Final Results for the Year to 31 January 2026

Summary by AI BETAClose X

27 May 2026

B.P. Marsh & Partners Plc

("B.P. Marsh", "the Company" or "the Group")

Final Results for the Year ended 31 January 2026

Continued strong performance; well positioned for future growth

B.P. Marsh & Partners Plc (AIM: BPM), the specialist private equity investor in early-stage financial services businesses, announces its audited final results for the year ended 31 January 2026 and changes to the composition of the Board.

Highlights:

· Net Asset Value ("NAV") growth of £33.8m (10.3%) to £360.2m (2025: £326.4m)

· Total shareholder return of £41.7m (12.8%)

· £8.0m of dividends (21.64p per share) paid in the year ended 31 January 2026 (2025: £4.0m)

· £13.0m of dividends (36.29p per share) paid or proposed in the year to 31 January 2027

· £7.0m of dividends (19.54p per share) intended to be paid in the year to 31 January 2028

· Consolidated profit before tax of £49.0m (2025: £104.7m)

· Undiluted NAV per share increased to 1009.9p (2025: 890.0p) and fully diluted NAV per share increased to 959.8p (2025: 847.3p)

· Two disposals totalling £30.7m: Stewart Specialty Risk Underwriting Limited and Sterling Insurance Pty Limited

· Eight new equity investments completed; two new equity investments post year-end

· Brian Marsh transitions from Non-Executive Chairman to Founder and Life President

· Rebecca Shelley is appointed Non-Executive Chair of the Board of B.P. Marsh

· Barrie Cornes is appointed as an Independent Non-Executive Director

Investor presentation:

The Company will host a presentation for all existing and potential shareholders via the Investor Meet Company platform on 27 May 2026 at 11:00am BST. Investors can submit questions pre-event via their Investor Meet Company dashboard up until 09:00am today or at any time during the live presentation. Investors can sign up to Investor Meet Company and add to meet B.P. Marsh via:

https://www.investormeetcompany.com/bp-marsh-partners-plc/register-investor.

Investors who already follow B.P. Marsh on the Investor Meet Company platform will automatically be invited.

For further information on B.P. Marsh, its strategy and current portfolio, please visit www.bpmarsh.co.uk or contact:

|

B.P. Marsh & Partners Plc Daniel Topping / Alice Foulk

|

+44 (0)20 7233 3112 |

|

Nominated Adviser & Joint Corporate Broker: Singer Capital Markets Advisory LLP Charles Leigh-Pemberton / Peter Steel / James Todd

|

+44 (0)20 7496 3000 |

|

Joint Corporate Broker: Investec Bank plc Christopher Baird / Maria Gomez de Olea

|

+44 (0)20 7597 5970 |

|

Financial PR & Investor Relations: Tavistock Simon Hudson / Katie Hopkins / Kuba Stawiski |

+44 (0)20 7920 3150 |

About B.P. Marsh

B.P. Marsh & Partners Plc (AIM: BPM) is a specialist investor in early stage and small to medium-sized financial services intermediary businesses, with a particular focus on the insurance sector. Bridging the gap to traditional private equity funding rounds, B.P. Marsh takes a typical initial equity stake of up to £5m, often complemented by loans, and is able to tailor its investment model to each opportunity. Taking a long-term view of its investments, with an average holding period of around seven years, the Group supplies strategic insight and capital while empowering entrepreneurial management teams to grow their businesses.

The B.P. Marsh portfolio is diversified by geography and class of business, spanning insurance brokers, underwriting agencies and financial advisers in the UK, Europe, North America and other international markets. For further information, including details of the current portfolio and recent exits, please visit: www.bpmarsh.co.uk.

Statement by the Founder and Life President:

"This announcement marks a significant moment in the history of B.P. Marsh & Partners Plc. On 26 May 2026, I stepped down from the Board, having served as Executive Chairman from the Company's foundation in 1990 until 1 December 2025, and as Non-Executive Chairman thereafter. I am proud and honoured to continue my association with the Group as Founder and Life President.

When I founded B.P. Marsh my belief was simple: that patient, partnership-led investment alongside talented entrepreneurial management teams could create exceptional long-term value. More than three decades on, with Net Asset Value having grown to £360.2m and a portfolio spanning international insurance and financial services markets, I believe that philosophy continues to be valid.

The year ended 31 January 2026 was another period of strong progress for the Group, with NAV increasing by 10.3%, and total shareholder return of £41.7m (12.8%).

What gives me greatest pride, however, is not simply the financial performance, but the culture and reputation that the business has built over many years, one based on integrity, long-term thinking and genuine partnership. I am enormously grateful to the team, my fellow Directors, our employees and all of our portfolio company partners for their continued hard work, commitment and stewardship of the business.

Alongside the growth of the Group, I am also proud of the work of the Marsh Charitable Trust, established in 1981, which today supports more than 540 organisations across the United Kingdom. Supporting the communities and sectors that shaped my career has always been deeply important to me.

Finally, I would like to thank our shareholders for the trust and support they have shown B.P. Marsh over so many years. The Group is exceptionally well positioned for the future, and I look forward to working with the team in my role going forward continuing the success in the years ahead."

Brian Marsh OBE

Founder & Life President

27 May 2026

Statement by the Non-Executive Chair of the Board

I am delighted to have been appointed Non-Executive Chair of B.P. Marsh & Partners plc on 26 May 2026, following Brian Marsh's transition to his new role as Founder and Life President. Whilst I was not in post during the financial year under review, it is clear from the results and activity outlined throughout this announcement that the Group enters this new chapter from a position of considerable strength. The results reflect another year of strong growth and shareholder returns.

The Group has a strong balance sheet, a healthy pipeline of opportunities and an experienced management team under the leadership of Daniel Topping as Chief Executive Officer. I look forward to working closely with the Board and executive team as the Group continues its next phase of development.

I would also like to recognise Brian Marsh's exceptional contribution to the business and thank him for the strong foundations, culture and investment philosophy he created as his enduring legacy to the Group.

Finally, I would like to thank our shareholders for their continued support and confidence in B.P. Marsh.

Rebecca Shelley

Non-Executive Chair

27 May 2026

Chief Executive Officer Statement

The Group has delivered another year of strong strategic and financial progress, continuing to demonstrate the resilience and scalability of B.P. Marsh's long-term partnership-led investment model.

For the year ended 31 January 2026, the valuation of the equity portfolio increased by 21.4%, adjusting for investments and realisations, while Net Asset Value increased by 10.3%. This performance was achieved alongside significant portfolio activity, including two realisations, eight new investments, multiple follow-on investments into existing high-performing portfolio companies and continued shareholder distributions through dividends and share buy-backs.

The year was characterised by disciplined capital allocation and the continued expansion of the Group's international specialty finance and insurance distribution portfolio. B.P. Marsh increased exposure to several of its strongest-performing investments, including Pantheon, XPT and ATC, whilst also deploying capital into a new generation of high-growth insurance intermediaries, underwriting agencies and complementary financial services businesses. Many of these investments were established alongside experienced management teams with proven sector expertise and, in several cases, leading institutional co-investors.

The Group's portfolio companies now collectively generate in excess of £2.3bn of insurance premium globally, reflecting the scale and maturity of the underlying platform that has been built over recent years. The portfolio remains diversified across brokers, underwriting agencies and specialist insurance services businesses operating across the UK, North America, Australia, Europe and Asia.

Alongside continued investment activity, the Group completed two realisations during the year. Most notably, the disposal of Stewart Specialty Risk Underwriting Limited to Ryan Specialty generated proceeds of £28.3m and an IRR of 89.9%, further evidencing the Group's ability to identify and support high-quality entrepreneurial businesses and realise value over time. The Group also completed the disposal of Sterling Insurance Pty Limited into ATC, increasing its strategic shareholding in one of Australia's leading independent underwriting agencies.

The Board continued to focus on shareholder returns and disciplined balance sheet management throughout the year. In aggregate, the Group has paid and/or proposed approximately £28.0m of dividends across the financial years 31 January 2026, 2027 and 2028, alongside continued share buy-backs aimed at enhancing shareholder value and managing the discount to NAV.

Whilst commercial insurance pricing softened across certain markets during the year, the Board believes the Group's portfolio remains comparatively well insulated from broader market cycles. A significant proportion of the Group's investments are early-stage or recently established businesses focused predominantly on generating new business opportunities, rather than relying heavily on the renewal of historically priced insurance portfolios. As a result, many portfolio companies are driven more by entrepreneurial growth, talent acquisition, product development and market share expansion than by prevailing premium rate conditions alone. In addition, the Group's focus on specialist and niche sectors, together with the fee and commission-based nature of many portfolio companies, continues to provide resilience against wider rating pressure across the insurance market.

The Group also continues to benefit from long-term structural trends within the insurance sector, including ongoing market consolidation, demand for specialist expertise and increasing entrepreneurial activity within niche markets.

The Group's performance over the long term continues to demonstrate the strength and consistency of B.P. Marsh's specialist investment model. Since flotation, NAV has increased from approximately £40.6m to £360.2m as at 31 January 2026, representing an 11.0% compound annual growth rate over the period, whilst NAV per share growth has significantly outperformed relevant AIM benchmarks over the long term.

Importantly, the Group has also demonstrated an increasing ability to translate portfolio growth into substantial realised cash returns. Over the last five years, the Group has completed a number of highly successful disposals, including Kentro Capital, CBC, Lilley Plummer Risks, Sterling Insurance and Stewart Specialty Risk Underwriting. Across the Group's highlighted realisations during this period, aggregate investment proceeds totalled approximately £178.9m from aggregate invested capital of £20.6m, representing an aggregate money multiple of 8.7x. These exits have generated significant realised profits and cash proceeds for the Group, supporting both reinvestment into new opportunities and meaningful shareholder distributions.

The Board believes this long-term track record reflects the enduring strength of the Group's investment philosophy: identifying talented entrepreneurial management teams early, supporting them patiently over the long term and realising value at scale when appropriate opportunities arise. This philosophy was established by Brian Marsh over more than three decades and remains embedded at the core of the Group today.

Brian began his career in insurance broking and underwriting at Lloyd's of London in the early 1960s. Over more than sixty years in the market, he built an unparalleled understanding of the insurance sector; how businesses are conceived, how they grow, and how genuine value is created through partnership rather than simply through capital. From 1979 to 1990, he served as Chairman of Nelson Hurst & Marsh (Holdings) Ltd, before founding B.P. Marsh & Partners in 1990 with a starting capital of £2.5m and a clear, long-term philosophy that has never wavered.

For 35 years, Brian served as Executive Chairman of the Company he built, guiding it from a private vehicle to an AIM-listed firm with a NAV exceeding £350m and a portfolio spanning the globe. The Group has invested in over 60 financial services businesses, building lasting partnerships with management teams, championing entrepreneurialism in insurance, and setting a standard for patient, responsible capital allocation that remains the foundation of everything B.P. Marsh does.

Beyond his business achievements, Brian is the Founder and Chairman of the Marsh Charitable Trust, established in 1981 which now supports over 540 organisations across the United Kingdom. His commitment to giving back to the communities and sectors that shaped him is a reflection of the same values that have always guided his approach to investment: integrity, long-term thinking, and genuine care for the people around him.

In May 2026, Brian stepped back from his governance responsibilities, becoming Founder and Life President. His legacy is not only the Company he founded, but the culture, philosophy and people: a firm that continues to invest in the way he always believed it should.

The Board and the entire team at B.P. Marsh are proud to recognise Brian's exceptional contribution and remain deeply grateful for the foundation he has built and look forward to working with him in his new role.

The Board and management team are also pleased to welcome Rebecca Shelley as Non-Executive Chair of the Company and Independent Non-Executive Director, and Barrie Cornes as an Independent Non-Executive Director.

Rebecca Shelley is an experienced Chair and Senior Independent Director with a strong track record across listed and private companies in financial services, insurance and consumer sectors. She currently serves as Chair of Sabre Insurance Group plc and is Senior Independent Director of Conduit Holdings Limited. Rebecca is also a Senior Independent Director on the board of Liontrust Asset Management PLC and a non-executive Director Hilton Food Group plc, where she chairs the Sustainability and Remuneration Committees. Across her portfolio she has chaired or served on remuneration, audit & risk, nomination and sustainability committees.

Barrie Cornes brings more than 40 years' experience in the insurance sector, having previously served as Managing Director and Head of Research at Panmure Gordon, where he was a leading equity insurance analyst, as well as holding senior investor relations and underwriting roles at Jardine Lloyd Thompson PLC and RSA Insurance Group.

Finally, I would like to thank the entire B.P. Marsh team and all of our portfolio company management teams for their continued hard work, commitment and positivity throughout the year. The progress achieved across the Group reflects the quality of the relationships we have built and the entrepreneurial culture that continues to underpin the business.

The Group entered the new financial year with a strong liquidity position, a healthy pipeline of opportunities and significant momentum across the portfolio. This remains supported by a proven long-term investment model, a diversified international portfolio and substantial available capital. The Board believes the Group is exceptionally well positioned to continue its development and deliver further long-term value growth for shareholders in the years ahead.

Capital allocation - summary

With approximately £29.6m of available cash, as at 26 May 2026, and a strong pipeline, the Group is well positioned to deploy capital selectively and continue its track record of delivering NAV growth and attractive shareholder returns.

Dividend

The Group aims to deliver shareholder value through growth in NAV and sustainable dividends, whilst maintaining sufficient capital for investment.

During the year ended 31 January 2026, the Group paid total dividends of £8.0m, comprising interim, special and final dividends (2025: £4.0m).

For the year ending 31 January 2027, the Group will pay total dividends of £13.0m, comprising a £2.5m interim

dividend (paid in February 2026) a special dividend of £8.0m (paid in March 2026, following the disposal of Stewart Specialty Risk Underwriting Limited) and a proposed final dividend of £2.5m, payable in July 2026.

As announced on 16 April 2026, the Company intends to pay a minimum of £7.0m for the year ending 31 January 2028, comprising an interim and final dividend of £5.0m and a £2.0m special dividend linked to the final deferred consideration from the disposal of Paladin Holdings Limited ("Paladin"), which completed in March 2024.

In aggregate, this represents £28.0m of dividends paid and/or intended across the financial years ending 31 January 2026, 2027, and 2028.

These distributions are aligned with the Group's long-term capital management strategy, balancing shareholder returns with the need to retain liquidity to fund further growth within the portfolio and for future investment opportunities.

Share buy-back

In April 2025, the Company announced a £2.0m share buy-back programme, reinforcing its commitment to managing the discount to NAV. At the General Meeting held on 2 June 2025, shareholders renewed the Company's authority to repurchase up to 10.0% of the issued ordinary share capital and approved a waiver allowing the Brian Marsh Concert Party's holding to increase to a maximum of 42.5% without triggering a mandatory offer.

Under this programme, 277,583 shares were repurchased for £2.0m. Additionally, 769,231 shares were acquired for £5.0m as part of the secondary placing completed in August 2025, through an accelerated bookbuild process. Therefore, the Company has repurchased a total of 1,046,814 Ordinary Shares for a total consideration of £6.9m.

The Board considers share buy-backs to be an important component of the Group's capital allocation strategy, alongside dividends and selective reinvestment, supporting disciplined capital deployment and shareholder returns.

Daniel Topping

Chief Executive Officer

27 May 2026

Portfolio activity

During the financial year ending 31 January 2026, the Group completed two realisations, being:

|

· Stewart Specialty Risk Underwriting Limited |

Sold to Ryan Specialty LLC for consideration of £28.3m (IRR: 89.9%). |

|

· Sterling Insurance Pty Limited |

Sold to ATC Insurance Solutions Pty Limited, for consideration of £3.1m settled via equity in ATC (IRR: 8.8%). |

These realisations generated strong returns and further demonstrate the Group's ability to identify and support high-quality businesses with capable management teams, delivering value for shareholders and other stakeholders over time.

During the financial year to 31 January 2026, the Group completed eight new investments:

|

· Oneglobal Broking Holdings Limited |

London headquartered international retail and wholesale insurance broker. |

|

· iO Finance Partners Topco Limited |

UK-based buy-and-build opportunity within the alternative financing market. |

|

· Sodalis Capital Limited |

London-based newly formed insurance intermediary group focusing on UK and international underwriting, wholesale broking and related services. |

|

· Gambit Risk Finance LLC |

US-based newly formed reinsurance vehicle supporting XPT Group. |

|

· Cameron Specialty HoldCo Limited |

London-based underwriting agency specialising in UK property insurance. |

|

· Amiga Specialty Holdings Limited

|

London-based start-up focused on establishing an international specialty underwriting agency. |

|

· XPT Producer Co LLC |

US-based platform established to recruit and incubate specialist producers for XPT Group. |

|

· Salus Capital Partners Limited

|

UK-based start-up insurance intermediary group specialising in Professional Indemnity insurance. |

During the financial year ending 31 January 2026, the Group completed four follow-on investments:

|

· Pantheon Specialty Group Limited |

A further 2.0% equity stake in Pantheon Specialty Group Limited for cash consideration of £5.5m from members of Pantheon's management team, increasing total shareholding to 39.0%. |

|

· ATC Insurance Solutions Pty Limited

|

A further 1.4% equity stake in ATC for non-cash consideration of AUD 6.5m (c. £3.1m) for the sale of Sterling Insurance Pty Limited, increasing total shareholding to 27.0% |

|

· XPT Group LLC |

A further 0.78% equity stake in XPT Group LLC for aggregate cash consideration of US$1.8m (c. £1.3m), from management shareholders increasing total shareholding to 30.4%. |

|

· Verve Risk Services Limited |

A further 4.0% equity stake in Verve Risk Services Limited for cash consideration of £76,000, increasing total shareholding to 39.0% |

Post Year-End activity

Since 31 January 2026, the Group has continued its momentum in new investments and portfolio activity.

In March 2026, the Group acquired a 25.0% shareholding in Ventura Risk Partners Holdings Limited, a newly formed energy-focused insurance broker placing into the Lloyd's and wider London insurance markets, and a 30.0% shareholding in Nine Edge Limited, a newly established independent financial advice business.

In April 2026, the Group completed the disposal of its investment in Amiga Specialty Holdings Limited ("Amiga") to Sodalis Capital Limited, also a B.P. Marsh portfolio company. The transaction valued Amiga at an initial £1.8m, with B.P. Marsh receiving approximately £0.7m for its 39.2% shareholding and full repayment of its £1.8m loan. The Group retains a 25.5% interest in the enlarged Sodalis group and remains entitled to its pro rata share of any deferred consideration, subject to performance conditions through 2027 and 2028.

In April 2026, the Group acquired an additional 2.0% Cumulative Preferred Ordinary equity stake in Pantheon from members of Pantheon's management team for cash consideration of £5.5m. As a result, the Group's shareholding in Pantheon increased to 41.0%.

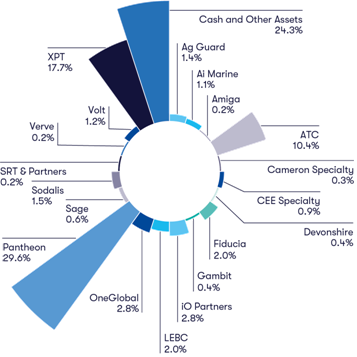

NAV breakdown by portfolio company

The composition of B.P. Marsh's underlying portfolio companies is shown on the chart below.

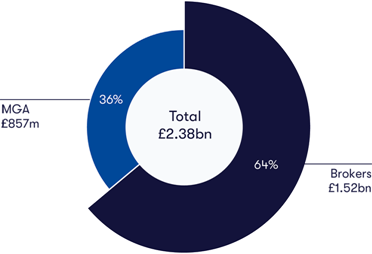

Our current insurance investments are budgeting to produce over £2.3bn of aggregate gross insurance premium during 2026 and a breakdown between brokers and Underwriting Agencies is shown below.

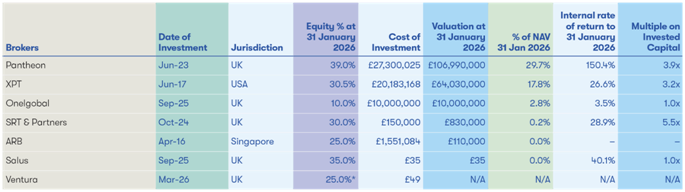

Current Insurance Brokers

The Group's Broking portfolio is budgeting to place over £1.5bn of gross written premium in 2026, generating over £142m of brokerage income, accessing specialty markets around the world.

*Investment into Ventura was made in March 2026, as such the reported equity percentage reflects the equity percentage held at this date

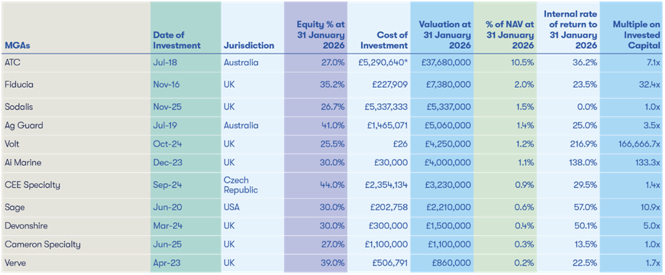

Current Underwriting Agencies

The Group's Underwriting Agencies are budgeting to underwrite £857m of gross written premium in 2026, yielding approximately £96m of commission income across many specialist product areas.

*ATC's equity investment is reported as the combined initial equity investment into ATC, MB Prestige Holdings PTY Limited, and Sterling Insurance PTY Limited

Current Other Financial Services Investments

While insurance-related businesses remain B.P. Marsh's primary focus, the firm selectively invests in adjacent UK financial services where its sector experience, network, and patient capital can support distinctive opportunities.

*Investment into Nine Edge was made in March 2026, as such the reported Equity percentage reflects the Equity percentage held at this date

Current Other XPT-Related Insurance Vehicle Investments

Disposals

Sterling Insurance Pty Limited - ("Sterling")

In May 2025, B.P. Marsh completed the disposal of its indirect equity interest in Sterling to ATC, an independent Australian Underwriting Agency, which it had held through a minority holding in Neutral Bay Investments Limited ("Neutral Bay").

ATC acquired 100.0% of the issued share capital of Sterling for a total consideration of AU$33.0m. B.P. Marsh's share of the consideration, via Neutral Bay, amounted to AU$6.5m (c.£3.1m), which B.P. Marsh received in shares in the enlarged ATC Group. B.P. Marsh's shareholding in ATC increased to approximately 27.0% as a result of the sale.

Stewart Specialty Risks Underwriting Limited - ("SSRU")

In December 2025, the sale of SSRU to Ryan Specialty, LLC.

Upon completion, the Group received CAD$51.2m (£27.6m) net of transaction costs, which represented a £4.7m uplift (20.5%) from the valuation as at 31 July 2025.

The sale represented an Internal Rate of Return of 89.9%, with the Company also receiving a further £739,000 of deferred consideration following the year-end. Taking into account this deferred consideration, the Company received £28.3m.

Disposal - Post Year-End

Amiga Specialty Holdings Limited - ("Amiga")

In March 2026, the Company completed the sale of Amiga to Sodalis Capital Limited.

Upon completion, the Group received £706,250 in cash for its 39.2% shareholding, together with full repayment of its outstanding £1.8m loan facility to Amiga.

Following completion, the Group retained a 25.5% equity interest in Sodalis, providing continued exposure to Amiga through the enlarged group, together with the potential to receive further deferred consideration contingent on Amiga's performance in the financial years ending December 2027 and December 2028.

New Investments

Oneglobal Broking Holdings Limited - ("Oneglobal")

In September 2025, the Group completed its investment in Oneglobal, a London headquartered international retail and wholesale insurance broker majority owned by J.C. Flowers & Co. The investment was made to provide strategic growth capital to support Oneglobal's continued expansion, initially through the acquisition of a Bermudian specialty insurance broker and further development into the Asian market.

Founded through the merger of two existing J.C. Flowers-owned Lloyd's brokers in 2018, Oneglobal operates across 15 offices worldwide spanning Europe, Asia, the Americas and the Middle East. The business specialises in a broad range of insurance lines including marine, property, aviation, financial lines, energy and casualty.

Oneglobal is led by an experienced management team including Jonathan Palmer-Brown, Roger Spicer and Luis Cardoso.

Date of initial investment: September 2025

31 January 2026 valuation: £10,000,000

Cost of Equity: £10,000,000

Equity stake: 10.0%

Loan Facility: N/A

iO Finance Partners Topco Limited - ("iO Partners")

In April 2025, the Group completed its investment in iO Partners, subscribing for an 8.0% shareholding, via a mix of Preferred and Ordinary shares for £10.0m.

iO Partners is a buy-and-build opportunity within the alternative finance market, intending to bring together a diverse group of alternative finance providers to support and grow the UK economy and SME market. Its strategy is to fill a funding gap in the UK market. Upon completion, iO Partners acquired three alternative finance providers.

Janus Henderson Group plc ("Janus Henderson") is a co investor, investing £10.0m on the same terms as B.P. Marsh. Janus Henderson is a NYSE listed global active asset manager headquartered in London. As of 31 December 2024, Janus Henderson had approximately £302.4bn in assets under management.

B.P. Marsh has a successful track record of investing in the financial services sector, backing experienced management teams alongside supportive partners. Whilst iO Partners is not within our primary focus of insurance distribution investments, B.P. Marsh sees this as an opportunity to invest in an experienced management team with a strong track record in the sector, that will deliver long term returns to our shareholders.

Date of initial investment: April 2025

31 January 2026 valuation: £10,000,000

Cost of Equity: £10,000,000

Equity stake: 8.0%

Loan Facility: N/A

Sodalis Capital Limited - ("Sodalis")

In November 2025, the Group completed its investment in Sodalis, a newly formed insurance intermediary group focused on UK and international underwriting, wholesale broking and related services.

Sodalis has been established to pursue a buy-and-build strategy within the international insurance intermediary sector, targeting specialist underwriting and wholesale broking platforms across the UK, Europe and Asia. The investment is intended to support initial acquisitions together with working and regulatory capital for Sodalis and its future trading subsidiaries.

The investment was made alongside Alliant Insurance Services, Inc., whose participation brings significant distribution reach and sector expertise to the platform. Sodalis is founded and led by Colin Thompson, an experienced insurance executive with more than 30 years of experience building and managing insurance intermediary businesses globally.

Date of initial investment: November 2025

31 January 2026 valuation: £5,337,000

Cost of Equity: £5,337,333

Equity stake: 26.7%

Loan Facility: N/A

Gambit Risk Finance LLC - ("Gambit Re")

In August 2025, the Group completed a complementary investment in support of its US-based investee company XPT Group LLC through the formation of Gambit Re, a newly established reinsurance vehicle for selected XPT underwriting programmes. The initiative was designed to support XPT's strategic growth ambitions and enhance its operational and financial flexibility.

Gambit Re provides limited risk capital to selected underwriting programmes within XPT's underwriting arm, Platinum Specialty Underwriters. The vehicle operates on a fully collateralised basis and initially supports five profitable programmes across Platinum's underwriting portfolio.

Date of initial investment: August 2025

31 January 2026 valuation: £1,370,000

Cost of Equity: £1,394,508

Equity stake: 8.3%

Loan Facility: N/A

Cameron Specialty HoldCo Limited - ("Cameron Specialty")

In June 2025, the Group completed its investment in Cameron Specialty, a London-based underwriting agency, specialising in UK property insurance across the commercial combined and property owners sectors.

Founded in 2021, Cameron Specialty is led by Founder & CEO Tom Kirkland, who brings 20 years of insurance industry experience spanning both broking and underwriting.

With the support of the Group, Cameron Specialty intends to expand its property insurance offering into the Republic of Ireland and mainland Europe, leveraging existing broker relationships, while also developing additional lines of business.

Date of initial investment: June 2025

31 January 2026 valuation: £1,100,000

Cost of Equity: £1,100,000

Equity stake: 27.0%

Loan Facility: £600,000

Amiga Specialty Holdings Limited - ("Amiga")

In June 2025, the Group completed its investment in Amiga, subscribing for a 49.0% shareholding for £49. Amiga is a start-up entity focused on establishing an international specialty underwriting agency.

Amiga aims to build a diversified portfolio of specialty insurance products across key global markets, pursuing both organic growth and a strategic mergers and acquisitions approach.

Amiga is led by its Managing Director, Adam Kembrooke, a seasoned insurance professional with over 20 years of industry experience. Prior to founding Amiga, Mr. Kembrooke served as CEO and President of Nexus US, as well as Group Chief Legal Officer at its parent company, Kentro Capital Limited.

Post year-end, in March 2026, the Company completed the sale of Amiga to Sodalis Capital Limited, receiving £706,250 in cash for its 39.2% shareholding together with full repayment of its outstanding £1.8m loan facility to Amiga upon completion.

Date of initial investment: June 2025

31 January 2026 valuation: £706,000

Cost of Equity: £49

Equity stake: 49.0%

Loan Facility: £10,000,000

XPT Producer Co LLC - ("XPT Producer Co")

In September 2025, the Group completed a follow-on investment in support of its US-based investee company XPT Group LLC ("XPT") through the establishment of XPT Producer Co, a new platform created to recruit and incubate new producers.

The vehicle has been designed to accelerate XPT's growth strategy by attracting experienced, high-quality, revenue-generating producers.

Date of initial investment: September 2025

31 January 2026 valuation: £2,565

Cost of Equity: £2,565

Equity stake: 35.0%

Loan Facility: £9,860,000

Salus Capital Partners Limited - ("Salus")

In September 2025, the Group completed its investment in Salus, a start-up UK-based insurance intermediary group specialising in Professional Indemnity insurance.

Salus operates through two subsidiaries: Forte Professions Limited, a specialist Professional Indemnity broker serving UK-domiciled businesses including architects, engineers, construction firms, surveyors, accountants and insurance brokers; and Scribe MGA Limited, the underwriting arm of Salus, focused on Professional Indemnity cover for small and medium-sized businesses.

Salus was founded by James Page, Matthew Jones, Dawn Zacharow and Stuart Barker, whose combined experience in insurance broking and underwriting within the Professional Indemnity market approaches 100 years. With the backing of the Group, the Salus team aims to establish a premier, client-focused brokerage and underwriting agency headquartered in Bristol.

Date of initial investment: September 2025

31 January 2026 valuation: £35

Cost of Equity: £35

Equity stake: 35.0%

Loan Facility: £2,000,000

New Investments - Post Year-End

Ventura Risk Partners Holdings Limited - ("Ventura")

In March 2026, the Group completed its investment in Ventura, a newly formed insurance broker focused on placing energy risks into the Lloyd's and wider London insurance markets.

Ventura is a London-based start-up broker, specialising in energy risks and aiming to serve a market that has experienced significant consolidation, reducing the number of independent specialist placement options available to North American retail brokers. The business intends to address this opportunity through an independent operating model, prioritising technical placement capability over scale.

Ventura was founded by Alex Taylor, an experienced energy insurance broker with established relationships across London market underwriters and North American brokers. The investment is consistent with the Group's strategy of backing high-quality early-stage insurance intermediary businesses.

Date of initial investment: March 2026

31 January 2026 valuation: N/A

Cost of Equity: £49

Equity stake: 25.0%

Loan Facility: £2,000,000

Nine Edge Wealth Limited - ("Nine Edge")

In March 2026, the Group completed its investment in Nine Edge, a newly established, UK-based independent financial advice business.

Upon completion, Nine Edge acquired RMS Limited, an Edinburgh-based advice company with approximately £70.0m of assets under management. This acquisition provided Nine Edge with immediate regulatory permissions and a recurring revenue base, forming the foundation of its platform for future organic growth and further acquisitions.

In addition to its core financial planning and advisory services, Nine Edge intends to develop complementary offerings including tax advisory services, wills, executor services and trusts, while leveraging artificial intelligence and technology-enabled solutions to enhance client outcomes and operational efficiency. The business commenced operations with offices in London and Edinburgh.

Nine Edge was established by Derek Miles, an experienced executive with more than 25 years in the UK financial planning sector and a longstanding relationship with the Group.

Date of initial investment: March 2026

31 January 2026 valuation: N/A

Cost of Equity: £30

Equity stake: 30.0%

Loan Facility: £5,000,000

Follow-on Investments and Funding During the Year

Pantheon Specialty Group Limited ("Pantheon") - UK

+ 26.1 pence NAV per share change in the Year

Since the Group's original investment in Pantheon in June 2023, when it subscribed for a 25.0% stake, the business has been a stand out performer in the portfolio.

Over the financial year to 31 January 2026, the Group made one further equity investment in Pantheon.

In June 2025, the Group acquired a further 2.0% Cumulative Preferred Ordinary equity stake in Pantheon from members of Pantheon's management team for cash consideration of £5.5m. Following completion of the transaction, the Group's total shareholding in Pantheon increased from 37.0% to 39.0%.

The transaction involved the purchase of shares from members of Pantheon's management team, enabling them to realise a portion of the value created in the business while continuing to retain a substantial majority interest and remaining fully aligned with the future growth of the company.

Since the Group partnered with management to establish Pantheon, the business has delivered a strong financial and operational performance, developing into a leading independent broker in the London insurance market.

Given this continued progress, the Group considered it an attractive opportunity to increase its investment in Pantheon, supporting a deserved partial liquidity event for management while further increasing its exposure to a high-growth business with significant ongoing potential.

Date of initial investment: June 2023

31 January 2026 valuation: £106,990,000

Cost of Equity: £27,300,025

Equity stake: 39.0%

ATC Insurance Solutions ("ATC") - Australia

+ 10.2 pence NAV per share change in the Year

In July 2025, the Group acquired a further 1.4% equity stake in ATC for non-cash consideration of AU$ 6.5m (c. £3.1m), facilitated through the disposal of its entire holding in Sterling Insurance Pty Limited ("Sterling") to ATC. Following completion of the transaction, the Group's shareholding in ATC increased to 27.0%.

ATC continues to perform strongly across its diverse range of product offerings and remains one of the Group's most significant investments. Since the Group's original investment in 2018, ATC has delivered substantial growth and has developed into the largest independent underwriting agency in Australia.

The business has demonstrated a strong track record of expansion through both organic growth and strategic acquisitions, supported by an experienced management team and a diversified operating platform. The Group remains confident in ATC's long-term prospects and expects the business to continue building on its strong market position.

Date of initial investment: July 2018

31 January 2026 valuation: £37,680,000

Cost of Equity: £9,603,303

Equity stake: 27.0%

XPT Group LLC ("XPT") - USA

+ 5.3 pence NAV per share change in the Year

In December 2025 and January 2026, the Group acquired a further 0.78% equity stake in XPT from management shareholders for aggregate cash consideration of US$1.8m (c.£1.3m). Following these acquisitions, together with other equity movements, the Group's fully diluted shareholding in XPT increased to 30.49%.

In addition, the Group participated in further strategic investments alongside XPT, including support for Gambit Re and XPT Producer Co, referenced above, both of which are intended to broaden XPT's platform capabilities and enhance its long-term growth prospects. These investments reflect XPT's continued strategy of expanding through a combination of organic development, targeted recruitment and selective acquisitions.

Since the Group's initial involvement in 2017, XPT has delivered a strong operational and financial performance, supported by disciplined execution and a scalable business model. The Group remains confident in XPT's growth trajectory and believes it is well positioned to continue capitalising on opportunities within the specialist insurance market.

Date of initial investment: June 2017

31 January 2026 valuation: £64,030,000

Cost of Equity: £20,183,168

Equity stake: 30.5%

Other Portfolio Company Highlights

Dempsey Group Limited (owns 100% of Ai Marine Risk Limited) ("Ai Marine") - UK

+ 10.4 pence NAV per share change in the Year

Ai Marine continues to perform strongly across its core marine underwriting activities and is progressing a number of strategic initiatives to broaden its product offering.

Since the Group's investment, Ai Marine has continued to strengthen its position within the specialist marine insurance market, supported by its technical underwriting expertise, disciplined risk selection and strong broker relationships. The Group remains encouraged by the Ai Marine's continued development and long-term growth prospects.

During the year, Ai Marine progressed the launch of a new Special Risks product, designed to provide shipowners with bespoke coverages beyond the scope of standard marine insurance lines. Each policy is tailored to the specific requirements and risk appetite of the insured, offering specialist protection across a range of complex physical damage and economic loss exposures.

In addition to creating new revenue opportunities, the launch of Special Risks is expected to enhance portfolio diversification, support the growth of Ai Marine's wider Hull & Machinery business and contribute positively to underwriting performance over time.

Date of initial investment: December 2023

31 January 2026 valuation: £4,000,000

Cost of Equity: £30,000

Equity stake: 30.0%

Volt UW Holdco Limited (owns 100% of Volt UW Limited) ("Volt") - UK

+ 11.1 pence NAV per share change in the Year

Volt has continued to build momentum during the year, supported by an increasing market presence and a number of strategic senior hires across the business.

Volt has continued to strengthen its position within its chosen markets through disciplined underwriting, strong broker relationships and the recruitment of high-calibre talent. The Group remains encouraged by the business's progress and long-term growth prospects.

During the year, Volt progressed the expansion of its energy offering through the planned appointment of an experienced senior underwriter to lead its Midstream Energy division. The individual joins from a major global insurer, bringing significant sector expertise, underwriting experience and established market relationships.

The Group believes this strategic hire will enhance Volt's underwriting capabilities, diversify its portfolio and create an additional platform for future growth within the specialist energy insurance market.

Date of initial investment: October 2024

31 January 2026 valuation: £4,250,000

Cost of Equity: £26

Equity stake: 25.5%

Agri Services Company Pty Limited ("Ag Guard") - Australia

+ 6.1 pence NAV per share change in the Year

Ag Guard has continued to make significant progress during the year with the launch of new products across its core agricultural markets.

In late 2025, Ag Guard agreed to transfer its principal Australian binder arrangements from QBE to Insurance Australia Group ("IAG"), with the new agreements now executed. The arrangements cover Ag Guard's core products. This new partnership with IAG materially enhances Ag Guard's growth platform in Australia, providing access to a significantly larger addressable market than was available under the previous arrangements.

In addition, Ag Guard has progressed the launch of a new Farm Pack product in New Zealand, backed by 100% capacity from IAG New Zealand Limited. The product is designed to provide comprehensive cover for farming businesses, including property damage, business interruption, commercial motor, liability, machinery breakdown and stock deterioration.

The Group believes these developments are transformational for Ag Guard, materially increasing its long-term growth prospects through a larger portfolio across both Australia and New Zealand.

Date of initial investment: July 2019

31 January 2026 valuation: £5,060,000

Cost of Equity: £1,465,071

Equity stake: 41.0%

Market Commentary

The Group continues to monitor key developments across the insurance sector, with a focus on pricing trends, M&A activity and the impact of artificial intelligence.

Commercial insurance pricing continued to soften through 2025 and into 2026. Marsh McLennan's Global Insurance Market Index reported rate declines of 4% in Q4 2025 and 5% in Q1 2026, marking the seventh consecutive quarter of reductions. This reflects increased insurer competition, favourable reinsurance conditions and strong underwriting capacity, with new entrants and growth-focused carriers driving more competitive pricing and broader terms.

The fee and commission-based revenue of brokers and underwriting agencies provide a degree of insulation from rating pressures. In addition, rate volatility in specialist risk segments, where many of the Group's portfolio companies operate, has typically been more moderate. The Board, therefore, remains confident in the resilience of underlying revenue generation. The Group works closely with investee management teams to ensure their businesses remain robust and well positioned to mitigate emerging risks.

The Group also continues to observe ongoing market consolidation across the insurance distribution landscape. M&A activity remains active among brokers, underwriting agencies and carriers, driven by the pursuit of scale, enhanced distribution capabilities and access to specialist expertise. This trend is being supported by continued private equity interest and favourable financing conditions, although transaction volumes have moderated slightly in line with broader economic uncertainty.

The Group continue to monitor the situation in the Middle East, which is currently driving rate increases across several specialty insurance lines, in which the Group's portfolio operates. Marine war risk premiums have seen some of the sharpest movements, with hull and machinery insurance for ships passing through the Strait of Hormuz jumping sharply in a short period.

Lastly, the Group also continues to monitor the effect of artificial intelligence on the insurance industry. B.P. Marsh sees AI as a net enabler, not disruptor, in the industry. The insurance and financial advice industries will continue to require skilled brokers, underwriters, and advisers. AI will assist by automating administrative bottlenecks, accelerating data management, and freeing professionals to focus on client relationships and judgement-led work.

New Business

During the year ended 31 January 2026, the Group completed eight new investments across its specialist sectors, maintaining a disciplined approach to identifying opportunities where it can add value.

The Group remains focused on niche SME markets, partnering with experienced management teams to support sustainable long-term growth and enhance shareholder returns.

New business activity remained strong, with 61 new business enquiries received during the year (2025: 63). The Group continues to maintain a healthy pipeline of prospective investments, and where terms are appropriate, expects to complete further transactions in the year ending 31 January 2027.

Supported by a strong liquidity position and established track record, the Group is well placed to continue originating and executing investments that deliver long-term value.

Daniel Topping

Chief Executive Officer

27 May 2026

Chief Finance Officer Statement

I am delighted to present the Full Year Results, and to report that the Group has maintained a strong financial performance for the year ended 31 January 2026.

Financial performance summary

The table below summarises the Group's financial results and key performance indicators for the year ended 31 January 2026:

|

|

Year to/as at |

|

Year to/as at |

|

|

|

31 January |

|

31 January |

|

|

|

2026 |

|

2025 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net asset value |

£360.2m |

|

£326.4m |

|

|

Net asset value per share - undiluted |

1009.9p |

|

890.0p |

|

|

Net asset value per share - diluted |

959.8p |

|

847.3p |

|

|

|

|

|

|

|

|

Profit before tax |

£49.0m |

|

£104.7m |

|

|

Dividend per share paid |

21.64p |

|

10.72p |

|

|

Total shareholder return (including dividends)1 |

£41.8m |

|

£101.2m |

|

|

Total shareholder return on opening shareholders' funds |

12.8% |

|

44.2% |

|

|

|

|

|

|

|

|

Net cash used by operating activities |

£(4.6)m |

|

£(4.2)m |

|

|

Equity investment for the year |

£37.9m |

|

£31.5m |

|

|

Realisations (net of disposal costs) |

£36.4m |

|

£65.7m |

|

|

Loans issued in the year |

£17.2m |

|

£11.2m |

|

|

Loans repaid by investee companies in the year |

£3.0m |

|

£14.7m |

|

|

Cash and treasury funds at end of year |

£49.5m |

|

£74.1m |

|

|

Borrowing / Gearing |

£Nil |

|

£Nil |

|

|

|

|

|

|

|

1Total shareholder return is the increase in NAV for the year of £33.8m plus dividends paid of £8.0m (2025: increase in NAV of £97.2m plus dividends paid of £4.0m)

The Group delivered an increase in NAV of £33.8m (10.3%) to £360.2m (2025: £326.4m), compared with an increase of £97.2m (42.4%) for the same period in 2025. Including the £8.0m aggregate dividend paid in February 2025, May 2025 and July 2025, this represented an overall return of 12.8% for the year (2025: including a £4.0m aggregate dividend, the overall return was 44.2%).

The NAV of £360.2m at 31 January 2026 represents a total increase in NAV of £331.0m since the Group was originally formed in 1990 having adjusted for the original capital investment of £2.5m, the £10.1m net proceeds raised on AIM in 2006 and the £16.6m of net proceeds raised through the Share Placing and Open Offer in July 2018. The Group has delivered an annual compound growth rate of 11.0% in Group NAV after running costs, realisations, losses, distributions and corporation tax since flotation, and 13.0% since 1990.

Investment performance

The Group's equity portfolio movement during the year was as follows:

|

31 January 2025 valuation |

Acquisitions at cost |

Disposal proceeds |

Adjusted 31 January 2025 valuation |

31 January 2026 valuation |

|

£224.1m |

£37.9m |

£(36.4)m |

£225.6m |

£273.8m |

The equity portfolio continued to increase in value, rising by 21.4% to £273.8m (31 January 2025: £224.1m, an increase of 83.5%) after adjusting for £36.4m of net realisations and £37.9m of acquisitions in the year.

The Group made two disposals during the year totalling £30.7m. AU$6.5m (£3.1m) was received from the sale of the Group's entire c.19.7% investment in Sterling to ATC which completed on 30 May 2025. The consideration received by the Group was satisfied entirely in the form of additional equity in the enlarged ATC Group. CA$ 51.2m (£27.6m) was also received from the sale of the Group's entire 28.2% investment in SSRU to Ryan Specialty, LLC.

In addition, the Group received a distribution of £5.7m following LEBC Holdings Limited's ("LEBC") receipt of the first tranche of deferred consideration payable over a three-year earn-out period in connection with the sale of 100% of Aspira Corporate Solutions Limited, LEBC's wholly-owned subsidiary, to Titan Wealth Holdings Limited, which completed in April 2024.

The Group invested a total of £37.9m in equity in the portfolio during the year (2025: £31.5m):

· £10.1m into the existing portfolio, including £5.5m in Pantheon, £3.1m in ATC, £1.4m in XPT, £0.1m in Verve; and

· £27.8m into eight new investments, including £10.0m in iO Partners, £10.0m in Oneglobal, £5.3m in Sodalis, £1.4m in Gambit, £1.1m in Cameron Specialty, £2,565 (nominal value) in XPT Producer Co, £49 (nominal value) in Amiga and £35 (nominal value) in Salus.

Operating income

Net gains from investments were £52.3m (2025: £107.5m), of which £32.6m related to the revaluation of the investment portfolio, and £19.7m in respect of realised gains on disposal of investments during the year to 31 January 2026 (2025: £90.2m related to revaluation of the investment portfolio and £17.3m related to realised gains on disposal of investments). Whilst net gains from investments were 51.3% lower compared to the previous year, the prior year's net gains from investments included substantial unrealised gains, of which £81.8m arose from the Group's three largest investments, Pantheon, XPT and ATC as a result of strong trading performance.

Despite completing two realisations during the year ended 31 January 2026, the Group's significant investment activity during the year contributed to a £2.6m increase in portfolio income, representing growth of 33.7% to £10.4m (2025: £7.8m). Dividend income was £1.3m higher due to both strong investment portfolio performance and new investments made during the year. Loan interest increased by £0.6m due to further drawdowns from the portfolio's existing facilities and new loans granted in the year to both the existing portfolio and to new investments. Fee income also increased by £0.7m due to new investments during the year and a higher amount of one-off transaction and loan arrangement fees charged in 2026 compared to 2025.

Operating expenses

Operating expenses increased by £1.1m, or 8.0%, during the year to £14.8m (2025: £13.7m), the majority of which related to general cost inflation and professional fees incurred for new and follow-on investment activity.

Profit before tax

The consolidated profit before tax for the year was £49.0m, representing a decrease of £55.7m, or 53.0%, compared to the £104.7m reported in 2025. As noted under 'Operating Income', the year-on-year reduction primarily reflects the significant unrealised gains recognised in the prior year, which created a particularly strong comparative base (2025: increase of £61.1m, or 140%, to £104.7m).

The consolidated profit after tax was £48.2m (2025: £99.5m).

The Group's strategy is to cover its expenses from the portfolio yield. On an underlying basis, including treasury returns and realised gains in cash, but excluding unrealised investment activity (unrealised gains on equity, movement in the provision for deferred consideration on equity portfolio disposals and provision against loans receivable from investee companies), this was achieved with a pre-tax profit of £12.2m2 for the year (2025: £9.0m2).

2Underlying pre-tax profit of £12.2m is calculated as profit before tax of £49.0m, less unrealised gains on equity investment revaluation of £32.7m, less movement in the provision for deferred consideration on equity portfolio disposals of £4.1m (2025: underlying pre-tax profit of £9.0m calculated as profit before tax of £104.7m, less unrealised gains on equity investment revaluation of £90.2m, less movement in the provision for deferred consideration on equity portfolio disposals of £5.5m).

Liquidity and Loan Portfolio

In addition to contributing equity to its investment portfolio, the Group frequently extends loan financing, either as part of the initial investment structure or as subsequent funding to support further growth. This additional financing may be used for acquisitions, working capital, recruitment or product development.

The Group's loan portfolio balance increased by £13.2m during the year to £38.8m as at 31 January 2026 (31 January 2025: £25.6m). The key movements were:

· £8.2m was provided to the existing investment portfolio, including £6.3m to Pantheon, £0.75m to SRT, £0.55m to Volt, £0.25m to Verve, £0.25m to Devonshire and £0.1m to Dempsey Group.

· £9.0m was provided to the new investments made by the Group during the year, including £6.3m to XPT Producer Co, £1.6m to Amiga, £0.8m to Salus and £0.3m Cameron Specialty.

· £3.0m of loans were repaid during the year, including £2.5m from Alchemy Underwriting Limited and £0.5m from The Fiducia MGA Company Limited ("Fiducia").

· A £1.0m decrease due to foreign exchange movements.

During the year the Group paid dividends totalling £8.0m and bought back £6.9m in shares.

Other significant cash movements during the year included the receipt of £9.2m in further consideration from the sale of the Group's investment in Paladin, which completed in March 2024. This represented the first of two anticipated tranches of deferred consideration that are expected in relation to the sale.

At 31 January 2026, the Group had total available cash and treasury funds of £49.5m (31 January 2025: £74.1m).

Post Year-End Activity

Since 31 January 2026 the Group has made two new equity investments. In March 2026, the Group made an investment into Nine Edge for a nominal equity of £30, alongside an initial loan drawdown of £1.75m from its agreed £5.0m loan facility. In the same month the Group also made an investment into Ventura for a nominal equity of £49.0, alongside an initial loan drawdown of £0.4m from its agreed £2.0m loan facility.

In April 2026 the Group also made a follow-on equity investment into Pantheon of £5.5m, increasing its shareholding from 39.0% to 41.0%.

In March 2026 the Group completed the disposal of its investment in Amiga, receiving initial consideration of £0.7m plus the repayment of its £1.8m loan outstanding.

The Group has provided £15.5m in further loans, including £4.0m in respect of its new investments in Nine Edge (£3.6m) and Ventura (£0.4m) and £11.0m to its existing portfolio in respect of further drawdowns from agreed loan facilities and new facilities provided, with £3.5m provided to XPT Producer Co, £2.0m to Oneglobal, £1.8m to iO Partners, £1.5m to Devonshire, £1.25m to Volt, £0.5m to Salus, £0.4m to Ag Guard, £0.2m to Ai Marine, £0.2m to Amiga and £0.15m to Pantheon. The Group also received £1.8m in loan repayments from Amiga (on disposal) and £0.1m from Fiducia. The loan portfolio balance is currently £52.4m.

Other significant cash movements include the receipt of £9.6m in further consideration from the sale of the Group's investment in Paladin in March 2024, representing the second and final tranche of deferred consideration that is expected in relation to the sale.

Further consideration of £0.7m was also received from the sale of the Group's investment in SSRU, which completed in December 2025. This represents the final deferred consideration that is expected in relation to the sale.

In addition, £10.5m has been distributed in dividends since the year end and £0.3m of share buybacks have been undertaken. The Group's current cash and treasury balance is £29.6m. Treasury funds are all in one month or less deposit accounts.

The Group is debt free.

Undiluted / Diluted NAV per share

The NAV per share at 31 January 2026 was 1009.9p (2025: 890.0p). This has been calculated using Group net assets as at 31 January 2026, adjusted to include the £1.5m (2025: £1.5m) loan due from the Employee Benefit Trust, which will be repaid upon the sale by the Trust of the 525,240 vested JSOP shares (2025: 525,240). The calculation excludes the 1,055,000 shares held in treasury (2025: 23,872) and the 236,259 unallocated shares held by the Trust (2025: 236,259).

The diluted NAV per share at 31 January 2026 is 959.8p (31 January 2025: 847.3p). This includes the full 761,499 (2025: 761,499) shares remaining within the Employee Benefit Trust and also includes £2.0m (2025: £2.0m) of loan repayable if the shares, including the 236,259 shares that are currently unallocated, were sold.

The diluted NAV per share calculation also includes the 1,685,000 (2025: 1,682,500) options over ordinary shares granted to certain Directors and employees of the Group in November 2023 (and subsequently in March 2025 following the reallocation of options forfeited on departure of a Director and two other employees), which became dilutive at 31 July 2024, as the performance criteria for NAV growth had been met.

Francesca Chappell

Chief Finance Officer

27 May 2026

Forward-looking statements:

Certain statements in this announcement are forward-looking statements. In some cases, these forward looking statements can be identified by the use of forward looking terminology including the terms "anticipate", "believe", "intend", "estimate", "expect", "may", "will", "seek", "continue", "aim", "target", "projected", "plan", "goal", "achieve" and words of similar meaning or in each case, their negative, or other variations or comparable terminology. Forward-looking statements are based on current expectations and assumptions and are subject to a number of known and unknown risks, uncertainties and other important factors that could cause results or events to differ materially from what is expressed or implied by those statements. Many factors may cause actual results, performance or achievements of B.P. Marsh to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Important factors that could cause actual results, performance or achievements of B.P. Marsh to differ materially from the expectations of B.P. Marsh, include, among other things, general business and economic conditions globally, industry trends, competition, changes in government and changes in regulation and policy, changes in its business strategy, political and economic uncertainty and other factors. As such, undue reliance should not be placed on forward-looking statements. Any forward-looking statement is based on information available to B.P. Marsh as of the date of the statement. All written or oral forward-looking statements attributable to B.P. Marsh are qualified by this caution. Other than in accordance with legal and regulatory obligations, B.P. Marsh undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise. Nothing in this announcement should be regarded as a profit forecast.

Investments

As at 31 January 2026 the Group's equity interests were as follows:

Ag Guard PTY Limited

Ag Guard is an underwriting agency, which provides insurance to the agricultural sector, based in Sydney, Australia. The Group holds its investment through Ag Guard's Parent Company, Agri Services Company PTY Limited.

Date of investment: July 2019

Equity stake: 41.0%

31 January 2026 valuation: £5,060,000

Ai Marine Risk Limited

(www.aimarinerisk.com)

Ai Marine is a start-up underwriting agency with a focus on marine hull insurance and with a strong focus on the UK & Europe, Middle East and Asia Pacific regions.

Date of investment: December 2023

Equity stake: 30.0%

31 January 2026 valuation: £4,000,000

Amiga Specialty Holdings Limited

(www.amigaspecialty.com)

Amiga is a start-up focused on establishing an international specialty underwriting agency. Amiga aims to build a diversified portfolio of specialty insurance products across key global markets, pursuing both organic growth and a strategic mergers and acquisitions approach.

Date of Investment: June 2025

Equity stake: 49.0%

31 January 2026 valuation: £706,000

Asia Reinsurance Brokers (Pte) Limited

(www.arbrokers.asia)

ARB is an independent specialist reinsurance and insurance risk solutions provider headquartered in Singapore.

Date of investment: April 2016

Equity stake: 25.0%

31 January 2026 valuation: £110,000

ATC Insurance Solutions PTY Limited

(www.atcis.com.au)

ATC is an underwriting agency and Lloyd's Coverholder, specialising in accident & health, construction & engineering, trade pack, motor and sports insurance headquartered in Melbourne, Australia.

Date of investment: July 2018

Equity stake: 27.0%

31 January 2026 valuation: £37,680,000

Cameron Specialty Holdco Limited

(www.cameron-specialty.com)

Cameron Specialty is a London-based underwriting agency specialising in UK property insurance in the commercial combined and properly owner sectors.

Date of investment: September 2025

Equity stake:27.0%

31 January 2026 valuation: £1,100,000

CEE Specialty s.r.o.

(https://cee-specialty.eu/index.php/cs/)

CEE Specialty is a underwriting agency based in Prague, Czech Republic specialising in Marine Hull, Bonds and Liability Insurance.

Date of investment: September 2024

Equity stake: 44.0%

31 January 2026 valuation: £3,230,000

Devonshire UW Limited

(www.devonshire-underwriting.co.uk)

Devonshire is a London-based underwriting agency, specialising in transactional risks encompassing Warranty and Indemnity, Specific Tax, and Legal Contingency Insurance.

Date of investment: March 2024

Equity stake: 30.0%

31 January 2026 valuation: £1,500,000

The Fiducia MGA Company Limited

(www.fiduciamga.co.uk)

Fiducia is a UK marine cargo Underwriting Agency and Lloyd's Coverholder which specialises in the provision of insurance solutions across a number of marine risks including, cargo, transit liability, engineering and terrorism Insurance.

Date of investment: November 2016

Equity stake: 35.2%

31 January 2026 valuation: £7,380,000

Gambit Risk Finance LLC

(www.gambitre.com)

Gambit Re is a US-based newly established reinsurance vehicle for selected XPT underwriting programmes designed to support XPT's strategic growth ambitions.

Date of investment: August 2025

Equity stake: 8.3%

31 January 2026 valuation: £1,370,000

iO Finance Partners

(www.iofp.co.uk)

iO Partners is a buy-and-build opportunity with the alternative financing market, intending to bring together a diverse group of alternative finance providers to support and grow the UK economy and SME market.

Date of investment: April 2025

Equity stake:8.0%

31 January 2026 valuation:£10,000,000

LEBC Holdings Limited

LEBC is an Independent Financial Advisory company providing services to individuals, corporates and partnerships, principally in employee benefits, investment and life product areas.

Date of investment: April 2007

Equity stake: 62.0%

31 January 2026 valuation: £7,120,000

New Denison Limited

Date of investment: June 2023

Equity stake:40%

31 January 2026 valuation: £0

Oneglobal Broking Holdings Limited

(www.oneglobalbroking.com)

Oneglobal is a London headquartered international retail and wholesale insurance broker which provides specialist insurance solutions across multiple markets.

Date of investment: September 2025

Equity stake:10.0%

31 January 2026 valuation: £10,000,000

Pantheon Specialty Group Limited

(www.pantheonspecialty.com)

Pantheon is a holding company established in partnership with Robert Dowman. Pantheon acquired 100% of the share capital of the Lloyd's broker Denison and Partners Limited. With the support of B.P Marsh, Robert Dowman is looking to build a market leading independent specialist broker, across multiple markets.

Date of investment: June 2023

Equity stake: 39.0%

31 January 2026 valuation: £106,990,000

Sage Program Underwriters, Inc.

(www.sageuw.com)

Sage provides specialist insurance products to niche industries, initially in the inland delivery and field sport sectors based in Bend, Oregon.

Date of investment: June 2020

Equity stake: 30.0%

31 January 2026 valuation: £2,210,000

Salus Capital Partners Limited

Salus is a UK-based start-up insurance intermediary group specialising in Professional Indemnity insurance.

Date of investment: September 2025

Equity stake: 35.0%

31 January 2026 valuation: £35

Sodalis Capital Limited

(www.sodaliscapital.com)

Sodalis is a newly formed, London-based insurance intermediary group focusing on UK and international underwriting, wholesale broking and related services.

Date of investment: November 2025

Equity stake:26.7%

31 January 2026 valuation: £5,337,000

SRT & Partners Limited

(www.srtpartners.co.uk)

SRT & Partners is a start-up UK Retail and London Market broker. Headquartered in London, it furnishes its clients and partners with access to the special Broking and Underwriting services they require.

Date of investment: October 2024

Equity stake:30.0%

31 January 2026 valuation: £830,000

Verve Risk Services Limited

(www.ververisk.com)

Verve is a London-based underwriting agency specialising in Professional and Management Liability for the insurance industry. Verve operates in the USA, Canada, Bermuda, Cayman Islands and Barbados.

Date of investment: April 2023

Equity stake: 39.0%

31 January 2026 valuation: £860,000

Volt UW Limited

(www.volt-uw.com)

Volt is a London-based underwriting agency, specialising in energy insurance with a clear focus on insuring property risks associated with power generation and midstream energy in both the non-renewable and renewable sector.

Date of investment: October 2024

Equity stake: 25.5%

31 January 2026 valuation: £4,250,000

XPT Group LLC

(www.xptspecialty.com)

XPT is a wholesale insurance broking and Underwriting Agency platform across the U.S. Specialty Insurance Sector operating from many locations in the United States of America.

Date of investment: June 2017

Equity stake: 30.5%

31 January 2026 valuation: £64,030,000

XPT Producer Co LLC

XPT Producer Co is a US-based platform established to recruit and incubate specialist producers for XPT Group.

Date of investment: September 2025

Equity stake: 35.0%

31 January 2026 valuation: £2,565

These investments have been valued in accordance with the accounting policies on Investments set out in note 1 of the Consolidated Financial Statements.

Consolidated Financial Statements

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

FOR THE YEAR ENDED 31 JANUARY 2026

|

|

Notes |

2026 |

2025

|

||

|

|

|

£'000 |

£'000 |

£'000 |

£'000 |

|

|

|

|

|

|

|

|

GAINS ON INVESTMENTS |

|

|

|

|

|

|

Realised gains on disposal of equity investments (net of costs) |

15 |

19,651 |

|

17,292 |

|

|

Net provision (made) / released against equity investments and loans |

|

- |

|

(36) |

|

|

Unrealised gains on equity investment revaluation |

13 |

32,650 |

|

90,207 |

|

|

|

|

|

52,301 |

|

107,463 |

|

INCOME |

|

|

|

|

|

|

Dividends |

25 |

5,178 |

|

3,910 |

|

|

Income from loans and receivables |

25 |

2,997 |

|

2,342 |

|

|

Fees receivable |

25 |

2,223 |

|

1,524 |

|

|

|

|

|

10,398 |

|

7,776 |

|

|

|

|

|

|

|

|

OPERATING INCOME |

|

|

62,699 |

|

115,239 |

|

|

|

|

|

|

|

|

Operating expenses |

3 |

(14,790) |

|

(13,672) |

|

|

|

|

|

(14,790) |

|

(13,672) |

|

|

|

|

|

|

|

|

OPERATING PROFIT |

|

|

47,909 |

|

101,567 |

|

|

|

|

|

|

|

|

Financial income |

5 |

1,923 |

|

3,184 |

|

|

Financial expenses |

4 |

(97) |

|

(137) |

|

|

Exchange movements |

9 |

(737) |

|

79 |

|

|

|

|

|

1,089 |

|

3,126 |

|

|

|

|

|

|

|

|

PROFIT BEFORE TAXATION |

9 |

|

48,998 |

|

104,693 |

|

|

|

|

|

|

|

|

Income taxes |

10 |

|

(781) |

|

(5,194) |

|

|

|

|

|

|

|

|

PROFIT AFTER TAXATION ATTRIBUTABLE TO EQUITY HOLDERS |

|

|

48,217 |

|

99,499 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL COMPREHENSIVE INCOME FOR THE YEAR |

|

|

48,217 |

|

99,499 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Earnings per share - basic (pence) |

11 |

|

132.6p |

|

269.5p |

|

Earnings per share - diluted (pence) |

11 |

|

125.9p |

|

256.2p |

The result for the year is wholly attributable to continuing activities.

CONSOLIDATED AND PARENT COMPANY STATEMENTS OF FINANCIAL POSITION

31 JANUARY 2026

(Company Number: 05674962)

|

|

|

Group |

|

Company |

||

|

|

Notes |

2026 |

2025 |

|

2026 |

2025 |

|

|

|

£'000 |

£'000 |

|

£'000 |

£'000 |

|

ASSETS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NON-CURRENT ASSETS |

|

|

|

|

|

|

|

Property, plant and equipment |

12 |

296 |

84 |

|

- |

- |

|

Right-of-use asset |

21 |

177 |

342 |

|

- |

- |

|

Investments - equity portfolio |

13 |

273,766 |

224,095 |

|

- |

- |

|

Investments - subsidiaries |

13 |

- |

- |

|

360,220 |

326,482 |

|

Loans and receivables |

16 |

28,724 |

22,623 |

|

1,979 |

1,979 |

|

|

|

302,963 |

247,144 |

|

362,199 |

328,461 |

|

CURRENT ASSETS |

|

|

|

|

|

|

|

Trade and other receivables |

17 |

23,379 |

19,603 |

|

- |

- |

|

Cash and cash equivalents |

14 |

49,480 |

74,137 |

|

7 |

7 |

|

TOTAL CURRENT ASSETS |

|

72,859 |

93,740 |

|

7 |

7 |

|

TOTAL ASSETS |

|

375,822 |

340,884 |

|

362,206 |

328,468 |

|

|

|

|

|

|

|

|

|

LIABILITIES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NON-CURRENT LIABILITIES |

|

|

|

|

|

|

|

Lease liabilities |

21 |

(15) |

(218) |

|

- |

- |

|

Deferred tax liabilities |

18 |

(12,596) |

(11,847) |

|

- |

- |

|

TOTAL NON-CURRENT LIABILITIES |

|

(12,611) |

(12,065) |

|

- |

- |

|

|

|

|

|

|

|

|

|

CURRENT LIABILITIES |

|

|

|

|

|

|

|

Trade and other payables |

19 |

(2,850) |

(2,215) |

|

- |

- |

|

Lease liabilities |

21 |

(203) |

(194) |

|

- |

- |

|

TOTAL CURRENT LIABILITIES |

19 |

(3,053) |

(2,409) |

|

- |

- |

|

|

|

|

|

|

|

|

|

TOTAL LIABILITIES |

|

(15,664) |

(14,474) |

|

- |

- |

|

|

|

|

|

|

|

|

|

NET ASSETS |

|

360,158 |

326,410 |

|

362,206 |

328,468 |

|

|

|

|

|

|

|

|

|