Final Audited Results

Summary by AI BETAClose X

THE INFORMATION CONTAINED WITHIN THIS ANNOUNCEMENT IS DEEMED BY THE COMPANY TO CONSTITUTE INSIDE INFORMATION AS STIPULATED UNDER ARTICLE 7 OF THE EU REGULATION 596/2014 AS IT FORMS PART OF THE UK LAW BY VIRTUE OF THE EUROPEAN UNION (WITHDRAWAL) ACT 2018 ("MAR"). UPON THE PUBLICATION OF THIS ANNOUNCEMENT VIA A REGULATORY INFORMATION SERVICE, THIS INFORMATION IS CONSIDERED TO BE IN THE PUBLIC DOMAIN.

25 February 2026

AFC Energy Plc

("AFC Energy" or the "Company")

Final Audited Results for the Financial Year Ended 31 October 2025

Delivering strategic and operational progress

AFC Energy Plc (AIM: AFC), a leading provider of ammonia-based low carbon hydrogen production and hydrogen-to-power solutions at a commercially viable price point, is pleased to announce its audited results for the financial year ended 31 October 2025 ("FY25").

John Wilson, Chief Executive of AFC Energy, said:

"12 months ago, we announced plans to accelerate our path to scalable commercial success, focus on areas of greatest opportunity and deliver a market push, rather than relying solely on market pull. We are successfully delivering on these plans, working to ensure AFC Energy creates significant shareholder value.

The successful execution of our oversubscribed £27.5 million (gross) fundraising in July 2025 was a further vote of confidence in the evolution of the business, enabling the business to invest with purpose to accelerate the commercial development and deployment of our fuel cell and ammonia cracking products. This has enabled the recent launch of our new LC30 fuel cell generator and continued progress to availability of our Hy-5 ammonia cracker, capable of producing 500kg/day of hydrogen which we aim to target selling at £10/kg.

We continue to execute successfully on our strategy as we look to deliver low-cost hydrogen power at scale without the need for government subsidies. AFC Energy remains well on track for 2026 to be a year of conversion of our growing pipeline of opportunities to contractual orders and the beginning of sustained revenue growth for our business. We look forward to the future with strong and increasing optimism."

FY25 Operational Highlights

|

• |

Strategic reset and focus on delivering the commercial deployment of our proprietary technology and products to create significant shareholder value |

|

• |

Multiple successful deployments of AR2 30kW fuel cell generators through our joint venture Speedy Hydrogen Solutions |

|

• |

Launch of our first hydrogen production product - the Hy-5 ammonia cracker - capable of producing 500 kg/hydrogen per day, for delivery in calendar year 2026 |

|

• |

Joint Development Agreement ("JDA") signed with S&P 500 partner to develop small to large scale decentralised ammonia to hydrogen crackers. Successful completion of first phase of JDA and discussions ongoing regarding commercial opportunities prior to commencing next phase |

|

• |

Strategic partnership with Volex Plc to manufacture at scale our fuel cell generators |

|

• |

Joint venture with Industrial Chemicals Group Limited to use AFC Energy's proprietary, leading ammonia cracking technology to produce the lowest cost bulk hydrogen available to industrial customers in the UK, by the end of calendar year 2026 (subject to permitting) |

|

• |

We announced targeting the provision of hydrogen-as-a-service, with an offer to customers of low-carbon hydrogen at £10/kg - making us one of the most cost-competitive, low-carbon hydrogen suppliers in the UK |

|

• |

Working in partnership with Tamgo, the successful deployment of H-Power 200kW liquid cooled fuel cell generator at the FIA Extreme H World Cup in Qiddiya City, Saudi Arabia |

|

• |

Significant focus on commercial viability, driving a streamlined business reorganisation with reduced headcount and footprint, and a clearer operational focus through the establishment of a Project Management Office and commercial function, with appointments of Programme Director, Chief Strategy Officer and Chief Commercial Officer to complement the leadership team |

FY25 Financial Highlights

|

• |

£27.5m successful oversubscribed placing to support the business' development ambitions |

|

• |

£25.3m cash, cash equivalents and short term investments at year end (FY24: £15.4m), with current cash of £20.4m as at 31 January 2026 (including short term investments). |

|

• |

Loss after tax of £22.2m (FY24: £17.4m) which includes an increase in non-cash expenditure of £8.4m (£5.5m due to stock and debtor write-offs, £1.9m increase in depreciation/amortisation, £0.5m in share-based payments and £0.5m of remuneration settled via equity) |

|

• |

R&D investment of £11.7m (FY24: £9.5m), with £1.6m R&D tax credits received (FY24: £2.7m) |

Post Period Developments

|

• |

Launch of the LC30, 30kW fuel cell generator, c. 85% lower cost, up to 20% more efficient, >95% fewer components and substantially smaller footprint than its predecessor, resulting in inbound commercial interest |

|

• |

Joint Development Agreement signed with Komatsu Ltd, c.$2 million contract value, to design and integrate AFC Energy's proprietary ammonia cracking technology with a Komatsu industrial internal combustion diesel engine to assess the feasibility of a new ammonia fuelled engine platform capable of scaled production |

|

• |

UK Environment Agency permit agreed to enable the sale of hydrogen produced from our pilot ammonia cracker in Dunsfold, ensuing AFC Energy will generate revenues from hydrogen production 3-4 months ahead of schedule |

Business Priorities - Commercialisation

|

• |

Commercial traction to deliver pre-orders of LC30 and Hy-5 units |

|

• |

Establish Fuel as a Service (FaaS) offering for UK customers |

|

• |

Progressing JDAs to deliver product and technology based commercial revenues |

|

• |

Continued expansion of our channel and refinement of go to market strategy |

|

|

o North American market focus |

|

|

o TAMGO market applications and optimal product set review |

|

|

o European market entry point and partnership review |

Business Priorities - Development and Technical

|

• |

Finalising development, build and roll out of Hy-5, the world's first containerised, portable, cracking system capable of producing up to 500kg/day, for delivery at the end of calendar year 2026 |

|

• |

Continuation of roadmap development for both fuel cell generator portfolio and cracker development, to further productise our technology |

|

• |

Continued successful patent applications filed based on core technology |

Outlook

|

• |

Through continued execution of our strategic plan, commercial momentum is building |

|

• |

Remain well on track for 2026 to be a year of conversion of our growing pipeline of opportunities to contractual orders and the beginning of sustained revenue growth for our business |

Investor Presentation

John Wilson, Chief Executive Officer, and Karl Bostock, Chief Financial Officer, will host a live presentation for retail investors via Investor Meet Company on Friday 27 February 2026, at 14:00 hrs GMT.

The presentation is open to all existing and potential shareholders. Questions can be submitted pre-event via your Investor Meet Company dashboard up until Wednesday 25 February 2026, 17:00 hrs, or at any time during the live presentation.

Investors can sign up to Investor Meet Company for free and add to meet AFC ENERGY PLC via: https://www.investormeetcompany.com/afc-energy-plc/register-investor

FOR FURTHER INFORMATION, PLEASE CONTACT:

|

AFC Energy Plc John Wilson (Chief Executive Officer) |

+44 (0) 14 8327 6726 |

|

Karl Bostock (Chief Financial Officer)

Peel Hunt LLP - Nominated Adviser and Joint Broker Richard Crichton / Georgia Langoulant / Emily Bhasin |

+44 (0) 207 418 8900

|

|

Zeus - Joint Broker David Foreman / James Hornigold (Investment Banking) Dominic King (Corporate Broking) / Rupert Woolfenden (Sales) |

+44 (0) 203 829 5000 |

|

DGA Group - Financial PR and Communications Advisors James Benjamin / James Styles

|

+44 (0) 7747 113 930 +44 (0) 7510 385 554 |

ABOUT AFC ENERGY

AFC Energy Plc is a leading provider of ammonia-based low carbon hydrogen production and hydrogen-to-power solutions. Our market-leading decentralised ammonia cracker and fuel cell generator products are engineered to unlock the low carbon hydrogen market by meeting customers' needs with scalable, reliable supplies of low carbon hydrogen and power. AFC Energy is enabling customers to decarbonise at a price that is commercially viable.

We are focused on the successful commercial rollout of our core product suite and on creating significant shareholder value by converting our growing opportunity pipeline into contracted orders and delivering sustained revenue growth.

Our core strategy is to develop and deploy products that enable the production of scalable, reliable supplies of clean hydrogen at commercially viable prices and without reliance on government subsidies or incentives. AFC Energy achieves this through our proprietary, decentralised and modular ammonia cracker technology, and providing low carbon, off‑grid power solutions with our fuel cell generators that are competitive with, and capable of displacing, diesel generators on a total cost of ownership basis.

The Company's modular, decentralised ammonia cracker systems have production capacities of approximately 0.5 and 4 tonnes of hydrogen per day respectively. These enable the generation of scaled volumes of low carbon hydrogen at the point of use within a highly compact footprint. Our systems have the potential to drive substantial revenue growth across a wide range of addressable markets, including hard‑to‑abate industrial facilities, transportation and power generation applications.

AFC Energy's fuel cell generator systems are currently offered with generation capacities of 30 kW and 200 kW. They are well-suited to off‑grid, decentralised and temporary power applications, including the displacement of diesel generators on construction and infrastructure sites. Further use cases include electric vehicle charging for cars, buses and trucks, as well as charging of battery‑powered non‑road machinery, with additional emerging opportunities in maritime, data centre and rail applications.

AFC Energy is listed on the London Stock Exchange's AIM Market and headquartered in Dunsfold, Surrey, UK.

Please read more on our website https://www.afcenergy.com/ and follow us on LinkedIn

Chairman's Statement

This year has been one of significant positive change for AFC Energy.

Building on the progress of previous years, the Company has taken decisive action to reposition itself for scalable commercial success to accelerate the creation of significant shareholder value.

As Chairman, I am proud to say that the Board is fully aligned with the executive leadership in both recognising the need for strategic change and supporting its rapid implementation.

In what has remained a challenging external environment, the Company has made great strides and is well positioned for the future.

We also welcomed a refreshed executive team early in the financial year. The appointments of John Wilson as Chief Executive Officer and Karl Bostock as Chief Financial Officer marked a critical turning point for the business. Under their stewardship, the Company has been restructured with a clear focus on execution, cost efficiency, and the creation of significant shareholder value. The progress made since their appointments reflects not only strong strategic and operational leadership, but a renewed cultural energy across the business, ensuring AFC Energy is well positioned to meet its ambitions. The strategic reset has addressed key realities in our sector, namely the high cost of capital, policy uncertainty, and a market that increasingly demands economically viable clean energy solutions. AFC Energy's sharpened focus on cost competitiveness, product simplification, and meaningful commercial partnerships is a necessary evolution and has already begun to deliver encouraging results.

The successful execution of our oversubscribed £27.5 (gross) million fundraising in July 2025 was a further vote of confidence in the evolution of the business, supported by both new and existing shareholders. On behalf of the Board, I would like to extend our sincere thanks to all shareholders who participated. This capital is enabling the business to invest with purpose in cost-down initiatives, strategic hires, and the infrastructure necessary to accelerate the commercial development of both our fuel-cell and ammonia cracking products.

Crucially, the business is not only developing advanced technology, but it is also now bringing that technology to market in defined commercial fuel cell and ammonia cracker products. The evolution of our go-to-market strategy, exemplified through the Speedy Hire joint venture, is allowing us to validate our proposition in live environments. The response from end-users to our diesel-equivalent pricing and low-emission profile has been encouraging and signals a maturing commercial platform.

Beyond the UK, our engagement with global supply chain partners such as Volex plc positions us to scale efficiently as demand increases. This aligns with a broader industry shift: hydrogen technologies at a commercially viable price point are now forming part of near-term procurement decisions across construction, infrastructure and logistics.

From a macro perspective, the global hydrogen economy is entering a new phase. Governments and industry stakeholders around the world are pushing forward with commercial-scale green hydrogen and ammonia projects. Ammonia is fast becoming the carrier of choice for transporting hydrogen due to its lower cost, scalability, and ability to utilise existing infrastructure. As an early advocate of this model, we are already seeing that belief rewarded through progress at our joint venture with ICL on Teesside.

Our early investment in ammonia-based systems not only differentiates our technology but also solves some of the hardest problems in the hydrogen value chain. It gives us the ability to decouple clean hydrogen supply from traditional infrastructure constraints, which is essential for us to enable widespread off-grid power applications.

Internally, the business has also matured. The restructuring carried out during the year has created a leaner, more agile and focused organisation. Strategic new hires have brought added capability in commercial and operational roles, and we have instilled a culture of delivery that will support the next stage of growth. Cost efficiency measures and operational discipline introduced this year are expected to deliver c.£1.5 million in annualised savings, extending our cash runway while improving focus.

While these strategic and operational developments are crucial, the resilience and determination of our team deserves recognition. The pace of change in the business over the past 12 months has been significant, and our team has met this challenge with professionalism and conviction. On behalf of the Board, I would like to extend heartfelt thanks to every member of the AFC Energy team. Their dedication continues to be the bedrock of our success.

I would also like to reiterate our gratitude to our shareholders for their continued support and belief in our vision. The success of this year's fundraising has allowed us to move forward with confidence and clarity. We remain committed to open and transparent engagement, and we understand the responsibility we carry to convert your investment into long-term, sustainable value.

Looking ahead to 2026, we do so with strong momentum and increasing confidence in our sector. AFC Energy is now well placed to play a central role in enabling the global transition to zero-emission power. With cost-competitive products, validated routes to market, and a strengthened leadership team, the Company has the right foundations for scalable growth and the creation of significant shareholder value.

The use of hydrogen as the green fuel of the future is a reality, and with ammonia an enabler, and innovation at our core, AFC Energy is ready to lead and successfully deliver on its ambitions.

Chief Executive Officer's Statement

Dear Shareholders,

In January 2025, I was appointed Chief Executive Officer of AFC Energy, with Karl Bostock joining as Chief Financial Officer. This report covers progress from that date.

Since appointment my focus has been on resetting the Company's strategy and delivering on it. We now live in a world where the cost of capital is high and both micro and macro uncertainty preclude willingness to invest. This, coupled with challenges in the global sector, necessitated a change of direction and pace.

Our business was on the cusp of commercialisation, but at a price point that the market was unwilling to bear, with product complexity that would not enable economies of scale to drive commercial viability. This needed to change.

While regulatory tailwinds support our sector in the medium term, a lack of long term government policy clarity, dilution of policy commitments and unwillingness to pay substantially more for "green," provided a clear steer of both the challenge and opportunity available to us. We need to build a business in which the "noise" of policy is secondary to our value proposition. Our business is blessed with an incredibly talented team that has developed, and continues to develop, world-class technology. The task at hand is to harness this creativity to create value, which is now our approach: Establish a product suite and offering that drives commercial viability without government subsidy.

With our go-to-market strategy for our fuel cell generators well defined in the UK through our JV with Speedy Hire, we undertook a comprehensive analysis to determine total cost of ownership of diesel generators, servicing and fuel cost over their economic life. In doing so, we confirmed very clear price points that we needed to attain to meet our goals. What followed was an 85% cost reduction from the 20-unit volume build the business undertook to satisfy the JV demand. In conjunction, we announced the launch of our first hydrogen production product - the Hy-5 ammonia cracker - under a fuel as a service model which will first be delivered at the back end of calendar year 2026, supported by Environment Agency approval for commercial use of hydrogen produced in Dunsfold to power our Speedy Hydrogen Solutions fuel cell generators. These products will enable us to be highly competitive with incumbent technology with respect to price.

1) Provide balance sheet strength to finance the Company's short-term goals

In July we announced an oversubscribed fundraise from both institutional and private investors. The c.£27.5m (gross) fundraise was a clear mandate to deliver the strategy. Through the process we have welcomed several new institutions to our business as shareholders.

2) Laser focus on costs and building Company infrastructure to deliver

Post fundraise, and following a strategic cost and business structure review, we have taken several steps to drive down costs:

a) Reduction of the Company's footprint, including the closure of our Germany facility in Stade, resulting in a £250,000 annual saving and the release of a significant bond guarantee to our balance sheet.

b) Realigning the headcount of the business to our new business strategy. This has resulted in a c.20% reduction in headcount as we seek to benefit from outsourcing manufacturing in the medium term.

c) Reduction of the number of advisors.

These actions are expected to deliver c.£1.5m of annualised savings. In addition, we have restructured the business: pooling the engineering talent as opposed to a divisional split, strengthened the Executive team through the addition of a Programme Director, Chief Strategy Officer (CSO) and Chief Commercial Officer (CCO) and introducing a more coherent, and cohesive organisational structure that focuses on delivery and execution.

3) Deliver proof points, technology validation and supply chains

Throughout the year, we delivered key proof points that served to provide peer validation of our technology and potential for market adoption, including validation of our cracker technology by a S&P500 partner and, post-FY25, Komatsu, in the form of our recently announced joint development agreement. Our partnership with Volex plc gives us potential access to manufacturing across multiple geographies served by 27 factories, and access to a substantial global supply chain that will support further reduction in generator costs with economies of scale.

Our joint venture with ICL continues at pace as we relocate our pilot cracker from Dunsfold, Surrey, to Port Clarence, Teesside, to generate the UK's first commercially available hydrogen from cracked ammonia. We have also worked to establish the supply chain for green ammonia to support this. Following line of sight on costings of our new LC30 generators, in conjunction with confidence of Hy-5 delivery, we offered "tomorrow's price today" to Speedy Hire's end customers: that of diesel equivalence. This action served to unlock the market with a pipeline quickly building from multiple end users. Deployments have begun in earnest across numerous use cases: from recharging of electrical excavators to powering welfare stations. The lessons learned from these deployments are essential to continue to build the business model for geographical expansion.

We successfully concluded our Red Diesel Replacement ("RDR") grant programme, showcasing our 200kW hydrogen fuel cell generator powering a 1.6 km conveyor, and 30kW system, as part of a Lower Thames Crossing project. This generated £2.2m of grant income (cash receipts) and demonstrated the resilience of our liquid-cooled platform to be utilised in our next generation of products. The same generator ran faultlessly in Saudi Arabia providing power for almost two weeks to the FIA Extreme H event.

4) Rebrand and building a commercial function to deliver

We have undertaken a rebranding exercise and website overhaul to better reflect the evolved business and strategy. This serves to provide greater clarity to both the investment community and to current and potential customers of our value proposition and product offerings.

At the start of my tenure, our commercial team consisted of one commercial director. We have begun to put in place the building blocks of a high quality commercial function capable of delivering our ambitions. The appointments of a Chief Strategy Officer, to focus on demand creation, in conjunction with a Chief Commercial Officer to close opportunities developed, are central to this.

2026 will be a year of go to market and channel development, with a focus on customer demand creation and geographic expansion from our newly created commercial function. 2026 will also see new product availability with our LC30 fuel cell generators and Hy-5 units, which will help to drive the conversion of our growing pipeline of opportunities to contractual orders and the beginning of sustained revenue growth for our business.

The resilience and expertise of our team members has been critical to the progress made this year to shift significantly the strategic and operational focus of the business. I extend my sincerest thanks for their support and dedication since I joined our business, and their belief in our strategy and ability to deliver.

In a sector mostly reliant on government subsidy for commercial viability, we stand out from the crowd. Our ability to produce hydrogen from ammonia, at a price point unmatched in the UK, is key to creating significant shareholder value. We look forward to the future with optimism.

Financial Review

As highlighted in the CEO Report, the business has undergone a commercial pivot in its drive to create value from the technology created by our talented employees. This report presents the impact of these changes on the FY25 financial information:

1. Establish a product suite and offering that drives commercial viability without government subsidy

The business is fulfilling this ambition by the launch of two products.

Proving the concept (Fuel Cells) - The work undertaken as part of the RDR grant paved the way for the concept of the new lower cost fuel cell generator (LC30). This project proved that we could take technology and harness its strengths to provide a like-for-like solution as the current generators (AR2) but at a highly reduced cost. In the year, total costs (including labour) of £2.3m were incurred on this project of which £2.1m was capitalised under IAS 38. Cash inflows relating to government grants totalled £2.2m during the year, all of which have been deferred (recognised as other creditors) which will be amortised over the life of the development asset (3 years).

In addition to the expenditure above, we incurred costs of £17k supporting the deployment of our 200kW hydrogen generator (which contains the same technology as the new lower cost 30kw hydrogen generator) supporting the Extreme H World Cup in Qiddiya. The fuel cell performed perfectly in the Saudi Arabian desert, operating in some of the harshest environmental conditions on planet. Sales revenues of £15k were recognised for this support.

Testing (Hy-5) - As part of the development of the Hy-5, the business is constantly seeking to improve the efficiency and durability of its cracker technology. During the year the total cash impact of these projects amounted to £967k.

Developing the product - The FY25 cost of the development for the 2 products are as follows:

|

Project |

Committed Spend (yet to be incurred / spent) £'000s |

Cost in FY25 £'000s |

Total £'000s |

|

30kW Fuel Cell |

586 |

559 |

1,145 |

|

Hy-5 |

627 |

712 |

1,339 |

|

|

1,213 |

1,271 |

2,484 |

Accounting for the current technology - As part of the strategic review, the business made the decision not to manufacture any further AR2 units (the model sold to the Speedy Hire JV) on the grounds that they were too expensive and the new model is set to be significantly cheaper. An outcome of this decision is that all inventory held of both finished goods and raw materials of the AR2 were written down to £nil at 31 October 2025. The total impact of this decision was £2.6m which is included within operating costs within the financial information.

In addition to inventory relating to the AR2 unit, the Directors also reviewed the recoverability of the debtor for the 15 remaining AR2 units which remain outstanding for payment from Speedy Hydrogen Services Limited (SHS). To accelerate the transition from diesel generators to hydrogen fuel cells we want to give the joint venture the lowest cost possible for the best available technology. For this reason, we have provided for the debt of £2.8m owed by Speedy Hydrogen Solutions to AFC Energy on the assumption that the joint venture will transition to the new technology.

2. Provide balance sheet strength to finance the Company's short-term goals

During July and August 2025, the business raised £27.5m (gross) via a fundraise, issuing new equity at 10p per share. This fundraise was oversubscribed and included new institutional investors capable of supporting future developments.

The cost of the fundraise was £1.7m (£1.4m in commissions and £0.3m in legal and corporate finance costs) resulting in net proceeds of £25.8m. The funds will be used to deliver the two product lines listed above.

3. Laser focus on costs and building Company infrastructure to deliver

The business has carried out a review of all costs which included the cost of employing our talented team. Due to the change in strategy the business needs different skills today and sadly the business had to part ways with 17 colleagues, and we redeployed a further four during October 2025 at a total cost of £276k. This cost is in addition to the rationalisation programme which concluded in November 2024 which cost a total of £262k. A summary of savings is as follows:

|

|

Total Cost in FY25 £'000s |

Cost to Execute in FY25 £'000s |

Annual Run Rate Cost Savings £'000s |

Total cost in FY26 £'000s |

|

Stade (Germany) Facility (excluding provision release) |

606 |

327 |

279 |

- |

|

Reduced footprint of UK facility (exited in January 26) |

225 |

- |

225 |

56 |

|

People cost (October 25 redundancy programme) |

1,206 |

276 |

930 |

- |

|

Broker rationalisation |

75 |

- |

75 |

- |

|

|

2,112 |

603 |

1,509 |

56 |

In the CEO Report, John Wilson reports on the pooling of the engineering and development teams, removing the segregation between fuel cells and fuel processing (Hyamtec) for the organisation. AFC Energy plc has two subsidiaries, Hyamtec Limited and H-Power Limited. Both of these entities are dormant and have no assets or liabilities. Any reference to Hyamtec within the annual report is making reference to the fuel processing (cracker) activities of the business and not the legal entity. In addition, the report makes reference to the ICL Joint Venture. The Joint Venture is in the progress of obtaining an Environmental Agency permit to enable the relocation of the AFC portable ammonia cracker from Dunsfold to its intended location in Middlesborough. After the permit is granted, it is our intention to incorporate a new limited company and commence trade.

4. Deliver proof points, technology validation and supply chains

Other than a small amount of Engineering Revenue and the expenditure on the development costs reported above, there is yet to be any impact on the financial information from these achievements.

Loss for the financial year of £22.2m

At first glance, this loss represents a significant increase from the prior year of £17.4m. However, the main elements of the increase are already explained above (with the stock and debtor write offs). Other items where there have been significant variances from the prior year include:

Revenue: In FY24 the business made revenue of £4m selling the current AR2 units. On joining the business, the decision was made not to manufacture or sell any additional AR2 units. Revenue for FY25 is only £0.1m and includes Rental of the unit to Acciona, Engineering Services and Extreme H support.

Other Income: Other income has dropped year in year due to the updated accounting treatment of Research and Development Tax Credits with the new combined scheme being recognised solely on the taxation line (FY24 £0.2m)..

Operating Costs: Operating costs in FY25 include a number of non-cash transactions. These are summarised as: (a) the stock write down of £2.6m (FY24 - £nil) as reported above; (b) the provision for expected credit losses of £2.9m (FY24 - £nil) as report above; (c) depreciation / amortisation of £4.4m (FY24 - £2.5m) the increase in this cost being accelerated depreciation on leasehold improvements on the property the business has decided to exit and the commencement of amortising the capitalised R&D spend; (d) share based payment of £2.0m (FY24 - £1.5m), the increase relating to a full year impact of the options issued in FY24 (£0.8m in FY25 vs £0.5m in FY24) as well as to the new leadership team (£0.8m in FY25 vs £nil in FY24), offset by a revaluation if £0.4m in FY24 which did not repeat in FY25. If we adjust for these non-cash items the underlying costs would be £13.4m (FY24 - £14.1m).

Taxation: In FY25 the business focus shifted back towards development from manufacturing which in turn has increased the amount of expenditure qualifying for tax credits. This coupled with a change in the qualification framework resulted in the Company qualifying for the enhanced R&D intensive support scheme in FY25 which was not achieved in FY24.

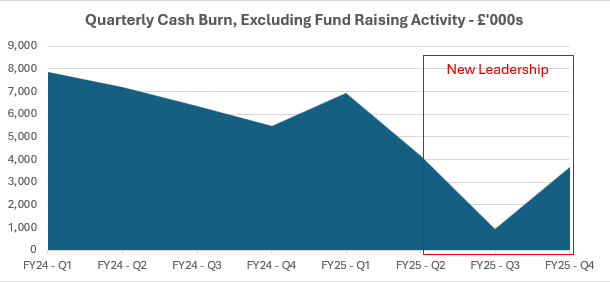

Cash Management and Closing Cash of £25.3m

Since joining the business, we have worked hard to preserve cash whilst the new strategy was set.

This resulted in a reduction of the quarterly cash burn from £6.7m per quarter in the 15 months before joining to £2.9m in the last three months of the financial year. The cash burn increased in Q4 due to the cost of restructuring the business, the exit of the German Stade facility and the reengagement of development activities around the two key products reported above. Q3 includes the benefit of R&D tax credit receipts in both financial years. At the year end, the Company had placed £11m in a 95 day notice account to maximise interest receivable. Due to the notice period, this £11m is classed as short term investment in the financial information. References to cash in this report includes these short term investments and this is different to how it is reported in the financial information.

A summary of the FY25 cash flows are as follows:

|

|

2025 £m |

2024 £m |

2023 £m |

|

Net Loss Before Tax |

(25.4) |

(19.3) |

(19.6) |

|

Non-cash items |

12.4 |

4.0 |

2.4 |

|

R&D Credits Received |

1.6 |

2.7 |

3.9 |

|

Changes in Working Capital |

(0.5) |

(6.3) |

0.2 |

|

Cash used in Operations |

(11.9) |

(18.9) |

(13.1) |

|

Investing Activities |

(3.5) |

(7.7) |

(1.2) |

|

Financing Activities (net of costs) |

25.3 |

14.6 |

1.5 |

|

Cash Movement in the Year |

9.9 |

(12.0) |

(12.8) |

|

Opening Cash |

15.4 |

27.4 |

40.2 |

|

Closing Cash |

25.3 |

15.4 |

27.4 |

A summary of non-cash items are as follows:

|

|

2025 £m |

2024 £m |

2023 £m |

|

Share Based Payment |

£2.0m |

£1.5m |

£0.8m |

|

Depreciation / Amortisation / Loss on Disposal |

£4.4m |

£2.5m |

£1.7m |

|

Stock Provision / Write Off |

£2.6m |

- |

- |

|

Provision for Expected Credit Losses |

£2.9m |

- |

- |

|

Staff costs paid in Equity |

£0.5m |

- |

- |

|

Consideration in kind |

- |

- |

(£0.1m) |

|

|

£12.4m |

£4.0m |

£2.4m |

Going Concern

The Directors have prepared and reviewed forecasts for the period ending February 2027 which they consider to be the appropriate period for assessing going concern. Whilst events and conditions beyond this period of assessment have been considered. In the judgement of the directors, such events and conditions do not require an extension to the period of assessment.

The base case forecast predominantly includes the continuation of the development of the Hy-5 ammonia cracker and the next generation of Fuel Cell products together with their associated costs and the fixed running costs of the business offset by a moderate volume of equipment and gas sales from the products developed. The sales commence in September 2026 and ramp steadily. In this base case scenario, the forecasts show that the business has sufficient resources throughout the assessment period.

As with prior years, the Directors have applied sensitivities to the above base case when considering their opinion on going concern. The sensitivities considered were:

· A 50% reduction in sales volumes

· A 6-month slippage in project delivery

· The timing and quantum of expected R&D tax credits

These sensitivities have been applied without any management action and the Directors have the ability to control the cost base as well as slow down the pace of development in order to preserve cash if one or more of the scenarios became a reality.

Given the outcome of the assessment above, the directors have a reasonable expectation that the Company has adequate resources to continue in operational existence for the foreseeable future, being the period to 28 February 2027. Accordingly, the directors continue to adopt the going concern basis of preparation in this financial information.

Longer Term Assessment

Considering the maturity of the organisation and the fact that the business is transitioning from a R&D led company to one which is commercially viable, the Directors have prepared forecasts which extend beyond the going concern assessment period. The longer term forecasts (beyond the assessment period) show that the business will require a sizable increase in revenue (delivering sustainable commercial revenues in excess of total costs) or additional funding through debt or a further fundraise in order to be able to continue to trade in the medium term (second half of calendar year 2027).

Whilst the Directors recognise the challenges of fundraising in the current economic climate, they are confident that when the Company chooses to seek additional funding that it will be available. This view is based on:

· A track record of being able to raise funds in the current economic climate (£27.5m raised in July 2025);

· The new product road map delivering an end to end solution at a comparable cost to the incumbent diesel technology in FY26;

· UK Government requirement for construction tenders to include a non-diesel solutions for onsite electricity generation on projects such as HS2 and the Lower Thames Crossing;

· Commercial and technical validation of our products through the JDA partnerships delivered in FY25; and

· Deployments of the current generator fleet through our Joint Venture partner Speedy Hire

The Directors acknowledge the requirement to create a commercially viable business as quickly as possible, with the recent strategy refresh having this objective at its core.

For the year ended 31 October 2025

|

|

|

|

|

Year Ended 31 October 2025 |

|

Year Ended 31 October 2024 |

||

|

|

|

Note |

|

£000 |

|

£000 |

||

|

|

|

|

|

|

|

|

|

|

|

Revenue from customer contracts |

|

5 |

|

125 |

|

4,002 |

|

|

|

Cost of sales |

|

|

|

(232) |

|

(5,868) |

|

|

|

Gross loss |

|

|

|

(107) |

|

(1,866) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Other income |

|

6 |

|

294 |

|

429 |

|

|

|

Expected Credit Losses |

|

19 |

|

(2,937) |

|

- |

|

|

|

Operating costs |

|

7 |

|

(22,851) |

|

(18,133) |

|

|

|

Operating loss |

|

|

|

(25,601) |

|

(19,570) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Finance income |

|

11 |

|

213 |

|

316 |

|

|

|

Finance costs |

|

11 |

|

(66) |

|

(55) |

|

|

|

Loss before tax |

|

|

|

(25,454) |

|

(19,309) |

|

|

|

Taxation |

|

12 |

|

3,259 |

|

1,890 |

|

|

|

Loss for the financial year and total comprehensive loss attributable to the owners of the company |

|

|

|

(22,195) |

|

(17,419) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic loss per share (pence) |

|

13 |

|

(2.41) |

|

(2.22) |

|

|

|

Diluted loss per share (pence) |

|

13 |

|

(2.41) |

|

(2.22) |

|

|

All amounts relate to continuing operations. There was no other comprehensive income in the year (2024: £nil).

Statement of financial position

As at 31 October 2025

|

|

|

|

|

31 October 2025 |

|

31 October 2024 |

|||

|

|

|

Note |

|

£000 |

|

£000 |

|||

|

Assets |

|

|

|

|

|

|

|||

|

Non-current assets |

|

|

|

|

|

|

|||

|

Intangible assets |

|

14 |

|

8,738 |

|

4,626 |

|

||

|

Right-of-use assets |

|

15 |

|

175 |

|

646 |

|

||

|

Investment in joint venture |

|

16 |

|

625 |

|

625 |

|

||

|

Property, plant and equipment |

|

17 |

|

2,508 |

|

4,666 |

|

||

|

|

|

|

|

12,046 |

|

10,563 |

|

||

|

Current assets |

|

|

|

|

|

|

|

||

|

Inventory |

|

18 |

|

- |

|

1,948 |

|

||

|

Trade and other receivables |

|

19 |

|

1,923 |

|

6,737 |

|

||

|

Income tax receivable |

|

|

|

3,159 |

|

1,517 |

|

||

|

Restricted cash |

|

|

|

- |

|

433 |

|

||

|

Short term investments |

|

20 |

|

11,000 |

|

- |

|

||

|

Cash and cash equivalents |

|

20 |

|

14,317 |

|

15,374 |

|

||

|

|

|

|

|

30,399

|

|

26,009 |

|

||

|

Total assets |

|

|

|

42,445 |

|

36,572 |

|

||

|

Current liabilities |

|

|

|

|

|

|

|

||

|

Trade and other payables |

|

21 |

|

5,630 |

|

4,955 |

|

||

|

Asset finance |

|

|

|

63 |

|

- |

|

||

|

Lease liabilities |

|

22 |

|

141 |

|

505 |

|

||

|

Provisions |

|

23 |

|

96 |

|

217 |

|

||

|

|

|

|

|

5,930 |

|

5,677 |

|

||

|

Non-current liabilities |

|

|

|

|

|

|

|

||

|

Lease liabilities |

|

22 |

|

19 |

|

159 |

|

||

|

Asset finance |

|

|

|

62 |

|

|

|

||

|

Provisions |

|

23 |

|

39 |

|

468 |

|

||

|

|

|

|

|

120 |

|

627 |

|

||

|

Total liabilities |

|

|

|

6,050 |

|

6,304 |

|

||

|

Capital and reserves attributable to the owners of the company |

|

|

|

|

|

|

|

||

|

Share capital |

|

24 |

|

1,131 |

|

854 |

|

||

|

Share premium |

|

24 |

|

159,046 |

|

133,555 |

|

||

|

Other reserve |

|

|

|

7,054 |

|

4,629 |

|

||

|

Retained loss |

|

|

|

(130,836) |

|

(108,770) |

|

||

|

Total equity attributable to shareholders |

|

|

|

36,395 |

|

30,268 |

|

||

|

Total equity and liabilities |

|

|

|

42,445 |

|

36,572 |

|

||

Statement of changes in equity

Statement of changes in equity

For the year ended 31 October 2025

|

|

|

Share capital |

|

Share premium |

|

Other reserve |

|

Retained loss |

|

Total |

|

||||||||||||||

|

|

|

£000 |

|

£000 |

|

£000 |

|

£000 |

|

£000 |

|

||||||||||||||

|

Balance at 1 November 2023 |

|

746 |

|

118,520 |

|

3,779 |

|

(91,960) |

|

31,085 |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

Loss after tax for the year |

|

- |

|

- |

|

- |

|

(17,419) |

|

(17,419) |

|

||||||||||||||

|

Issue of equity shares |

|

105 |

|

14,810 |

|

- |

|

- |

|

14,915 |

|

||||||||||||||

|

Equity-settled share-based payments |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

- Lapsed or exercised in the year |

|

3 |

|

225 |

|

(609) |

|

609 |

|

228 |

|

||||||||||||||

|

- Charged in the year |

|

- |

|

- |

|

1,459 |

|

- |

|

1,459 |

|

||||||||||||||

|

Balance at 31 October 2024 |

|

854 |

|

133,555 |

|

4,629 |

|

(108,770) |

|

30,268 |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

Loss after tax for the year |

|

- |

|

- |

|

- |

|

(22,195) |

|

(22,195) |

|

||||||||||||||

|

Issue of equity shares |

|

275 |

|

25,491 |

|

- |

|

- |

|

25,766 |

|

||||||||||||||

|

Equity-settled share-based payments |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

- Equity settled renumeration |

|

- |

|

- |

|

557 |

|

- |

|

557 |

|||||||||||||||

|

- Exercised in the year |

|

2 |

|

- |

|

- |

|

- |

|

2

|

|||||||||||||||

|

- Lapsed in the year |

|

- |

|

- |

|

(129) |

|

129 |

|

- |

|||||||||||||||

|

- Charged in the year |

|

- |

|

- |

|

1,997 |

|

- |

|

1,997 |

|||||||||||||||

|

Balance at 31 October 2025 |

|

1,131 |

|

159,046 |

|

7,054 |

|

(130,836) |

|

36,395 |

|

||||||||||||||

Share capital is the amount subscribed for shares at the nominal value.

Share premium represents the excess of the amount subscribed for share capital over the nominal value of these shares net of share issue expenses. The issue of shares above is presented net of issue cost (refer to Note 24 for further details on issue costs).

Other reserve represents the charge to equity in respect of unexercised equity-settled share-based payments and warrants granted.

Retained loss represents the cumulative loss of the Company attributable to equity shareholders of the parent company.

Cash flow statement for the year ended 31 October 2025

|

|

|

|

|

Year ended 31 October 2025 |

|

Year ended 31 October 2024 |

|

|

|

Note |

|

£000 |

|

£000 |

|

Cash flows from operating activities |

|

|

|

|

|

|

|

Loss before tax for the year |

|

|

|

(25,454) |

|

(19,309) |

|

Adjustments for: |

|

|

|

|

|

|

|

Amortisation of intangible assets |

|

14 |

|

1,049 |

|

81 |

|

Depreciation of right-of-use assets |

|

15 |

|

471 |

|

470 |

|

Depreciation of property, plant and equipment |

|

17 |

|

2,728 |

|

2,043 |

|

Loss on disposal of property, plant and equipment |

|

17 |

|

145 |

|

- |

|

Share-based payments |

|

25 |

|

1,997 |

|

1,459 |

|

Staff costs settled in equity |

|

|

|

558 |

|

- |

|

Finance income |

|

|

|

(213) |

|

(316) |

|

Lease finance charges |

|

|

|

29 |

|

41 |

|

Inventory write down |

|

|

|

2,573 |

|

- |

|

Movement in expected credit losses |

|

7 |

|

2,937 |

|

- |

|

Income recognised on government grants |

|

|

|

(45) |

|

- |

|

R&D tax credits receivable |

|

|

|

- |

|

(224) |

|

Working capital changes: |

|

|

|

|

|

|

|

Decrease in restricted cash |

|

|

|

434 |

|

(176) |

|

(Increase) in inventory |

|

|

|

(625) |

|

(1,770) |

|

Decrease in receivables |

|

|

|

1,860 |

|

(5,506) |

|

(Decrease) in payables |

|

|

|

(1,133) |

|

1,227 |

|

(Increase) in provisions |

|

|

|

(550) |

|

384 |

|

|

|

|

|

(13,239) |

|

(21,596) |

|

R&D tax credits received |

|

|

|

1,616 |

|

2,685 |

|

Net cash flows from operating activities |

|

|

|

(11,623) |

|

(18,911) |

|

Capital investment in joint venture |

|

16 |

|

- |

|

(625) |

|

Purchase of plant and equipment |

|

17 |

|

(724) |

|

(2,952) |

|

Government Grant received |

|

|

|

1,871 |

|

|

|

Additions to intangible assets |

|

14 |

|

(5,160) |

|

(4,443) |

|

Term Deposits |

|

26 |

|

(11,000) |

|

- |

|

Interest received |

|

11 |

|

213 |

|

316 |

|

Net cash flows used in investing activities |

|

|

|

(14,800) |

|

(7,704) |

|

Proceeds from the issue of share capital |

|

|

|

27,473 |

|

15,792 |

|

Proceeds from the exercise of options |

|

|

|

2 |

|

228 |

|

Asset finance |

|

|

|

125 |

|

- |

|

Cost of issue of share capital |

|

24 |

|

(1,707) |

|

(877) |

|

Lease finance Charge |

|

|

|

(29) |

|

(41) |

|

Lease payments |

|

22 |

|

(498) |

|

(520) |

|

Net cash flows from financing activities |

|

|

|

25,366 |

|

14,623 |

|

Net increase/(decrease) in cash and cash equivalents |

|

|

|

(1,057) |

|

(11,992) |

|

Cash and cash equivalents at the start of the year |

|

|

|

15,374 |

|

27,366 |

|

Cash and cash equivalents at the end of the year |

|

20 |

|

14,317 |

|

15,374 |

|

|

|

|

|

|

|

|

Notes forming part of the financial information

1. Corporate information

AFC Energy Plc (the Company) is a public limited company incorporated in England & Wales. The address of the registered office is Unit 68.3, Dunsfold Park, Cranleigh, Surrey, GU6 8TB. The Company is quoted on the AIM Market of the London Stock Exchange with the ticker symbol LSE: AFC.

The principal activity of the Company is the development and manufacturing of fuel cells and development of fuel processing technology and equipment.

2. Accounting policies

Accounting convention

The final results for the year ended 31 October 2025 were approved by the Board of Directors on 24 February 2026. The final results do not constitute full accounts within the meaning of section 434 of the Companies Act 2006 but are derived from audited financial information for the year ended 31 October 2025 and the year ended 31 October 2024. This announcement is prepared on the same basis as set out in the audited statutory accounts for the year ended 31 October 2025. The accounts for the years ended 31 October 2025 and 31 October 2024, upon which the auditors issued unqualified opinions, also had no statement under section 498(2) or (3) of the Companies Act 2006. While the financial information included in this results announcement has been prepared in accordance with the recognition and measurement criteria of UK adopted international accounting standards (IFRS), this announcement does not in itself contain sufficient information to comply with IFRS.

The Company has taken advantage of the exemption under Section 402 of the Companies Act 2006, which allows a parent company not to prepare consolidated financial information where its subsidiaries are immaterial both individually and in aggregate.

The Directors have assessed the size, nature, and financial impact of the company's subsidiaries and have concluded that they are immaterial for the purpose of presenting a true and fair view of the company's financial position. Accordingly, the company has not prepared consolidated financial information and instead has prepared individual financial information in accordance with applicable accounting standards.

The company accounts for its investment in joint ventures at cost in accordance with IAS 27 Separate Financial Statements. For further details refer to the accounting policy note below.

This financial information is prepared in pounds sterling and rounded to the nearest thousand.

Going concern

The Directors have prepared and reviewed forecasts for the period ending February 2027 which they consider to be the appropriate period for assessing going concern. Whilst events and conditions beyond this period of assessment have been considered. In the judgement of the directors, such events and conditions do not require an extension to the period of assessment. Longer-term factors are included in the Financial Review section within the Strategic report.

The base case forecast predominantly includes the continuation of the development of the HY-5 ammonia cracker and the next generation of Fuel Cell products together with their associated costs and the fixed running costs of the business offset by a moderate volume of equipment and gas sales from the products developed. The sales commence in September 2026 and ramp steadily. In this base case scenario, the forecasts show that the business has sufficient resources throughout the assessment period.

As with prior years, the Directors have applied sensitivities to the above base case when considering their opinion on going concern. The sensitivities considered were:

• A 50% reduction in sales volumes

• A 6-month slippage in project delivery

• The timing and quantum of expected R&D tax credits

These sensitivities have been applied without any management action and the Directors have the ability to control the cost base as well as slow down the pace of development in order to preserve cash if one or more of the scenarios became a reality.

Given the outcome of the assessment above, the directors have a reasonable expectation that the Company has adequate resources to continue in operational existence for the foreseeable future, being the period to 28 February 2027. Accordingly, the directors continue to adopt the going concern basis of preparation in this financial information.

Standards, amendments, and interpretations to published standards not yet effective.

The following amendments to International Financial Reporting Standards (IFRS), issued by the International Accounting Standards Board (IASB) and endorsed by the UK, are effective for annual periods beginning on or after 1 November 2024. The Company has adopted these amendments from 1 November 2024, where applicable, and their adoption has not had a material impact on the Company's results, financial position, or disclosures:

· IAS 1 (amended) - Classification of Liabilities as Current or Non-current; Non-current Liabilities with Covenants: Amends the requirements for classifying liabilities as current or non-current and introduces new disclosure requirements for covenants (IAS 1.69-76, 76ZA-76ZB).

· IFRS 16 (amended) - Lease Liability in a Sale and Leaseback: Amends the measurement requirements for lease liabilities arising in sale and leaseback transactions (IFRS 16.100A-100B).

· IAS 7 and IFRS 7 (amended) - Supplier Finance Arrangements: Introduces new disclosure requirements for supplier finance arrangements (IAS 7.44F-44I, IFRS 7.39A-39C).

The following standard and amendments issued by the IASB have been endorsed by the UK and have not been adopted by the Company. The Company intends to adopt these new and amended standards and interpretations, if applicable, when they become effective:

· IAS 21 (amended) - Lack of Exchangeability: Provides guidance on how to determine the spot exchange rate when exchangeability between two currencies is lacking (IAS 21.8A-8D), effective for annual periods beginning on or after 1 January 2025.

· IFRS 18 - Presentation and Disclosure in Financial Statements: A new standard replacing IAS 1, effective for annual periods beginning on or after 1 January 2027.

· IFRS 19 - Subsidiaries without Public Accountability: Disclosures: Provides reduced disclosure requirements for eligible subsidiaries, effective for annual periods beginning on or after 1 January 2027.

· Amendments to IFRS 9 and IFRS 7 - Classification and Measurement of Financial Instruments: Amendments relating to financial assets with ESG-linked features and settlement of financial liabilities by electronic payments, effective for annual periods beginning on or after 1 January 2026

Capital policy.

The Company manages its equity as capital. Equity comprises the items detailed within the principal accounting policy for equity and financial details can be found in the statement of financial position. The Company adheres to the capital maintenance requirements as set out in the Companies Act 2006.

Revenue recognition

Revenue is recognised in accordance with IFRS 15 using the following five-step model:

· Identify the contract with a customer

· Identify performance obligations

· Determine the transaction price

· Allocate the transaction price to performance obligations

· Recognise revenue as performance obligations are satisfied

Revenue arises from:

· Sale of goods and parts

· Sale of services and maintenance

· Short-term rental contracts

Contracts are assessed to determine whether performance obligations are satisfied at a point in time or over time:

· Point in time: Standard product sales are recognised when control transfers to the customer, typically at factory or site acceptance.

· Over time: Customised products, rentals, and long-term service agreements are recognised based on progress toward completion, using input or output methods as appropriate.

Consideration received in advance of performance is recorded as deferred revenue; conversely, performance ahead of consideration is recorded as a contract asset.

Government grants

Government grants are recognised where there is reasonable assurance that the grant will be received and all attached conditions will be complied with. When the grant relates to an expense item, it is recognised as income on a systematic basis over the periods that the related costs, for which it is intended to compensate, are expensed. The company presents grants related to an expense item as other operating income in the statement of comprehensive income.

When the grant relates to an asset, it is recognised as other operating income in equal amounts over the expected useful life of the related asset.

Foreign currency

The financial information of the Company is presented in the currency of the primary economic environment in which it operates (the functional currency) which is pounds sterling. In accordance with IAS 21, transactions entered by the Company in a currency other than the functional currency are recorded at the rates ruling when the transactions occur.

At each Statement of Financial Position date, monetary items denominated in foreign currencies are retranslated at the rates prevailing at the date of the Statement of Financial Position.

Inventory

Inventory is recorded at the lower of actual cost and net realisable value, applying the average cost methodology.

Work in progress comprises direct labour, direct materials, and direct overheads. Direct labour is allocated on an input basis that reflects the consumption of those resources in the production process.

Cash and cash equivalents

For the purpose of the statement of cash flows, cash and cash equivalents comprise cash balances and bank overdrafts that form an integral part of the Company's cash management process. They are recorded in the statement of financial position and valued at amortised cost.

Restricted cash represents bank deposit accounts where disbursement is dependent upon certain contractual performance conditions.

Term deposits

Term deposits with original maturities exceeding three months are not classified as cash and cash equivalents under IAS 7. These instruments are instead recognised as short‑term investments (or financial assets), with their carrying amount based on amortised cost. Any interest income is accrued and recognised in profit or loss over the deposit period, consistent with the effective interest method.

Other receivables

These assets are initially recognised at fair value and are subsequently measured at amortised cost less any provision for impairment.

Property, plant, and equipment

Property and equipment are stated at cost less any subsequent accumulated depreciation and impairment losses. Where parts of an item of property and equipment have different useful lives, they are accounted for as separate items of property and equipment.

Depreciation is charged to the statement of comprehensive income within cost of sales and/or operating expenses on a straight-line basis over the estimated useful lives of each part of an item of plant, machinery, and equipment. Depreciation of the assets commences when the assets are available for use. The estimated useful lives are as follows:

|

Decommissioning asset |

Life of the contract |

|

|

Leasehold improvements |

Life of the lease |

|

|

Plant, machinery and equipment |

3 to 10 years |

|

|

|

|

|

Expenses incurred in respect of the maintenance and repair of property and equipment are charged against income when incurred. Refurbishment and improvement expenditure, where the benefit is expected to be long lasting, is capitalised as part of the appropriate asset.

The useful economic lives of tangible fixed assets are reviewed annually, and any revision is accounted for as a change in accounting estimate and the net book value of the asset, at the time of the revision, is depreciated over the remaining revised economic life of the asset.

Right-of-use assets

At inception each contract is assessed as to whether it conveys the right to control the use of an identified asset and obtain substantially all the economic benefits from the use of that asset, for a period in exchange for consideration. If so, the contract should be accounted for as a lease and the Company should recognise a right-of-use asset, and related lease liability, at the lease commencement date.

The right-of-use assets comprise the corresponding lease liability, lease payments made before the commencement date, less any lease incentives received and any initial direct costs. They are subsequently measured at cost less accumulated depreciation and impairment losses. The lease liability is initially measured at the present value of the lease payments and discounted using the interest rate implicit in the lease or, if that rate cannot be determined, the incremental borrowing rate is used. The lease liability continues to be measured at amortised cost using the effective interest method. It is remeasured when there is a change in the future lease payments. When the lease liability is remeasured in this way, a corresponding adjustment is made to the carrying amount of the right-of-use asset.

At lease commencement date, a right-of-use and lease liability are recognised on the statement of financial position. The right-of-use asset is measured at cost, which comprises the initial measurement of the lease liability, any initial direct costs incurred, an estimate of costs to dismantle and remove the asset at the end of the lease term and any lease payments made in advance of the lease commencement date.

Lease payments included in the measurement of the lease liability are made up of fixed payments (including in-substance fixed), variable payments based on an index or rate, amounts expected to be payable under a residual value guarantee and payments arising from options reasonably certain to be exercised.

After initial measurement, the liability will be reduced for payments made and increased for interest. It is remeasured to reflect any reassessment or modification, or if there are changes to in-substance payments. Interest expense is recognised in finance costs in the statement of comprehensive income.

Right-of-use assets are depreciated on a straight-line basis over the shorter of the lease term and the estimated useful lives of the assets. The depreciation expense is recognised within operating costs or cost of sales depending on the nature of the underlying asset.

When the lease liability is remeasured, the corresponding adjustment is reflected in the right-of-use asset, or profit and loss if the right-of-use asset is already reduced to zero.

Short-term leases and low value assets are accounted for using the practical expedients set out in IFRS 16 and the payments are recognised as an expense in profit or loss on a straight-line basis over the lease term.

The Company has elected not to recognise right-of-use assets and lease liabilities for leases of less than 12-months and leases of low value assets. These largely relate to short-term rentals of equipment. The lease payments associated with these leases are expensed on a straight-line basis over the lease term.

Intangible assets

The useful economic lives of intangible fixed assets are reviewed annually, and any revision is accounted for as a change in accounting estimate and the net book value of the asset, at the time of the revision, is amortised over the remaining revised economic life of the asset. Amortisation only commences when the asset is available for use.

Development costs

Development expenditures on an individual project are recognised as an intangible asset when the Company can demonstrate:

· The technical feasibility of completing the intangible asset so that the asset will be available for use or sale

· Its intention to complete and its ability and intention to use or sell the asset

· How the asset will generate future economic benefits

· The availability of resources to complete the asset

· The ability to measure reliably the expenditure during development

Following initial recognition of the development expenditure as an asset, the asset is carried at cost less any accumulated amortisation and accumulated impairment losses. Amortisation of the asset begins when development is complete with key objectives achieved as intended by management, and the asset is available for use. It is amortised over the period of expected future benefit. The amortised period is agreed by management and the Technical Advisory board.

The following periods are used:

Capitalised Development Costs 3 to 5 years

Amortisation is recorded in operating costs. During the period of development, the asset is assessed for impairment annually.

Research costs are expensed as incurred.

Patent, commercial rights and trade marks

Intangible assets that are acquired by the Company are stated at cost less accumulated amortisation and impairment losses. Amortisation of intangible assets is charged using the straight-line method to operating expenses over the following periods:

|

Patents |

5 to 20 years |

|

Commercial rights |

5 years |

|

Trade marks |

5 years |

Investment in joint ventures

The Company holds 50% interest in a joint venture, Speedy Hydrogen Services Limited.

A joint venture is a type of joint arrangement whereby the parties that have joint control of the arrangement have rights to the net assets of the joint venture. Joint control is the contractually agreed sharing of control of an arrangement, which exists only when decisions about the relevant activities require the unanimous consent of the parties sharing control.

The Company's investment in its joint venture is initially recognised at cost, including directly attributable transaction costs. Subsequently, the carrying amount is adjusted for any impairment losses, if applicable. The Company assesses the investment for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable.

Impairment testing of intangible assets and property, plant, and equipment

At each statement of financial position date, the carrying amounts of the assets are reviewed to determine whether there is any indication that those assets have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated to determine the extent of the impairment loss (if any). In assessing whether an impairment is required, the carrying value of the asset is compared with its recoverable amount. The recoverable amount is the higher of the fair value less costs of disposal (FVLCD) and value in use (VIU).

Financial instruments

Financial instruments are measured on initial recognition at fair value, plus, in the case of financial instruments other than those classified as fair value through profit or loss (FVTPL), directly attributable transaction costs. Receivables are initially recognised at transaction price. Financial instruments are recognised when the Company becomes a party to the contracts that give rise to them and are classified as amortised cost, fair value through profit or loss or fair value through other comprehensive income, as appropriate. The Company considers whether a contract contains an embedded derivative when the entity first becomes a party to it. The embedded derivatives are separated from the host contract if the host contract is not measured at fair value through profit or loss and when the economic characteristics and risks are not closely related to those of the host contract. Reassessment only occurs if there is a change in the terms of the contract that significantly modifies the cash flows that would otherwise be required.

In the periods presented the Company does not have any financial assets categorised as FVTPL or FVOCI.

Financial assets at amortised cost

A financial asset is measured at amortised cost if it is held within a business model whose objective is to hold assets to collect contractual cash flows and its contractual terms give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding and is not designated as FVTPL. Financial assets classified as amortised cost are measured after initial recognition at amortised cost using the effective interest method, less any provision for impairment Cash, restricted cash, trade receivables, and certain other assets are classified as, and measured at, amortised cost.

Financial liabilities

Financial liabilities are classified as measured at amortised cost or FVTPL. A financial liability is classified as at FVTPL if it is classified as held-for-trading, it is a derivative or it is designated as such on initial recognition. Financial liabilities at FVTPL are measured at fair value and net gains and losses, including any interest expense, are recognised in profit or loss.

Other financial liabilities are subsequently measured at amortised cost using the effective interest method. Gains and losses are recognised in net earnings when the liabilities are derecognised as well as through the amortisation process. Borrowing liabilities are classified as current liabilities unless the Company has an unconditional right to defer settlement of the liability for at least 12 months after the statement of financial position date. Accounts payable and accrued liabilities and lease liabilities are classified as, and measured at, amortised cost.

Impairment of financial assets

A loss allowance for expected credit losses is recognised in the Statement of Comprehensive Income for financial assets measured at amortised cost. At each year end date, on a forward-looking basis, the Company assesses the expected credit losses associated with its financial assets (such as trade receivables) carried at amortised cost.

The expected loss rates are based on the historical credit losses adjusted to reflect current and forward-looking information on economic factors affecting the ability of the customers to settle the receivables.

The impairment methodology applied depends on whether there has been a significant increase in credit risk. The expected credit losses are required to be measured through a loss allowance at an amount equal to the 12-month expected credit losses (expected credit losses that result from those default events on the financial instrument that are possible within 12 months after the reporting date), or full lifetime expected credit losses (expected credit losses that result from all possible default events over the life of the financial instrument). A loss allowance for full lifetime expected credit losses is required for a financial instrument if the credit risk of that financial instrument has increased significantly since initial recognition.

Derecognition of financial assets and liabilities

A financial asset is derecognised when either the rights to receive cash flows from the asset have expired or the Company has transferred its rights to receive cash flows from the asset or has assumed an obligation to pay the received cash flows in full without material delay to a third party. If neither the rights to receive cash flows from the asset have expired nor the Company has transferred its rights to receive cash flows from the asset, the Company will assess whether it has relinquished control of the asset or not. If the Company does not control the asset, then derecognition is appropriate. A financial liability is derecognised when the associated obligation is discharged, cancelled, or expires.

When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as the derecognition of the original liability and the recognition of a new liability. The difference in the respective carrying amounts is recognised in the statement of Comprehensive Income.

Share-based payment transactions

The fair value of options granted under the Employee Share Option Plan, the Employee Performance Share Plan and the Save-As-You-Earn scheme are recognised as an employee benefits expense, with a corresponding increase in equity. The total amount to be expensed is determined by reference to the fair value of the options granted: