MTVH unaudited results Y/e 31 Mar 2025

Metropolitan Housing Trust Ltd / Metropolitan Funding PLC

Metropolitan Housing Trust (MHT), trading as MTVH, announces unaudited consolidated financial results for the year ended 31 March 2025

Continued strong performance and delivery for our residents in 2024/25

Overview and highlights

o Total revenue increased to £454m (FY24; £421m)

§ Revenue from rent and service charges £381m (FY24: £349m) driven by the government's social rent increase of 7.7%

§ Higher sales of new homes (289 FY25 vs 287 FY24) resulted in £7.6m increase in first tranche sales revenue year-on-year

o Underlying operating surplus £148m (FY24: £127m)

§ Adjusted operating margin 33% (FY24: 30%)

§ Operating margin 30% (FY24: 4%)

§ Operating surplus* £136m (FY24: £17m)

§ Surplus before tax £47.8m (2024: Loss before tax of £80.3m)

o Our development programme delivered 544 new homes in the full year through partnership projects such as Clapham Park and Cambourne West.

§ Value of assets under construction totalled £626m (FY24: £419m)

§ Sales of 289 units completed (FY24: 287)

o Investment in our residents' homes

§ Capitalised improvement works to our estate £47.5m (FY24: £33.0m)

o £723m (March 24: £846m) of available liquidity

o S&P Group rating of A- (Stable outlook), unchanged following the MTVH Rating Review in December 2024, and the change to the corporate structure 31 December 2024, making MHT the group parent.

o Fitch Ratings A- (Stable outlook) since September 2024.

o Ritterwald refreshed the Sustainable Housing Certification, moving MTVH up to Frontrunner for all criteria covering Social and Governance, and now Environmental criteria.

*As a not-for-profit Registered Provider our Total Surplus is re-invested to maintain existing homes and build more new homes.

Mel Barrett, Chief Executive, commented:

"I am pleased to announce another set of strong financial results for MTVH which underlines the resilience of our model and the performance of the team. This underlying financial strength allows us to meet the multiple demands of maintaining and improving existing homes, funding building safety remediation, delivering quality customer service while still developing the new affordable homes the country so desperately needs.

I am particularly proud of our efforts to develop and improve our Customer Voice Framework which provides residents with meaningful opportunities to influence the decisions we make. In the past year, residents have influenced the development of a new Customer Experience strategy, customer communications, and the roll-out of our new CRM system all of which are significant steps in our journey to improve our services to our residents.

In our residents' communities we have continued to work with public sector and charity partners to create integrated systems of support that help residents to live well. The cost of living crisis continues for many of our residents and over the year we delivered money advice that created financial savings of £3.4m for residents.

Providing safe, warm and affordable homes is core to our purpose and the foundation on which people can build successful lives. Therefore, we remain ambitious to deliver new affordable homes and there are 4,970 homes in our 5-year development pipeline. Our financial performance in 2024/25 demonstrates successful delivery of the multi-tenure cross subsidy model with initial equity stakes in shared ownership homes, along with our Shared Ownership staircasing, redemptions and surpluses derived from our Joint Venture partnerships, achieving more than £39m in operating surplus. This contributed significantly to our overall surplus that we reinvest into maintaining and building more affordable homes.

This is my first set of full year results as Chief Executive of MTVH and I want to offer my thanks to the whole team for their effort and hard work to deliver for our residents over the past year. To build on these strong foundations and secure further sustainable success we are working on our corporate strategy for 2026 to 2031. This new strategy will be informed through consultation with residents, colleagues and stakeholders and insights from our recent regulatory inspection. I am excited about what we can achieve in the future."

Senior Management Changes

In February we announced the retirement of our CFO, Ian Johnson, later in the Autumn. The process for the selection of his replacement is well advanced and should be announced before the end of June 2025.

Segmental performance

Trading overview

Total revenue including home sales is c 7% higher than last year as a result of the 7.7% rent increases and higher sales revenues from First Tranche Sales. Revenues from our other operations, including Care & Support and the market rent portfolio were slightly lower at £36m (2024: £40m), owing mainly to development agency services growth, but offset by a withdrawal from some of our Care & Support activity.

Turnover from sales was £46m (FY24: £54m) as we sold 289 units and at 30 March 2025, we had 95 unsold units, only 74 are unsold over 90 days, with a sales value of £8.4m (FY24: £5.8m). While sales are currently in line with expectations, we remain well-placed if the sales market strengthens following reductions in interest rates.

Net surplus from rental operations (i.e. net rents less total operating costs) for FY25 was 77% higher than last year, reflecting strong cost control in a high inflation and increasingly challenging service environment. Gross margin from First Tranche sales increased to 31% (FY24 15%) compared to the same period last year.

Operating costs were £328m (FY24: £319m) up 3%. Key to this increase was the general pay rise of 5%, general inflation on contractor costs along with continued increased investment in our repairs and compliance solution. Surplus from Development activities increased to £53.9m (FY24: £46.4m) largely due to Homebuy Loan redemptions and the Strategic Asset Management (SAM) sales. Staircasing surplus was £12.5m (FY24: £10.3m) as we completed 321 staircasing transactions (FY24: 263).

The Group recorded a surplus after tax of £48m (2024: loss of £80m) after net interest costs of £91m (2024: £90m). Other comprehensive income includes a credit of £9m (2024: charge of £15m) in respect of our defined benefit pension obligations, and a £10m credit (2024: £3m credit) in respect of the movement in fair value of the Group's financial hedging derivatives.

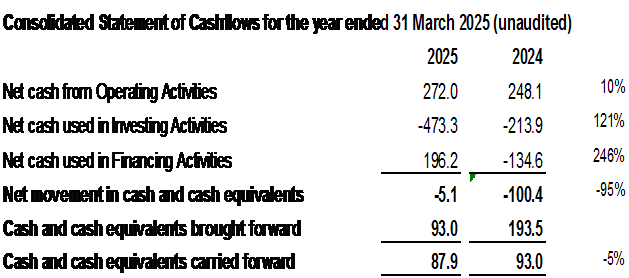

Cashflow from operating activities is up 10% at £272m (FY24: £248m) driven by higher rental and sales income. Development expenditure in new projects totalled £442m (FY24: £280m) as MTVH continued to develop new homes, with expenditure largely funded by the drawdown of debt.

The organisation completed 544 homes during the year (FY24: 293) and has a sufficiently identified pipeline to meet our commitments to the GLA and homes England (HE) 2021-2026 programme.

Net interest costs (excluding mark to market movements on derivatives) are just £1m higher than last year, despite increased debt resulting from greater development spend, offset as rates started to fall, and the increased use of short-term interest rate swaps. At 31 March 2025, we had £723m (March 2024: £846m) of available liquidity (both cash and committed facilities).

Facilities have been drawn to cover development spend, resulting in total debt of £2.2bn (Mar 24: £1.9bn). EBITDA interest cover was 1.9 times (2024: 2.0 times).

We completed on £150m of additional secured debt at the end of the financial year which reduced the charged security available to £491m. Liquidity management remains a key focus to mitigate the impact of a wider economic downturn. At the same time, our relatively low gearing, at 39%, and available security, provides further resilience to shock.

Thames Valley Housing Association's Standard & Poor's credit rating was unchanged in December 2024 at A- with the outlook Stable, and following the change to the corporate structure on 31 December 2024 making MHT the group parent. Fitch Ratings downgraded the organisation rating to A- (Stable) in October 2024.

Full-year outlook

This outlook statement is subject to uncertainty/unforeseen market and business interruption as a result of uncertainty over the direction of government policy, as well as the impact of US tariffs and the risk of a world recession. The economic and geopolitical environments remain challenging, with higher levels of inflation and interest rates, along with continuing concerns over energy supplies. The 2024 elections in the UK and USA have resulted in significant changes in economic policy and international trade, that could cause inflation, supply chain challenges as well as higher unemployment which could impact the sector.

Trading

The core housing business will see revenues increase by the CPI+1 rent settlement of 2.7%. This will boost revenues, but operating margins will remain under pressure since operating costs are also expected to rise. Similarly, the sustained high cost of term debt continues to put pressure on Interest Cover ratios, reducing the capacity to deliver on our corporate objectives. This will impact on our capacity to build new homes.

We expect to invest a record amount in new homes development as part of our current programme to build around 1,000 new homes per year, however without an increase in direct revenue support from the government our capacity to build new homes will be limited.

Investment in building safety

Fire safety and damp and mould works have increased investment to our existing homes. This is a sector issue. The longer-term impact of remediation obligations has led to a reduction in our capacity to develop new homes, particularly homes for sale.

We are continuing with our Safer Buildings programme driven by our desire to put customer safety first. We expect that developers/warranty providers will pick up the costs of remediation for newer buildings where this relates to construction defect.

MHT, trading as Metropolitan Thames Valley, will report results for the six months ended 30 September 2025 in winter 2025.

Consolidated financials

Cashflow

Enquiries

Please contact Donald McKenzie, Director of Corporate Finance, on 07738-714126 or at donald.mckenzie@mtvh.co.uk

This information for investors is also available on our website:

https://www.mtvh.co.uk/about-us/investors/

Notes

1) Operating margin is operating surplus/turnover

2) Metropolitan Housing Trust (MHT) is the parent of the group trading under the brand of Metropolitan Thames Valley (MTVH). Thames Valley Housing Association (TVHA) is a wholly owned subsidiary of MHT and MHT owns 100% of the shares of Metropolitan Funding Plc.

Disclaimer

The information in this announcement of unaudited consolidated interim results has been prepared by the Metropolitan Housing Trust Group and is for information purposes only.

The unaudited results announcement should not be construed as an offer or solicitation to buy or sell any securities, or any interest in any such securities, and nothing herein should be construed as a recommendation or advice to invest in any such securities.

This unaudited results announcement contains certain 'forward-looking' statements reflecting, among other things, our current views on markets, activities and prospects. By their nature, forward looking statements involve a number of risks, uncertainties or assumptions that could cause actual results to differ materially from those expressed or implied by those statements. Actual outcomes may differ materially. Such statements are a correct reflection of our views only on the publication date and no representation or warranty is given in relation to them, including as to their completeness or accuracy or the basis on which they were prepared. Financial results quoted are unaudited. We do not undertake to update or revise such public statements as our expectations change in response to events. Accordingly undue reliance should not be placed on forward looking statements.

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.

Latest directors dealings

- 1 day ago TotalEnergies SE

- 1 day ago Bango

- 1 day ago Zigup

- 1 day ago PureTech Health

- 1 day ago Peel Hunt Limited NPV