Interim Results

Summary by AI BETAClose X

2 June 2026

GOOCH & HOUSEGO PLC

("G&H", the "Company" or the "Group")

Interim Results

Gooch & Housego PLC (AIM: GHH), the specialist manufacturer of optical components and systems, today announces its interim results for the six months ended 31 March 2026 ('H1 2026' or the 'Period').

Key Financials

|

Period ended 31 March |

H1 2026 |

H1 2025 |

Change

|

|

Revenue |

£81.9m |

£70.9m |

+15.5% |

|

Adjusted profit before tax* |

£5.8m |

£5.1m |

+13.9% |

|

Adjusted basic earnings per share* |

16.4p |

15.0p |

+9.3% |

|

Net debt excluding IFRS 16 |

£36.6m |

£24.1m |

+£12.5m |

|

Net debt including IFRS 16 |

£49.8m |

£35.5m |

+£14.3m |

|

|

|

|

|

|

Statutory profit before tax |

£3.3m |

£2.9m |

+15.8% |

|

Statutory basic earnings per share |

9.2p |

8.1p |

+13.6% |

|

|

|

|

|

|

Interim dividend per share |

4.9p |

4.9p |

- |

*Adjusted for amortisation of acquired intangible assets and non-recurring items.

Key Highlights

§ Revenue increased by 15.5% to £81.9m, or 9.1% on an organic, constant currency basis.

§ Aerospace & Defence revenue increased by 51.7% to £35.6m (H1 2025: £23.5m), reflecting strong demand, enhanced capabilities and benefits from recent acquisitions.

§ Adjusted operating profit increased by 16.9% to £7.2m, with operating profit margins improving slightly to 8.8% (H1 2025: 8.7%).

§ A&D segment profitability significantly improved to £3.6m, demonstrating the benefits of the Group's strategic focus and operational improvement programme.

§ Order book increased to record £167.3m (Sept 2025: £142.4m), up 16.5% on a constant currency basis, providing near full cover for expected FY2026 revenue.

§ Net debt leverage at 1.5x (Sept 2025: 1.3x). Committed debt facility increased to $70m.

§ Phoenix Optical and Global Photonics integration now largely complete, with capacity expanded supporting customer demand.

§ FY2026 expectations unchanged; Board remains confident in further profitable growth and progress towards mid-teens returns over the medium-term.

Charlie Peppiatt, Chief Executive Officer of Gooch & Housego, commented: "I am pleased with the positive progress that G&H has made in the first half of the financial year. The record order book growth in the period demonstrates the increased confidence our customers have in G&H to provide them with their most complex photonics and optical systems requirements. This enlarged order book gives us stronger forward visibility than we have had historically and reflects the benefits of our strengthened positions in structurally attractive end-markets. We remain focused on converting this demand through disciplined capacity expansion, improved operational execution and continued supply-chain resilience. The strategic actions taken over the last few years, including important speed-to-value acquisitions, have started to translate into improved financial and operational performance, and the Group is well-positioned to meet this increased demand.

"While we continue to navigate the significant macroeconomic uncertainties, the recovery in our Industrial and Semiconductor markets, coupled with record demand from US and European Aerospace and Defence sectors, firmly supports our path to achieving mid-teens returns over the medium term."

Analyst meeting

A meeting for analysts will be held at 9.30 a.m. today at the offices of Burson Buchanan, Rose Court, 2 Southwark Bridge Road, London SE1 9HS. To register attendance, please contact Burson Buchanan at: G&H@buchanan.uk.com.

An audiocast of the presentation will be made available via the Group's website at 9.30am today https://gandh.com/investors/.

For further information please contact:

|

Gooch and Housego PLC |

|

|

Charlie Peppiatt, Chief Executive Officer |

Tel: +44 (0) 1460 256 440 |

|

James Corte, Chief Financial Officer |

|

Burson Buchanan (Financial Communications) |

|

|

Henry Harrison-Topham / Sophie Wills / Abby Gilchrist |

Tel: +44 (0) 20 7466 5000 |

|

|

|

Investec Bank plc (NOMAD and Broker) |

|

|

Chris Baird / Charles Craven / Carlton Nelson |

Tel: +44 (0) 20 7597 5970 |

|

|

Notes to editors:

Gooch & Housego is a photonics technology business with operations in the USA and Europe. A world leader in its field, the company researches, designs, engineers and manufactures advanced photonic systems, components and instrumentation for applications in the Aerospace and Defence, Industrial and Telecom, and Life Sciences sectors. World-leading design, development and manufacturing expertise is offered across a broad range of complementary technologies. It is headquartered in Ilminster, Somerset, UK. For more information please visit www.gandh.com.

This announcement contains certain forward-looking statements that are based on management's current expectations or beliefs as well as assumptions about future events. These are subject to risk factors associated with, amongst other things, the economic and business circumstances occurring from time to time in the countries and sectors in which G&H operates. It is believed that the expectations reflected in these statements are reasonable but they may be affected by a wide range of variables which could cause actual results, and G&H's plans and objectives, to differ materially from those currently anticipated or implied in the forward-looking statements. Investors should not place undue reliance on any such statements. Nothing in this announcement should be construed as a profit forecast.

Operating and Financial Review

Performance Overview

The Group's revenue for the period totalled £81.9m (H1 2025: £70.9m) representing 15.5% growth over the prior year comparator period, or 9.1% on an organic, constant currency basis. Demand from the Group's Aerospace & Defence ('A&D') market has remained strong and continues to grow. Revenue from the Group's industrial laser and semiconductor markets also improved with encouraging signs that the recovery in semiconductors is now underway.

Revenue in the Group's Industrial segment was broadly flat on prior year or 4.6% higher on an organic, constant currency basis. We saw some improvement in our industrial laser and semiconductor markets in the period. Encouragingly, order intake across this sector has increased significantly and demand from our subsea data cable market remains strong.

Revenue into the Group's A&D markets grew by 51.7% or 26.0% on an organic, constant currency basis, helped by our refocused go-to-market strategy combined with the commercial synergy benefits arising from recent acquisitions of Global Photonics and Phoenix Optical. Operational improvements and our enhanced germanium processing capabilities drove margin improvement, and, for the first time, this sector was a major contributor to the Group's profitability in H1 2026.

Revenue in the Group's Life Sciences segment was down by 7.7% or 5.8% on an organic, constant currency basis. We saw continued disruption to our Pockels Cells production from materials availability particularly in the first quarter. Production increased in the second quarter as we qualified alternative materials suppliers and is expected to continue to ramp up in the second half. Revenues from our medical diagnostics products were lower due to phasing of customer demand and are expected to improve throughout H2 2026.

Overall, due to the volume growth and the benefits of our operational efficiency and supply chain actions, underlying operating profit increased by 16.9% to £7.2m (H1 2025: £6.2m). This represents a return on sales of 8.8% (H1 2025: 8.7%).

The integration of the Phoenix Optical and Global Photonics businesses is now largely complete and the enhanced offering the Group now provides has been key in helping secure new orders from defence customers in the US, UK and Europe.

The Group's order book increased to £167.3 million (30 September 2025: £142.4 million). The growth on an organic constant currency basis was 16.5%. The level of enquiries for the Group's products and services remains high, especially in defence, from both existing and new customers.

Order book growth was not limited to one end-market. Aerospace & Defence remained particularly strong, supported by customer demand for advanced optical systems and regional supply assurance. Industrial order intake also improved, aligned to the recovery in semiconductor-related markets, while Life Sciences performance remained affected by customer phasing and legacy product transition activity.

The geopolitical and macroeconomic background remains volatile with fluid tariff policies, retaliatory measures and continued unrest in Ukraine and the Middle East. G&H's direct exposure to those countries that have been subjected to the current most significant tariff increases on imports to the US is limited, but we remain vigilant to the more general market instability, potential for order delays and inflationary impacts of increasing global tariffs. We have been able to re-source our supply of certain key raw materials where availability has been restricted and continue to hold higher stock levels. We are passing on cost base increases arising from these developments through higher pricing where possible. The Group has also continued to strengthen its position in germanium-related products, which are important to a number of Aerospace & Defence and Semiconductor applications. While raw material availability remains variable, actions taken to optimise sourcing and increase resilience have improved the Group's ability to support customer demand.

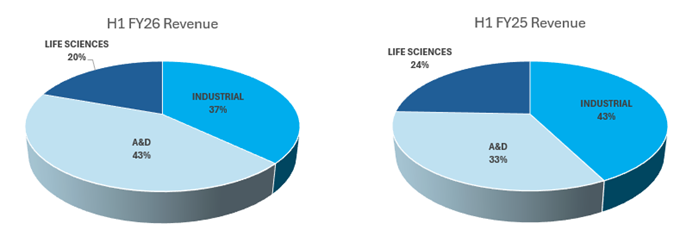

Revenue

|

Six months ended 31 March |

2026 |

2025 |

|

||

|

From continuing operations |

£'M |

£'M |

% Change |

|

|

|

Industrial |

30.3 |

30.1 |

0.7% |

||

|

Aerospace & Defence |

35.6 |

23.5 |

51.7% |

||

|

Life Sciences |

16.0 |

17.3 |

(7.7%) |

||

|

Group Revenue |

81.9 |

70.9 |

15.5% |

||

Products and Markets - Industrial

Gooch & Housego's principal industrial markets are industrial lasers, telecommunications, sensing and semiconductor manufacturing. Industrial lasers are used in a diverse range of high precision material processing applications ranging from microelectronics and semiconductors to automotive manufacturing.

Overall, sales of products by the Group into our industrial markets in the six months ended 31 March 2026 increased by 0.7%, or 4.6% when measured on an organic, constant currency basis, compared with the equivalent period last year. The semiconductor market is now showing strengthening signs of a recovery and we are seeing increased order intake from the semiconductor processing, sensing and advanced microelectronics markets. The scale and phasing of this recovery remains under review, but the improvement in order activity provides greater confidence in the medium-term outlook for the segment.

Adjusted operating profit was slightly ahead of the prior year at £3.8m, and the adjusted return on sales percentage was 12.7% (H1 2025: 12.6%).

Products and Markets - Aerospace & Defence ('A&D')

In A&D the Group continues to strengthen and grow well-established positions in periscopes and sighting systems, target designation and range finding, ring laser gyroscope navigational systems, advanced opto-mechanical subsystems and space-based optical communications. The Group is also seeing increasing involvement in laser directed energy weapon ('LDEW') programmes, where our precision optical and subsystem capabilities are supporting the development of next generation defensive technologies for allied naval and land-based defence applications.

Demand across the sector remains strong as key allied nations continue to prioritise the enhancement of defensive capabilities in response to the evolving global security environment. This has resulted in increased demand for the Group's infrared lens systems and optical assemblies for counter-unmanned aerial systems ('C-UAS'), short-range air defence ('SHORAD'), near-Earth orbit and naval applications, areas where our precision optical expertise and vertically integrated manufacturing capabilities provide a differentiated offering.

The continued recovery and production ramp within the commercial aviation market is also driving increased demand for the Group's ring laser gyroscope ('RLG') products, with customers seeking reliable supply partners capable of supporting higher build rates and long-term programme requirements. Operational improvements across the Group's precision optics facilities have enabled increased throughput and enhanced production efficiency to support this growing demand.

The defence focused investments made through the acquisitions of Artemis Optical, Phoenix Optical Technologies and Global Photonics (Meopta US) combined with our existing enhanced capabilities have further strengthened the Group's defence market position and demonstrated our commitment to expanding manufacturing capacity and technical capability across multiple regions. Aligned to the Group's strategy launched in June 2023, these acquisitions have enhanced our ability to provide customers with a broader integrated optical solutions offering whilst also supporting increasingly regionalised supply chain requirements of allied nations. G&H now has manufacturing and technical capability aligned to UK and European customer requirements as well as dedicated US-based capability supporting North America's growing demand. The combination of these businesses with the Group's existing capabilities continues to support new customer opportunities and reinforces our position as a strategic supplier within the A&D market. Customers are increasingly prioritising security of supply, regional manufacturing capability and vertically integrated optical fabrication, areas where G&H's strengthened UK, European and US footprint provides a differentiated proposition.

Group revenue into the A&D market grew by 51.7%, or 26.0% on an organic constant currency basis compared with the first half of FY 2025. Additional volumes in this segment together with our operational efficiency improvements resulted in the segment generating an adjusted operating profit in the period of £3.6m (H1 2025: £0.6m).

Products and Markets - Life Sciences

G&H has established itself as a trusted supplier in the Life Sciences market, delivering advanced optical components that enhance the performance and reliability of life science instruments. Our contributions span applications such as microscopy, medical diagnostics, biomedical imaging, and laser surgery, where our reputation as a leading provider of advanced optics, fibre optics, acousto-optics, and electro-optics is well recognised globally.

Revenues from our medical diagnostic markets reduced compared with the first half of FY2025. This was principally due to customer demand phasing, with certain customers having procured systems from G&H in FY2025 and moved into installation and qualification phases during H1 of FY2026. A number of customer programmes also remain in clinical trial and regulatory approval phases, with volume production now expected to contribute from FY2027.

As reported in G&H's 2025 Annual Report, the Group has made the decision to end-of-life the majority of its Pockels Cells product lines for the medical lasers market. Last-time-buy activity created elevated short-term demand in these products during the period, which coincided with material supply constraints and production yield challenges at the Group's Cleveland facility.

Management has taken action to qualify alternative material sources and improve in-house production performance. Production increased through the second quarter and is expected to continue to recover in the second half. While these factors affected margins in H1 2026, the Board expects Life Sciences margins to improve as production normalises and customer demand strengthens.

Revenue from the Group's Life Sciences market reduced by 7.7% or 5.8% on an organic, constant currency basis in H1 2026, compared with H1 2025. The reduction in revenue combined with the production and supply chain challenges outlined above, meant that operating profit returns in this segment declined to 4.6% (H1 2025: 12.0%).

Strategy

G&H's strategy to become an 'innovative customer focused technology company' delivered responsibly by making a 'better world with photonics', continues to progress positively and we are now seeing the benefits of having refocused the whole business on delivering sustainable margin growth in the medium term. The successful execution of this value creation strategy will ensure that G&H remains the 'first choice' for all our stakeholders whether that's for our employees, our customers, our shareholders, our eco-system partners or the communities in which we operate. We will offer differentiated performance through four key strategic priorities.

Key Strategic Priorities:

|

The first-half performance provides clear evidence of progress against the Group's strategy: stronger exposure to structurally growing A&D markets, improved operational execution, enhanced regional manufacturing capability, increased supply-chain resilience, active capacity and efficiency improvements, and a higher-quality order book.

Financial Review

Group revenue grew by 15.5% or 9.1% on an organic, constant currency basis. Operating margins progressed slightly to 8.8% from 8.7% in H1 2026, reflecting the benefits of additional volume and the delivery of the strategic actions we are implementing, which were partially offset by the impact of certain supply chain and production challenges particularly in our Life Sciences business.

The Group's spend on R&D totalled £3.9m, up 10.6% on the first half of FY 2025 (H1 2025: £3.5m). We continue to focus on our six vital few R&D workstreams and progress in these areas has been positive. We have invested in engineering resource where necessary and continue to expect these projects to generate in excess of £50m of margin-accretive revenue in the medium term.

The growth in the Group's overheads to £13.0m (H1 2025: £11.9m) reflected the inclusion of the Global Photonics business and, to a lesser extent, the full period effect of Phoenix Optical, combined with inflationary increases to staff salaries.

Underlying operating profit increased by 16.9% to £7.2m (H1 2025: £6.2m). Reported operating profit grew to £4.9m (H1 2025: £4.2m). Further details of the adjustments made between underlying and reported profit measures are set out below.

The Group's interest charges totalled £1.6m (H1 2025: £1.3m). The increased charge was largely due to additional borrowing taken to fund the acquisition of the Global Photonics business in June 2025.

The Group's adjusted effective tax rate was 22.4% (H1 2025: 22.9%). Adjusted earnings per share was 16.4p (H1 2025: 15.0p)

Alternative Performance Measures

In the analysis of the Group's financial performance, alternative performance measures are presented to provide readers with additional information. The interim report includes both statutory and adjusted non-GAAP financial measures. The Directors believe the latter reflect the underlying performance of the business. Items excluded from the adjusted results, together with their prior period comparatives, are set out below.

Reconciliation of adjusted performance measures

|

|

Operating profit |

Net finance costs |

Profit before tax |

Taxation |

Profit after tax from continuing operations |

Earnings per share |

||||||

|

Half Year to 31 March |

2026 £000 |

2025 £000 |

2026 £000 |

2025 £000 |

2026 £000 |

2025 £000 |

2026 £000 |

2025 £000 |

2026 £000 |

2025 £000 |

2026 Pence |

2025 Pence |

|

Reported |

4,874 |

4,156 |

(1,552) |

(1,288) |

3,322 |

2,868 |

(825) |

(776) |

2,497 |

2,092 |

9.2p |

8.1p |

|

Amortisation of acquired intangible assets |

1,519 |

1,097 |

- |

- |

1,519 |

1,097 |

(321) |

(234) |

1,198 |

863 |

4.4p |

3.3p |

|

Restructuring and other costs |

385 |

412 |

- |

- |

385 |

412 |

(67) |

(80) |

318 |

332 |

1.2p |

1.3p |

|

Acquisition and integration costs |

193 |

426 |

- |

- |

193 |

426 |

(26) |

(17) |

167 |

409 |

0.6p |

1.6p |

|

Site closure costs |

- |

64 |

- |

- |

- |

64 |

- |

- |

- |

64 |

- |

0.2p |

|

Local employment litigation costs |

227 |

- |

- |

- |

227 |

- |

(23) |

- |

204 |

- |

0.7p |

- |

|

Interest on deferred consideration |

- |

- |

108 |

184 |

108 |

184 |

(27) |

(50) |

81 |

134 |

0.3p |

0.5p |

|

Adjusted |

7,198 |

6,155 |

(1,444) |

(1,104) |

5,754 |

5,051 |

(1,289) |

(1,157) |

4,465 |

3,894 |

16.4p |

15.0p |

Cash Flow and Financing

In the six months ended 31 March 2026, G&H generated net cash from operations of £3.9m, compared with £2.6m in the same period of FY2025. Working capital levels increased by £4.9m from the end of FY 2025. This was driven by growth in receivables following high levels of invoicing in March which have since largely been converted to cash. The Group's inventory also grew by £1.3m although this was offset by higher trade creditor balances at the end of March. The Group has chosen to increase its inventory of some materials such as Germanium in response to continued uncertainty in their availability as a result of export restrictions imposed by the Chinese government.

In October 2025, deferred consideration of £1m was paid in respect of the Artemis Optical business, which was acquired in July 2023. No further deferred consideration is payable in respect of this acquisition.

Capital expenditure on property, plant and equipment was £3.4m in the period (H1 2025: £2.5m). The principal areas of investment in H1 2026 were in increasing capacity in our Tampa, Florida facility by the installation of a new clean room and optical systems assembly equipment and on additional production equipment for fibre optic modules in Torquay.

On 12 March 2026, the Group extended its revolving credit facility, which now comprises a committed facility of US$70m. As at 31 March 2026 the Group had drawn US$54.8m on its revolving credit facility (September 2025: US$50.2m).

At 31 March 2026 the Group's net debt totalled £49.8m (30 September 2025: £43.9m) including lease liabilities of £13.2m (30 September 2025: £14.0m). Consistent with the Group's borrowing agreements, which exclude the impact of IFRS 16, Leases, our leverage ratio was 1.5 times at 31 March 2026 (30 September 2025: 1.3 times).

Environmental, Social and Governance

In H1 2026, the Group's carbon intensity measure increased by 15.7% due to the recent acquisitions of Phoenix Optical in North Wales and Global Photonics in Tampa, Florida. However, on an organic basis the Group achieved a like for like reduction of 6.4%.

During the period, and as part of the integration of these acquisitions, we will transition these sites' electricity supplies to renewable sources during the second half of the year in line with the Group's stated aim of reducing emissions by 10% per annum.

The Group continues to invest to support its target of being net zero for Scope 1 and 2 emissions by 2035 and Scope 3 by 2050. We are working with the landlord of our facility in Tampa, Florida to explore the installation of solar panels for the onsite generation of electricity.

Our programme to extend ISO 14001 - Environmental Management - to all the Group's sites continues to schedule. We expect our Moorpark, California and Tampa, Florida sites to achieve accreditation in the second half of this financial year and to have all Group's facilities accredited ahead of plan by the end of FY 2027.

The Group manages its activities in this area through the Sustainability Committee of the Board. This Committee is chaired by our non-executive director, Susan Searle. This Committee is supported in its work by a Sustainability subcommittee staffed with representatives from across the Group. The remit of the Sustainability Committee includes oversight of the Group's activities to ensure appropriate adherence to the Group's Ethics & Anti-Corruption, Equality, Diversity & Inclusion, Trade Compliance and Cyber Security policies. We are using the Group's new HR Information System to deliver training content electronically and to use the system to record course completion by employees.

Dividends

An interim dividend of 4.9p per share (H1 2025: 4.9p) has been declared. This dividend will be payable to shareholders on the register as at 19 June 2026 on 24 July 2026.

Prospects and Outlook

The Group's strong H1 2026 performance demonstrates the positive progress the Group continues to make with the deployment of its strategy and highlights the resilience and depth of experience across our leadership team in navigating complex market dynamics. Our growing order book, strengthening market positions and differentiated photonics expertise aligned to structural growth drivers from megatrends, mean we remain confident in our ability to deliver further progress on our journey to mid-teens returns over the medium term and generate value for all our stakeholders.

The Group enters H2 2026 with a record order book, near full revenue cover for FY2026 and strong demand in Aerospace & Defence. Industrial and Semiconductor markets are showing encouraging signs of growth, whilst Life Sciences production disruption is expected to ease through H2 2026.

Although global geopolitical uncertainty and macroeconomic challenges remain, the Group is proactively managing this increased complexity and volatility in global supply chains and remains vigilant regarding operations and inventory planning. Despite these challenges, the Board's expectations for FY2026 are unchanged, and the Group's strengthened market positions, improved operational performance and differentiated photonics capabilities reinforce our confidence in further profitable growth and continued progress to mid-teens returns over the medium term.

Principal Risks and Uncertainties

The principal risks and uncertainties to which G&H is exposed and our approach to managing those risks are unchanged from those identified in the Group's 2025 Annual Report. At the end of 2025 we identified geopolitical risks and raw materials supply as the two most significant for the Group and with the rapidly changing geopolitical landscape those risks have affected the Group in H1 2026.

We continue to strive to limit as much as possible our direct exposure to supply from China. However, in the first half, as explained above, we needed to qualify several Chinese suppliers for certain raw materials which has meant the Group incurred higher tariffs on certain material purchases.

Security of material supply continues to be an important risk for the Group. Our supply chain team has taken actions to mitigate the impact of export restrictions imposed by the Chinese government on certain raw materials. This has ensured continuity of supply overall, although delivery timing has remained variable in certain instances.

Group Income Statement

Unaudited interim results for the 6 months ended 31 March 2026

|

|

|

Half Year to 31 March 2026 (Unaudited) |

Half Year to 31 March 2025 (Unaudited) |

Full Year to 30 September 2025 (Audited) |

||||

|

|

Note |

Underlying |

Non-underlying |

Total |

Underlying |

Non-underlying |

Total |

Total |

|

|

|

£'000 |

£'000 |

£'000 |

£'000 |

£'000 |

£'000 |

£'000 |

|

Revenue |

4 |

81,876 |

- |

81,876 |

70,878 |

- |

70,878 |

150,485 |

|

Cost of revenue |

|

(57,816) |

- |

(57,816) |

(49,310) |

- |

(49,310) |

(103,821) |

|

Gross profit |

|

24,060 |

- |

24,060 |

21,568 |

- |

21,568 |

46,664 |

|

Research and development |

|

(3,911) |

- |

(3,911) |

(3,535) |

- |

(3,535) |

(7,296) |

|

Sales and marketing |

|

(4,720) |

- |

(4,720) |

(4,344) |

- |

(4,344) |

(8,870) |

|

Administration |

|

(9,097) |

(2,324) |

(11,421) |

(7,857) |

(1,999) |

(9,856) |

(23,910) |

|

Other income and expenses |

|

866 |

- |

866 |

323 |

- |

323 |

1,546 |

|

Operating profit / (loss) |

4 |

7,198 |

(2,324) |

4,874 |

6,155 |

(1,999) |

4,156 |

8,134 |

|

Net finance costs |

|

(1,444) |

(108) |

(1,552) |

(1,104) |

(184) |

(1,288) |

(2,807) |

|

Profit / (loss) before income tax expense |

|

5,754 |

(2,432) |

3,322 |

5,051 |

(2,183) |

2,868 |

5,327 |

|

Income tax expense |

6 |

(1,289) |

464 |

(825) |

(1,157) |

381 |

(776) |

(1,791) |

|

Profit / (loss) for the period |

|

4,465 |

(1,968) |

2,497 |

3,894 |

(1,802) |

2,092 |

3,536 |

|

|

|

|

|

|

|

|

|

|

|

Earnings / (loss) per share |

|

|

|

|

|

|

|

|

|

From continuing operations |

|

|

|

|

|

|

|

|

|

Basic earnings per share |

7 |

16.4p |

(7.2p) |

9.2p |

15.0p |

(6.9p) |

8.1p |

13.7p |

|

Diluted earnings per share |

7 |

16.1p |

(7.1p) |

9.0p |

14.8p |

(6.8p) |

8.0p |

13.3p |

|

|

|

|

|

|

|

|

|

|

Group Statement of Comprehensive Income |

Half Year to |

Half Year to |

Full Year to |

|

|

£'000 |

£'000 |

£'000 |

|

Profit for the period |

2,497 |

2,092 |

3,536 |

|

Other comprehensive (expense) / income |

|

|

|

|

(Losses) / gains on cash flow hedges |

(149) |

18 |

8 |

|

Currency translation differences |

683 |

1,737 |

137 |

|

Other comprehensive income for the period |

534 |

1,755 |

145 |

|

Total comprehensive income for the period |

3,031 |

3,847 |

3,681 |

Group Balance Sheet

Unaudited interim results for the 6 months ended 31 March 2026

|

|

|

31 Mar 2026 |

31 Mar 2025

|

30 Sep 2025 |

|

|

|

£'000 |

£'000 |

£'000 |

|

Non-current assets |

|

|

|

|

|

Property, plant and equipment |

|

37,450 |

38,370 |

36,518 |

|

Right of use assets |

|

12,135 |

10,395 |

12,956 |

|

Intangible assets |

|

65,828 |

55,495 |

66,561 |

|

|

|

115,413 |

104,260 |

116,035 |

|

Current assets |

|

|

|

|

|

Inventories |

|

42,380 |

37,597 |

40,794 |

|

Trade and other receivables |

|

48,625 |

37,860 |

42,068 |

|

Current asset investments |

|

761 |

- |

761 |

|

Cash and cash equivalents |

|

4,423 |

5,546 |

7,198 |

|

|

|

96,189 |

81,003 |

90,821 |

|

Current liabilities |

|

|

|

|

|

Trade and other payables |

|

(29,223) |

(22,010) |

(28,542) |

|

Lease liabilities |

|

(2,214) |

(1,881) |

(2,234) |

|

Tax liabilities |

|

(1,233) |

(1,992) |

(2,420) |

|

Deferred consideration |

|

- |

(2,074) |

- |

|

|

|

(32,670) |

(27,957) |

(33,196) |

|

|

|

|

|

|

|

Net current assets |

|

63,519 |

53,046 |

57,625 |

|

|

|

|

|

|

|

Non-current liabilities |

|

|

|

|

|

Borrowings |

|

(41,049) |

(29,604) |

(37,066) |

|

Lease liabilities |

|

(10,998) |

(9,591) |

(11,755) |

|

Provision for other liabilities and charges |

|

(2,014) |

(1,100) |

(2,031) |

|

Deferred consideration |

|

(1,899) |

(1,682) |

(959) |

|

Deferred tax liabilities |

|

(3,913) |

(4,809) |

(4,412) |

|

|

|

(59,873) |

(46,786) |

(56,223) |

|

|

|

|

|

|

|

Net assets |

|

119,059 |

110,520 |

117,437 |

|

|

|

|

|

|

|

Shareholders' equity |

|

|

|

|

|

Called up share capital |

|

5,474 |

5,159 |

5,423 |

|

Share premium account |

|

16,051 |

16,051 |

16,051 |

|

Merger reserve |

|

19,589 |

11,561 |

19,109 |

|

Cumulative translation reserve |

|

5,921 |

6,838 |

5,238 |

|

Hedging reserve |

|

- |

159 |

149 |

|

Retained earnings |

|

72,024 |

70,752 |

71,467 |

|

Total equity |

|

119,059 |

110,520 |

117,437 |

Statement of Changes in Equity

Unaudited interim results for the 6 months ended 31 March 2026

|

|

Share capital account |

Share premium account |

Merger reserve |

Retained earnings |

Hedging reserve |

Cumulative translation reserve |

Total equity

|

|

|

£000 |

£000 |

£000 |

£000 |

£000 |

£000 |

£000 |

|

At 1 October 2024 |

5,159 |

16,051 |

11,561 |

70,375 |

141 |

5,101 |

108,388 |

|

Profit for the period |

- |

- |

- |

2,092 |

- |

- |

2,092 |

|

Other comprehensive income for the period |

- |

- |

- |

- |

18 |

1,737 |

1,755 |

|

Total comprehensive (expense) / income for the period |

- |

- |

- |

2,092 |

18 |

1,737 |

3,847 |

|

Dividends |

- |

- |

- |

(2,140) |

- |

- |

(2,140) |

|

Share based payments |

- |

- |

- |

425 |

- |

- |

425 |

|

At 31 March 2025 (unaudited) |

5,159 |

16,051 |

11,561 |

70,752 |

159 |

6,838 |

110,520 |

|

|

|

|

|

|

|

|

|

|

At 1 October 2025 |

5,423 |

16,051 |

19,109 |

71,467 |

149 |

5,238 |

117,437 |

|

Profit for the period |

- |

- |

- |

2,497 |

- |

- |

2,497 |

|

Other comprehensive (expense) / income for the period |

- |

- |

- |

- |

(149) |

683 |

534 |

|

Total comprehensive income / (expense) for the period |

- |

- |

- |

2,497 |

(149) |

683 |

3,031 |

|

Issue of new shares |

51 |

- |

480 |

- |

- |

- |

531 |

|

Dividends |

- |

- |

- |

(2,272) |

- |

- |

(2,272) |

|

Share based payments |

- |

- |

- |

150 |

- |

- |

150 |

|

Tax on share based payments in equity |

- |

- |

- |

182 |

- |

- |

182 |

|

At 31 March 2026 (unaudited) |

5,474 |

16,051 |

19,589 |

72,024 |

- |

5,921 |

119,059 |

Group Cash Flow Statement

Unaudited interim results for the 6 months ended 31 March 2026

|

|

Half Year to 31 Mar 2026 (Unaudited) |

Half Year to 31 Mar 2025 (Unaudited) |

Full Year to 30 Sep 2025 (Audited) |

|

|

£'000 |

£'000 |

£'000 |

|

Cash flows from operating activities |

|

|

|

|

Cash generated from operations |

6,035 |

3,590 |

11,167 |

|

Income tax paid |

(2,110) |

(1,040) |

(1,811) |

|

Net cash generated from operating activities |

3,925 |

2,550 |

9,356 |

|

Cash flows from investing activities |

|

|

|

|

Acquisition of subsidiaries, net of cash acquired |

(989) |

(2,716) |

(10,060) |

|

Purchase of property, plant and equipment |

(3,428) |

(2,463) |

(4,565) |

|

Sale of property, plant and equipment |

75 |

325 |

340 |

|

Purchase of intangible assets |

(860) |

(1,218) |

(1,744) |

|

Interest received |

7 |

8 |

14 |

|

Net cash used in investing activities |

(5,195) |

(6,064) |

(16,015) |

|

Cash flows from financing activities |

|

|

|

|

Drawdown of borrowings |

3,920 |

7,874 |

20,662 |

|

Repayment of borrowings |

(560) |

(1,585) |

(5,474) |

|

Repayment of lease liabilities |

(1,162) |

(794) |

(1,875) |

|

Interest paid |

(1,451) |

(1,112) |

(2,528) |

|

Dividends paid to ordinary shareholders |

(2,272) |

(2,140) |

(3,469) |

|

Net cash (used in) / generated by financing activities |

(1,525) |

2,243 |

7,316 |

|

Net (decrease) / increase in cash |

(2,795) |

(1,271) |

657 |

|

Cash at beginning of the period |

7,198 |

6,622 |

6,622 |

|

Exchange gains / (losses) on cash |

20 |

195 |

(81) |

|

Cash at the end of the period |

4,423 |

5,546 |

7,198 |

Notes to the Group Cash Flow Statement

|

|

|

Half Year to 31 Mar 2026 (Unaudited) |

Half Year to 31 Mar 2025 (Unaudited) |

Full Year to 30 Sep 2025 (Audited) |

|

|

|

£'000 |

£'000 |

£'000 |

|

Profit before income tax from continuing operations |

|

3,322 |

2,868 |

5,327 |

|

Adjustments for: |

|

|

|

|

|

- Amortisation of acquired intangible assets |

|

1,519 |

1,097 |

2,500 |

|

- Amortisation of other intangible assets |

|

654 |

758 |

1,451 |

|

- Loss on disposal of property, plant and equipment |

|

21 |

- |

133 |

|

- Depreciation |

|

3,965 |

4,046 |

8,220 |

|

- Share based payments |

|

150 |

425 |

1,025 |

|

- Release of deferred consideration creditor |

|

- |

- |

(658) |

|

- Non-cash consideration received from customer contracts |

|

- |

- |

(761) |

|

- Amounts claimed under the RDEC |

|

(225) |

(200) |

(391) |

|

- Finance income |

|

(7) |

(8) |

(14) |

|

- Finance costs |

|

1,451 |

1,112 |

2,821 |

|

- Non cash interest charge included in finance costs |

|

109 |

184 |

- |

|

Total adjustments |

|

7,637 |

7,414 |

14,326 |

|

|

|

|

|

|

|

Changes in working capital |

|

|

|

|

|

- Inventories |

|

(1,284) |

(5,299) |

(7,616) |

|

- Trade and other receivables |

|

(6,376) |

(4,884) |

(8,963) |

|

- Trade and other payables |

|

2,736 |

3,491 |

8,093 |

|

Total changes in working capital |

|

(4,924) |

(6,692) |

(8,486) |

|

|

|

|

|

|

|

Cash generated from operating activities |

|

6,035 |

3,590 |

11,167 |

Reconciliation of net cash flow to movements in net debt

|

|

|

Half Year to |

Half Year to |

Full Year to 30 Sep 2025 |

|

|

|

£'000 |

£'000 |

£'000 |

|

Decrease in cash in the period |

|

(2,795) |

(1,271) |

657 |

|

Drawdown of borrowings |

|

(3,920) |

(7,874) |

(20,662) |

|

Repayment of borrowings |

|

2,096 |

2,647 |

7,958 |

|

Changes in net debt resulting from cash flows |

|

(4,619) |

(6,498) |

(12,047) |

|

New leases |

|

(215) |

(414) |

(2,241) |

|

Acquired leases |

|

- |

(1,631) |

609 |

|

Translation differences |

|

(750) |

(830) |

(456) |

|

Non cash movements including leases disposed |

|

(397) |

(347) |

(3,912) |

|

Movement in net debt in the period / year |

|

(5,981) |

(9,720) |

(18,047) |

|

|

|

|

|

|

|

Net debt at start of period |

|

(43,857) |

(25,810) |

(25,810) |

|

Net debt at end of period |

|

(49,838) |

(35,530) |

(43,857) |

Analysis of net debt

|

|

At 1 Oct 2025 |

New leases |

Cash flow |

Exchange movement |

Non-cash movement |

At 31 Mar 2026 |

|

|

£'000 |

£'000 |

£'000 |

£'000 |

£'000 |

£'000 |

|

Cash at bank and in hand |

7,198 |

- |

(2,795) |

20 |

- |

4,423 |

|

|

|

|

|

|

|

|

|

Debt due after one year |

(37,066) |

- |

(3,360) |

(596) |

(27) |

(41,049) |

|

Lease liabilities |

(13,989) |

(215) |

1,536 |

(174) |

(370) |

(13,212) |

|

|

|

|

|

|

|

|

|

Net debt |

(43,857) |

(215) |

(4,619) |

(750) |

(397) |

(49,838) |

Notes to the Interim Report

1. Basis of Preparation

The unaudited Interim Report has been prepared under the historical cost convention as modified by financial assets and financial liabilities at fair value and in accordance with UK adopted International Accounting Standards and with the requirements of the Companies Act 2006 as applicable to companies reporting under those standards.

The Interim Report was approved by the Board of Directors on 2 June 2026. The Interim Report does not constitute statutory financial statements within the meaning of the Companies Act 2006 and has not been audited.

Comparative figures in the Interim Report for the year ended 30 September 2025 have been taken from the Group's audited statutory financial statements on which the Group's auditors, PricewaterhouseCoopers LLP, expressed an unqualified opinion. The comparative figures to 31 March 2025 are unaudited.

The Interim Report will be announced to all shareholders on the London Stock Exchange and published on the Group's website on 2 June 2026. Copies will be available to members of the public upon application to the Company Secretary at Dowlish Ford, Ilminster, Somerset, TA19 0PF.

There were no changes to accounting policies described in the annual financial statements for the year ended 30 September 2025 that had a material effect on the financial statements.

Cash flow projections show that the Group has sufficient funding available to withstand plausible downside scenarios, and therefore the financial statements have been prepared on a going concern basis.

2. Estimates

The preparation of interim financial statements requires management to make estimates and assumptions that affect the application of accounting policies and the reported amounts of assets and liabilities, income and expense. Actual results may differ from these estimates.

In preparing these condensed consolidated interim financial statements, the significant judgments made by management in applying the Company's accounting policies and the key sources of estimation uncertainty were the same as those that applied to the consolidated financial statements for the year ended 30 September 2025.

3. Financial risk management

The Company's activities expose it to a variety of financial risks, market risk (including currency risk, cash flow interest rate risk and price risk), credit risk and liquidity risk.

The interim condensed consolidated financial statements do not include all financial risk management information and disclosures required in the annual financial statements and should be read in conjunction with the Company's annual financial statements as at 30 September 2025. There have been no changes to the risk management policies since the year end.

4. Segmental analysis

|

|

Aerospace & Defence |

Life Sciences / Biophotonics |

Industrial |

Corporate |

Total |

|

For half year to 31 March 2026 |

£'000 |

£'000 |

£'000 |

£'000 |

£'000 |

|

Revenue |

|

|

|

|

|

|

Total revenue |

42,326 |

16,434 |

33,007 |

- |

91,767 |

|

Inter and intra-division |

(6,739) |

(471) |

(2,681) |

- |

(9,891) |

|

External revenue |

35,587 |

15,963 |

30,326 |

- |

81,876 |

|

Divisional expenses |

(30,498) |

(14,809) |

(25,178) |

(379) |

(70,864) |

|

EBITDA¹ |

5,089 |

1,154 |

5,148 |

(379) |

11,012 |

|

EBITDA % |

14.3% |

7.2% |

17.0% |

- |

13.4% |

|

Depreciation and amortisation |

(1,861) |

(548) |

(1,551) |

(659) |

(4,619) |

|

Operating profit / (loss) before amortisation of acquired intangible assets |

3,228 |

606 |

3,597 |

(1,038) |

6,393 |

|

Amortisation of acquired intangible assets |

- |

- |

- |

(1,519) |

(1,519) |

|

Operating profit / (loss) |

3,228 |

606 |

3,597 |

(2,557) |

4,874 |

|

Operating profit / (loss) margin % |

9.1% |

3.8% |

11.9% |

- |

6.0% |

|

Add back non-recurring items |

417 |

136 |

249 |

1,522 |

2,324 |

|

Operating profit / (loss) excluding non-recurring items |

3,645 |

742 |

3,846 |

(1,035) |

7,198 |

|

Adjusted operating profit / (loss) margin % |

10.2% |

4.6% |

12.7% |

- |

8.8% |

|

|

|

|

|

|

|

|

|

Aerospace & Defence |

Life Sciences / Biophotonics |

Industrial |

Corporate |

Total |

|

For half year to 31 March 2025 |

£'000 |

£'000 |

£'000 |

£'000 |

£'000 |

|

Revenue |

|

|

|

|

|

|

Total revenue |

25,147 |

17,760 |

31,463 |

|

74,370 |

|

Inter and intra-division |

(1,681) |

(470) |

(1,341) |

- |

(3,492) |

|

External revenue |

23,466 |

17,290 |

30,122 |

- |

70,878 |

|

Divisional expenses |

(21,385) |

(14,529) |

(25,325) |

418 |

(60,821) |

|

EBITDA¹ |

2,081 |

2,761 |

4,797 |

418 |

10,057 |

|

EBITDA % |

8.9% |

16.0% |

15.9% |

|

14.2% |

|

Depreciation and amortisation |

(1,748) |

(927) |

(1,382) |

(747) |

(4,804) |

|

Operating (loss) / profit before amortisation of acquired intangible assets |

333 |

1,834 |

3,415 |

(329) |

5,253 |

|

Amortisation of acquired intangible assets |

- |

- |

- |

(1,097) |

(1,097) |

|

Operating (loss) / profit |

333 |

1,834 |

3,415 |

(1,426) |

4,156 |

|

Operating (loss) / profit margin % |

1.4% |

10.6% |

11.3% |

- |

5.9% |

|

Add back non-recurring items |

266 |

245 |

391 |

1,097 |

1,999 |

|

Operating (loss) / profit excluding non-recurring items |

599 |

2,079 |

3,806 |

(329) |

6,155 |

|

Adjusted operating (loss)/profit margin % |

2.6% |

12.0% |

12.6% |

- |

8.7% |

¹EBITDA = Earnings before interest, tax, depreciation and amortisation.

All of the amounts recorded are in respect of continuing operations.

4. Segmental analysis continued

Analysis of revenue from continuing operations by destination

|

|

Half year to 31 Mar 2026 (Unaudited) |

|

Half year to 31 Mar 2025 (Unaudited) |

|

|

£'000 |

|

£'000 |

|

United Kingdom |

21,807 |

|

24,064 |

|

North and South America |

34,023 |

|

22,864 |

|

Continental Europe |

16,419 |

|

13,107 |

|

Asia-Pacific |

9,627 |

|

10,843 |

|

|

81,876 |

|

70,878 |

5. Non-underlying items

|

|

|

Half Year to |

Half Year to |

Full Year to |

|

|

|

£'000 |

£'000 |

£'000 |

|

Profit before tax from continuing operations |

|

3,322 |

2,868 |

5,327 |

|

Amortisation of and impairment of acquired intangible assets |

|

1,519 |

1,097 |

2,500 |

|

Restructuring and other costs

|

|

385 |

412 |

3,169 |

|

Acquisition and integration costs |

|

193 |

426 |

995 |

|

Release of deferred contingent consideration |

|

- |

- |

(658) |

|

Site closure costs |

|

- |

64 |

78 |

|

Local employment litigation |

|

227 |

- |

200 |

|

Interest on deferred consideration |

|

108 |

184 |

293 |

|

Adjusted profit before tax |

|

5,754 |

5,051 |

11,904 |

The restructuring costs in the period ended 31 March 2026 relate to non-recurring costs arising from our manufacturing streamlining activities.

6. Tax expense

Analysis of tax charge in the period

|

|

|

Half Year to 31 Mar 2026 |

Half Year to |

Full Year to 30 Sep 2025 (Audited) |

|

|

|

£'000 |

£'000 |

£'000 |

|

Current taxation |

|

|

|

|

|

UK Corporation tax |

|

1,396 |

1,368 |

2,819 |

|

Overseas tax |

|

(94) |

(181) |

(467) |

|

Adjustments in respect of prior year tax charge |

|

- |

- |

257 |

|

Total current tax |

|

1,302 |

1,187 |

2,609 |

|

|

|

|

|

|

|

Deferred tax |

|

|

|

|

|

Origination and reversal of temporary differences |

|

(477) |

(411) |

(161) |

|

Adjustments in respect of prior years |

|

- |

- |

(657) |

|

Total deferred tax |

|

(477) |

(411) |

(818) |

|

|

|

|

|

|

|

Tax expense / (credit) per income statement |

|

825 |

776 |

1,791 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The tax charge for the six months ended 31 March 2026 is based on the estimated effective rate of the tax for the Group for the full year to 30 September 2026. The estimated rate is applied to the profit before tax.

The adjusted effective tax rate on profit from continuing activities is 22.4% (H1 2025: 22.9%).

7. Earnings per share

The calculation of earnings per 20p Ordinary Share is based on the profit for the period using as a divisor the weighted average number of Ordinary Shares in issue during the period. The weighted average number of shares is given below.

|

|

Half Year to |

Half Year to |

Full Year to 30 Sep 2025 |

|

|

No. |

No. |

No. |

|

Number of shares used for basic earnings per share |

27,228,141 |

25,786,397 |

25,897,092 |

|

Dilutive shares |

490,600 |

487,379 |

608,376 |

|

Number of shares used for dilutive earnings per share |

27,718,741 |

26,273,776 |

26,505,468 |

A reconciliation of the earnings used in the earnings per share calculation is set out below:

|

|

Half Year to |

Half Year to |

Full Year to |

|||

|

|

£'000 |

p per |

£'000 |

p per |

£'000 |

p per |

|

Basic earnings per share from continuing operations |

2,497 |

9.2p |

2,092 |

8.1p |

3,536 |

13.7p |

|

Adjustments net of income tax expense: |

|

|

|

|

|

|

|

Amortisation of acquired intangible assets |

1,198 |

4.4p |

863 |

3.3p |

1,969 |

7.6p |

|

Acquisition costs |

167 |

0.6p |

410 |

1.6p |

951 |

3.7p |

|

Site closure costs |

- |

- |

64 |

0.2p |

78 |

0.3p |

|

Restructuring costs |

318 |

1.2p |

331 |

1.3p |

2,882 |

11.0p |

|

Unwind of discount on deferred consideration |

81 |

0.3p |

134 |

0.5p |

220 |

0.8p |

|

Release of deferred consideration creditor |

- |

- |

- |

- |

(658) |

(2.5p) |

|

Litigation costs |

204 |

0.7p |

- |

- |

200 |

0.8p |

|

Total adjustments net of income tax expense |

1,968 |

7.2p |

1,802 |

6.9p |

5,642 |

21.7p |

|

|

|

|

|

|

|

|

|

Adjusted basic earnings per share |

4,465 |

16.4p |

3,894 |

15.0p |

9,178 |

35.4p |

|

|

|

|

|

|

|

|

|

Basic diluted earnings per share |

2,497 |

9.0p |

2,092 |

8.0p |

3,536 |

13.3p |

|

Adjusted diluted earnings per share |

4,465 |

16.1p |

3,894 |

14.8p |

9,178 |

34.6p |

Adjusted earnings per share before amortisation of acquired intangible assets and adjustments has been shown because, in the opinion of the Directors, it more accurately reflects the trading performance of the Group.

8. Dividend

The Directors have declared an interim dividend of 4.9p per share for the half year ended 31 March 2026 (2025: 4.9p).

|

|

Half Year to |

Half Year to |

Full Year to |

|

|

£'000 |

£'000 |

£'000 |

|

Final 2025 dividend: 8.3p per share (Final 2024 dividend paid in 2025: 8.3p) |

2,272 |

2,140 |

2,140 |

|

2025 Interim dividend of 4.9p per share (2024: 4.9p per share) |

- |

- |

1,329 |

|

|

2,272 |

2,140 |

3,469 |

9. Borrowings

|

|

31 March 2026 |

31 March 2025 £000 |

30 September 2025 £'000 |

|

Current: |

|

|

|

|

Leases |

2,214 |

1,881 |

2,234 |

|

|

2,214 |

1,881 |

2,234 |

|

Non-current: |

|

|

|

|

Bank borrowings |

41,049 |

29,604 |

37,066 |

|

Leases |

10,998 |

9,591 |

11,755 |

|

|

52,047 |

39,195 |

48,821 |

|

|

|

|

|

|

Total borrowings |

54,261 |

41,076 |

51,055 |

G&H's primary lending bank is NatWest Bank. The Group's facilities were extended on 12 March 2026 and now comprise a US$70m (£52.9m) dollar revolving credit facility. At 31 March 2026, the balance drawn on the revolving credit facility was US$54.8m (£41.3m) (September 2025: US$50.2m (£37.3m)).

The revolving credit facility is committed until 31 March 2030 and attracts an interest rate of between 1.45% and 1.95% above rates specified by the bank dependent upon the Company's leverage ratio, payable on rollover dates.

The Group's banking facilities are secured on certain of its assets including land and buildings, property plant and equipment and inventory.

Maturity profile of bank borrowings

|

|

31 March 2026 |

31 March 2025 |

30 September 2025 |

|

Between one and five years |

41,049 |

29,604 |

36,536 |

|

|

41,049 |

29,604 |

36,536 |

Maturity profile of lease liabilities

|

|

31 March 2026 |

31 March 2025 |

30 September 2025 |

|

Within one year |

2,874 |

2,442 |

2,926 |

|

Between two and five years |

9,247 |

7,602 |

10,635 |

|

After five years |

3,621 |

3,263 |

3,225 |

|

|

15,742 |

13,307 |

16,786 |

10. Called up share capital

|

|

31 Mar 2026 No. |

30 Sep 2025 No. |

31 Mar 2026 £'000 |

30 Sep 2025 £'000 |

|

Allotted, issued and fully paid Ordinary share of 20p each |

27,370,726 |

27,115,033 |

5,474 |

5,423 |

- ENDS -

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.

Latest directors dealings

- 22 hours ago TotalEnergies SE

- 23 hours ago Bango

- 23 hours ago Zigup

- 23 hours ago PureTech Health

- 23 hours ago Peel Hunt Limited NPV