Annual Report & Financial Statements

Summary by AI BETAClose X

28 May 2026

Alkemy Capital Investments Plc

Annual Report & Financial Statements

Alkemy Capital Investments plc ("Alkemy") (ALK:LSE) (JV2:FRA) is pleased to announce the publication of its audited Annual Report and Accounts for the year ended 31 January 2026 (the "Annual Report"). The Annual Report is available on the Company's website, www.alkemycapital.co.uk and is set out in full below.

Further information

For further information, please visit Alkemy's website: www.alkemycapital.co.uk or TVL's website www.teesvalleylithium.co.uk.

-Ends-

|

Alkemy Capital Investments Plc

|

Tel: 0207 317 0636 |

|

Zeus |

Tel: 0203 829 5000 |

Chairman's Statement

I have great pleasure in presenting our Annual Report for the year ended 31 January 2026.

Alkemy Capital Investments plc ("Alkemy") was formed to invest in the critical minerals sector. Our strategy is to finance and develop projects at the asset level through a combination of project-related debt, institutional equity, and strategic partnerships. As a holding company, our focus is on fostering the growth of our subsidiaries while upholding high standards of operational excellence, sustainability, and innovation.

Our principal asset, Tees Valley Lithium Limited ("TVL"), continued to make significant progress during the year as it advanced the development of the UK's flagship lithium refinery in Teesside. The project is being developed to produce battery-grade lithium hydroxide for the European electric vehicle and energy storage supply chain, supporting the broader industrial and critical minerals ambitions.

Over the course of the year, TVL achieved several important milestones across engineering, commercial development, project positioning, and strategic engagement. The company completed its Front End Engineering Design ("FEED") activities, further refining the project configuration, process integration, and site layout to optimise both capital efficiency and operational performance. During this process, TVL continued to strengthen its relationships with leading engineering, construction, and technology partners while advancing discussions across the supply chain to support future operations. The Board is particularly encouraged by the continued development of TVL's commercial framework. During the period, TVL entered into a binding offtake agreement with a wholly owned subsidiary of Glencore plc covering a significant proportion of the refinery's initial production capacity. The agreement represented an important milestone for the project, providing further validation of market interest in domestic European lithium refining capacity and supporting the continued development of TVL's long-term commercial strategy.

A major achievement during the year was the continued maturation of the project's infrastructure strategy and site development activities. TVL secured and progressed a strategically located site within the Teesside industrial cluster, providing access to existing infrastructure, utilities, logistics connectivity and an experienced industrial workforce. The Board believes the advantages of locating within an established chemical and industrial hub continue to differentiate the project relative to many competing European developments. The macroeconomic and geopolitical backdrop has continued to reinforce the strategic importance of domestic refining capacity. Across Europe, governments and industry increasingly recognise the need for resilient and diversified battery raw material supply chains amid ongoing concentration and evolving industrial policy. In the UK this has been reflected through the Government's Critical Minerals Strategy and ambitions to support approximately 50,000 tonnes per annum of domestic lithium chemical production capacity by the mid 2030s. Against this backdrop, TVL has continued to attract growing strategic interest as a large-scale UK lithium conversion project.

Looking ahead, the Board's focus remains on advancing TVL through construction and into commercial production. Key priorities over the coming year include financing workstreams, continued development of strategic supply and customer partnerships, finalisation of major project contracts and conclusion of planning activities. Whilst challenges remain in delivering projects of this scale and complexity, the Board believes Alkemy and TVL are well positioned to capitalise on the growing demand for strategically important battery materials infrastructure in Europe. We remain committed to developing a project that can play a meaningful role in supporting industrial growth, supply chain resilience and the energy transition.

On behalf of the Board, I would like to thank or employees, shareholders, advisers, and partners for their continued support during the year.

Paul Atherley

Non-Executive Chairman

27 May 2026

Strategic Report

The Directors present the Strategic Report of the Group for the year ended 31 January 2026.

Review of business and future developments

The Company was incorporated and registered in England and Wales on 21 January 2021 and on 27 September 2021 was admitted to the Standard Listing segment of the Official List of the UK Listing Authority and to trading on the London Stock Exchange.

In 2022 the Company incorporated wholly-owned subsidiary TVL with an objective to design, finance and construct a plant to produce lithium hydroxide monohydrate from lithium sulphate or carbonate feedstock, becoming a key supplier to the UK and European battery cell manufacturers (the "Project").

The principal activity of the Company is to act as the holding company to TVL, an operating subsidiary and the Company aims to implement an operating strategy with a view to generating value for its shareholders through the creation of the Project.

Key developments for the Group during the course of the financial year and following the year end included the following:

· In February 2025 the Company announced the appointment of Vikki Jeckell as CEO of TVL and the commencement of the FEED study.

· In March 2025 the Company announced that TVL had entered into an exclusive negotiation period with Touchstone Capital Partners to finalise a long-term binding feedstock agreement for over 100,000 tonnes of lithium carbonate equivalent. This agreement, if secured, would provide the primary lithium feedstock to fully support at least the first five years of production at TVL's refinery, producing 24,000 tonnes per annum of battery-grade lithium hydroxide. Alongside this, TVL's existing Heads of Terms with Wogen Resources Ltd remains an important element of its supply strategy, providing additional flexibility and continuity as TVL ramps up operations. Touchstone is fully financing the development of a high-grade lithium brine project and this combination of supply sources will ensure that TVL has a stable, long-term, and diversified feedstock position, reinforcing its potential to deliver a secure and sustainable lithium hydroxide supply chain for Europe's battery industry.

· In May 2025 the Company announced that it had entered into an exclusivity agreement with Ara Advisors LLC, a global private equity firm specialising in industrial decarbonisation, in connection with a proposed strategic investment in TVL.

· In June 2025 the Company announced that it has completed an oversubscribed subscription to raise £500,000.

· In July 2025 the Company announced that it had secured a £5m debt facility to provide funding for the FEED study and that a non-binding term sheet had been received from Ara Partners to lead the equity investment of the Project at the construction stage.

· In August 2025 the Company announced that TVL had appointed Gemma Cooper as its Chief Commercial Officer.

· In October 2025 the Company announced that TVL had appointed Richard Rose as its Chief Operating Officer.

· In November 2025 the Company announced that ABG Sundal Collier had been engaged to lead TVL's US$245m Bond and Equity Financing.

· In January 2026 the Company announced the signing of a binding offtake agreement with a wholly-owned subsidiary of Glencore plc for the supply of battery grade lithium hydroxide.

· In February 2026 the Company announced the completion of TVL's FEED Study.

· In February 2026 the Company announced the signing of heads of terms with Wates Construction Limited for a pre-construction services agreement.

Alkemy was formed to invest in the critical minerals sector. As a holding company its strategy is to foster the growth and expansion of its subsidiaries, steering them towards operational excellence and sustainable practices and to finance the development of these individual businesses at the asset level through project related debt, and institutional equity or strategic partnerships.

TVL is currently in discussions with a number of leading financial institutions and potential strategic partners for the financing of its Teesside refinery. The US$245m (approx. £178m) approximate capital cost of train 1 is expected to be financed with a mix of debt, strategic equity finance and grant funding, all at project level.

Having secured feedstock for its first train, a key component for these financing discussions, TVL's primary short term focus is to consummate discussions with leading financial institutions and strategic partners to obtain project-level funding that will enable it to reach a final investment decision for the project finance.

Key performance indicators

When the Group reaches a final investment decision for the project finance, financial, operational, health, safety, and environmental KPIs will become more relevant and reported upon as appropriate. As a result, the Directors are of the opinion that analysis using KPI's is not appropriate for an understanding of the business at this time.

Principal risks and uncertainties

The principal risks and uncertainties currently faced by the Group are set out further in the Risk Management Report.

Gender analysis

A split of the Directors, senior managers and employees by gender at the end of the financial year is as follows:

Male - 3 (2 directors)

Female - 2 (1 director)

The Group recognises the need to operate a gender diverse business. The Board will also ensure any future employment takes into account the diversity requirements and compliance with all employment law. The Board has experience and sufficient training and qualifications in dealing with such issues to ensure they would meet all requirements.

Corporate social responsibility

The Group aims to conduct its business with honesty, integrity and openness, respecting human rights and the interests of shareholders and employees. The Group aims to provide timely, regular and reliable information on the business to all its shareholders and conduct its operations to the highest standards.

The Group strives to create a safe and healthy working environment for the wellbeing of its staff and to create a trusting and respectful environment, where all members of staff are encouraged to feel responsible for the reputation and performance of the Group.

The Group aims to establish a diverse and dynamic workforce with team players who have the experience and knowledge of the business operations and markets in which we operate. Through maintaining good communications, members of staff are encouraged to realise the objectives of the Group and their own potential.

Corporate environmental responsibility

The Board contains personnel with a good history of running businesses that have been compliant with all relevant laws and regulations and there have been no instances of non-compliance in respect of environment matters.

The Group's policy is to minimize the risk of any adverse effect on the environment associated with its activities with a thoughtful consideration of key areas such as energy use, pollution, transport, renewable resources, health and wellbeing. The Group also aims to ensure that its suppliers and advisors meet with their legislative and regulatory requirements and that codes of best practice are met.

Section 172(1) Statement - Promotion of the Group for the benefit of the members as a whole

|

The Directors believe they have acted in the way most likely to promote the success of the Group for the benefit of its members as a whole, as required by s172 of the Companies Act 2006. |

The requirements of s172 are for the Directors to:

1. Consider the likely consequences of any decision in the long term,

2. Act fairly between the members of the Group,

3. Maintain a reputation for high standards of business conduct,

4. Consider the interests of the Group's employees,

5. Foster the Group's relationships with suppliers, customers and others, and

6. Consider the impact of the Group's operations on the community and the environment.

The pre-revenue nature of the business is important to the understanding of the Group by its members, employees and suppliers, and the Directors are as transparent about the cash position and funding requirements as is allowed under LSE regulations.

The application of the s172 requirements can be demonstrated in relation to some of the key decisions made during 2025 financial year and after the year end:

· The appointment of Vikki Jeckell as CEO of TVL and the commencement of the FEED study.

· The entering into of an exclusive negotiation period with Touchstone Capital Partners to finalise a long-term binding feedstock agreement for over 100,000 tonnes of lithium carbonate equivalent.

· The entering into of an exclusivity agreement with private equity firm Ara Advisors LLC in connection with a potential strategic investment in TVL.

· The completion an over subscribed subscription to raise £500,000.

· The securing of a £5m debt facility to provide funding for the FEED study and that a non-binding term sheet had been received from Ara Partners to lead the equity investment of the project at the construction stage.

· The appointment of Gemma Cooper as Chief Commercial Officer of TVL.

· The appointment of Richard Rose as Chief Operating Officer of TVL.

· The engagement of ABG Sundal Collier to lead TVL's US$245m Debt and Equity Financing.

· The signing of a binding offtake agreement with a wholly-owned subsidiary of Glencore plc for the supply of battery grade lithium hydroxide.

· The completion of TVL's FEED Study.

· The signing of heads of terms with Wates Construction Limited for a pre-construction services agreement.

The Board takes seriously its corporate social responsibilities to the environment in which it works which will become more relevant once the Project has reached the appropriate stage of development.

Paul Atherley

Non-Executive Chairman

27 May 2026

Board of Directors

Paul Atherley - Non-Executive Chairman

Paul Atherley is a highly experienced senior resources executive with wide ranging international and capital markets experience. He graduated as mining engineer from Imperial College London and has held a number of senior executive and board positions. Paul is currently Chairman of LSE listed Pensana Plc.

Paul is based in London and has broad experience in raising debt and equity finance for resource companies. He served as Executive Director of the investment banking arm of HSBC Australia where he undertook a range of advisory roles in the resources sector. He has completed a number of acquisitions and financings of resources projects in Europe, China, Australia and Asia.

Paul is a strong supporter of Women in STEM and has established a scholarship which provides funding for young women to further their education in science and engineering.

Sam Quinn - Non-Executive Director

Sam Quinn is a corporate lawyer with over 20 years' worth of experience in the natural resources sector, in both legal counsel and management positions. Sam is a principal of Silvertree Partners, a London-based specialist corporate services provider for the natural resources industry. In addition Sam holds various other Non-Executive Directorships and company secretarial roles for listed and unlisted natural resources companies. During time spent in these roles, Sam has gained significant experience in the administration, operation, financing and promotion of natural resource companies.

Previously, Sam worked as the Director of Corporate Finance and Legal Counsel for the Dragon Group, a London based natural resources venture capital firm and as a corporate lawyer for Jackson McDonald Barristers & Solicitors in Perth, Western Australia and for Nabarro LLP in London.

Helen Pein - Non-Executive Director

Helen Pein has over 35 years' experience in the natural resources sector and currently serves as a Director of Pan Iberia Ltd, Trident Royalties Plc and Panex Resources Pty Ltd.

Helen is the current CEO of Goldrange Resources, a private company focused on gold exploration in Africa. She was previously a Director at Pangea Exploration Pty Ltd, a company affiliated with Denham Capital, where she was part of the team responsible for discovering several world-class gold and mineral sands deposits across Africa. Helen has also served as a technical advisor to various listed and private resource companies, and as a Non-Executive Director of a US-based SPAC. She is a recipient of the Gencor Geology Award.

Directors' Report

The Directors present their annual report together with the financial statements and Auditor's Report for the year ended 31 January 2026. The following information is not presented in the Directors' report as it is presented in the Strategic Report in accordance with s414C(11); Review of business, Key Performance Indicators, Principal risks and uncertainties, Gender analysis, Corporate social responsibility, Corporate environmental responsibility, Section 172(1) statement. Director's remuneration is detailed in the Directors' Remuneration Report.

Results and dividends

The results of the Group for the year ended 31 January 2026 are set out in the Statement of Comprehensive Income. The Directors do not recommend the payment of a dividend for the year.

Directors and Directors' interests

The Directors who served during the year to date are as follows:

Paul Atherley

Sam Quinn

Helen Pein

Vikki Jeckell (resigned 10 November 2025)

The beneficial shareholdings of the Board in the Company as at 31 January 2026 were as follows:

|

|

Number of ordinary shares |

% of issued share capital |

Share options |

|

|

|

|

|

|

P Atherley |

3,547,226 |

33.05% |

400,000 |

|

S Quinn |

533,095 |

4.97% |

365,000 |

|

H Pein |

40,142 |

0.37% |

100,000 |

Director incentives

Details on Directors remuneration can be found in the Directors' Remuneration Report.

Substantial shareholders

As at the date of this Report, the total number of issued Ordinary Shares with voting rights in the Company was 10,976,625. The Company has been notified of the following interests of 3 per cent or more in its issued share capital as at the date of this report.

|

Shareholder |

Number of ordinary shares |

% of issued share capital |

|

Paul Atherley |

3,547,226 |

32.32% |

|

Sam Quinn |

533,095 |

4.86% |

Corporate governance

The Group has set out its full Corporate Governance Statement on pages 21-22. The Corporate Governance Statement forms part of this Directors' Report and is incorporated into it by cross reference.

Greenhouse gas disclosures

As the Group remains in the early stages of development without any current physical operations across its portfolio of projects, it is not practical to obtain and analyse emissions data for the Group operations. However, given the minor level of physical operations in the year, and the lack of any plant or office space, the carbon footprint and climate change impact of the Group's operations are considered to be negligible, and in any event below the 40 MWh threshold prescribed for detailed emissions disclosures.

As such, the Group does not consider it relevant to provide climate related disclosures under TCFD guidelines, nor would determination of the relevant emissions data be practical. Once the Group has commenced the construction of physical premises across any of its projects, and hence transitioned into an operating company, it will revisit its position on climate disclosures accordingly and in the meantime will continue to monitor climate related risks at a strategic level.

Supplier payment policy

The Group's current policy concerning the payment of trade payables is to follow the CBI's Prompt Payers Code (copies are available from the CBI, Centre Point, 103 New Oxford Street, London WC1A 1DU).

The Group's current policy concerning the payment of trade payables is to:

· settle the terms of payment with suppliers when agreeing the terms of each transaction;

· ensure that suppliers are made aware of the terms of payment by inclusion of the relevant terms in contracts; and

· pay in accordance with the Group's contractual and other legal obligations.

Financial instruments and risk management

The Group is exposed to a variety of financial risks and the impact on the Group's financial instruments are summarised in the Risk Management Report. Details of the Group's financial instruments are disclosed in notes to the financial statements.

Directors' insurance

The Group has implemented Directors and Officers Liability Indemnity Insurance.

Events after the reporting year

On 3 February 2026 the Company announced the completion of its FEED study for the lithium processing plant in Teesside, England. The FEED study included a revision to the assessed project economics including total capex estimate of US$244m and post completion EBITDA estimates of US$66m per annum based on 25,000 tpa of production.

On 4 February 2026 the Company issued 70,446 ordinary shares of 2p through conversion of debt at a price of £3.48 per share.

On 5 February 2026 the Company announced the allotment of 685,000 long term incentivisation share awards to directors and senior management of the Company and its subsidiary TVL. Pricing of the share awards based on a 30 day VWAP was £3.59 per share with the awards being as follows:

|

Director/Senior Management |

Position |

Number of New Share Awards Granted |

|

Paul Atherley |

Chairman |

175,000 |

|

Sam Quinn |

Director |

175,000 |

|

Helen Pein |

Director |

30,000 |

|

Vikki Jeckell |

CEO, TVL |

175,000 |

|

TVL Senior Management |

|

130,000 |

On 12 February 2026 the Company announced it had entered into an agreement with Watercycle Technologies and Circulor UK Limited to advance the integration of on-site lithium recovery using deployed UK technology, with the potential to unlock up to c.US$16 million per annum of otherwise lost lithium value. They also establish a framework for up to 50,000 tonnes of additional recycled lithium feedstock and embed digital tracking capability at a batch level. Together these measures strengthen project economics, increase access to recycled feedstock and ensure future UK and EU Battery Regulatory compliance as TVL progresses toward construction.

On 24 February 2026 the Company announced it had entered into a heads of terms with Wates Construction Limited for Pre Construction Services to progress pre-construction activities, bringing in relevant local industrial, construction and MEP experience from its Construction and SES divisions and strengthens the Project's readiness as it transitions into execution.

On 27 February 2026 the Company announced the conversion of £500,000 of debt into 143,587 new ordinary shares at a conversion price of £3.48 per share.

On 19 March 2026 the Company announced the allotment of 100,000 new ordinary shares to Wave International at a price of £3.97 per share in connection with engineering and project development services provided to the Company, while at the same time issuing 61,004 warrants for new shares with an exercise price of £6.15 per share and exercisability period of 48 months.

On 24 April 2026 the Company provided an update on its Teesside project progress, including the entering into of an MOU with Buxton Lime for the provision of long term quicklime supply and the completion of ecological studies at its Billingham site where no adverse findings were reported.

Going concern

As part of their assessment of going concern, the Directors have prepared cash forecasts to determine the funding requirements of the business over the 18 months from the reporting date. Cash requirements over this period have been projected in the range of a £3m minimum (decelerated project development case) to £4.2m + (accelerated project development case) depending on the level of technical project development work being undertaken, as determined by funding availability. These cashflows have been prepared on a "pre - project finance / FID" basis and assumes the Company will continue to develop the Project over this period without moving to FID. Should the Company be in a position to secure project financing and undertake FID in this period then the funding requirements will be substantially greater, as met by project finance and other funding availability forming part of the investment decision.

As at the date of this report, the Directors are considering a variety of funding options from numerous parties to consider the option best suited to balancing the immediate cash flow needs of the business and desire to accelerate the project development timeframe against the need to avoid unnecessary dilution of the shareholders during a period of depressed equity market prices. Options ranging from:

· project level debt or strategic equity which would provide sufficient funding to accelerate the project development program over the period of consideration, including general working capital requirements;

· market equity placings to secure working capital funding needs whilst project development funding opportunities continue to be assessed;

· convertible and term loan lending facilities which may act as a hybrid of working capital and project development funding, allowing progression of project development at a less accelerated rate that would be the case under a more substantial project lending facility;

· any combination of the above.

The Board remains in detailed discussions on the above funding opportunities and anticipates concluding this process in the medium term. The Directors are therefore reasonably confident that the necessary funding will be secured, as and when required, by executing on one of the above options under consideration, such that the Directors have a reasonable expectation that the Group will continue in operational existence for the next 12 months. However as successful execution of one of the above fundraising options cannot be assured, a material uncertainty exists which may cast significant doubt on the ability of the Company and Group to continue as a going concern and realise its assets and discharge its liabilities in the normal course of business.

Accordingly, the Directors believe that as at the date of this report it is appropriate to continue to adopt the going concern basis in preparing the financial statements.

Disclosure of information to Auditor

The Directors confirm that:

· So far as each Director is aware, there is no relevant audit information of which the company's auditor is unaware; and

· The Directors have taken all steps that they ought to have taken as Directors in order to make themselves aware of any relevant audit information and to establish that the auditor is aware of that information.

Auditor

A resolution proposing the re-appointment of Crowe U.K. LLP as auditor will be put to shareholders at the Annual General Meeting.

This Directors' Report has been approved by the Board and signed on its behalf by:

Paul Atherley

Non-Executive Chairman

27 May 2026

Directors' Remuneration Report

The Board periodically reviews the quantum of Directors' fees, taking into account the interests of shareholders and the performance of the Company and the Directors.

The Directors who held office at 31 January 2026 are summarised as follows:

|

Name of Director |

Position |

|

P Atherley |

Non-Executive Chairman |

|

S Quinn |

Non-Executive Director |

|

H Pein |

Non-Executive Director |

Directors' Letters of appointment

Letter of Appointment - Paul Atherley

Pursuant to a letter of appointment dated 21 September 2021 between the Company and Mr Atherley, Mr Atherley is engaged as Chairman with fees of £24,000 per annum. The appointment can be terminated by either party on three months written notice.

Letter of Appointment - Sam Quinn

Pursuant to a letter of appointment dated 21 September 2021 between the Company and Sam Quinn, Mr Quinn is engaged as a Non-Executive Director with fees of £18,000 per annum. In addition Sam Quinn will be remunerated for additional work performed for the Company which is outside the scope of his service agreements, including consultancy and management services, at a rate of £1,000 per day subject to a maximum of 3 days per calendar month. The appointment can be terminated by either party on three months written notice.

Letter of Appointment - Helen Pein

Pursuant to a letter of appointment dated 21 September 2021 between the Company and Helen Pein, Helen is engaged as a Non-Executive Director with fees of £18,000 per annum. In addition Helen Pein will be remunerated for additional work performed for the Company which is outside the scope of her service agreements, including project due diligence, consultancy and management services at a rate of £1,000 per day subject to a maximum of 3 days per calendar month. The appointment can be terminated by either party on three months written notice.

Consultancies

Pursuant to a consultancy agreement between the Group and Selection Capital Investments Limited, Paul Atherley is engaged as Key Personnel (as defined under the consultancy agreement) contracted to provide services to the Group in consideration of payment of £7,000 per month.

Pursuant to a consultancy agreement dated 1 October 2021 between the Company and Lionshead Consultants Limited ("Lionshead"), a company of which Sam Quinn is a director and sole shareholder, Lionshead is contracted to provide services to the Company in consideration of payment of £5,000 per month.

Terms of appointment

The services of the Directors are provided under the terms of letters of appointments, as follows:

|

Director |

|

Year of appointment |

Number of periods completed |

Date of current engagement letter |

|

|

|

|

|

|

|

P Atherley |

|

2021 |

5 |

21 September 2021 |

|

S Quinn |

|

2021 |

5 |

21 September 2021 |

|

H Pein |

|

2021 |

5 |

21 September 2021 |

Consideration of shareholder views

The Board considers shareholder feedback received. This feedback, plus any additional feedback received from time to time, is considered as part of the Group's annual policy on remuneration.

Policy for salary reviews

The Group may from time to time seek to review salary levels of Directors, taking into account performance, time spent in the role and market data for the relevant role. It is intended that there will be a salary review during the next year as the Company achieves key milestones.

Policy for new appointments

It is not intended that there will be any new appointments to the Board in the near term. It is intended however that a review of the Board will take place on the achievement of key milestones including funding and project development.

Directors' emoluments and compensation (audited)

Remuneration attributed to the Directors' during the year ended 31 January 2026 was as follows (all figures are stated in GBP):

Year Ended 31 January 2026:

|

Director |

|

Directors fees |

Salary/Consulting fees |

Total remuneration |

|

|

|

|

|

|

|

P Atherley |

|

£48,000 |

£138,209 |

£186,209 |

|

|

|

|

|

|

|

S Quinn |

|

£36,000 |

£68,811 |

£104,811 |

|

|

|

|

|

|

|

H Pein |

|

£18,000 |

- |

£18,000 |

|

|

|

|

|

|

|

V Jeckell |

|

£202,279 |

£145,000 |

£347,279 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

£304,279 |

£352,020 |

£656,299 |

Year Ended 31 January 2025:

|

Director |

|

Directors fees |

Salary/Consulting fees |

Total remuneration |

|

|

|

|

|

|

|

P Atherley |

|

57,274 |

108,500 |

165,774 |

|

|

|

|

|

|

|

S Quinn |

|

45,274 |

60,000 |

105,274 |

|

|

|

|

|

|

|

H Pein |

|

18,000 |

- |

18,000 |

|

|

|

|

|

|

|

V Jeckell |

|

36,000 |

240,000 |

276,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

156,548 |

408,500 |

565,048 |

Director incentives

In the year ended 31 January 2026, no options were granted to Directors (2025: 475,000). As at 31 January 2026, 865,000 (2025: 1,190,000) options issued to Directors were outstanding.

On 5 February 2026, 380,000 Share Awards were granted to Directors which are subject to the satisfaction of certain performance conditions to be interpreted at the discretion of the Board over a three year review period.

Directors' Remuneration Policy

Pursuant to the Directors' letters of appointment, as described above, the Directors receive fees, all payable monthly in arrears. There is currently a long-term incentive plan in operation for the Directors by way of share incentive options.

Based on the foregoing, the remuneration policy of the Group can be summarised as follows:

|

How the element supports our strategic objectives |

Operation of the element |

Maximum potential payout and payment at threshold |

Performance measures used, weighting and time period applicable |

|

|

|

|

|

|

Base Pay |

|

|

|

|

Recognises the role and the responsibility for the delivery of strategy and results |

Paid in 12 monthly instalments |

Contractual sum |

None |

|

|

|

|

|

|

Pensions |

|

|

|

|

None |

n/a |

n/a |

n/a |

|

|

|

|

|

|

Short term incentives |

|

|

|

|

None |

n/a |

n/a |

n/a |

|

|

|

|

|

|

Long term incentives |

|

|

|

|

Aligns directors and shareholders in share price and project development |

Share options issued |

n/a - employee exercises at cost and accesses long term capital gain |

Vesting conditions include: · completion of fund raising to fund the FEED study; · completion of the fund raising to fund construction of the first 24,000 tpa capacity at the Project; · following commissioning of the first 24,000 tpa capacity at the Project. |

|

|

Share Awards |

n/a - shares issued at nil cost, quantum and effective value determined at time of each award |

Subject to the satisfaction of certain performance conditions to be interpreted at the discretion of the Alkemy Board over a three year review period. Upon vesting, no consideration is payable. Subject to vesting and such performance conditions being met, the new Share Awards will be allocated to the participant as fully paid ordinary shares, subject to any regulatory restrictions. |

A remuneration committee is expected to be appointed in due course to consider an appropriate level of Directors' remuneration.

Although there is no formal Director shareholding policy in place, the Board believe that share ownership by Directors strengthens the link between their personal interests and those of shareholders.

The Group does not currently operate malus or clawback provisions in respect of Directors' remuneraton.

No views were expressed by shareholders during the year on the remuneration policy of the Group.

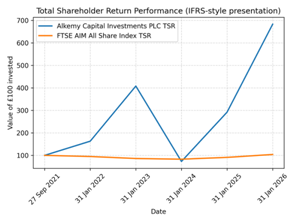

Total Shareholder Return Performance

The following graph illustrates the Company's Total Shareholder Return ("TSR") performance over the period from 27 September 2021 to 31 January 2026, compared with the FTSE AIM All Share Index. TSR is calculated on a £100 notional investment made at the commencement of the performance period and assumes reinvestment of dividends however this is not applicable in the below.

This measure has been selected as it provides a market-based assessment of shareholder value creation over time and is widely used within listed company remuneration frameworks under UK corporate governance best practice.

Over the period, the Company's TSR demonstrates significant volatility, reflecting both the development stage of the Group and broader market conditions affecting AIM-listed companies. The TSR increased materially during the earlier part of the measurement period, followed by a period of contraction, before recovering strongly in the most recent period end.

Given the Company's size, market capitalisation and nature of operations, the Directors consider the FTSE AIM All-Share Index to be the most appropriate comparative index for the TSR analysis, as it provides a more relevant peer group than broader market indices.

While TSR is an important indicator of shareholder value creation, it is considered alongside other financial and strategic performance measures within the overall assessment of executive remuneration outcomes. The Committee recognises that TSR may not fully capture underlying operational performance in the short to medium term, particularly for companies in investment and development phases.

Other matters

The Group does not currently have any short-term incentive schemes in place for any of the Directors.

The Group does not have any pension plans for any of the Directors and does not pay pension amounts in relation to their remuneration.

This Directors' Remuneration Report has been approved by the Board and signed on its behalf by:

Paul Atherley

Non-Executive Chairman

27 May 2026

Risk Management Report

The Company has undertaken an evaluation of the risks it is exposed to which are summarised as follows:

There is no assurance that the Group will determine that the Project is economically viable

The success of the Group's business strategy is dependent on its ability to identify sufficient suitable acquisition opportunities. Whist the Group believes that the Project presents a good opportunity, it is still in the process of evaluating such opportunity. If the Group fails to complete the development of the Project it may be left with substantial unrecovered transaction costs, potentially including fees, legal costs, accounting costs, due diligence or other expenses. Furthermore, even if an agreement is reached relating to the Project, the Group may fail to complete the Project for reasons beyond its control. Any such event will result in a loss to the Group of the related costs incurred, which could materially adversely affect subsequent attempts to identify and acquire another target business.

Development and production activities are capital intensive and inherently uncertain in their outcome and the Group may not make a return on its investments, recover its costs or generate cash flows

The construction of industrial facilities are capital intensive. In addition, environmental damage could greatly increase the cost of operations, and various operating conditions may adversely and materially affect the levels of production. These conditions include delays in obtaining governmental approvals or consents, insufficient storage or transportation capacity or a change in demand for the product. While diligent supervision and effective maintenance operations can contribute to maximising production rates over time, production delays and declines from normal operations cannot be eliminated and may adversely and materially affect the revenues, cash flow, business, results of operations and financial resources and condition of the Group.

Currently the Group has insufficient capital to meet the funding requirements for the development of the Project

The Group will need to raise additional funding in the near term to meet its working capital requirements for the next twelve months. In addition to working capital needs, the Group is of the opinion that if it decides to proceed with the Project, the Group does not have sufficient capital in order to complete the construction of the Project and hence will be required to raise additional funds in support of project development expenditure requirements.

Based on the results of the FEED Study, the Directors anticipate that a total of approximately US$245 million (excluding financing costs) of additional debt/equity financing will be required and subject to the Group's confirmation to proceed with the Project to fund the evaluation, development and construction of the Project. The Group intends to raise the development costs of the Project by:

(a) Debt finance - Any debt finance in respect of the Group for the purposes of developing and completing the Project, is likely to be subject to customary conditions precedent. As of the date of this document, the Group is in the process of seeking third party debt financing in respect of the Project.

(b) Equity finance - In relation to any equity financing, the Group expects to engage advisors to assist the Group with its equity funding requirements. The Group has begun the process of seeking formal engagement with advisors for debt/equity financing in respect of the Project.

Based on the Group's informal discussions with potential debt and equity providers to date, the Directors are confident that within the period of twelve months following the date of this document the Group will be able to secure all the necessary finance required to develop and complete the Project.

The failure to secure additional financing or to secure such additional financing on terms acceptable to the Group could have a material adverse effect on the continued development or growth of the acquired business, prospects, and the financial condition and results and operations of the Group and could, ultimately lead to the insolvency of the Company or Group.

The price of lithium hydroxide is affected by factors beyond the Group's control

If the Group proceeds with the Project, and the market price of lithium hydroxide decreases significantly for an extended period of time, the ability for the Group to attract finance and ultimately generate profits could be adversely affected. Numerous external factors and industry factors that are beyond the control of the Group that affect the price of lithium hydroxide include:

· industrial demand;

· levels of production;

· rapid short term changes in supply and demand because of speculative or hedging activities; and

· global or regional political or economic events.

The price at which the Group can sell any lithium hydroxide it may produce in the future will therefore be relevant to the future revenues that can be generated by the Group and its ability to finance the Company going forward and any adverse effects on such price could have a material adverse effect on the Group's business, financial performance, results of operations and prospects.

The Group may be unable to hire or retain personnel required to support the Group going forward

The Group's ability to compete depends upon its ability to retain and attract highly qualified management and technical personnel. Following completion of the Project, the Group will evaluate the personnel of the acquired business and may determine that it requires increased support to operate and manage the acquired business in accordance with the Group's overall business strategy. There can be no assurance that existing personnel of the acquired business will be adequate or qualified to carry out the Group's strategy, or that the Group will be able to hire or retain experienced, qualified employees to carry out the Group's strategy.

During the development of the Project, the Group may be unable to acquire or renew necessary concessions, licenses, permits and other authorisations

The Project will require certain concessions, licences, permits and other authorisations to carry out its operations. Any delay in obtaining or renewing a license, permit or other authorisation may result in a delay in investment or development of a resource and may have a materially adverse effect on the acquired business' results of operations, cash flows and financial condition. In addition, any concessions, licences, permits and other authorisations of the Project may be suspended, terminated or revoked if it fails to comply with the relevant requirements.

Failure to obtain (and shortages and disruptions in lead times to deliver) certain key inputs may adversely affect the Group's operations during the development of the Project

During the development of the Project, the Group's inability to timely acquire feedstock, strategic consumables, raw materials, and processing equipment could have an adverse impact on any results of operations and financial condition. Periods of high demand for supplies can arise when availability of supplies is limited. This can cause costs to increase above normal inflation rates. Interruption to supplies or increase in costs could adversely affect the operating results and cash flows of the Group during the development of the Project.

This Risk Management Report has been approved by the Board and signed on its behalf by:

Paul Atherley

Non-Executive Chairman

27 May 2026

Corporate Governance Statement

The Group observes the requirements of the Quoted Company Alliance corporate governance code (the "QCA Code") and applies the QCA Code's ten principles as set out below.

· Strategy: The principal activity of the Company is to act as the holding company to TVL, an operating subsidiary and the Company aims to implement an operating strategy with a view to generating value for its shareholders through the creation of the Project. Further details of the Group's strategy are set out in the Strategic Report.

· Corporate Culture: The Group and Board is committed to promoting a corporate culture that is based on ethical values and behaviours. The Group has adopted and abides by a share dealing code that complies with the requirements of the Market Abuse Regulations. All persons discharging management responsibilities (comprising only the Directors) comply with the share dealing code.

· Shareholders: The Group keeps its shareholders informed by giving regular updates on developments via RNS announcements, and through Company interviews and meetings, both informal and formal. The Group also engages with shareholders and prospective investors at the Annual General Meeting and other General meetings and various physical and virtual presentations.

· Stakeholders: The Group recognises its duties to all of its stakeholders including its employees, consultants, business partners, contractors, suppliers, service providers and regulators and strives at all times to meet stakeholder needs and expectation and to deal with them in a fair and professional manner. Further details of key stakeholders are set out in the s172 disclosures in the Strategic Report.

· Risk: The Group continues to build an effective risk management framework, which identifies the risks to which the Group has been or could be exposed. Further details of risks facing the Group and its responses are set out in the Risk Management Report.

· Board: The Group has a Board it believes is well suited for the purposes of implementing its business strategy, combining skill sets for the assessment of investment and acquisition of royalties and streams in the mining sector. The Directors are responsible for carrying out the Group's objectives, implementing its business strategy and conducting its overall supervision. Acquisition, divestment and other strategic decisions will all be considered and determined by the Board. The Board will provide leadership within a framework of prudent and effective controls. The Board will establish the corporate governance values of the Group and will have overall responsibility for setting the Group's strategic aims, defining the business plan and strategy and managing the financial and operational resources of the Group. The Board aims to hold meetings on a quarterly basis and is regularly in contact to discuss prospective acquisition opportunities. The Articles of the Company contain express provisions relating to conflicts of interest in line with the Companies Act 2006. Given the composition of the Board, certain provisions of the QCA Code are considered by the Board to be inapplicable to the Company. Specifically, the Company does not consider it necessary to have a senior independent Director and the Board will, at the outset, consist of two non-executive Directors and one non-executive chairman. The QCA Code also recommends the submission of Directors for re-election at annual intervals. The Company Articles of Association require all directors to retire by rotation and seek reappointment by the shareholders at a general meeting every two years.

· Corporate governance and structures: The Group does not have nomination, remuneration, audit or risk committees. The Board as a whole will instead review its size, structure and composition, the scale and structure of the Directors' fees (taking into account the interests of shareholders and the performance of the Group), take responsibility for the appointment of auditors and payment of their audit fee, monitor and review the integrity of the Group's financial statements and take responsibility for any formal announcements on the Group's financial performance. The Board intends to put in place nomination, remuneration, audit and risk committees in due course.

· Remuneration Policy: The Group's remuneration policy is set out in the Directors' Remuneration Report.

· Shareholder and stakeholder communications: The Group uses its corporate website (www.alkemycapital.co.uk) to ensure that the latest announcements, press releases and published financial information are available to all shareholders and other interested parties. The AGM is used to communicate with both institutional shareholders and private investors and all shareholders are encouraged to participate. Separate resolutions are proposed on each issue so that they can be given proper consideration and there is a resolution to approve the Annual Report and Accounts. Notice of the AGM is sent to shareholders at least 21 days before the meeting and the results are announced to the London Stock Exchange and are published on the Company's website.

Paul Atherley

Non-Executive Chairman

27 May 2026

Directors' Responsibility Statement

The Directors are responsible for preparing the Annual Report and the Financial Statements in accordance with applicable law and regulations.

Company law requires the Directors to prepare Financial Statements for each financial year. Under that law the Directors have elected to prepare the financial statements in accordance with UK Adopted International Accounting Standards ("IAS"). Under company law the Directors must not approve the financial statements unless they are satisfied that they give a true and fair view of the state of affairs of the Group and of the profit or loss for that period.

In preparing these financial statements, the Directors are required to:

1. select suitable accounting policies and then apply them consistently;

2. make judgements and accounting estimates that are reasonable and prudent;

3. state whether applicable UK-adopted IAS have been followed, subject to any material departures disclosed and explained in the financial statements; and

4. prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Company and Group will continue in business.

The Directors are responsible for keeping adequate accounting records that are sufficient to show and explain the Company and Group's transactions and disclose with reasonable accuracy at any time the financial position of the Company and Group and enable them to ensure that the Financial Statements and the Directors Remuneration Report comply with the Companies Act 2006. They are also responsible for safeguarding the assets of the Company and Group, and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

They are also responsible to make a statement that they consider that the Annual Report and Financial Statements, taken as a whole, is fair, balanced, and understandable and provides the information necessary for the shareholders to assess the Group's position and performance, business model and strategy.

The Directors are responsible for the maintenance and integrity of the corporate and financial information included on the Company's website. Legislation in the United Kingdom. governing the preparation and dissemination of the Financial Statements may differ from legislation in other jurisdictions.

Directors' responsibility statement pursuant to disclosure and Transparency Rule

Each of the Directors, whose names and functions are listed within the Board of Directors confirm that, to the best of their knowledge:

1. the financial statements are prepared in accordance with UK-adopted IAS give a true and fair view of the assets, liabilities, financial position and loss of the Company and Group; and

2. the Annual Report and financial statements, including the Strategic Report, includes a fair review of the development and performance of the business and the position of the Company and Group, together with a description of the principal risks and uncertainties that they face.

Approved by the Board on 27 May 2026.

Paul Atherley

Non-Executive Chairman

Independent auditor's report to the members of Alkemy Capital Investments Plc

Opinion

In our opinion, the financial statements:

· give a true and fair view of the state of the group's and of the company's affairs as at 31 January 2026 and of the group's loss for the year then ended;

· have been properly prepared in accordance with UK-adopted international accounting standards; and

· have been prepared in accordance with the requirements of the Companies Act 2006.

Basis for opinion

We conducted our audit in accordance with International Standards on Auditing (UK) (ISAs (UK)) and applicable law. Our responsibilities under those standards are further described in the Auditor's responsibilities for the audit of the financial statements section of our report. We are independent of the group and the company in accordance with the ethical requirements that are relevant to our audit of the financial statements in the UK, including the FRC's Ethical Standard as applied to listed public interest entities, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Material uncertainty related to going concern

We draw attention to the section headed 'Going Concern' in note 2 to the financial statements, which details the factors the group has considered when assessing its going concern position. As stated in note 2, the uncertainty surrounding the availability of funds to finance the commercial development of the group's projects indicates that a material uncertainty exists that may cast significant doubt on the group's and company's ability to continue as a going concern. Our opinion is not modified in respect of this matter.

In auditing the financial statements, we have concluded that the directors' use of the going concern basis of accounting in the preparation of the financial statements is appropriate. Our evaluation of the directors' assessment of the group's and company's ability to continue to adopt the going concern basis of accounting included:

· discussions with management in relation to the future plans of the group and company;

· checking activity after the year end to the date of signing of the financial statements;

· challenging the directors' going concern assessment including the worst-case scenario cashflow forecasts that covers at least 12 months from the date of approval of the financial statements;

· evaluating the reliability of the data underpinning the cashflow forecasts, including checking the numerical accuracy of the model and agreeing opening positions used;

· assessing the cashflow requirements of the group based on forecasted capital and administrative expenditures;

· checking what forecast expenditure is committed and what could be discretionary;

· considering the options available to management for further fundraising or additional sources of finance;

· assessing the likelihood of receipt of fundraising;

· challenging potential downside scenarios and the resulting impact on funding requirements and the group's ability to raise such funds; and

· assessing the completeness and accuracy of the disclosures made on going concern in the annual report and financial statements.

Our responsibilities and the responsibilities of the directors with respect to going concern are described in the relevant sections of this report.

Overview of our audit approach

Materiality

In planning and performing our audit we applied the concept of materiality. An item is considered material if it could reasonably be expected to change the economic decisions of a user of the financial statements. We used the concept of materiality to both focus our testing and to evaluate the impact of misstatements identified.

Based on our professional judgement, we determined overall materiality for the financial statements as a whole to be £122,000 (2025: £60,000), based on 5% of loss before taxation. Materiality for the parent company financial statements as a whole was set at £49,500 (2025: £35,000) based on 5% of loss before taxation.

We use a different level of materiality ('performance materiality') to determine the extent of our testing for the audit of the financial statements. Performance materiality is set based on the audit materiality as adjusted for the judgements made as to the entity risk and our evaluation of the specific risk of each audit area having regard to the internal control environment. Performance materiality was set at 70% of materiality for the financial statements as a whole, which equates to £85,400 (2025: £42,000) for the group and £34,500 (2025: £25,500) for the parent.

Where considered appropriate performance materiality may be reduced to a lower level, such as, for related party transactions and directors' remuneration.

We agreed with the Board to report to it all identified errors in excess of £6,100 (2025: £3,000). Errors below that threshold would also be reported to it if, in our opinion as auditor, disclosure was required on qualitative grounds.

Overview of the scope of our audit

Our audit was scoped by obtaining an understanding of the group and its environment, including the group's system of internal control, and assessing the risks of material misstatement in the financial statements. We also addressed the risk of management override of internal controls, including assessing whether there was evidence of bias by the directors that may have represented a risk of material misstatement.

In establishing our overall approach to the group audit, we determined the type of work that needed to be undertaken at each of the components. The base of operations is in the United Kingdom, which is where the head office is. The parent company and its principal operating subsidiary, Tees Valley Lithium Limited, were subject to full scope audit. The consolidation was also subject to a full scope audit. This, together with the additional procedures performed at the group level, such as performing limited scope procedures for non-UK components, gave us appropriate and sufficient audit evident to support our opinion on the group financial statements. All audit work was undertaken by the group audit team.

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the financial statements of the current period and include the most significant assessed risks of material misstatement (whether or not due to fraud) we identified, including those which had the greatest effect on the overall audit strategy, the allocation of resources in the audit; and directing the efforts of the engagement team. These matters were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

We set out below, together with the material uncertainty related to going concern above, those matters we considered to be key audit matters. This is not a complete list of all risks identified by our audit.

|

Key audit matter |

How our scope addressed the key audit matter |

|

Capitalisation of intangible assets The group continues to invest in the planned construction of its lithium hydroxide processing facility in Teesside, UK. Determining whether the cost of development meets the capitalisation criteria requires management to make significant judgement based on the requirements of IAS 38. We therefore consider the inappropriate capitalisation of development costs to be a key audit matter. Refer to notes 2 and 10.

|

We performed the following procedures as part of our audit: · Obtained an understanding of the process and key controls relating to the capitalisation of development costs. · Tested, on a sample basis, capitalised development costs to source documentation such as third-party invoices and assessed whether these meet the criteria for capitalisation. · Challenged management on the reasonableness of the key judgements in the capitalisation of development costs including assessment of technical feasibility of the project, funding to complete the development and expectation of future economic benefits. · Assessed the completeness and accuracy of the disclosures included in the financial statements. Based on the work performed, we concluded that the development costs capitalised is reasonable. |

Our audit procedures in relation to these matters were designed in the context of our audit opinion as a whole. They were not designed to enable us to express an opinion on these matters individually and we express no such opinion.

Other information

The other information comprises the information included in the annual report other than the financial statements and our auditor's report thereon. The directors are responsible for the other information contained within the annual report.

Our opinion on the financial statements does not cover the other information and, except to the extent otherwise explicitly stated in our report, we do not express any form of assurance conclusion thereon. Our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the course of the audit, or otherwise appears to be materially misstated. If we identify such material inconsistencies or apparent material misstatements, we are required to determine whether this gives rise to a material misstatement in the financial statements themselves. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact.

We have nothing to report in this regard.

Opinions on other matters prescribed by the Companies Act 2006

In our opinion the part of the directors' remuneration report to be audited has been properly prepared in accordance with the Companies Act 2006.

In our opinion based on the work undertaken in the course of our audit:

· the information given in the strategic report and the directors' report for the financial year for which the financial statements are prepared is consistent with the financial statements; and

· the strategic report and directors' report have been prepared in accordance with applicable legal requirements.

Matters on which we are required to report by exception

In the light of the knowledge and understanding of the group and the parent company and their environment obtained in the course of the audit, we have not identified material misstatements in the strategic report or the directors' report.

We have nothing to report in respect of the following matters in relation to which the Companies Act 2006 requires us to report to you if, in our opinion:

· adequate accounting records have not been kept by the company, or returns adequate for our audit have not been received from branches not visited by us; or

· the company financial statements and the part of the directors' remuneration report to be audited are not in agreement with the accounting records and returns; or

· certain disclosures of directors' remuneration specified by law are not made; or

· we have not received all the information and explanations we require for our audit

Responsibilities of the directors for the financial statements

As explained more fully in the directors' responsibilities statement set out on page 23, the directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view, and for such internal control as the directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, the directors are responsible for assessing the group's and the parent company's ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the directors either intend to liquidate the group or the parent company or to cease operations, or have no realistic alternative but to do so.

Auditor's responsibilities for the audit of the financial statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance but is not a guarantee that an audit conducted in accordance with ISAs (UK) will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

Irregularities, including fraud, are instances of non-compliance with laws and regulations. We design procedures in line with our responsibilities, outlined above, to detect material misstatements in respect of irregularities, including fraud. The extent to which our procedures are capable of detecting irregularities, including fraud is detailed below:

We obtained an understanding of the legal and regulatory frameworks that are applicable to the group and company and the procedures in place for ensuring compliance in the jurisdiction where the group and company operate, focusing on those laws and regulations that have a direct effect on the determination of material amounts and disclosures in the financial statements. The laws and regulations we considered in this context were the Companies Act 2006 and relevant tax legislation.

We assessed the nature of the group's business, the control environment and performance to date when evaluating the incentives and opportunities to commit fraud.

We identified the greatest risk of material impact on the financial statements from irregularities, including fraud, to be the override of controls by management to manipulate financial reporting and misappropriate funds. Our procedures to address the risk of management override included:

· enquiries of management about their own identification and assessment of the risks of irregularities, including any non-compliance with laws or regulations, or any potential claims of fraud;

· reviewing minutes of board meetings throughout the period;

· reviewing the system for the generation, authorisation and posting of journal entries;

· obtaining supporting evidence for a risk-based sample of journals, derived using a data analytics tool;

· considering significant estimates and judgements made by management for evidence of bias, and performing retrospective reviews where applicable;

· considering audit adjustments identified from our audit work for evidence of bias in reporting;

· audit of significant transactions outside the normal course of business, or those that appear to be unusual; and

· reviewing the other information presented in the annual report for fair presentation and consistency with the audited financial statements and the information available to us as the auditors.

Owing to the inherent limitations of an audit, there is an unavoidable risk that some material misstatements of the financial statements may not be detected, even though the audit is properly planned and performed in accordance with the ISAs (UK). The potential effects of inherent limitations are particularly significant in the case of misstatement resulting from fraud because fraud may involve sophisticated and carefully organized schemes designed to conceal it, including deliberate failure to record transactions, collusion or intentional misrepresentations being made to us.

A further description of our responsibilities for the audit of the financial statements is located on the Financial Reporting Council's website at: www.frc.org.uk/auditorsresponsibilities. This description forms part of our auditor's report.

Other matters which we are required to address

We were appointed by the Board on 27 March 2022 to audit the financial statements for the period ending 31 January 2022. Our total uninterrupted period of engagement is five years, covering the periods ending 31 January 2022 to 31 January 2026.

The non-audit services prohibited by the FRC's Ethical Standard were not provided to the group or the company and we remain independent of the group and the company in conducting our audit.

Our audit opinion is consistent with the additional report to the Board.

Use of our report

This report is made solely to the company's members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the company's members those matters we are required to state to them in an auditor's report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company and the company's members as a body, for our audit work, for this report, or for the opinions we have formed.

Matthew Stallabrass

Senior Statutory Auditor

For and on behalf of

Crowe U.K. LLP

Statutory Auditor

London

27 May 2026

Consolidated Statement of Comprehensive Income

for the year ended 31 January 2026

|

|

|

|

|

|

|

Notes |

Year ended 31 January 2026 |

Year ended 31 January 2025 |

|

|

|

£ |

£ |

|

Continuing operations |

|

|

|

|

Other income |

|

235 |

- |

|

Administrative expenses |

4 |

(1,708,841) |

(1,226,984) |

|

Project development expenses |

4 |

(175,241) |

(65,276) |

|

Finance costs |

|

(532,710) |

(135,073) |

|

Foreign exchange gains (losses) |

|

(71,291) |

1,007 |

|

Loss before taxation |

|

(2,487,848) |

(1,426,326) |

|

|

|

|

|

|

Taxation |

7 |

- |

- |

|

Loss for the year after taxation |

|

(2,487,848) |

(1,426,326) |

|

|

|

|

|

|

Other Comprehensive Income |

|

|

|

|

Foreign exchange differences on translation of overseas subsidiaries |

|

(13) |

(12,976) |

|

Total Comprehensive loss for the year |

|

(2,487,861) |

(1,439,302) |

|

|

|

|

|

|

Earnings per share: |

|

|

|

|

Basic and diluted earnings per share (pence) |

8 |

(25.27p) |

(16.18p) |

The notes on pages 36 to 53 are an integral part of these financial statements.

Consolidated Statement of Financial Position

As at 31 January 2026

|

|

Notes |

31 January 2026 |

31 January 2025 |

|

|

|

£ |

£ |

|

Non Current Assets |

|

|

|

|

Intangibles - Project development costs |

10 |

3,757,569 |

506,184 |

|

Total Non Current Assets |

|

3,757,569 |

506,184 |

|

|

|

|

|

|

Current assets |

|

|

|

|

Trade and other receivables |

12 |

141,277 |

47,808 |

|

Cash and cash equivalents |

13 |

153,286 |

16,673 |

|

Total Current Assets |

|

294,563 |

64,481 |

|

|

|

|

|

|

Total Assets |

|

4,052,132 |

570,665 |

|

|

|

|

|

|

Equity |

|

|

|

|

Share Capital |

17 |

213,252 |

176,297 |

|

Share Premium |

17 |

7,173,207 |

4,261,626 |

|

Share Based Payments |

17 |

1,051,652 |

689,029 |

|

Foreign Exchange Reserve |

|

(17,940) |

(17,927) |

|

Retained Earnings |

|

(9,127,565) |

(6,639,717) |

|

Total Equity |

|

(707,394) |

(1,530,692) |

|

|

|

|

|

|

Current Liabilities |

|

|

|

|

Trade and other payables |

14 |

2,708,929 |

1,501,966 |

|

Borrowings |

16 |

904,877 |

599,391 |

|

Total Current Liabilities |

|

3,613,806 |

2,101,357 |

|

|

|

|

|

|

Non Current Liabilities |

|

|

|

|

Borrowings |

16 |

1,145,720 |

- |

|

Current and Total Liabilities |

|

4,759,526 |

2,101,357 |

|

|

|

|

|

|

Total Equity and Liabilities |

|

4,052,132 |

570,665 |

|

|

|

|

|

The notes on pages 36 to 53 are an integral part of these financial statements.

The financial statements were approved and authorised for issue by the Board on 27 May 2026.

Paul Atherley

Director

Alkemy Capital Investments plc

Consolidated Statement of Changes in Equity

For the year ended 31 January 2026

|

|

Share capital |

Share Premium |

Share Based Payments |

Foreign Exchange Reserve |

Retained Earnings |

Total |

|

|

£ |

£ |

£ |

£ |

£ |

£ |

|

As at 1 February 2024 |

176,297 |

4,261,626 |

259,771 |

(4,951) |

(5,213,391) |

(520,648) |

|

|

|

|

|

|

|

|

|

Loss for the year |

- |

- |

- |

- |

(1,426,326) |

(1,426,326) |

|

Foreign exchange losses on translation of overseas subsidiaries |

- |

- |

- |

(12,976) |

- |

(12,976) |

|

Total Comprehensive income |

- |

- |

- |

(12,976) |

(1,426,326) |

(1,439,302) |

|

|

|

|

|

|

|

|

|

Transactions with owners: |

|

|

|

|

|

|

|

Share based payments |

- |

- |

429,258 |

- |

- |

429,258 |

|

Total transactions with owners |

- |

- |

429,258 |

- |

- |

429,258 |

|

|

|

|

|

|

|

|

|

Balance at 31 January 2025 |

176,297 |

4,261,626 |

689,029 |