Half-year Financial Report

Summary by AI BETAClose X

18 December 2025

CyanConnode Holdings plc

("CyanConnode" or the "Company")

Positive H1 Results with Accelerating Smart Metre Roll-out in India Creating a Strong Tail Wind

CyanConnode (AIM: CYAN), a world leader in narrowband radio frequency (RF) mesh networks, announces its unaudited interim results for the six months ended 30 September 2025 (H1 FY 2026).

John Cronin, CEO, commented:

"This has been a successful period for the business. In April, we secured our first Advanced Metering Infrastructure Service Provider (AMISP) contract to deliver a major smart metering rollout in Goa - our largest contract to date - which nearly doubled our contracted order book to £157 million at 30 September 2025. This milestone win has significantly increased our scale and strengthened our ability to win additional AMISP contracts, alongside ongoing subcontracting opportunities. In India alone, our Serviceable Obtainable Market (SOM) is £231 million.

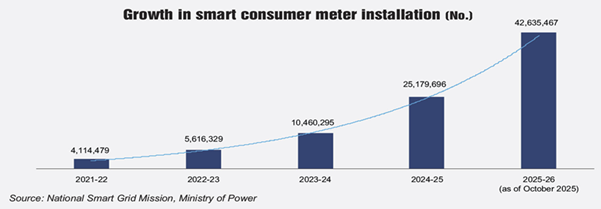

India is our largest market, and the Indian Government remains very focused on reversing approximately $15 billion lost annually to electricity theft and inefficiencies. To address this, the revised national smart metering programme (RDSS), launched in 2022, is now accelerating, as shown in the graph below. This is creating a positive tail wind which is reflected in our revenue performance up by 32% in the period to £7.4 million (over 40% on a constant currency basis).

We also strengthened our financial position by raising $15 million through two convertible loan notes, supporting both working capital and our ability to win further contracts. Outside India, performance remains strong, including winning a £1.2 million cellular gateways order in the Middle East and North Africa.

With 17 live smart metering projects and revenue generation from the Goa project expected to begin in earnest shortly, the business is well-positioned for sustained growth through the remainder of FY 2026 and into FY 2027."

Financial Highlights

· Revenue grew to £7.4m (H1 FY 2025: £5.6m), driven by increased shipments of hardware

· Gross profit of £1.9m (H1 FY 2025: £2.3m), reflecting a lower gross margin of 25% versus 41% in H1 FY 2025, due to lower software and services revenue as a proportion of revenue (8% versus H1 FY 2026 20%) and to lower than usual pricing on certain contracts agreed in anticipation of new higher margin products coming through such as FG28 module, cellular modules and In-Meter Gateways, which have significantly lower costs. The Group is targeting overall project margins of upwards of 35% following commencement of deployments using the new products, with this margin varying across the course of each project (driven by lower margin hardware being shipped in the first two years of a project). With the use of In-Meter Gateways, gateway installation and maintenance costs will be substantially reduced.

· Increase in operating costs from £4.4m in H1 FY 2025 to £5m in H1 FY 2026, driven by £0.9m of foreign exchange losses in translation of accounts

· Operating loss of £3.0m (H1 FY 2025 loss: £2.1m), driven primarily by the £0.9m of foreign exchange losses

· Cash received from customers of £7.4m (H1FY 2025: £7.3m)

· Cash and cash equivalents at end of period £1.6m (FY 2025: £3.7m). In addition, £6 million is held in a fixed deposit at ICICI Bank in London, securing an overdraft facility in India for the same amount.

Operational Highlights

· £70 million AMISP contract won in April 2025 from the Government of Goa

· Under an innovative agreement with a sector specialist multi-national contractor in July, the Goa contract has been fully funded and resourced without any further capital requirements from the Group

· £157 million Group order book as of 30 Sept 2025

· 893,000 Omnimesh Modules were shipped compared with 377,000 in the same period in the prior year, reflecting strong market momentum

· £1.2 million follow-on order secured for cellular gateways in the Middle East and North Africa (MENA) region

· $15 million raised through two convertible loan notes for $7.5 million each supporting the Group's working capital requirements and ability to pursue further contract tenders

· Chair and CEO roles separated with the appointment of Bjorn Lindblom as Non-Executive Chairman increasing Board independence and enabling John Cronin to focus more on his operational role as Group CEO

Post-Period Highlights

· In November, successfully raised $5.25 million through a convertible loan note, to provide additional capital for use as deposits for AMISP contract tenders

· Key operational metrics remain positive, with Q3 2026 shipments of Omnimesh Modules positioning the Group well for sustained growth through FY 2026 and beyond

|

Investor Presentation

· Following completion of Q3 FY 2026 on 31 December 2025, the Company intends to hold an Investor Presentation on the Investor Meet Company platform for shareholders in Q4 FY 2026.

Enquiries:

|

|

About CyanConnode

CyanConnode (AIM:CYAN.L), is a global provider of IoT communication and smart metering solutions. Its comprehensive technology portfolio includes narrowband RF mesh, advanced cellular modules, and hybrid communication platforms, delivering scalable and cost-effective connectivity for smart energy and infrastructure applications.

The Company's flagship Omnimesh platform offers highly reliable, self-forming and self-healing networks, optimised for deployment across diverse geographic and environmental conditions. Complemented by innovations such as long-range RF, in-meter gateways, and AI-enhanced cellular connectivity, CyanConnode provides flexible solutions tailored to evolving utility needs.

CyanConnode's Universal Head-End System (UHES) enables seamless integration across multiple communication technologies, enhancing interoperability and simplifying network management at scale.

As a trusted AMISP and OEM partner, CyanConnode works with utilities, system integrators, and meter manufacturers through a global, vendor-agnostic ecosystem. The Company is playing a central role in the digital transformation of the energy sector, with projects spanning India, Southeast Asia, the Middle East, and Europe.

For more information, please visit www.cyanconnode.com.

CEO's Statement

Introduction

I am pleased to present our results for the first six months. It has been a successful period for the business with the Company's contracted order book standing at £157m at the end of the period. In India the Government's determination to reduce electricity theft and roll-out its national smart metering programme is creating positive trading conditions for CyanConnode, evidenced by the sharp increase in Omnimesh Modules being shipped to customers and the 32% increase in group revenue versus the same period last year. Winning the £70 million AMISP Goa contract and subsequently securing full funding and resourcing for the project may well come to represent an important inflection point for the business marking the start of a period of long-term expansion. To that end, in India alone, the Group is pursuing a mix of potential AMISP and sub-contractor communications projects worth approximately £231 million.

India

Market

The Indian smart metering market, the Company's principal focus, continues to demonstrate strong growth, with over 40 million smart meters deployed across various states as of October 2025.

The government's long-standing target to deploy 250 million smart meters under the Revamped Distribution Sector Scheme (RDSS) remains the primary driver of the market. As of mid-2025, approximately 223.7 million consumer smart meters have been sanctioned under the RDSS.

While the RDSS experienced a slower pace of installation than initially anticipated, and the scheme's completion date has been revised to 2027-28, additional efforts have been made to accelerate progress. The Union Budget 2025-26 allocated approximately £1.32 billion to support ongoing infrastructure upgrades and meter deployments. In addition, the basic customs duty on smart meters was reduced from 25% to 20%, easing the cost burden on both Distribution Companies (DISCOMs) and manufacturers.

Installation rates have improved significantly from an average of 11,000-12,000 meters per day, to a milestone pace of 80,000 meters per day in January 2025, with expectations to reach 100,000 meters per day, as recently reported by the Ministry of Power. The increase in installation and further funding commitments provides a significant opportunity for suppliers, whilst the extended RDSS timeline to 2027-28 provides better medium-term visibility for CyanConnode.

Sub-contractor for smart metering projects

CyanConnode currently has 17 projects where it is acting as a sub-contractor providing smart metering communication systems. During the period, shipments of Omnimesh modules increased sharply to 893,000 compared with 377,000 in the same period last year. This is a clear indicator of operational momentum, reflecting the rate of smart meter installations across our projects.

The Company is well placed to bid for further smart metering projects as a sub-contractor providing communication systems and is targeting an estimated £45 million worth of these project overs the next 18 months.

AMISP (Advanced Metering Infrastructure Service Provider)

In May 2024, CyanConnode India's subsidiary, DigiSmart Networks Private Ltd was successfully empanelled as an AMISP for both RF and cellular, making it eligible to bid for smart metering contracts under the Revamped Distribution Sector Scheme. This was a key milestone for the Group which enabled DigiSmart to win its first AMISP project in April 2025, a circa £70 million contract in Goa, which has been fully funded and resourced through an innovative agreement with a sector specialist multi-national contractor. The project is shortly expected to become revenue generating and be a key contributor to Group sales going forward.

Having established a track record, in November 2025, the Company raised $5.25 million through a convertible loan note to be used to secure Earnest Money Deposits ("EMDs") for AMISP tenders on which DigiSmart intends to bid. EMDs are refundable deposits required when submitting bids under the RDSS, demonstrating a bidder's commitment to proceed with the project if selected. The deposits are typically returned following the tender process, except where a bidder withdraws or fails to complete contractual formalities after being awarded the contract.

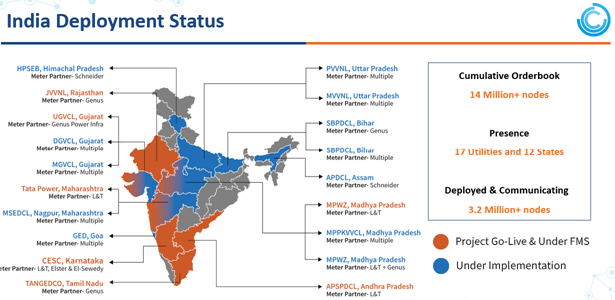

Key Active Projects in India

Source: CyanConnode Holdings plc

MPWZ - 4 (Jabalpur) | AMISP - MCL - one of CyanConnode's largest RF-based smart metering deployments, with over one million smart meters successfully installed and operating on the Omnimesh RF mesh communication network.

MPWZ - Phase 2 | AMISP - IPCL - involves deploying CyanConnode's Omnimesh RF communication network across Indore, Madhya Pradesh, with approximately 320,000 meters installed.

SBPDCL - 1 (South Bihar) | AMISP - Genus - supports the rollout of CyanConnode's Omnimesh RF communication network across South Bihar, with approximately 120,000 meters deployed to date.

SBPDCL - 2 (South Bihar) | AMISP - IntelliSmart - involves deploying CyanConnode's Omnimesh RF communication network to support AMI operations in South Bihar, with approximately 34,000 meters deployed to date.

MSEDCL - Nagpur | AMISP - MCL - involves deploying CyanConnode's Omnimesh RF communication network across the Nagpur region, with approximately 316,000 meters installed to date out.

DGVCL (Dakshin Gujarat) | AMISP - IntelliSmart - involves deploying CyanConnode's Omnimesh RF communication network across parts of South Gujarat, with approximately 277,000 meters deployed to date.

MGVCL (Madhya Gujarat) | AMISP - IntelliSmart - involves deploying CyanConnode's Omnimesh RF communication network across parts of central Gujarat, with approximately 116,000 meters deployed to date.

PVVNL (Paschimanchal Vidyut Vitran Nigam Limited) | AMISP - IntelliSmart - marks the initiation of CyanConnode's Omnimesh RF communication deployment across Western Uttar Pradesh. Approximately 11,000 meters have been deployed to date.

MVVNL (Madhyanchal Vidyut Vitran Nigam Limited) | AMISP - IntelliSmart - represents the initiation of CyanConnode's Omnimesh RF communication deployment across central Uttar Pradesh. Approximately 5,500 meters have been deployed to date.

Goa - Statewide Smart Metering Project | AMISP - Digismart Networks - the Goa statewide smart metering project is a flagship AMI deployment covering approximately 750,000 consumers across the state. DigiSmart Networks Pvt. Ltd., a wholly owned subsidiary of CyanConnode, is implementing the project as the Advanced Metering Infrastructure Service Provider (AMISP), with CyanConnode delivering the Omnimesh communication network and core AMI technology.

Projects under FMS (Field Maintenance Services) - in addition to the active deployments, CyanConnode is currently providing Field Maintenance Services (FMS) for multiple completed and operational smart metering projects across India.

APAC and Middle East

As smart metering adoption progresses in the APAC and Middle Eastern regions, substantial opportunities are emerging for CyanConnode.

In August 2025, the Company announced a follow-on order for a project in the Middle East North Africa ("MENA") region for £1.2 million, which was delivered and revenue fully recognised during the period. The Company continues to pursue near-term opportunities in its Rest of World ("ROW") markets.

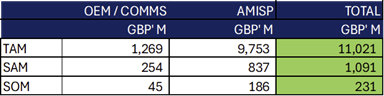

Addressable market in India

Looking ahead, the pipeline of opportunities in India remains substantial. The Total Addressable Market ("TAM") for AMISP projects currently stands at approximately 104.9 million smart meters, representing an estimated value of £9.8 billion, which have been sanctioned but are yet to be awarded. DigiSmart's Serviceable Available Market ("SAM") comprises around 9 million meters, with an estimated value of £837 million. Within this framework, CyanConnode's SAM for just communications (i.e. as a subcontractor) is estimated at approximately £254 million.

CyanConnode's Serviceable Obtainable Market (SOM) over the next 18 months for communications alone (i.e. acting as a subcontractor) is expected to be approximately £45 million. For DigiSmart AMISP, the SOM over the same period is expected to be approximately £186 million, providing a substantial £231 million near-term pipeline to support continued revenue growth.

Based on an estimated market size of approximately 250 million smart meters, the values in the table below represent potential order values and are in addition to the Company's existing contracted order book.

1. TAM (Total Addressable Market) - The total addressable market in India in relation to the Company's products and services. 2. SAM (Serviceable Available Market) - The maximum portion of the TAM that the Company could serve, taking into account practical and operational constraints. 3. SOM (Serviceable Obtainable Market) - The share of the SAM that the Company is targeting to capture within the next approximately eighteen months. 4. AMISP values are based upon the Goa project per-meter price.

Board Changes

In May 2025, the Company made the decision to separate the positions of Chairman and CEO, welcoming independent Non-Executive Director Björn Lindblom to the role of Non-Executive Chairman. John Cronin transitioned from Executive Chairman to Group CEO, allowing him to focus on driving the operational development of the business. This separation enhances the Company's governance, as well as Board independence.

Industry Events

During the period, CyanConnode showcased its solutions internationally at key industry events, including Enlit Africa in Cape Town. The Company also co-sponsored the 8th Annual Conference on Smart Metering in Utilities in New Delhi, and exhibited at Middle East Energy 2025 in Dubai, where it acted as Silver Conference Sponsor at the Leadership Summit.

Outlook

The successful execution of existing projects, positions CyanConnode for a period of sustained growth and market expansion. In H2 2026, the Goa AMISP contract is expected to become revenue generating, which is likely to have a positive impact on trading for the year. Overall, while recognising that the precise timing of revenue recognition remains dependent on project schedules, the Board is encouraged by the Group's strong contracted order book standing at £157 million at the period end and pipeline visibility.

Financial review

Key figures

|

|

H1 FY 2026 £'000 |

H1 FY 2025 £'000 |

% Change |

|

Revenue |

7,443 |

5,629 |

+ 32% |

|

Gross profit |

1,859 |

2,336 |

- 20% |

|

Operating costs |

(4,978) |

(4,424) |

- 13% |

|

Other operating income |

134 |

- |

+100% |

|

Operating loss |

(2,985) |

(2,088) |

- 43% |

|

EBITDA |

(2,658) |

(1,901) |

- 40% |

|

Adjusted EBITDA |

(1,894) |

(1,597) |

- 19% |

|

Cash |

1,625 |

3,714 |

- 56% |

|

Basic and diluted loss per share |

0.86p |

0.71p |

+ 21% |

Revenue, Gross Margin and Operating Costs

Revenue for H1 FY 2026 increased compared to the revenue for the same period of FY 2025, driven largely by increased deployments (893,000 modules shipped in H1 FY 2026 compared to 377,000 in the same period of FY 2025). Reduction in gross margin percentage from 41% in H1 FY 2025 to 25% in H1 FY 2026 (FY 2025: 35%) was partly due to the decreased software and services revenue as a proportion of total revenue and partly due to lower than usual pricing on certain contracts which were agreed to in anticipation of the Company's new product suite. Margins will improve substantially once the Company commences shipping of its new products such as FG28 module, cellular modules and In-Meter Gateways, which have significantly lower costs. We are targeting overall project margins of upwards of 35% following commencement of deployments using the new products, with this margin varying across the course of each project (driven by more lower margin hardware being shipped in the first two years of the project). With the use of In-Meter Gateways, gateway installation and maintenance costs will be substantially reduced.

An increase in operating costs from £4.4m in H1 FY 2025 to £5m in H1 FY 2026 was driven by £0.9m of foreign exchange losses partly as a result of translation of accounts. Operating loss of £3m (H1 FY 2025 loss: £2.1m) was also driven by the £0.9m of foreign exchange losses

Cash

Cash and cash equivalents at end of period was £1.6m (FY 2025: £3.7m), excluding £6 million held in a fixed deposit at ICICI Bank in London, securing an overdraft facility in India for the same amount.

During the period the Company raised $15 million through two convertible loan notes for $7.5 million each supporting the Group's working capital requirements and ability to pursue further contract tenders. A further $5.25 million was raised from the same investor after period end to secure Earnest Money Deposits ("EMDs") for AMISP tenders on which DigiSmart intends to bid.

Accounts receivable

A total of £7.4m cash was collected from customers during the period (compared to £7.3m for the same period in FY 2025), and a further £1.6m since the period end. In the period, our non-current trade receivables such as contract assets, reported in the non-current assets part of the balance sheet, increased to £6.0m (FY 2025: £3.3m), where revenue has been recognised in accordance with IFRS 15, and will be paid for over the period of the contract. The remainder of trade receivables included in non-current assets related to accrued income from contracts. Approximately 23% of cash collection during H1 FY 2026 related to trade receivables from FY 2025 and a further 17% of FY 2025 trade receivables has been collected since period end.

Consolidated income statement

|

|

Note |

|

|

Unaudited 6 months to 30 September 2025 £000 |

Unaudited 6 months to 30 September 2024 £000 |

Audited 12 months to 31 March 2025 £000 |

|

|

Continuing operations |

|

|

|

|

|

|

|

|

Revenue |

|

|

|

7,443 |

5,629 |

14,177 |

|

|

Cost of sales |

|

|

|

(5,584) |

(3,293) |

(9,239) |

|

|

Gross profit |

|

|

|

1,859 |

2,336 |

4,938 |

|

|

Other operating costs |

|

|

|

(4,978) |

(4,424) |

(9,053) |

|

|

Other operating income |

|

|

|

134 |

- |

268 |

|

|

Operating loss |

|

|

|

(2,985) |

(2,088) |

(3,847) |

|

|

|

|

|

|

|

|

|

|

|

Amortisation and depreciation |

|

|

|

417 |

187 |

396 |

|

|

Share based payments |

|

|

|

(226) |

(24) |

220 |

|

|

Inventory impairment |

|

|

|

- |

5 |

17 |

|

|

Impairment of intangible assets |

|

|

|

- |

- |

- |

|

|

Foreign exchange losses/(gains) |

|

|

|

900 |

323 |

393 |

|

|

Adjusted EBITDA |

|

|

|

(1,894) |

(1,597) |

(2,821) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Finance income |

|

|

|

98 |

- |

216 |

|

|

Financing costs |

|

|

|

(187) |

(33) |

(106) |

|

|

Loss before tax |

|

|

|

(3,074) |

(2,121) |

(3,737) |

|

|

Tax credit |

|

|

|

- |

- |

(88) |

|

|

Loss for the period |

|

|

|

(3,074) |

(2,121) |

(3,825) |

|

|

Loss per share (pence) |

|

|

|

|

|

|

|

|

Basic |

3 |

|

|

(0.86) |

(0.71) |

(1.17) |

|

|

Diluted |

3 |

|

|

(0.86) |

(0.71) |

(1.17) |

|

Consolidated statement of comprehensive income

Derived from continuing operations and attributable to the equity owners of the Company

|

|

Unaudited 6 months to 30 September 2025 £000 |

Unaudited 6 months to 30 September 2024 £000 |

Audited 12 months to 31 March 2025 £000 |

|

|

Loss for the period |

(3,074) |

(2,121) |

(3,825) |

|

|

Exchange differences on translation of foreign operations |

(280) |

(311) |

(234) |

|

|

Total comprehensive income for the year |

(3,354) |

(2,432) |

(4,059) |

|

Consolidated statement of financial position

|

As at

|

Unaudited 30 September 2025 £000 |

Unaudited 30 September 2024 £000 |

Audited 31 March 2025 £000 |

|

Non-current assets |

|

|

|

|

Intangible assets |

4,639 |

4,179 |

4,529 |

|

Goodwill |

1,930 |

1,930 |

1,930 |

|

Property, plant and equipment |

251 |

182 |

188 |

|

Right of use asset |

310 |

412 |

363 |

|

Other financial assets (note 5) |

1,425 |

49 |

443 |

|

Trade and other receivables (note 4) |

6,101 |

3,326 |

5,500 |

|

Total non-current assets |

14,656 |

10,078 |

12,953 |

|

Current assets |

|

|

|

|

Inventories |

3,241 |

1,652 |

2,290 |

|

Trade and other receivables (note 4) |

15,595 |

8,270 |

11,745 |

|

R&D tax credit receivables |

491 |

229 |

367 |

|

Other financial assets (note 5) |

6,000 |

- |

2,500 |

|

Cash and cash equivalents |

1,625 |

3,714 |

3,332 |

|

Total current assets |

26,952 |

13,865 |

20,234 |

|

Total assets |

41,608 |

23,943 |

33,187 |

|

Current liabilities |

|

|

|

|

Trade and other payables |

(9,488) |

(6,076) |

(9,902) |

|

Short-term borrowing (note 6) |

(6,244) |

(158) |

(6,731) |

|

Corporation tax liabilities |

(889) |

(477) |

(956) |

|

Lease liabilities |

(119) |

(113) |

(118) |

|

Total current liabilities |

(16,740) |

(6,824) |

(17,707) |

|

Net current assets |

10,212 |

7,041 |

2,527 |

|

Non-current liabilities |

|

|

|

|

Lease liabilities |

(184) |

(305) |

(245) |

|

Deferred tax liability |

(28) |

(252) |

(11) |

|

Long-term borrowing (note 6) |

(13,022) |

- |

- |

|

Other payables |

(125) |

(83) |

(135) |

|

Total non-current liabilities |

(13,359) |

(640) |

(391) |

|

Total liabilities |

(30,099) |

(7,464) |

(18,098) |

|

Net assets |

11,509 |

16,479 |

15,089 |

|

Equity |

|

|

|

|

Share capital |

7,178 |

7,178 |

7,178 |

|

Share premium account |

84,894 |

84,152 |

84,411 |

|

Own shares held |

(3,525) |

(3,259) |

(3,525) |

|

Share option reserve |

923 |

1,388 |

1,632 |

|

Translation reserve |

(574) |

(371) |

(294) |

|

Accumulated losses |

(77,387) |

(72,609) |

(74,313) |

|

Total equity being equity attributable to owners of the Company |

11,509 |

16,479 |

15,089 |

|

|

|

|

|

Consolidated statement of changes in equity

|

|

Share Capital £000 |

Share Premium Account £000 |

Own Shares Held £000 |

Share Option Reserve £000 |

Translation Reserve £000 |

Retained Losses £000 |

Total Equity £000 |

|

|

Balance at 31 March 2024 |

5,982 |

80,196 |

(3,611) |

1,412 |

(60) |

(70,488) |

13,431 |

|

|

Loss for the period |

- |

- |

- |

- |

- |

(2,121) |

(2,121) |

|

|

Other comprehensive income for the period |

- |

- |

- |

- |

(311) |

- |

(311) |

|

|

Total comprehensive income for the period |

- |

- |

- |

- |

(311) |

(2,121) |

(2,432) |

|

|

Issue of share capital |

1,196 |

3,956 |

352 |

- |

- |

- |

5,504 |

|

|

Credit to equity for share options |

- |

- |

- |

(24) |

- |

- |

(24) |

|

|

Total transactions with owners |

1,196 |

3,956 |

352 |

(24) |

- |

- |

5,480 |

|

|

Balance at 30 September 2024 |

7,178 |

84,152 |

(3,259) |

1,388 |

(371) |

(72,609) |

16,479 |

|

|

Loss for the period |

- |

- |

- |

- |

- |

(1,704) |

(1,704) |

|

|

Other comprehensive income for the period |

- |

- |

- |

- |

77 |

- |

77 |

|

|

Total comprehensive income for the period |

- |

- |

- |

- |

77 |

(1,704) |

(1,627) |

|

|

Issue of share capital |

- |

(8) |

(352) |

- |

- |

- |

(360) |

|

|

Disposal of shares |

- |

267 |

86 |

- |

- |

- |

353 |

|

|

Debit to equity for share options |

- |

- |

- |

244 |

- |

- |

244 |

|

|

Total transactions with owners |

- |

259 |

(266) |

244 |

- |

(1,704) |

237 |

|

|

Balance at 31 March 2025 |

7,178 |

84,411 |

(3,525) |

1,632 |

(294) |

(74,313) |

15,089 |

|

|

Loss for the period |

- |

- |

- |

- |

- |

(3,074) |

(3,074) |

|

|

Other comprehensive income for the period |

- |

- |

- |

- |

(280) |

- |

(280) |

|

|

Total comprehensive income for the period |

- |

- |

- |

- |

(280) |

(3,074) |

(3,354) |

|

|

Transfer of warrants lapsed |

- |

483 |

- |

(483) |

- |

- |

- |

|

|

Credit to equity for share options |

- |

- |

- |

(226) |

- |

- |

(226) |

|

|

Total transactions with owners |

- |

483 |

- |

(709) |

- |

- |

(226) |

|

|

Balance at 30 September 2025 |

7,178 |

84,894 |

(3,525) |

923 |

(574) |

(77,387) |

11,509 |

|

|

|

|

|

|

|

|

|

|

|

Consolidated cash flow statement

|

|

Unaudited 6 months to 30 September 2025 £000 |

Unaudited 6 months to 30 September 2024 £000 |

Audited 12 months to 31 March 2025 £000 |

||||||

|

Net cash outflow from operating activities (Note 5) |

(9,081) |

(1,801) |

(5,540) |

||||||

|

Investing activities |

|

|

|

||||||

|

Interest received |

5 |

- |

16 |

||||||

|

Purchases of property, plant and equipment |

(108) |

(69) |

(121) |

||||||

|

Disposals of property, plant and equipment |

|

- |

15 |

||||||

|

Purchases of intangible assets |

(333) |

(495) |

(927) |

||||||

|

Sale of other financial assets |

- |

2 |

- |

||||||

|

Net cash used in investing activities |

(436) |

(562) |

(1,017) |

||||||

|

Financing activities |

|

|

|

||||||

|

Interest paid on borrowings |

(178) |

- |

(81) |

||||||

|

Proceeds on sales of shares |

|

- |

353 |

||||||

|

Money put on deposit as security |

(4,482) |

- |

(2,943) |

||||||

|

Cash inflow from borrowings |

13,267 |

- |

5,000 |

||||||

|

Cash outflow from borrowings |

(5,245) |

- |

- |

||||||

|

Cash inflow from directors' loan |

- |

- |

1,060 |

||||||

|

Cash outflow from directors' loan |

- |

- |

(660) |

||||||

|

Cash net inflow/(outflow) from debt factoring |

- |

158 |

- |

||||||

|

Loan repayment |

- |

- |

- |

||||||

|

Capital repayments of lease liabilities |

(54) |

(52) |

(111) |

||||||

|

Interest paid on lease liabilities |

(10) |

(13) |

(25) |

||||||

|

Proceeds on issue of shares |

- |

5,383 |

5,383 |

||||||

|

Share issue costs |

- |

(231) |

(239) |

||||||

|

Net cash from financing activities |

3,298 |

5,245 |

7,737 |

||||||

|

Net increase/(decrease) in cash and cash equivalents |

(6,219) |

2,882 |

1,180 |

||||||

|

Effects of exchange rate changes on cash and cash equivalents |

- |

49 |

38 |

||||||

|

Cash and cash equivalents at beginning of period |

2,001 |

783 |

783 |

||||||

|

Cash and cash equivalents at end of period |

(4,218) |

3,714 |

2,001 |

||||||

|

|

|

|

|

||||||

|

Analysis of changes in net /cash debt |

|

|

|

|

|

|

|||

|

|

At 1 April 2024 |

Cash flow |

At 1 April 2025 |

Cash flow |

At 30 September 2025 |

|

|||

|

For the 6 months ended 30 September 2025 |

£'000 |

£'000 |

£'000 |

£'000 |

£'000 |

|

|||

|

|

|

|

|

|

|

|

|||

|

Cash and cash equivalents |

783 |

2,549 |

3,332 |

(1,706) |

1,626 |

|

|||

|

Bank overdraft |

- |

(1,331) |

(1,331) |

(4,513) |

(5,844) |

|

|||

|

Cash and cash equivalents |

783 |

1,218 |

2,001 |

(6,219) |

(4,218) |

|

|||

|

|

|

|

|

||||||

Notes to the Accounts

1. Basis of Preparation

The interim financial statements are for the six months ended 30 September 2025. They do not include all the information required for full annual financial statements and should be read in conjunction with the consolidated financial statements of the Group for the year ended 31 March 2025, which have been filed at Companies House. The Group's auditor issued a report on those financial statements that was unqualified and did not contain a statement under section 498(2) or section 498(3) of the Companies Act 2006, however, the auditor's report emphasized the uncertainty around the Group's ability to continue as a going concern.

These interim financial statements have been prepared in accordance with accounting policies which are consistent with the measurement requirements of UK-adopted International Accounting Standards. These financial statements have been prepared under the historical cost convention.

These interim financial statements have been prepared in accordance with the accounting policies adopted in the last annual financial statements for the year to 31 March 2025. The accounting policies have been applied consistently throughout the group for the purpose of preparing these interim financial statements and are expected to be followed throughout the year ending 31 March 2026.

2. Going Concern

To assess the ability of the Group to continue as a going concern, the Directors have prepared a business plan and cash flow forecast for the period to 31 March 2027 which, together, represent the Directors' best estimate of the future development of the Group. The forecast contains certain assumptions, the most significant of which are the level and timing of sales and the timing of customer payments. These detailed cashflow scenarios include Letters of Credit which have been secured from the customers against contracts and convertible loan notes recently secured.

The Group's business activities, together with the factors likely to affect its future development, performance and position, have been considered in depth as part of the Directors' assessment of the Group's ability to continue as a going concern. The Directors have reviewed detailed trading forecasts for H2 of FY 2026. At 30 September 2025 the Group had cash reserves of £1.6 million (31 March 2025: £3.3 million). Based on detailed cash flow provided to the Board to cover the period to 31 March 2027, there is sufficient cash for a period of at least 12 months from the date of approval of this report, with forecasts prepared in line with its standard operating model. The Company continues to discuss potential working capital funding facilities with banks and other financial institutions, particularly in India. The Company has been approached with alternative sources of finance, to support growth, such as secured loans, which it could accept should such a requirement arise. It also continues to discuss options of taking equity into its subsidiary in India.

The Company received a R&D tax credit of £340,858 from HMRC in October 2025. An advance loan of £400,000 received in February 2025 was in place against this R&D tax credit and was repaid in October 2025 out of the proceeds of the tax credit received.

Notwithstanding the material uncertainties described above, which may cast significant doubt on the ability of the Group to continue as a going concern, on the basis of sensitivities applied to the cash flow forecast, the directors have a reasonable expectation that the company can continue to meet its liabilities as they fall due, for a period of at least 12 months from the date of approval of this report.

3. Loss per Share

The calculation of the basic and diluted loss per share is based on the following data:

|

|

Unaudited 6 months to 30 September 2025 |

Unaudited 6 months to 30 September 2024 |

Audited 12 months to 31 March 2025 |

|

Loss for the purposes of basic loss per share being net loss attributable to equity holders of the parent (£000) |

(3,074) |

(2,121) |

(3,825) |

|

Weighted average number of ordinary shares for the purposes of basic and diluted loss per share |

358,174,092 |

297,056,605 |

326,247,246 |

|

Loss per share (pence) |

(0.86) |

(0.71) |

(1.17) |

Notes to the Accounts continued

The denominations used are the same as those detailed above for both basic and diluted earnings per share from continuing operations. However, in accordance with IAS 33 "Earnings Per Share", potential ordinary shares are only considered dilutive when their conversion would decrease the profit per share or increase the loss per share from continuing operations attributable to the equity shareholders.

4. Trade and Other Receivables

|

|

Unaudited 6 months to 30 September 2025 |

Unaudited 6 months to 30 September 2024 |

Audited 12 months to 31 March 2025 |

|

|

£000 |

£000 |

£000 |

|

Non-current |

|

|

|

|

|

|

|

|

|

Contract assets |

4,029 |

2,812 |

4,055 |

|

Other non-current assets |

2,072 |

514 |

1,445 |

|

Trade and other receivables |

6,101 |

3,326 |

5,500 |

|

Current |

|

|

|

|

|

|

|

|

|

Trade receivables: amount receivable for the sale of goods and services[1] |

9,737 |

6,882 |

7,731 |

|

Allowance for expected credit losses |

(159) |

(127) |

(160) |

|

|

9,578 |

6,755 |

7,571 |

|

Contract assets |

1 |

854 |

1,309 |

|

Other receivables |

5,934 |

603 |

2,686 |

|

Prepayments |

82 |

58 |

179 |

|

Trade and other receivables |

15,595 |

8,270 |

11,745 |

5. Other financial assets

|

|

Unaudited 6 months to 30 September 2025 |

Unaudited 6 months to 30 September 2024 |

Audited 12 months to 31 March 2025 |

|

|

£000 |

£000 |

£000 |

|

Non-current |

|

|

|

|

|

|

|

|

|

Bank securities |

1,425 |

- |

443 |

|

Other financial assets |

1,425 |

- |

443 |

Notes to the Accounts continued

|

Current |

|

|

|

|

|

|

|

|

|

Bank securities |

6,000 |

- |

2,500 |

|

Other financial assets |

6,000 |

- |

2,500 |

CyanConnode Holdings Plc has entered an agreement with ICICI Bank UK Plc to provide a Letter of Credit to ICICI Bank India to guarantee the working capital facility for CyanConnode Private Limited. A charge has been registered with Companies House for CyanConnode Holdings Plc whereby ICICI Bank UK Plc has first fixed charge over the account balances and all other rights, titles and interest of CyanConnode Holdings Plc in and to the deposit account.

6. Borrowings

|

|

Unaudited 6 months to 30 September 2025 |

Unaudited 6 months to 30 September 2024 |

Audited 12 months to 31 March 2025 |

|

|

£000 |

£000 |

£000 |

|

Long-term borrowings |

|

|

|

|

|

|

|

|

|

Other loans |

13,022 |

- |

- |

|

Long-term borrowings |

13,022 |

- |

- |

|

Short-term borrowings |

|

|

|

|

|

|

|

|

|

Loan from director |

400 |

158 |

400 |

|

Other loans |

- |

- |

5,000 |

|

Bank overdraft |

5,844 |

- |

1,331 |

|

Short-term borrowings |

6,244 |

158 |

6,731 |

During the period, CyanConnode Holdings received $15 million from Smart Sustainability Solutions Limited (the "Lender"), split into two convertible loan notes of $7.5 million each. The first $7.5 million was received in May 2025 and the second $7.5 million was in July 2025. The parties have executed Convertible Loan Note instruments under which the Lender has advanced these amounts to CyanConnode Holdings Plc. The first $7.5 million was used to repay the £5 million short-term loan, received in March 2025 from Axia Investments Limited.

Interest will be charged at 7% per annum. Repayment of the first $7.5 million is due at the earliest of April 2028 and no later than April 2030, after which the Lender is entitled to convert the shares into equity if the loan is not repaid. Repayment of the second $7.5 million is due to be repaid at the earliest date of July 2028 and no later than July 2030 after which the Lender is entitled to convert the loan into equity if not repaid.

In February 2025, the Company received advance loans for £400,000 in aggregate from two Directors against its R&D tax credit. These loans were repaid in October 2025 out of the funds received from HMRC for the group's R&D tax credit. No loans are currently outstanding to Directors of the Company.

In March 2025, the Company received a short-term, unsecured loan for £5m from its shareholder Axia Investments Limited to support near-term opportunities to grow the business. Interest is charged at 15% per annum. The term of the loan was set at three months with the option to extend a further three months under certain circumstances at the Company's discretion. The loan was repaid in June 2025.

Notes to the Accounts continued

7. Reconciliation of Operating Loss to Operating Cash Flows

|

|

Unaudited 6 months to 30 September 2025 £000 |

Unaudited 6 months to 30 September 2024 £000 |

Audited 12 months to 31 March 2025 £000 |

|

Operating loss for the period |

(2,985) |

(2,088) |

(3,847) |

|

Adjustments for: |

|

|

|

|

Depreciation of property, plant and equipment |

45 |

55 |

128 |

|

Amortisation of intangible assets |

319 |

75 |

157 |

|

Depreciation on right of use assets |

53 |

57 |

111 |

|

Share-option payment expense |

(226) |

(24) |

220 |

|

R&D tax credit |

- |

(224) |

- |

|

Operating cash flows before movements in working capital |

(2,794) |

(2,149) |

(3,231) |

|

(Increase)/decrease in inventories |

(951) |

34 |

(621) |

|

(Increase)/decrease in receivables |

(4,727) |

1,980 |

(3,688) |

|

(Decrease)/increase in payables |

(425) |

(2,378) |

1,500 |

|

Cash outflows from operating activities |

(8,897) |

(2,513) |

(6,040) |

|

Income taxes received |

(184) |

712 |

500 |

|

Net cash outflow from operating activities |

(9,081) |

(1,801) |

(5,540) |

8. Post Balance Sheet Event

In November 2025 the Company entered into a further US$5.25 million unsecured convertible loan note agreement (the "Loan Note") with Smart Sustainability Solutions Limited (the "Lender"), a Middle Eastern climate technology company, that is a wholly owned subsidiary of a publicly listed, Abu Dhabi based global investment group. The Loan Note follows two similar agreements with the Lender completed earlier this year, which together totalled US$15.0 million.

Interest will be charged at 7% per annum, payable on redemption or at the time of conversion. The term of the Loan Note is 60 months, and it can be repaid at any time between the date of agreement and 60 days from date of issuance at the election of the Company.

If the Loan Note has not been redeemed during its term, the principal, together with any accrued but unpaid interest, may be converted after the 60-month maturity date into equity in CyanConnode or one or more of its subsidiaries, associates, or group companies. Conversion is at the election of the Lender but subject to mutual agreement with the Company regarding the conversion price and the entity or entities into which it may convert. Any conversion into CyanConnode equity shall not result in a breach of Rule 9 of the UK Takeover Code.

9. Interim Results

The Group's Interim Results report will be available for download on the Group's website, www.cyanconnode.com. The report will not be posted to shareholders.

[1] £1,916k of trade receivables has been collected via invoice discounting and reflected as short-term borrowings in the balance sheet as required by IFRS. The net value of trade receivables in the current section of the balance sheet after taking this into account is therefore £9,737k less £1,916k = £7,821k (FY 2025 £6,882k less £158k = £6,724)

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.

Latest directors dealings

- 2 days ago Workspace Group

- 2 days ago Talon Resources Plc

- 2 days ago Vodafone Group

- 2 days ago Synthomer

- 2 days ago Ondo Insurtech