production Sharing Agreement ("MPSA") (MPSA-356-2024-CAR) to MMCI on 15 March 2024. The mining permit covers an initial mine life of 25 years with the option for renewal for a further 25years[4].

Figure 1. Location of MCB Exploration Tenement area and associated drilling related to the reported MRE.

Geology and Mineral Resource Estimate ("MRE")

The MCB Project hosts a large-scale porphyry copper-gold deposit. The MRE, announced on 24 November 2025, is based on geological interpretation, surface mapping and 60 diamond drill holes totaling 31,616.2 m completed by MMCI between 2006 and 2025.

Mineralisation is associated with a tonalite intrusive and its contact with surrounding mafic volcanic host rocks and is controlled by a dominant north-east (~050°), near-vertical structural fabric. Mineralized domains have been defined based on continuous copper-gold mineralisation aligned with geological, structural and alteration controls. While minor epithermal-style mineralisation occurs locally, the MRE is defined solely on a porphyry copper-gold deposit model.

At depth, the system extends for up to 1 km along strike with true widths of up to 280 m, while at shallower levels mineralisation is developed within multiple overlapping domains of up to 600 m strike length and 150 m true width.

The MRE has been reported at a 0.20% copper cut-off grade and classified as Measured, Indicated and Inferred in accordance with the JORC Code (2012), based on drill spacing, sample density and geological confidence.

Table 2. Summary results for the updated MRE at MCB at a cut-off grade of 0.20% copper[5].

|

|

Gross |

Net Attributable |

|||||||

|

Classification |

Domain |

Tonnes (Mt) |

Copper Grade (%) |

Gold Grade (g/t) |

Copper Metal (kt) |

Gold Metal (koz) |

Tonnes (Mt) |

Copper Metal (kt) |

Gold Metal (koz) |

|

Measured |

Type 1HGV |

13 |

1.15 |

0.50 |

145 |

202 |

5 |

58 |

81 |

|

Type 1HGH |

4 |

0.72 |

0.10 |

32 |

14 |

2 |

13 |

6 |

|

|

Type 3LG |

32 |

0.37 |

0.08 |

119 |

84 |

13 |

48 |

34 |

|

|

Totals |

49 |

0.60 |

0.19 |

296 |

300 |

20 |

118 |

120 |

|

|

Indicated |

Type 1HGV |

48 |

0.66 |

0.28 |

316 |

433 |

19 |

126 |

173 |

|

Type 1HGH |

11 |

0.79 |

0.12 |

83 |

41 |

4 |

33 |

16 |

|

|

Type 3LG |

190 |

0.35 |

0.07 |

674 |

438 |

76 |

270 |

175 |

|

|

Totals |

248 |

0.43 |

0.11 |

1,072 |

913 |

99 |

429 |

365 |

|

|

Inferred |

Type 1HGV |

19 |

0.50 |

0.12 |

94 |

72 |

8 |

38 |

29 |

|

Type 1HGH |

0.1 |

0.80 |

0.14 |

0.5 |

0.3 |

0 |

0 |

0 |

|

|

Type 3LG |

26 |

0.49 |

0.08 |

129 |

71 |

10 |

52 |

28 |

|

|

Totals |

45 |

0.49 |

0.10 |

224 |

143 |

18 |

90 |

57 |

|

|

Total |

Type 1HGV |

79 |

0.70 |

0.28 |

554 |

708 |

32 |

222 |

283 |

|

Type 1HGH |

15 |

0.77 |

0.11 |

115 |

55 |

6 |

46 |

22 |

|

|

Type 3LG |

248 |

0.37 |

0.07 |

922 |

593 |

99 |

369 |

237 |

|

|

Totals |

343 |

0.46 |

0.12 |

1,592 |

1,356 |

137 |

637 |

542 |

|

Note for table of results: Estimates have been rounded to the nearest Mt of ore, two significant figures for Cu and Au grade and to the nearest kt of Cu metal and koz of Au metal. Some apparent errors may occur due to rounding. The MCB Project is an affiliate company of Celsius and MMCI will be the operator of the MCB Project.

Mining Summary

The MCB Project is a long-life underground copper-gold operation with a current mine life of 35 years, based on the recently announced JORC Code (2012) compliant Ore Reserve[6] (see Table 3).

Table 3. MCB Project Ore Reserve Estimates.

|

|

Gross |

Net Attributable |

|||||||

|

Tonnes |

Copper Grade (%) |

Gold Grade (g/t) |

Copper Equivalent Grade (%) |

Contained Cu (t) |

Contained Au (oz) |

Tonnes |

Copper Metal (t)

|

Gold Metal (oz) |

|

|

Proven |

22,074,084 |

0.90 |

0.34 |

1.19 |

197,563 |

244,136 |

8,829,634 |

79,025 |

97,654 |

|

Probable |

108,198,583 |

0.61 |

0.19 |

0.77 |

658,929 |

647,031 |

43,279,433 |

263,572 |

258,812 |

|

Total |

130,272,667 |

0.66 |

0.21 |

0.84 |

856,492 |

891,167 |

52,109,067 |

342,597 |

356,467 |

Note for table of results: Estimates have been rounded to two significant figures for Cu and Au grade. Some apparent errors may occur due to rounding. The MCB Project is an affiliate company of Celsius and MMCI will be the operator of the MCB Project.

The optimised 35-year mine plan schedules 90.0 Mt of Ore Reserve for extraction. The remaining 40.3 Mt of Ore Reserve has been sterilised under the current plan due to social boundary constraints, including areas located beneath nearby communities and surface infrastructure where underground access is currently limited.

Recovering this material would require significant additional underground development which, under current assumptions, would reduce the project's Net Present Value ("NPV").

This material remains part of the declared Ore Reserve and may provide future value. Its potential extraction will be considered in later phases of the operation, subject to mine plan optimisation, community engagement, and confirmation of development access.

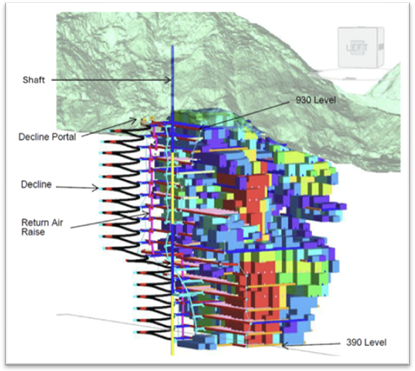

Mining will be undertaken using transverse SLOS with cemented paste backfill, a method well suited to the orebody geometry and favourable geotechnical conditions. Initial access and early production are established via a decline with truck haulage during the first three years, followed by commissioning of a vertical shaft and hoisting system that becomes the primary material handling system as the mine deepens to improve haulage efficiency, reduce operating costs, and support higher production rates over the long term (refer Figure 2. Underground Mine Design). The access strategy balances early cash flow with long‑term operational efficiency and reduced material handling distances.

Figure 2. Image of stoping and decline development.

The base-case mining profile ramps up to approximately 2.28 Mt/y, increases to ~2.65 Mt/y for the majority of the mine life, and provides flexibility to support a potential increase to ~3.0 Mt/y from around Year 10, leveraging fully developed infrastructure to offset grade decline and sustain metal production. Geotechnical and hydrogeological conditions are considered manageable for long-term operations, and the Mineral Resource remains open at depth, providing clear potential for future resource growth and mine life extension.

Metallurgy and Process Plant Summary

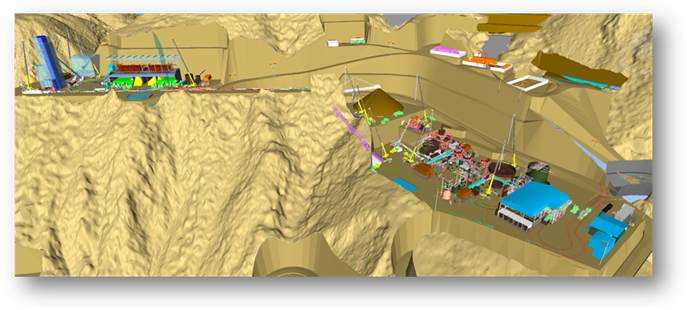

Metallurgical testwork undertaken by MMCI across multiple ore types and representative grade ranges confirms supports forecast average recoveries of approximately 92.5% for copper and 79.7% for gold for years 1-10 into a saleable copper-gold concentrate[7]. The process plant is designed to treat underground run-of-mine sulphide ore at 2.28 Mt/y during Years 1-2, increasing to ~2.65 Mt/y from Year 3 onward, with variability testwork indicating that blending in the mine is required and planned for, and additional limited capital may be required to manage locally harder basaltic ore. Ore mined by transverse SLOS is delivered to surface via the shaft and winder system (via truck haulage in Year 1-3) and processed through a conventional flowsheet comprising SSAG milling, rougher flotation, regrind, cleaner flotation and concentrate dewatering. Tailings are either returned underground as paste backfill or placed in a dry-stack area after Tailings filtration, supporting efficient and environmentally responsible operation.

Figure 3: Process plant, paste backfill plant and shaft/winder system supporting underground ore delivery.

Non- Process Infrastructure

The non-process infrastructure ("NPI") for the MCB Copper-Gold Project has been defined in accordance with JORC Code (2012) to support safe, reliable and efficient construction and operations over the full life of the Project. NPI comprises all facilities, utilities and services required for mine and plant activities other than ore processing, including a consolidated site layout, administration and accommodation facilities, medical facilities, workshops, warehousing, laboratories, mine surface installations, and essential utilities such as power distribution, water supply, wastewater treatment, fuel storage and communications. Supporting infrastructure also includes site access and grid power connection arrangements designed to meet operational, safety and regulatory requirements. Logistics and concentrate export infrastructure, including transport corridors and off-site handling facilities, is incorporated into the Project execution plan to ensure reliable year-round product shipment. All NPI elements have been sized based on the defined construction and steady-state workforce, ensuring infrastructure is appropriately scaled to support operations throughout the life of the Project.

Capital Cost Estimate

The capital cost estimate for the Project, excluding provisions for growth and contingency is USD 234.5 million. A growth provision of USD 15.1 million was added to the base estimate, in accordance with Ausenco's internal benchmarks and guidelines. A contingency provision of USD 26.5 million, equivalent to 11.3% of the base estimate, was added based on the P50 estimate derived from a Monte Carlo assessment to account for estimating and project-specific risks.

The capital cost estimate for the Project inclusive of growth and contingency is USD 276 million.

Table 4. Capital Cost Summary.

|

Key Areas |

Value Exc. Growth USD M |

Growth USD M |

Total Inc. Growth USD M |

|

Mining |

30.8 |

0.7 |

31.5 |

|

Process Plant |

74.0 |

7.2 |

81.2 |

|

Tailings Filtration & Handling |

29.9 |

2.6 |

32.5 |

|

On Site Infrastructure |

45.1 |

4.5 |

49.6 |

|

Off Site Infrastructure |

20.7 |

0.0 |

20.7 |

|

Project Preliminaries |

10.0 |

0.0 |

10.0 |

|

Project Delivery |

10.3 |

0.0 |

10.3 |

|

Owner's Costs |

13.7 |

0.0 |

13.7 |

|

Sub-Total Excluding Contingency |

234.5 |

15.1 |

249.5 |

|

Contingency |

26.5 |

0.0 |

26.5 |

|

Total |

261.0 |

15.1 |

276.1 |

Operating Cost Estimate

A summary of the average annual LOM operating costs is shown in Table 5 below.

Table 5: Operating Cost Summary and Cost Metrics.

|

Item |

USD M/Year |

USD/t (mined) |

|

Mining |

48.8 |

18.9 |

|

Process |

42.4 |

16.4 |

|

General and Administrative |

4.9 |

1.9 |

|

Total OPEX |

96.1 |

37.1 |

Operating cost estimates for the MCB Project were prepared by Ausenco on behalf of MMCI, incorporating mining costs developed by DMT with owner's general and administration costs (G&A), power and fuel pricing provided by MMCI. The estimates have been developed to a Class 3 accuracy (±15%).

Mining, reagents, paste backfill binder, and dry-stack tailings operating and sustaining capital costs have all been derived on a first-principles basis, using defined mine plans, testwork-based consumption rates, quoted material prices, contractor rates and fuel consumption.

Economic Evaluation

Strong project economics, delivering a post-tax NPV (8%) of US$771 million and a post-tax IRR of 24.1%, with payback of 4.7 years from the commencement of operations.

Life-of-mine revenue of ~US$8.95 billion, with approximately 79% derived from payable copper and the balance from gold credits, supporting margin stability.

Robust cash generation, with LOM EBITDA of ~US$5.1 Billion, averaging ~US$144.6 Million per annum, and ~US$230 Million per annum during the first 10 years of production, reflecting early mining of higher-grade ore.

Cash cost (C1) during the first 10 years average US$0.41/lb Cu and LOM average of US$1.73/lb Cu, net of credits. While the life-of-mine all-in sustaining costs ("AISC") of ~US$1.91/lb Cu after gold credits. AISC represents the total cost of producing copper, including mining, processing, site G&A, sustaining capital, royalties, transport and refining, providing a comprehensive measure of operating margin and cost competitiveness.

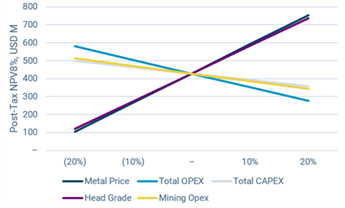

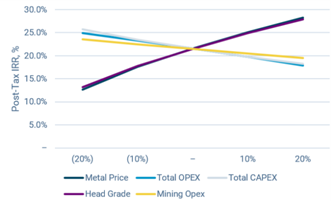

Resilient economics, with sensitivity analysis indicating the Project is most sensitive to metal prices and head grade, and comparatively less sensitive to operating and capital cost variations.

|

|

|

Figure 4: NPV Sensitivity Analysis of Key Assumptions. Figure 5: IRR Sensitivity Analysis of Key Assumptions.

The preferred case used an 8% real discount rate. Sensitivity to the discount rate is shown on the table below:

Table 6: Pre-Tax and Post Tax Net Present Value results under different discount rates.

|

Discount Rate |

8% |

10% |

12% |

|

Post Tax NPV, M USD |

772 |

568 |

416 |

|

Pre Tax NPV, M USD |

1,323 |

1,005 |

768 |

Schedule Summary

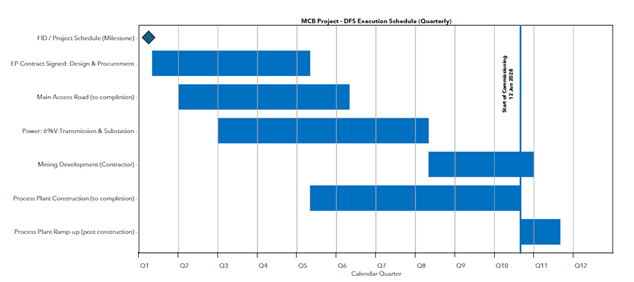

The MCB Project is supported by a fully integrated engineering, procurement and construction execution schedule, defining the development pathway from Final Investment Decision ("FID") targeted for Q1 2026 through to commissioning and first concentrate expected in Q2 and Q3 2028, respectively. Early works and detailed engineering commence immediately post-FID, with process plant construction scheduled to start in Q1 2027 and progressive handover to commissioning from Q2 2028, supporting an orderly start-up and ramp-up to steady-state operations.

Figure 6: MCB Project DFS Execution Schedule (Quarterly).

Opportunities

In addition to the robust base case defined in the DFS, the MCB Project presents a number of identified, non-base-case opportunities that have the potential to enhance production flexibility, sustain output and improve overall Project value. These opportunities are incremental in nature, leverage existing or planned infrastructure, and are not included in the current mine plan or financial model, but provide optionality that may be evaluated and progressed as the Project advances.

Surface Material Optionality

The current mine plan is underground-focused, and near-surface mineralisation was not considered in the original mine planning. Weathered surface material exposed during slope stabilisation and infrastructure works (particularly road works) has been identified as a potential incremental mining opportunity and is within the Mineral Resource Estimate and Ore Reserve Estimate but excluded from the base case mine plan and financial model. The material occurs adjacent to internal road alignments and within areas affected by required site development activities and therefore represents an opportunistic recovery option, rather than a change to the core underground mining strategy.

The identified surface material comprises approximately 0.9 Mt at an average grade of 0.64% Cu and 0.11 g/t Au, interpreted as predominantly transition-style mineralisation. Any potential recovery would be staged and discretionary, providing ramp-up support or contingency feed, and would not affect the early years of operation or the base life-of-mine schedule, preserving flexibility while maintaining the robustness of the underground base case.

Potential Production Increase

The current mine plan aligns with the process plant ramp-up, achieving steady-state production of 2.28 Mt/y during the initial operating period of three years, before increasing to 2.64 Mt/y for the majority of the mine life as underground infrastructure is established. In the early years, production rates are constrained by the progressive development of key capital infrastructure, including haulage, ventilation and ore-handling systems. By approximately Year 10, the primary underground infrastructure is fully developed, and operational constraints are materially reduced. As higher-grade stopes are depleting and feed grades declining, the Project presents a clear opportunity to increase ore throughput to sustain concentrate production and enhance project value. Preliminary assessments indicate that, subject to further study, the existing process plant primarily could support an increase to up to ~3.0 Mt/y, leveraging established mine infrastructure and potential concentrator upgrades, while mineralisation remains open at depth, providing additional long-term optionality.

Risk Management

Risk and opportunity management is an integral component of the DFS for the MCB Project and embedded throughout the engineering and planning process. Structured risk assessments and specialist reviews were used to inform mine design, site layout, execution strategy and early works planning, resulting in engineering solutions that reduce risk exposure, improve constructability and schedule confidence, and enhance project value.

A number of risks identified early in the study have been mitigated through design changes incorporated into the DFS, while opportunities relating to mine optimisation, infrastructure staging and operational flexibility have been captured and reflected in the capital estimate. At completion of the DFS, the Project benefits from a clearly defined risk profile and a structured framework for managing residual risks and opportunities, supported by detailed risk registers and analysis.

Study Contributors

Ausenco served as the lead consultant for the DFS, managing and integrating the work undertaken by MMCI and various third-party specialists as detailed in Table 6 below.

Table 7. Definitive Feasibility Study Contributors

|

Primary Contributor |

Scope |

|

Ausenco Services Pty Ltd |

Process plant design, surface infrastructure and earthworks design, capital cost estimation, operating cost estimation, financial model compilation |

|

Makilala Mining Company, Inc. |

Environmental, Social, Permitting, Operations and Owners and Handover planning and General Administration. Financial Model review and taxation, royalties, owners' costs

|

|

DMT Consulting Pty Ltd |

Optimized Underground Mine Design, mine cost estimates, JORC Compliant Ore Reserve Estimate |

|

Brisbane Met Labs |

Metallurgical Test Work |

|

BMECs Pty Ltd., Australia (John Burgess) |

Metallurgy and recovery models, Process plant design inputs and review |

|

Steven Olsen, CP Geology |

JORC Mineral Resource Estimate and Geology |

|

Resource Development Consultants Limited |

Surface geotechnical report, Dry Stacking (tailings) area design, Freshwater Intake Structure Design, GAF Retaining Wall Design |

|

ALS Metallurgy Pty Ltd., Australia |

Metallurgical Test Work (2021 DFS) |

|

DMT Brisbane, Australia |

Paste Plant Technical Report |

|

Metso Outotec |

Thickening and tailings filtration testwork (2021 and 2025 DFS) |

|

Quattro Project Engineering |

Backfill testwork |

Compliance Statements

The Company confirms that it is not aware of any new information or data that relates to previously reported Exploration Results, Ore Reserves and Mineral Resources at the MCB Project. In respect of previously reported Mineral Resource Estimates dated 24 November 2022, apart from additional data that has been used in the 24 November 2025 MRE update, all originally reported material assumptions and technical parameters underpinning the estimates continue to apply and have not been materially changed or qualified. The form and context in which the relevant Competent Person's findings are presented in ASX/AIM announcements dated 24 November 2025 and 12 December 2025, have not been materially modified from the original documents.

Competent Person Statement

Information in this report relating to the Ore Reserve Estimate is based on information compiled, reviewed and assessed by the following Competent Persons: Mr. Steven Olsen (Geology) from Global Geologica, Mr. John Burgess (Metallurgy) from BMECS Pty Ltd, Mr. Florian Beier (Mining) From DMT, and Mr. Matt Pyle (Process Plant and on-site infrastructure capital and operating costs) from Ausenco Australia, who are all Members of the Australasian Institute of Mining and Metallurgy. Each is a consultant through their relevant companies to Makilala Mining Company, Inc., an affiliate of Celsius Resources Limited, and has sufficient experience relevant to the style of mineralisation, the type of deposit, and mining project under consideration, the activities undertaken to qualify as a Competent Person as defined by the 2012 Edition of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (JORC Code) and to be considered as a Qualified Person for the purposes of the AIM Rules.

This ASX announcement and accompanying DFS have been prepared in compliance with the current JORC Code (2012) and the ASX Listing Rules. All material assumptions on which the forecast financial information are based have been included in the ASX announcement and accompanying DFS.

Definitions

|

Term |

Definition |

|

Cut-off Grade |

The minimum grade of a mineralised material considered economically viable to process. For this announcement, a preferred lower cut-off grade of 0.2% copper has been applied, consistent with industry practice and economic assumptions. |

|

Dry-Stack Tailings |

Dry-stack tailings is a storage method where tailings are mechanically dewatered to form a low-moisture, semi-solid cake that is transported, placed, and compacted into a stable, stackable landform instead of being stored as a slurry in a conventional tailings dam. |

|

Epithermal vein deposit |

An epithermal vein deposit is a shallow, low-temperature mineral system formed when hot, metal-rich fluids circulate near the Earth's surface and precipitate gold, silver, and other metals within fractures and veins. |

|

Feasibility Study |

A comprehensive technical and economic assessment conducted to determine the viability of a proposed mining project. The feasibility study evaluates all key aspects of the project, including geology, mineral resources, mining methods, processing, infrastructure, environmental and social impacts, capital and operating costs, and financial returns. Its purpose is to provide sufficient detail and confidence to support a final investment decision and project financing. The outcomes of a feasibility study typically include detailed engineering designs, cost estimates, implementation schedules, and risk assessments. |

|

Front-End Engineering Design (FEED) |

A detailed engineering phase undertaken prior to the commencement of project construction, during which the technical requirements, design specifications, cost estimates, and project execution plans are developed. In mining, FEED typically includes studies of process flows, plant layout, equipment selection, infrastructure, and environmental considerations. The FEED process provides the basis for final investment decisions and forms the foundation for subsequent detailed engineering, procurement, and construction activities |

|

Indicated Mineral Resource |

The part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are sufficiently well established to allow for a reasonable level of confidence in the estimate, but not as high as for Measured Resources. |

|

Inferred Mineral Resource |

The part of a Mineral Resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling, resulting in a lower level of confidence. |

|

Measured Mineral Resource |

The part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are so well established that they can be estimated with confidence sufficient to allow for detailed mine planning. |

|

Mine Recovery |

The proportion of ore successfully extracted during mining compared to the in-situ resource, accounting for losses due to dilution, geotechnical constraints, and mining method. |

|

Mineral Resource Estimate/MRE |

The estimate of mineral resources as calculated and presented in accordance with a minerals code or standard |

|

Mineral Resource |

A concentration or occurrence of solid material of economic interest in or on the earth's crust in such form, grade (or quality), and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade (or quality), continuity and other geological characteristics of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling. Mineral Resources are sub-divided, in order of increasing geological confidence, into Inferred, Indicated and Measured categories |

|

Ordinary Kriging |

A geostatistical estimation technique that predicts block grades by weighting nearby sample data, assuming a constant but unknown local mean. |

|

Ore Reserve |

The economically mineable portion of a Mineral Resource, defined by detailed mine planning, applying modifying factors that demonstrate technical, economic, and regulatory viability. |

|

Porphyry Copper Deposit |

A large, disseminated copper system associated with porphyritic intrusive rocks, characterised by broad alteration zones and low-grade but bulk-mineable mineralisation. |

|

Proven Reserves |

The highest confidence category of Ore Reserves, based on detailed and reliable information, where geological continuity and modifying factors are well established. |

|

Probably Reserves |

The Ore Reserve category with lower confidence than Proven, derived from Indicated Resources where geological and economic factors are reasonably assumed but not fully confirmed. |

|

Sublevel Open Stoping/SLOS |

An underground mining method where ore is extracted in large, vertical or inclined stopes, accessed from multiple sublevels, typically requiring drill-and-blast and remote mucking. |

|

Tonalite |

A coarse-grained intrusive igneous rock composed mainly of plagioclase feldspar with lesser quartz and amphibole, typically associated with calc-alkaline magmatic arcs. |

|

Type 1HGV |

Vertically oriented high-grade copper mineralisation, following geological contacts |

|

Type 1HGH |

Shallow, flat-lying high-grade copper mineralisation, near-surface |

|

Type 3LG |

Broad zones of mineralisation with copper grades generally below high-grade thresholds, modelled for continuity and tonnage estimation |

Forward Looking Statements

Some of the statements appearing in this announcement may be in the nature of forward-looking statements. You should be aware that such statements are only predictions and are subject to inherent risks and uncertainties. Those risks and uncertainties include factors and risks specific to the industries in which the Company operates and proposes to operate as well as general economic conditions, prevailing exchange rates and interest rates and conditions in the financial markets, among other things. Actual events or results may differ materially from the events or results expressed or implied in any forward-looking statement.

No forward-looking statement is a guarantee or representation as to future performance or any other future matters, which will be influenced by a number of factors and subject to various uncertainties and contingencies, many of which will be outside the Company's control.

The Company does not undertake any obligation to update publicly or release any revisions to these forward-looking statements to reflect events or circumstances after today's date or to reflect the occurrence of unanticipated events. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information, opinions or conclusions contained in this announcement. To the maximum extent permitted by law, none of the Company's Directors, employees, advisors, or agents, nor any other person, accepts any liability for any loss arising from the use of the information contained in this announcement. You are cautioned not to place undue reliance on any forward-looking statement. The forward-looking statements in this announcement reflect views held only as at the date of this announcement.

The information contained within this announcement is deemed by the Company to constitute inside information as stipulated under the Market Abuse Regulations (EU) No. 596/2014 as it forms part of UK Domestic Law by virtue of the European Union (Withdrawal) Act 2018.

Celsius Resources Contact Information

Level 5, 191 St. Georges Terrace

Perth WA 6000

PO Box 7059

Cloisters Square PO

Perth WA 6850

P: +61 8 9324 4516

E: info@celsiusresources.com.au

|

Celsius Resources Limited |

|

|

Neil Grimes |

P: +61 419 922 478 |

|

Multiplier Media (Australia Media Contact) Jon Cuthbert |

M: +61 402 075 707 E: jon.cuthbert@multiplier.com.au

|

|

Zeus James Joyce/ James Bavister (Investment Banking) Harry Ansell (Broking)

|

P: +44 (0) 20 3 829 5000 |

Zeus Capital Limited ("Zeus") is the Company's Nominated Adviser and is authorised and

regulated by FCA. Zeus's responsibilities as the Company's Nominated Adviser,

including a responsibility to advise and guide the Company on its responsibilities under

the AIM Rules for Companies and AIM Rules for Nominated Advisers, are owed solely to

the London Stock Exchange. Zeus is not acting for and will not be responsible to any

persons for providing protections afforded to customers of Zeus nor for advising them in

relation to the proposed arrangements described in this announcement or any matter referred to in it.

[1] ASX/AIM announcements 24 November 2025 and 12 December 2025

[2] ASX/AIM announcement 19 May 2025

[3] ASX/AIM announcement 18 June 2025

[4] ASX/AIM announcement 18 March 2024

[5] Refer to ASX/AIM announcement dated 24 November 2025 including the relevant Competent Person Statement

[6] Refer to ASX/AIM announcement 12 December 2025 including the relevant Competent Person Statement

[7] ASX/AIM announcement 11 November 2025

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.

Latest directors dealings

- 3 hours ago Smith & Nephew

- 3 hours ago Autotrader Group plc

- 4 hours ago Wizz Air Holdings

- 4 hours ago Wizz Air Holdings

- 4 hours ago Diageo